Joined February 2021

- Tweets 1,334

- Following 1,128

- Followers 2,923

- Likes 14,088

471 Photos and videos

Pinned Tweet

13 Oct 2025

I’m sharing my first investment article on the Finnish forum Sijoitustieto - covering $LMND.

Happy to hear your views and feedback - more articles to come in the future.

Summary:

I see $LMND as a high-risk, high-beta investment case, with its story centered on the company’s ability to disrupt the traditional insurance market over the coming years. The numbers show early signs that the fundamentals are moving in the right direction. During H2, I’ll be closely watching the development of IFP (in-force premium). As the business scales through growth investments, I believe the company can reach positive EBITDA next year.

sijoitustieto.fi/sijoitusart…

13 Oct 2025

Sijoitustietoon saatiin uusi erinomainen kirjoittaja @ValueByMarkus . Ensimmäisessä artikkelissaan hän analysoi vakuutusalan disruptoijaa, Lemonadea.

”…ensimmäinen puhtaasti diginatiivi vakuutusyhtiö, joka lupasi mullistaa alan mm. tekoälyn avulla.”

sijoitustieto.fi/sijoitusart…

4

5

124

50,791

Jun 13

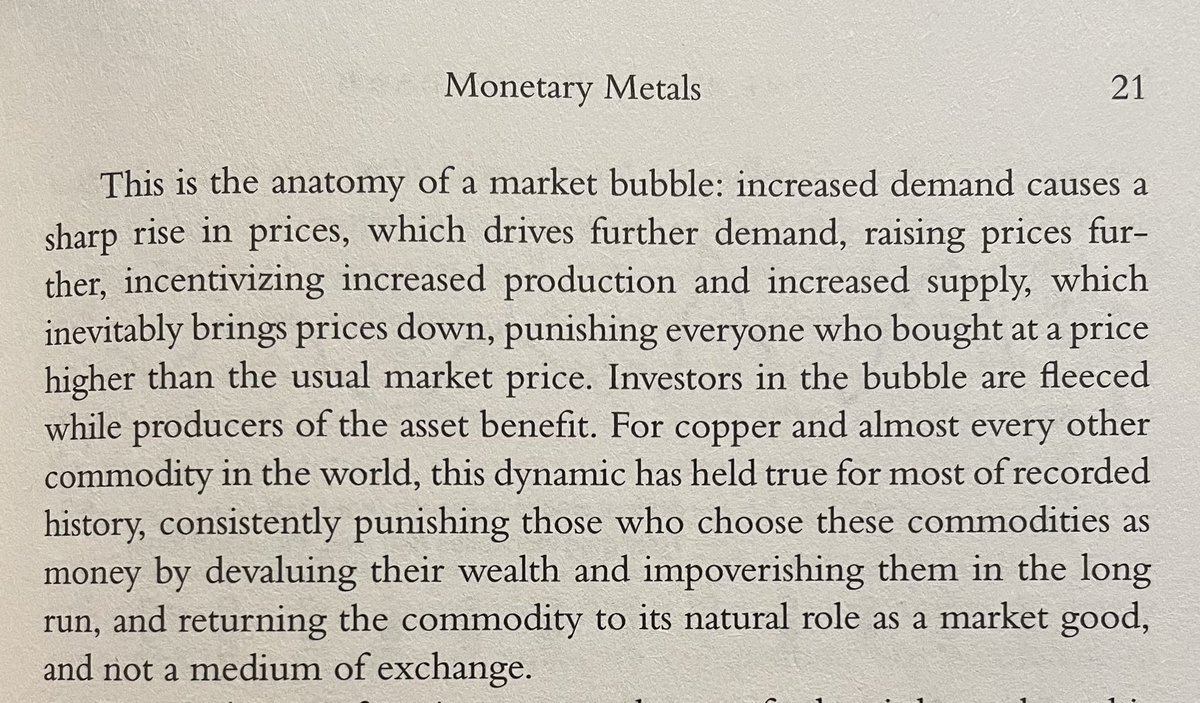

Great summary of simple supply-demand economics.

The quote focuses on metals, but the same dynamic applies across most markets:

1. ↑ Prices

2. ↑ Production

3. ↑ Supply

4. ↓ Prices

Over time, high prices incentivize their own destruction.

One reason why I don’t own commodities and keep my portfolio >100% allocated (including leverage) fully to equities.

Businesses can grow through innovation, pricing power, capital allocation, and productivity gains. A barrel of oil or a ton of copper can’t.

Jun 8

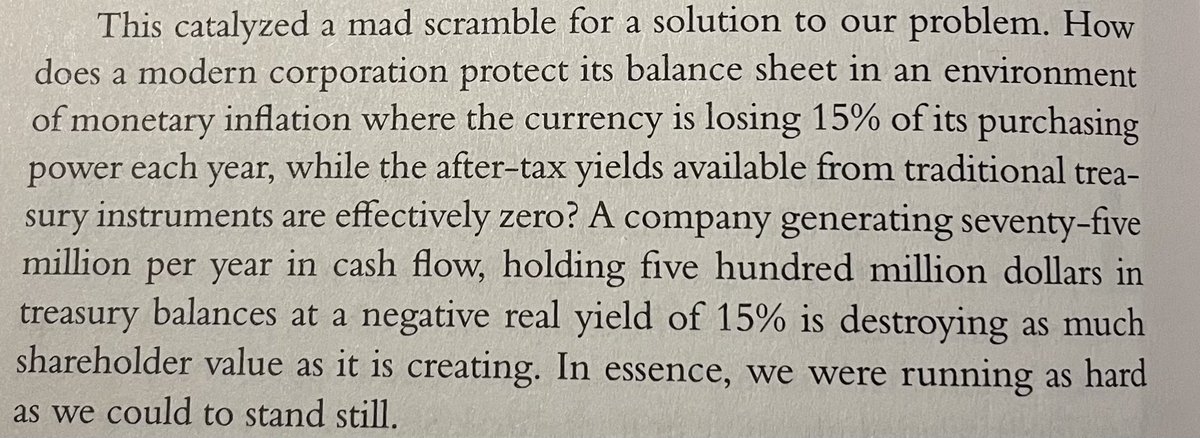

Started reading The Bitcoin Standard to understand the topic better.

It’s somewhat ironic that the foreword was written by @saylor in March 2021, given that Strategy is now sitting on more than 10 B$ of unrealized Bitcoin losses.

Managing a company’s treasury operations is a crucial part of running a business, and my starting hypothesis going into the book is skepticism toward the crypto treasury business model.

Happy to be proven wrong.

1

5

994

Jun 11

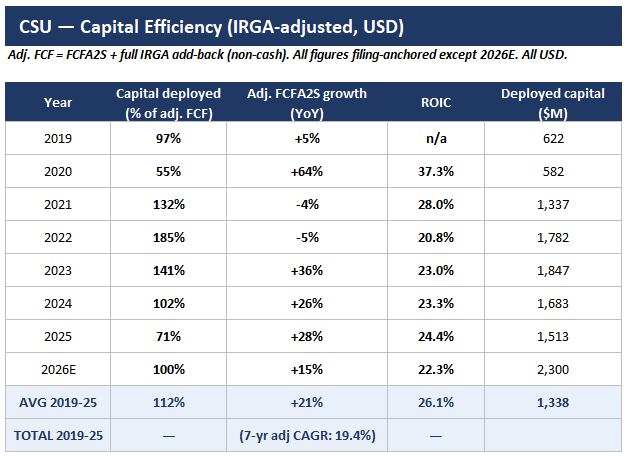

I would estimate that $CSU would deploy even more than ~100% of its FCF into M&A, maybe even closer to 3B$.

With 20% ROIC, the current valuation of EV/FCF under 20x is still not demanding, even after a ~30% rally over the past month. That assumes software is not disrupted away, as the market is now hinting.

Probably a quite attractive environment to buy software businesses when you have the firepower, even if private valuations have not come down as much as in the public markets.

8

1,789

Jun 11

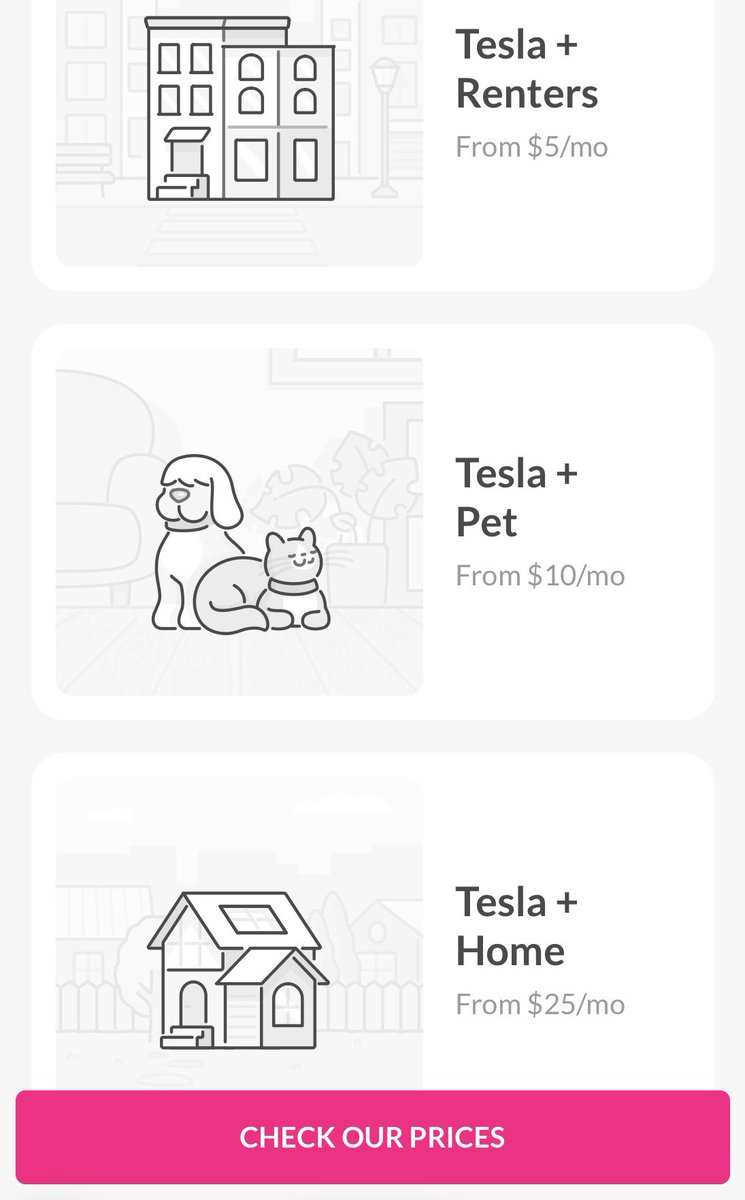

Recent $LMND expansions in June: the renters product is now live in North Dakota and Montana.

The autonomous car offering is also live in Indiana. Solid execution, in line with the management storyline.

Indiana Tesla drivers can now get 50% off every mile driven with Full Self-Driving (Supervised) turned on.

This is exactly in line with the $LMND playbook, scaling in-force premium (IFP) both through customer growth and higher IFP per customer. Cross-sell is being offered in a very attractive way for a (younger) target customer base.

While I don’t foresee Tesla FSD contributing meaningfully to total IFP yet, it is very exciting to follow the progress and observe the first-mover advantage versus more traditional car insurers relying only on basic telematics.

I expect the number of customers to continue growing 20–25% YoY, while IFP per customer should increase 5–10%, driven by cross-sell, especially into car and pet.

17 Oct 2025

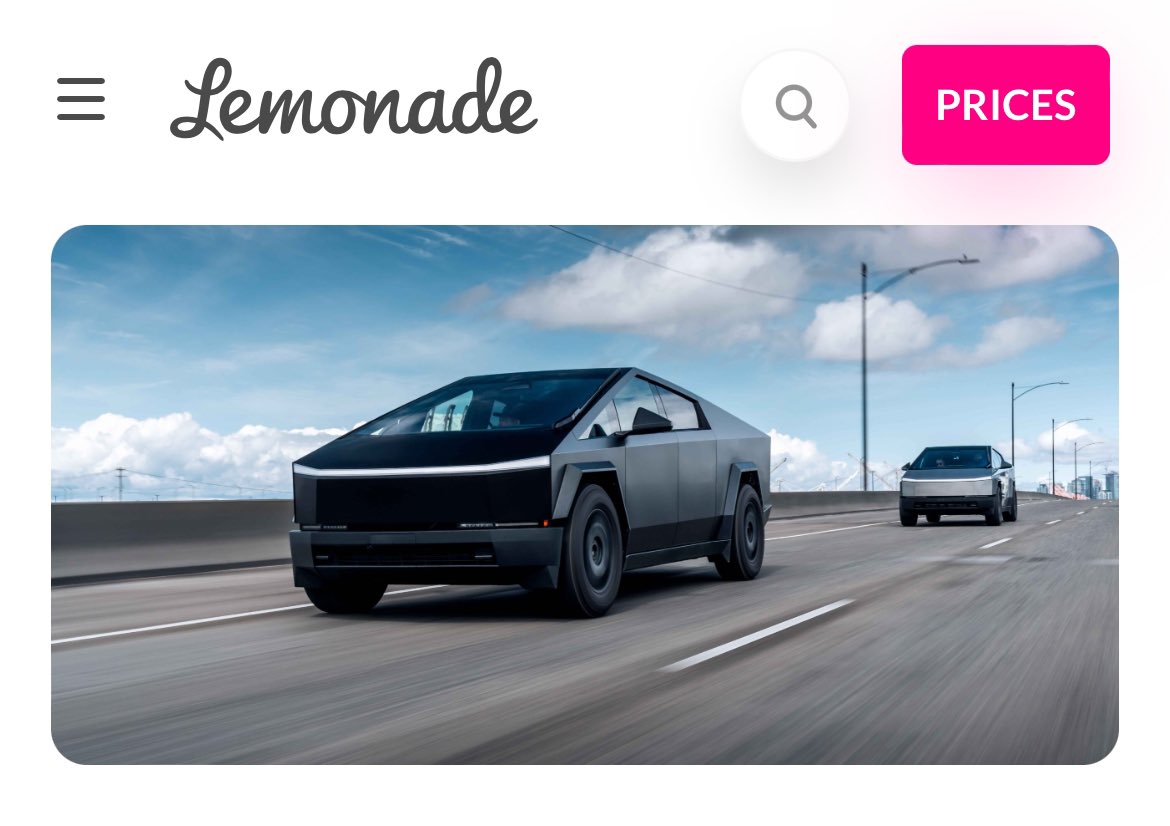

Lemonade is upgrading its Car insurance game. By directly integrating with @Tesla vehicles, they’re eliminating the need for a UBI device in their Pay-Per-Mile product.

What this means strategically:

1. Lower costs, higher scale potential

No hardware or shipping means lower CAC and operational complexity. Tesla drivers get cheaper policies, Lemonade keeps more margin.

2. Better data, smarter pricing

Tesla’s API delivers richer driving behavior info than traditional UBI devices. More accurate risk assessment - more precise pricing and rewards for safe (potentially FSD) driving.

3. Stronger moat, seamless customer experience

A seamless Tesla experience may make Lemonade the go-to choice for EV owners. Switching friction rises when insurance is integrated directly into the car ecosystem, versus legacy players.

4. Optional upside to growth

While Tesla drivers are still a niche for Lemonade, this positions the company to capture a premium, tech-savvy customer segment first. Could be a small but strategic lever in gross-selling to other insurance products, and expand API capabilities for other EVs.

This isn’t just a product tweak, it’s a subtle but meaningful step toward smarter, lower-cost, data-driven insurance that could compound Lemonade’s competitive edge in EV insurance. Interesting to hear more about this in the Q3 report.

$LMND

1

35

4,299

Jun 11

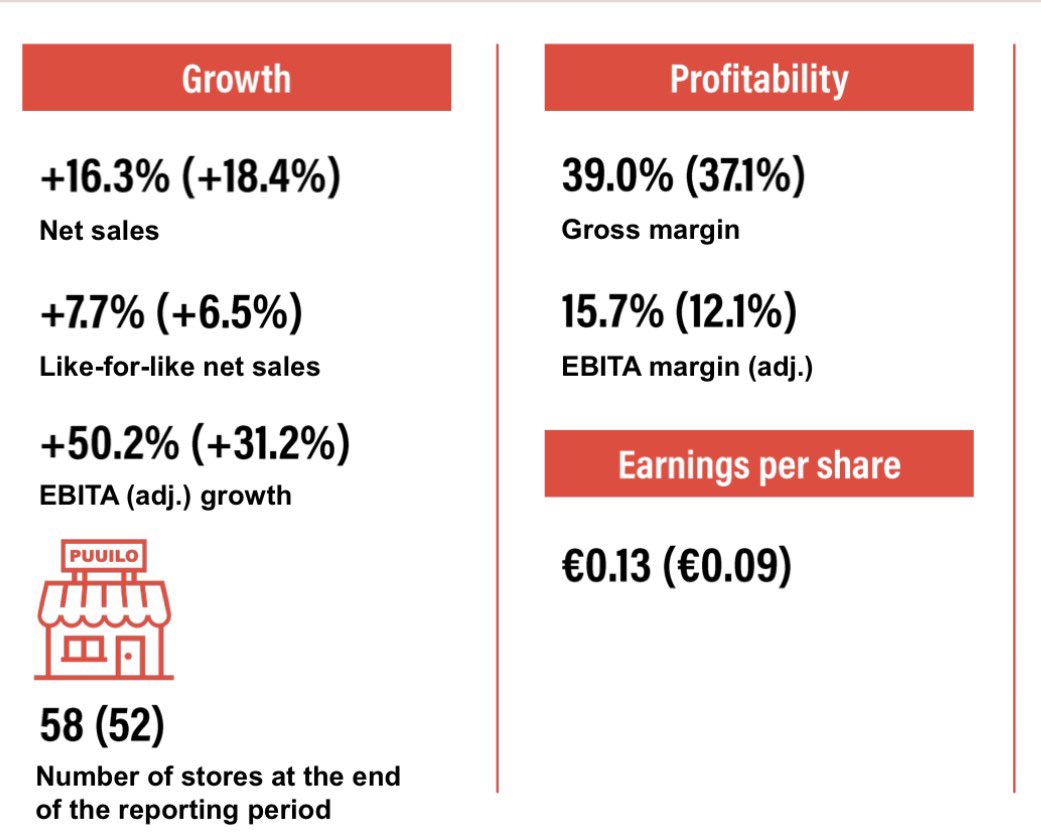

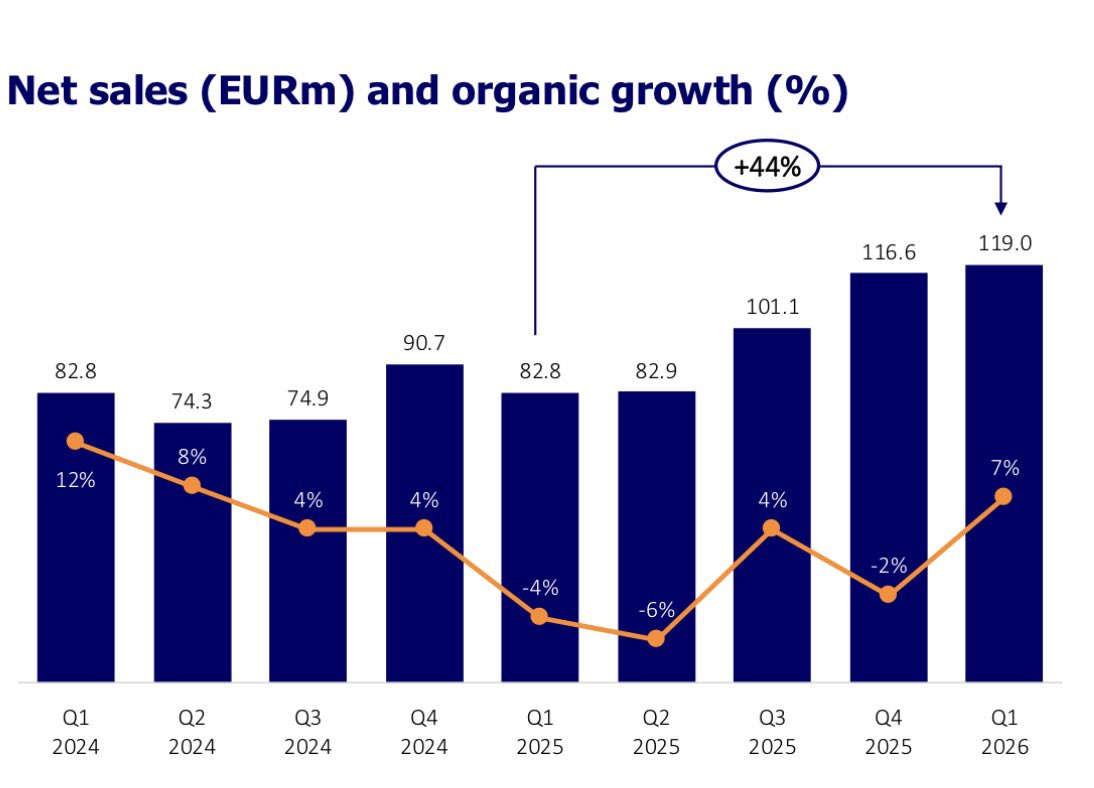

One of the most impressive retail stories in the Nordics right now is $PUUILO

Q1 was strong across the board:

Revenue: 103 M€ ( 15% YoY)

Grosd margin: 39.0% (37.1%)

Comparable sales: 7%

EBITA margin: 15.7% (12.1%)

Growth was not driven by new stores ( 6 stores YoY, and currently 58) alone. Existing stores continued to perform strongly while profitability improved at the same time.

That’s often a sign of a retailer with genuine competitive advantages rather than a business simply benefiting from a cyclical tailwind. Especially when considering the management comments:

"The average basket size increased slightly relative to the comparison period, despite consumer confidence remaining at a low level in Finland"

The Sweden expansion gets most of the attention. But the core Finnish business is already demonstrating why Puuilo has been one of the best-performing Nordic retailers in recent years.

Mr. Market is also pricing in the solid execution and business quality, and with the current valuation of ~18x EV/EBIT 2026e, I’m not too thrilled about the estimated risk/return profile at current levels, while I really like the biz quality.

1

2

40

4,053

Jun 11

Time to lock in for the next five-plus weeks and enjoy international football.

I definitely don’t recommend betting, and I’ll be keeping my money in the equity markets, but it’s still interesting to see the market’s view on the favourites.

Naturally, given the amount of money involved in the sports betting market, the pricing should be relatively efficient.

That said, I see Spain and Argentina as the favourites (with a pinch of personal country bias), while France also looks extremely strong on paper.

The “black horse” countries I could see making a deep run this year are Ecuador, Norway, and Japan. With many third-placed teams advancing to the knockout stage, these three collective and well-organized teams could surprise a lot of expectations.

5

683

Jun 8

Started reading The Bitcoin Standard to understand the topic better.

It’s somewhat ironic that the foreword was written by @saylor in March 2021, given that Strategy is now sitting on more than 10 B$ of unrealized Bitcoin losses.

Managing a company’s treasury operations is a crucial part of running a business, and my starting hypothesis going into the book is skepticism toward the crypto treasury business model.

Happy to be proven wrong.

Feb 12

I have nothing against BTC and could even see myself owning it at some point.

But when I read the future assumptions like:

“After 10 years at a 25% Bitcoin CAGR…”

I’d rather lean short than long.

Eventually leveraging the balance sheet at a 10% cost of capital, relying on financial engineering and assuming the underlying asset will sustainably outperform that hurdle that’s where it gets uncomfortable.

The bull case for $MSTR is valid if BTC performs.

But I hope investors understand the embedded risks, especially now that the market has started to price some of them in.

5

2,106

Jun 8

Admicom just issued a profit warning $ADMCM

2026 ARR growth guidance was cut from 6–12% to 3–10%, while revenue growth guidance was lowered from 5–10% to 2–6%. Profitability guidance was left unchanged at 31–36% adjusted EBITDA.

Management says the new growth strategy is "progressing well", but the growth-accelerating initiatives are not delivering benefits as quickly as expected in the current market environment.

"The company's share value has decreased significantly compared to the beginning of 2026. The valuation levels of unlisted companies have not changed to the same extent, which makes value creation through acquisitions more challenging at the moment."

Excuse me, what?

I understand if you want to use your own stock as an M&A tool, but assuming the deals would be executed with cash / debt, I don’t see the company’s share price as an issue.

That said, it does reinforce the view that private SaaS valuations have not come down nearly as brutally as those of publicly traded companies.

Is this a temporary delay in realizing the benefits of the strategy, or evidence that Admicom path back to >15% organic ARR growth wont be realistic?

8 Oct 2025

Talking about the annual profit warning season:

Admicom issues guidance downgrade.

The Finnish SaaS company $ADMCM cut its 2025 ARR and revenue growth outlook as the construction market recovery stalls.

"The recovery of the construction market has been delayed."

ARR growth: now 6–10% (prev. 8–14%)

Revenue growth: 5–8% (prev. 6–11%)

EBITDA margin: 31–33% (prev. 31–36%)

Bankruptcies and weak customer growth are hitting churn and usage levels, while internal restructuring still hasn’t boosted sales or product dev pace.

Falling rates in Europe should eventually support construction, but the recovery seems delayed, likely not before 2026.

Until then, it’s a tough operating environment, though we’ve seen some positive execution elsewhere, like $TEKOVA, showing that selective resilience is still possible.

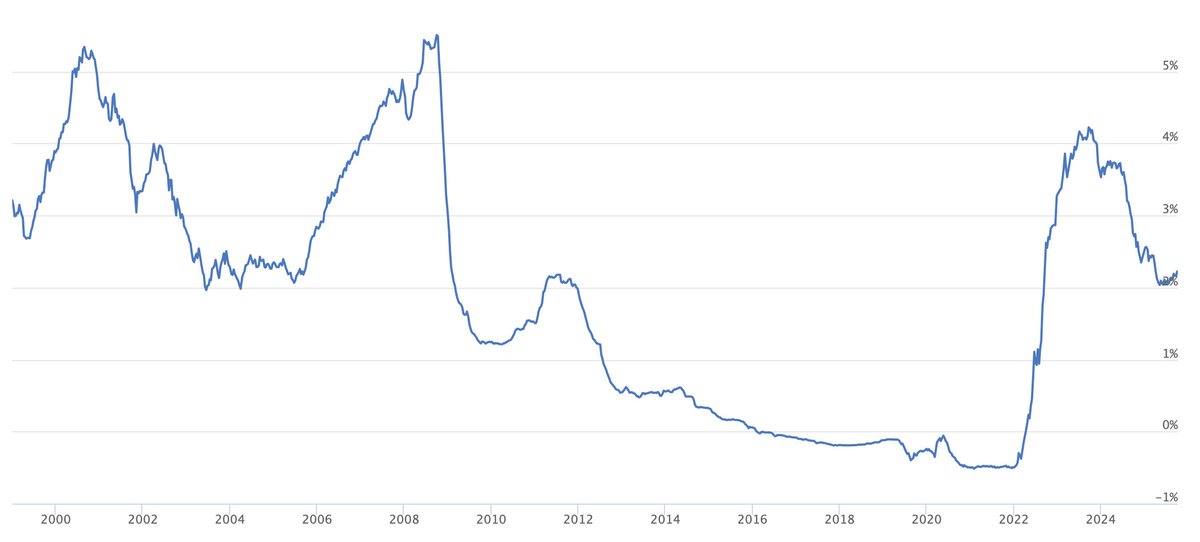

Euribor 12 months:

2

1

13

2,393

22 Sep 2024

📚 Kicking off my book thread! 📚 Join me as I share the books that shaped my mind and took me on unforgettable journeys. Let's dive into the pages together! #BookThread

4

8

31

6,020

Apr 11

39/x

The Almanack by @naval

9.5/10

Naval’s core idea is simple but underestimated. Wealth and happiness are skills, not outcomes and both can be systematically built.

A few key takeaways:

Leverage is the force multiplier

Code, media, and capital allow you to scale decisions without scaling time. That’s where asymmetry comes from.

Judgment is the ultimate asset

In a world of leverage, one good decision can outweigh years of incremental work.

Play long-term games with long-term people.

And finally. His framing of happiness is almost Stoic. educe desires instead of chasing more outcomes.

A great one, and highly recommended.

1

4

873

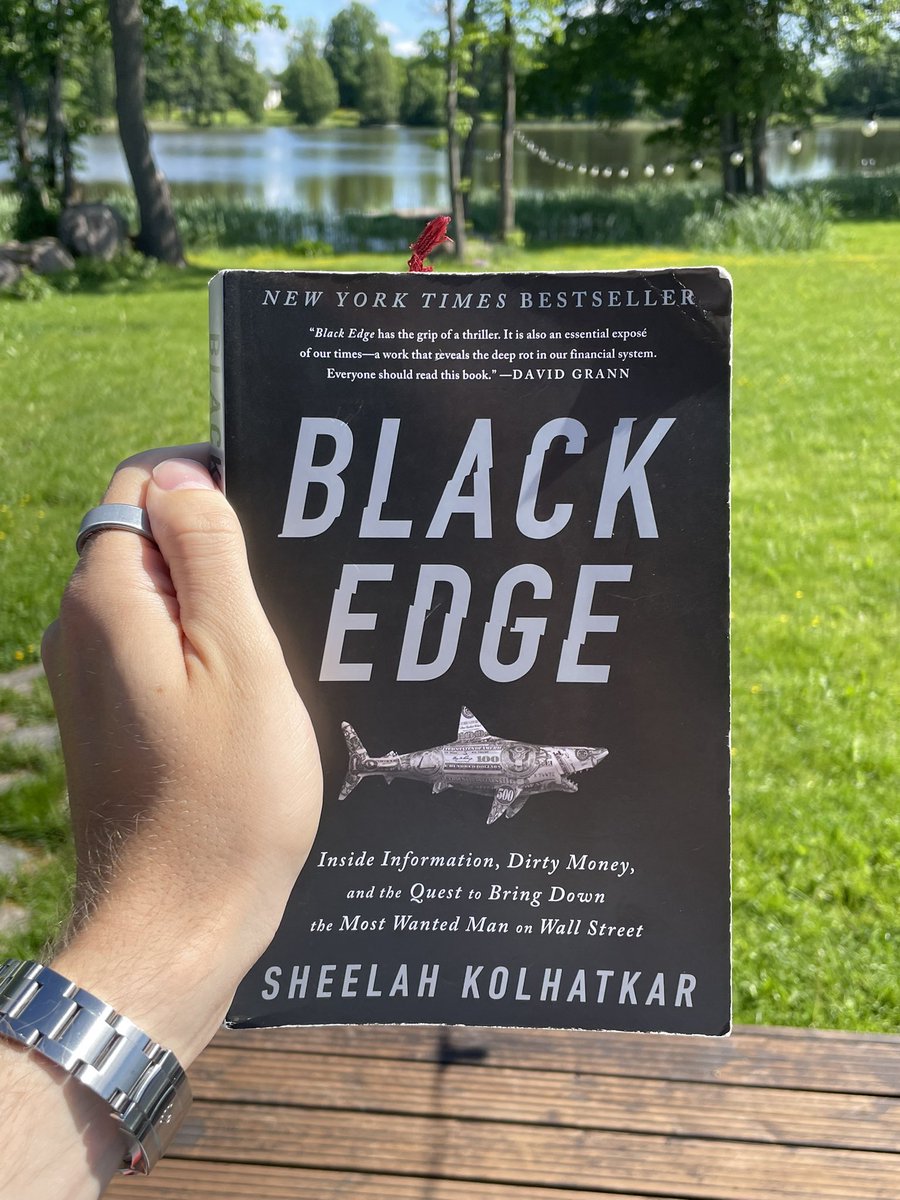

Jun 7

40/x

Black Edge by @sheelahk

9/10

The real-life story that inspired the TV series Billions wasn’t fiction.

The story of hedge fund manager Steven A. Cohen and the insider trading investigations with SAC capital and SEC.

Information is valuable. Exclusive information is priceless.

Many of the smartest people on Wall Street (Hedge fund business) spent enormous energy chasing incremental informational advantages rather than understanding businesses.

The people involved rarely looked like criminals. They looked like ambitious, intelligent professionals operating in environments where incentives gradually distorted judgment.

A fascinating look into hedge funds, behavioral psychology, incentives, and the constant search for an edge. Highly recommended.

1

2

471

Jun 1

Jensen has a point, but it’s important to keep in mind that these companies, his “partners and friends” are also the direct customers buying the GPUs.

That said, I broadly agree with the view. In software, as long as companies make the right strategic decisions leaning into agentic capabilities from technical infrastructure to pricing models and operating models, this could be a strong moment for stock pickers to selectively buy software names.

My main AI-native software horse is $LMND, but I see many other interesting names and valuations in the current market.

5

985

Jun 1

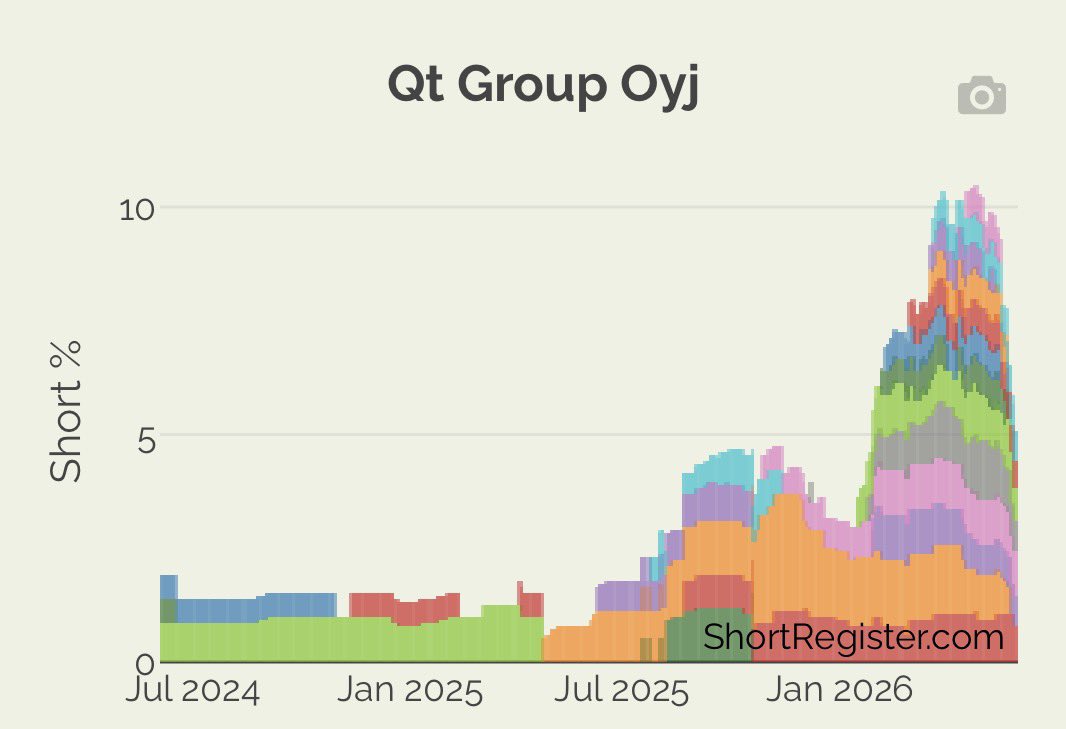

$QTCOM is up ~60% from the April lows, while short positions have decreased from 10% to ~5% of shares outstanding.

Q1 indicated a potential turnaround after market expectations were reset to rock-bottom levels.

At the same time, the major shareholder / insider, Ingman family office has been adding meaningful stakes.

Even with weaker 2026 profitability due to IAR integration and cost-cutting initiatives, 2026 EV/EBIT could still be around 16x in my estimates.

Fair value still appears reasonable in my view, assuming profitability trends upward with the organic growth outlook into 2027 and beyond.

Apr 20

$QTCOM to undergo an operational reorg to enhance efficiency.

They will cut up to 200 FTEs globally (close to 20% of the workforce), aiming to deliver approximately €20M in annual cost savings starting in 2027.

IAR acquisition and integration synergy benefits are being harvested, although I would estimate that a significant portion of the savings is coming from elsewhere.

While the reorg and cost focus were expected, the scale is much larger than I anticipated. It will be interesting to follow how this impacts the growth outlook, as the sales organization will likely also be trimmed.

Given the 2025 EBIT of ~€42M, the scale of the cost measures is significant. It will be particularly interesting to hear more detail and reasoning from management, especially regarding where the FTE reductions will occur.

13

3,292

May 28

Anthropic valuation looks something like this. What wild outcome even with a huge dilution, while I think they will close the year with close to 100B$ ARR.

2021 ~$0.5B (Series A)

2022 ~$4B

2024 ~15B

2025 (Mar) ~$61.5B

2025 (Sep) ~$183B

2026 (Feb) ~$380B

2026 (May) ~$965B

May 28

We've raised $65 billion in Series H funding at a $965 billion post-money valuation, led by @AltimeterCap, Dragoneer, @Greenoaks, and @sequoia.

This investment will help us advance our research and expand our capacity to meet growing demand for Claude.

1

9

1,163

May 28

And I’m sure their CFO has been rather busy lately.

I highly recommend the recent podcast, hope to hear more from him in the future.

May 15

One of the best podcasts I’ve listened to so far this year on AI & Tech.

What a great and clear communicator Anthropic CFO Krishna Rao is. I’d love to hear more of his insights, he balances the opportunity, benefits, and risks exceptionally well.

A core insight for me was the trade-off in compute deployment:

Buy too much with massive capex = out of business.

Buy too little and fail to meet demand = your models fall behind and you’re out of business.

Also, how to allocate compute between internal use, serving customers, and training next-generation models.

open.spotify.com/episode/5aq…

2

763

May 27

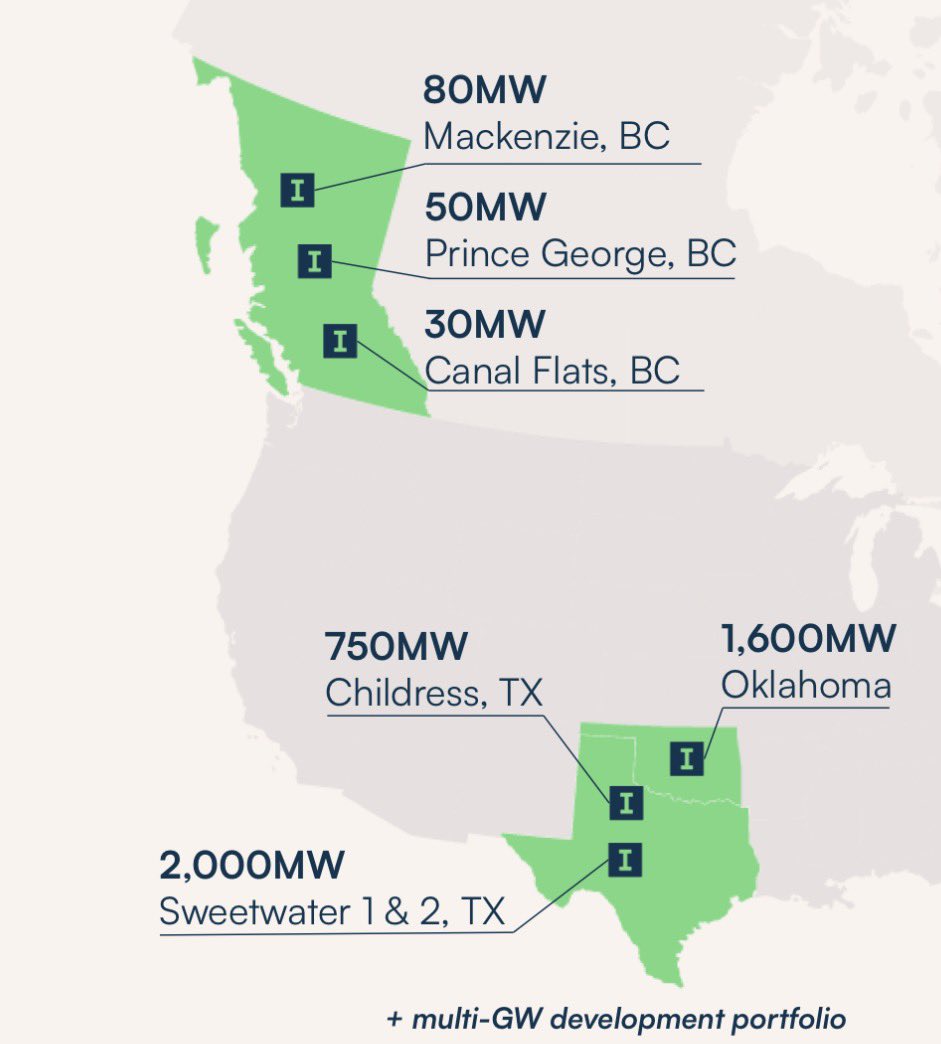

$IREN raising the YE ARR guidance from 3.7 B$ to 4.4 B$.

Solid execution recently, especially the Sweetwater site energization, strategic acquisitions, the $NVDA partnership, and the recent Dell air-cooled Blackwell agreement, has been rewarded by the market, and in my view, for good reason.

After a volatile start to the year, the stock is now up ~60% YTD and more than doubled from the April lows.

It would be tempting to trim the position after this kind of price movement, but I still feel the story is early and continue to hold with potential future catalysts ahead increasing the value of the business.

Apr 18

Interesting insights on potential catalysts around $IREN

What I’m watching most in the near term is the Sweetwater 1 energization.

I would expect to see the site energized by late April, bringing ~1.4 GW of capacity online.

To put that into perspective, this is more than the output of an average US nuclear power plant.

Delivering within the communicated timeline would also add credibility and, more importantly, demonstrate valuable operational know-how in building efficient, high-quality power-to-compute infrastructure.

As mentioned, this would also position $IREN well for potential commercial agreements with (hyperscaler) customers looking to access large-scale compute capacity.

Given the expected wave of major AI IPOs (OpenAI, Anthropic) and the rapid progress of models like Claude, driving the application layer of AI (performance, unit-cost), I remain confident that the structural demand drivers are intact.

As a practical anecdote from my work in the financial sector: AI is at the center of all major transformation initiatives, with usage (even at the token level) and capability building growing at an exponential pace.

Great takes by @Agrippa_Inv , as usual.

1

4

43

5,120

May 27

Now he doubled down with an additional ~600 k$ $NOK purchase.

Even for a C-level executive 1 M$ is already a significant statement of conviction. At the current ~90 B$ market cap, there are already quite a lot of positive assumptions baked in.

I'm still not convinced on r/r.

May 25

$NOK senior executive Owczarek Konstanty (Chief Business Development Officer) bought a meaningful ~500 k$ stake.

I didn’t expect insider buying at these valuation levels, but they likely have good visibility into the pipeline. Selling can indicate many things, but buying usually indicates just one.

I hope I’m wrong, but for me $NOK current valuation is far from an attractive risk/reward, with EV/EBIT at ~30x and so far limited realized top-line growth, with analyst estimates implying only ~5% annual growth for the coming years.

17

4,713

May 26

$RACE stock down ~5% following the new EV release, Luce.

Easy to say the market and many car fans were not impressed with the reveal.

Former Ferrari chairman Luca Cordero di Montezemolo summarized the sentiment well:

“If I said what I really think, I’d harm Ferrari. We’re risking the destruction of a myth. I’m very sorry about that. I hope they at least remove the Prancing Horse from that car.”

The interior was already controversial when it leaked earlier, but imo the exterior design is the biggest issue here.

Interesting to follow how legacy car makers navigate the EV transition.

In my opinion, Porsche has done a much better job with the Taycan, which is one of the few EVs I would genuinely consider buying myself.

1

9

1,752

May 25

$NOK senior executive Owczarek Konstanty (Chief Business Development Officer) bought a meaningful ~500 k$ stake.

I didn’t expect insider buying at these valuation levels, but they likely have good visibility into the pipeline. Selling can indicate many things, but buying usually indicates just one.

I hope I’m wrong, but for me $NOK current valuation is far from an attractive risk/reward, with EV/EBIT at ~30x and so far limited realized top-line growth, with analyst estimates implying only ~5% annual growth for the coming years.

May 15

Howard Marks, one of the investors I admire most, reduced his $NOK position by ~40%.

Even if $NOK is the “next AI bottleneck opportunity,” the current valuation still doesn’t justify the risk/reward, in my opinion.

x.com/valuebymarkus/status/2…

1

15

11,174

May 24

While I respect @chamath and enjoy @theallinpod , I can’t stop thinking about how overvalued and overheated the SpaceX IPO will be.

As Chamath has said, the IPO will be a great moment to “take chips off the table,” and if I were on the cap table, I’d want to do the same at a ~1.5-2T$ valuation.

Imo it’s wild that future narratives around space data centers, colonizing other planets, e.g., are already stretching valuation expectations to ~100x P/S (LTM) at this scale.

The exit liquidity might learn a hard lesson, and while retail will surely be interested, I’m genuinely wondering which institutional players would step in beyond the passive funds.

May 24

Chamath Lays Out the Case for SpaceX at $2 Trillion

– Starlink: the most important internet infra project since the internet itself

– Rockets: underlying platform that allows everything else to happen

– AI: apps top layer, datacenter bottom layer

– The Elon Flywheel: operating leverage ➡️ investment ➡️ competitive moat ➡️ capital moat ➡️ technology moat ➡️ execution/learning moat

– Potential Tesla merger down the road

– Elon’s premium for being “the guy” right now

@chamath:

“ If I'm asking myself, ‘Chamath, how do I underwrite SpaceX at $2T?’

Here's the basic math that I would do.

Last year it did $18-19 billion. It'll probably do $25-30 billion this year. So I'm buying this thing at a fairly costly premium, right?

So what am I buying?

I'm buying probably the most important internet infrastructure project that's happened since the internet itself. That's going to scale to hundreds of millions of users, and the reason that's going to scale to hundreds of millions of users is it's just very useful, and it's just going to become cheaper and cheaper and cheaper. So that's number one.

I'm buying a delivery infrastructure, I think over time, GDP plus 10, GDP plus 15, kind of a grower. So good business, valuable business, but it's the underlying platform that allows everything else to happen.

And then I'm buying an AI business, which will be at the top level the apps, but at the bottom layer all the compute capability.

So I suspect what happens is next year it's probably $40-45 billion. And then the year after that it probably doubles again, so then I'm buying it at 20x revenue.

And you would say, ‘Well, why can you buy a company like this on revenue versus earnings and cash flow?’

And I think the reason is because what the revenue does is it gives him the operating leverage to go and invest in all of these other businesses that ultimately consolidate his differentiation and his competitive moat, because what he creates is a capital moat that then accelerates a technology moat, that then accelerates an execution and a learning moat.

And that flywheel, when it starts to spin very quickly, and you would say, ‘Hey, hold on a second. It's probably spinning quickly now.’ I would say we're at the beginning of the beginning.

He still has all these disparate assets. I still don't like the fact that Tesla's over here, and as I've told you, that will get merged in.

And now you have this incredible corpus of physical capability, movement of all kinds, X, Y, and Z, right? That thing will look very cheap, I think, in a few years.

And he has this one thing that nobody else, if you look at the big CEOs, who steps on stage where you're always curious, ‘Okay, what has he got up his sleeve?’ You know, the Steve Jobs, ‘Oh, and one more thing.’ He's the guy. Whether you like him or you hate him, he's the guy, and there's a premium that is well-deserved that comes with that.”

1

4

1,036

May 24

Very solid start for $AUROORA

The numbers are solid, and especially the organic growth of ~12% was a positive surprise.

The Swedish-style serial acquirer model is gaining more traction in Finland.

$BOREO has continued its turnaround after a very tough few years, and a potential economic rebound in Finland could provide additional tailwinds.

$RELAIS has also reiterated its M&A-driven strategy, with a focus across the Nordics and Baltics.

These acquirers have also been hit hard simply by being part of the Nordic small-cap segment, and any mean reversion there could provide additional upside to valuations.

May 22

$AUROORA 🇫🇮 Finnish serial acquirers first earnings are out and looking pretty strong all around.

12% organic growth, which is solid in the sluggish Finnish economy ( 41% total growth). Margins improved, ROCE stable.

Still fairly cheap vs peers (12-ish x LTM EV/EBITA)

1

15

2,367

May 24

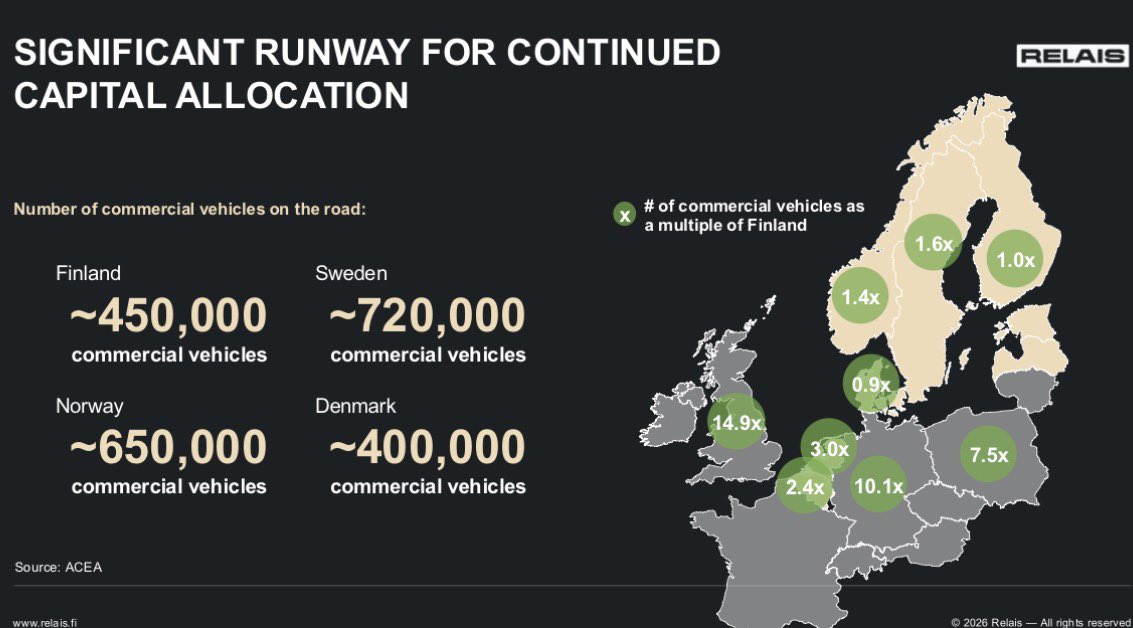

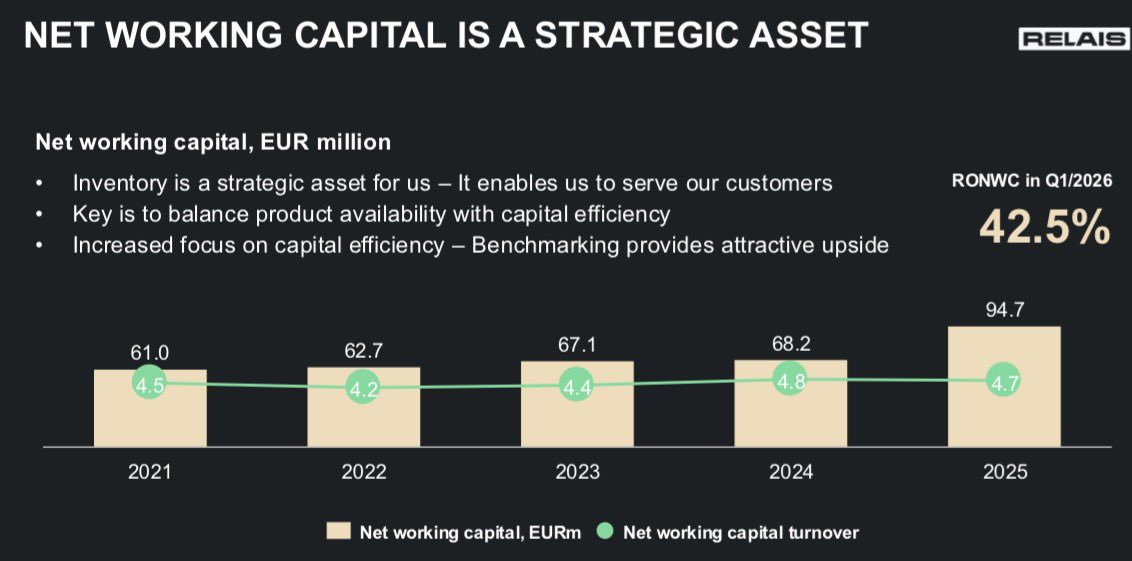

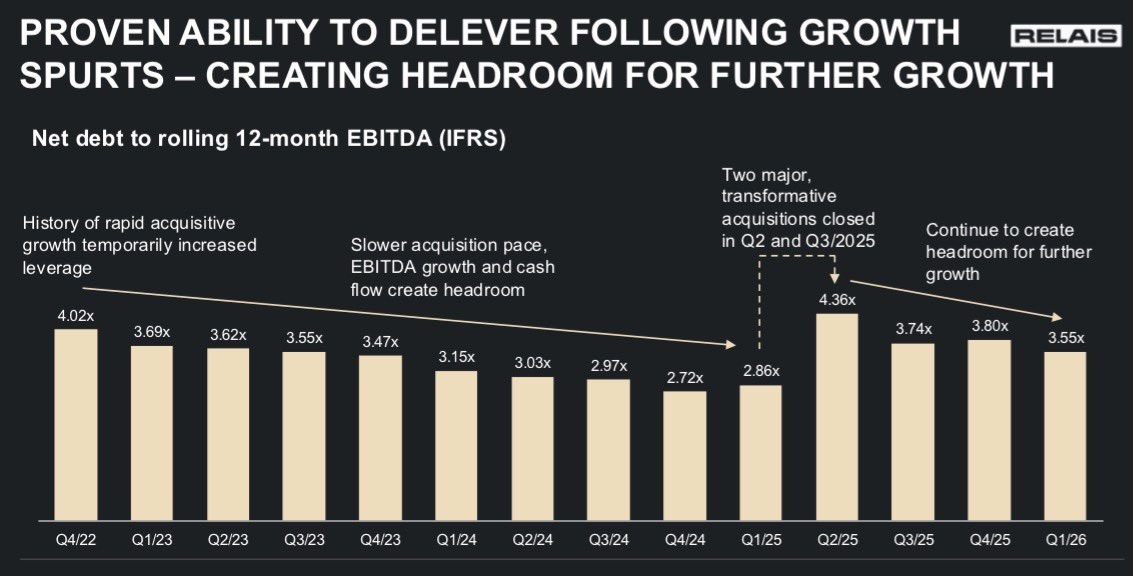

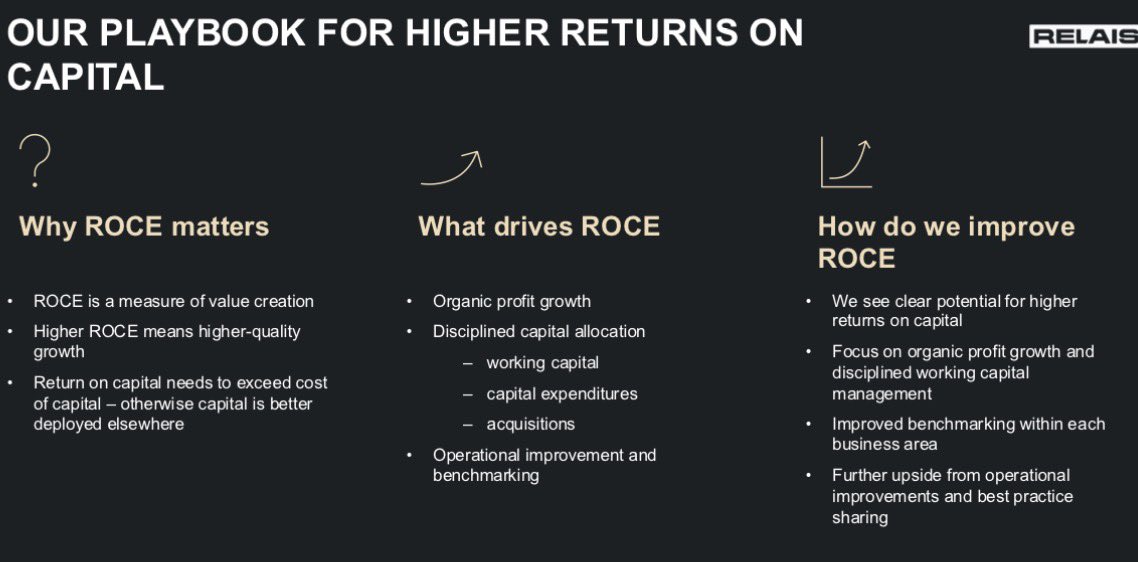

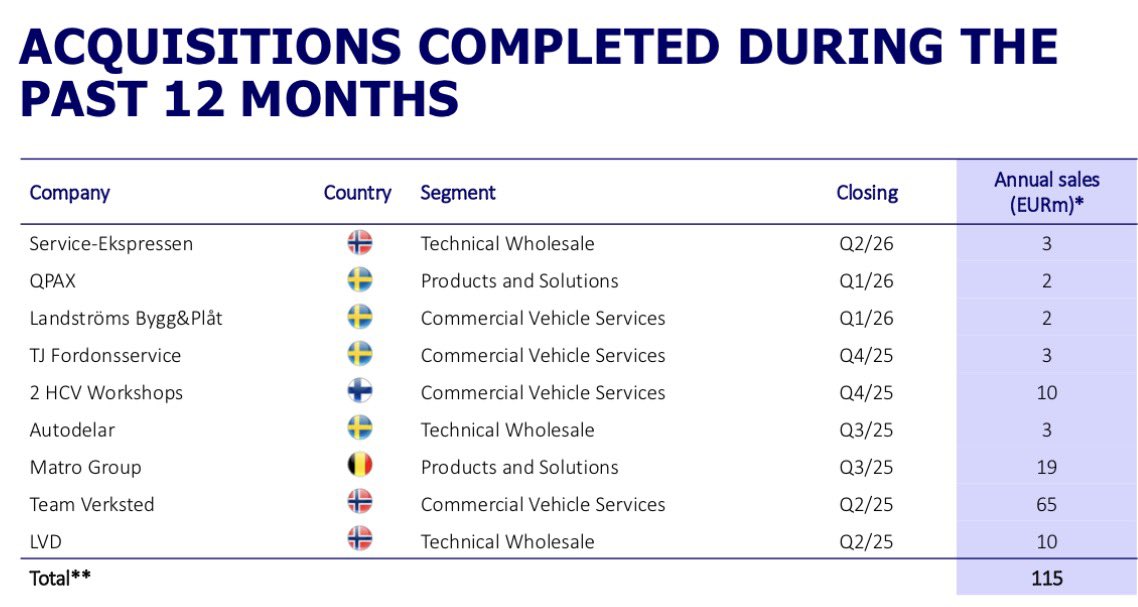

$Relais CMD: expected pivot towards focus on capital returns.

The company is finally shifting from fixed scale targets toward capital efficiency and shareholder returns.

Let's dive in:

May 13

$Relais Q1: Good organic growth driven by the cold environment

Sales: 44% (organic 7%)

EBITA margin: 10.8% (11.1% YoY)

Net debt / EBITA: 3.5x (2.9x)

While the M&A machine continues to contribute to growth, I’m very pleased to see organic growth returning to the growth trend. The drivers behind this were partly the cold weather in Q1, so it will be interesting to see whether this was a one-off effect or a more structural trend.

The CMD will be in one week, and I’m very excited to see management’s strategic focus. As mentioned before, I hope to see more focus around return-on-capital metrics. I would also like to see a greater emphasis on capital allocation to create shareholder value i.e. no dividends and preferably share buybacks at the current (in my opinion attractive) valuation levels of ~10x EV/EBITA (NTM).

Unfortunately, given the board’s priorities, I think that may be too much to ask for. Keeping the balance sheet under control will also be critical since, in my opinion, it is somewhat stretched at the moment, and I would prefer to see leverage closer to 3x.

If the investor story were expanded more outside Finland where the serial acquirer business model is less well known there could also be room for valuation multiple expansion toward Swedish peers.

1

9

1,666

May 24

Expansion ahead?

I’m also positive that during the strategic period until 2028, we will likely see bigger geographical expansion outside the Nordics and Baltics.

There is still room to consolidate the current market further.

The EV market is providing interesting new dynamics, though I'm assuming a slower transition in the heavy vehicle market, especially during this strategy period.

1

4

448

May 24

Valuation

In my estimates, $Relais is trading at ~11x EV/EBIT 2026E.

Given the quality of the business, that looks like reasonable value at the current price, in my view.

That said, ROCE will be the key variable to watch, alongside keeping leverage under control.

I also hold $Relais, so I may be biased, and I would be interested in counter arguments, especially anything bearish.

5

391