Ganesh Velu retweeted

An undercover investigation by LCA released in 2025, exposed the cruelty of rabbit pyrogen tests at a N. American toxicology research facility. During pyrogen testing, rabbits are forced into restraints, have test items injected into their ear veins, and are monitored with a temperature probe to determine if they develop a fever. At the end of tests, they were killed.

During 2024, there were over 100,000 rabbits used in research in the United States. For some tests, like rabbit pyrogen studies, there are non-animal alternatives available - yet regulatory testing bodies can continue to use rabbits in this test if they choose. Animal testing is cruel, unsustainable, and must end.

U.S. residents: Tell your House Representative and Senator you support prioritizing non-animal testing methods. Send an email to your elected officials here:

secure.lcanimal.org/page/817…

Thanks for sharing! Vidéo : @lc4a

#trending

#endanimaltesting

#stopanimaltesting

#rabbits

#endanimalcruelty

7

9

188

Jun 13

#Beezaasan

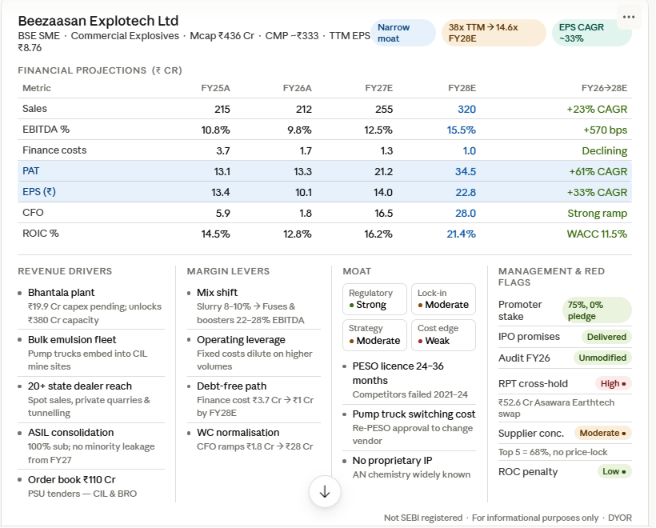

🧨 Beezaasan Explotech (SME)— Solar Industries and Premier Explosives are the sector benchmarks. Can Beezaasan ever trade at those multiples?

Solar dominates scale. Premier dominates defence. Beezaasan is neither — so what exactly is it, and is the market pricing it right? Let's break it down 👇

🏭 What does it actually do?

Beezaasan is a Gujarat-based commercial explosives company serving India's mining and infrastructure sector — coal mines, cement quarries, highway tunnels, and stone-crushing belts across 20 states.

Four business lines: packaged slurry explosives (legacy, low margin), bulk emulsion site services (pump trucks that mix chemicals directly in the borehole — safer, stickier), detonating fuses, and cast boosters & initiators. The new Bhantala plant is purpose-built for the last two.

The real model shift: they stopped selling boxes of explosive sticks and started delivering clean rock fragmentation as a service — mobile mixing trucks, on-site blasting engineers, zero live explosive storage at the mine. Coal India doesn't want a supplier; it wants a blasting partner. That's the wedge.

Does it have a moat?

Narrow, but real. PESO licensing takes 2–3 yrs just to get started. Once their pump trucks are embedded in a mine site, switching suppliers means halting operations. Their new Bhantala plant (fuses boosters) earns ~22–28% EBITDA vs 8–10% for basic slurry. Moat is widening — slowly.

📊 FY28E projections — the operating leverage story

New plant product mix shift = margin expansion on a growing revenue base.

The margin driver: basic slurry earns 8–10% EBITDA. Bulk emulsions 12–14%. Detonating fuses and cast boosters from Bhantala earn 22–28%. Every rupee that shifts toward the Bhantala product mix improves consolidated margins structurally — that's the operating leverage.

Finance costs nearly gone — from ₹3.7 Cr in FY25 to ~₹1.0 Cr in FY28E after IPO debt prepayment. Flows straight to PAT. EPS CAGR FY26–FY28E: ~33%.

One more trigger: ₹19.94 Cr of IPO cash is still parked in FDRs. The moment final PESO clearances under the Explosives Rules 2008 come through, that cash unlocks the next Bhantala capacity block.

💰 Valuation — what is the market actually pricing in?

At 32x trailing, the stock looks expensive on today's earnings.

On FY28E EPS of ₹22.8, the forward P/E compresses to ~12 x. For an SME commercial explosives utility with ~33% EPS CAGR through FY28E, 12–15x forward is not expensive. The market is asking you to believe in the Bhantala ramp and the mix shift. If you do — reasonably priced. If execution slips — there's limited margin of safety at 32x TTM.

Summary: fairly priced if Bhantala executes. No margin of safety if it doesn't.

Management quality — trust but verify

The Somani family runs the show — MD Navneet Somani (25 yrs explosives ops). Domain-deep, operationally hands-on. That counts in a high-compliance, dangerous-logistics business.

Redflags:

Related party cross-holding — ₹52.6 Cr

Management deployed a share swap to acquire a 34.84% stake in Asawara Earthtech Limited — an associate company in earthmoving & civil ops. Done via non-cash swap (not IPO proceeds), but complex group structures obscure true cash realities. Investors will discount until AEL contributes real, traceable earnings. This is the single biggest governance concern.

Pending litigation — ₹98.3 Lakh tax disputes

Standard for industrial/chemical companies in India. Immaterial at <0.5% of revenue. But worth tracking as the company scales into new states — regulatory surface area grows with geography.

These are SME transition friction flags, not structural fraud signals.

Can it ever re-rate like Premier Explosives (~80x P/E)?

Premier commands 80x because defence & aerospace is 76% of revenue — solid propellants for Akash/Astra missiles, ISRO pyrogen igniters, countermeasure Chaffs & Flares, and a record ₹1,569 Cr order book (4x annual revenue). Irreplaceable supplier relationships built over years of MoD qualification cycles.

Beezaasan is 100% commercial mining. No missile contracts. No ISRO lines. No export pipeline. Management has explicitly confirmed no defence pivot — every IPO rupee is going into emulsion plant expansion and commercial bulk trucks, not cleanroom propellant facilities.

For a re-rating, the business model itself must change. Entering defence requires years of R&D, MoD qualification cycles, and entirely new infrastructure. Zero signal from management today.

📌 Final take

Beezaasan is a clean, well-run, narrowly moated commercial explosives company with a credible earnings ramp. Disciplined promoters — 75% stake, zero pledge. Real operating leverage as Bhantala scales. Governance flags are manageable, not structural — but they are real and need watching.

At 32x TTM, you are paying for FY28E delivery. The ~33% EPS CAGR and 12x FY28E P/E make it reasonable if execution holds — but there's limited downside buffer if the Bhantala ramp or PESO clearances disappoint.

Re-rating story? Doesn't exist yet. Without a mix shift toward defence — which management has not signalled — this trades as a mining infrastructure utility, not a defence-tech compounder. Everything seems fairly priced at current levels.

📌 The one thing to watch: any strategic pivot toward defence/aerospace. That's the single catalyst that changes the valuation conversation entirely. Until then — priced to perfection on the existing plan.

[Not investment Advice, DYOR]

[Any contrarian views or missing information , please do share in comments]

4

28

2,561

💉 Water For Injection System

Delivering sterile, pyrogen-free water with reliable performance and regulatory compliance. 🏭🔬

✅ USP, EP & JP Compliant

✅ Hygienic Design

✅ Pharma-Grade Quality

#WaterForInjectionSystem #WFISystem #PharmaWater #PurifiedWater #SwjalProcess

7

Jun 12

Comparison of the pyrogen tests in rabbits and with limulus lysate popline.org/node/3210?v=185

4

Jun 11

Can't comment on AI's role in automating PK/PD but I think there's going to be major use cases for it in some of the other bullet points in the screenshot

E.g. preclin toxicity testing already has precedent in evolving from cruder in vivo methods (rabbit pyrogen test to LAL in testing for presence of endotoxin)

1

7

376

0.22 filter will remove bacteria, but endotoxin molecules slip right through

Sterile... yes

Pyrogen-free... no

So you may still cause immune responses like flu or fever, etc.

1

4

394

1

2

57

May 27

ADI has urged the United States Pharmacopeia (USP) to end animal-based drug tests like the rabbit pyrogen test which has already ended in Europe. Safer, human-relevant alternatives exist. Learn more & take action👉 https//www.ad-international.org/animal_experiments/go.php?id=5067

1

7

22

417

May 17

definitely IL-1,, The exact molecule responsible for making you feel like you need 5 blankets in the middle of summer🥶

It acts as a potent endogenous pyrogen by stimulating COX-2 expression in the hypothalamus, leading to increased PGE_2 production. Along with TNF-\alpha and IL-6, they form the ultimate "fever-inducing trio" 🌡️🧠

1

13

1,724

In severe Sepsis, hypothermia is often a sign that the body’s compensatory mechanisms are failing rather than mounting an effective febrile response.

Why hypothermia can occur instead of fever

Early infection usually triggers pyrogen-mediated fever (IL-1, TNF-α, prostaglandins acting on the hypothalamus).

In advanced sepsis, especially septic shock:

Cytokine regulation becomes dysregulated

Metabolic reserves become depleted

Peripheral vasodilation increases heat loss

Mitochondrial dysfunction impairs heat generation

Hypothalamic thermoregulation may fail

The result can be a core temperature <36°C, particularly in:

Elderly patients

Immunocompromised patients

Severe gram-negative or hemorrhagic infections

Late-stage shock states

Why it is more dangerous

Hypothermia in sepsis is associated with:

Higher lactate levels

Worse circulatory collapse

Coagulopathy

Reduced immune efficiency

Multi-organ dysfunction

Clinically, septic patients with hypothermia often have higher mortality than those with fever because it reflects physiologic exhaustion and severe systemic dysregulation rather than a robust immune response.

1

2

34

danny fact of the day:

moldy boy... the rot for him, forever

(art also by pyrogen <3)

5

9

113

1,160