Srivatsa 🪴 retweeted

2h

The Netherlands have been very basic in possession, 4-3-3 with very little movement or rotations, everything is static. Only from around 15-20 mins onwards have we seen Dumfries move high into the right half space once in settled possession. Apart from that very little to give the Japan 5-3-2/5-4-1 anything to think about.

Off the ball an extremely passive 5-4-1 with De Jong dropping from midfield into the defensive line at CCB.

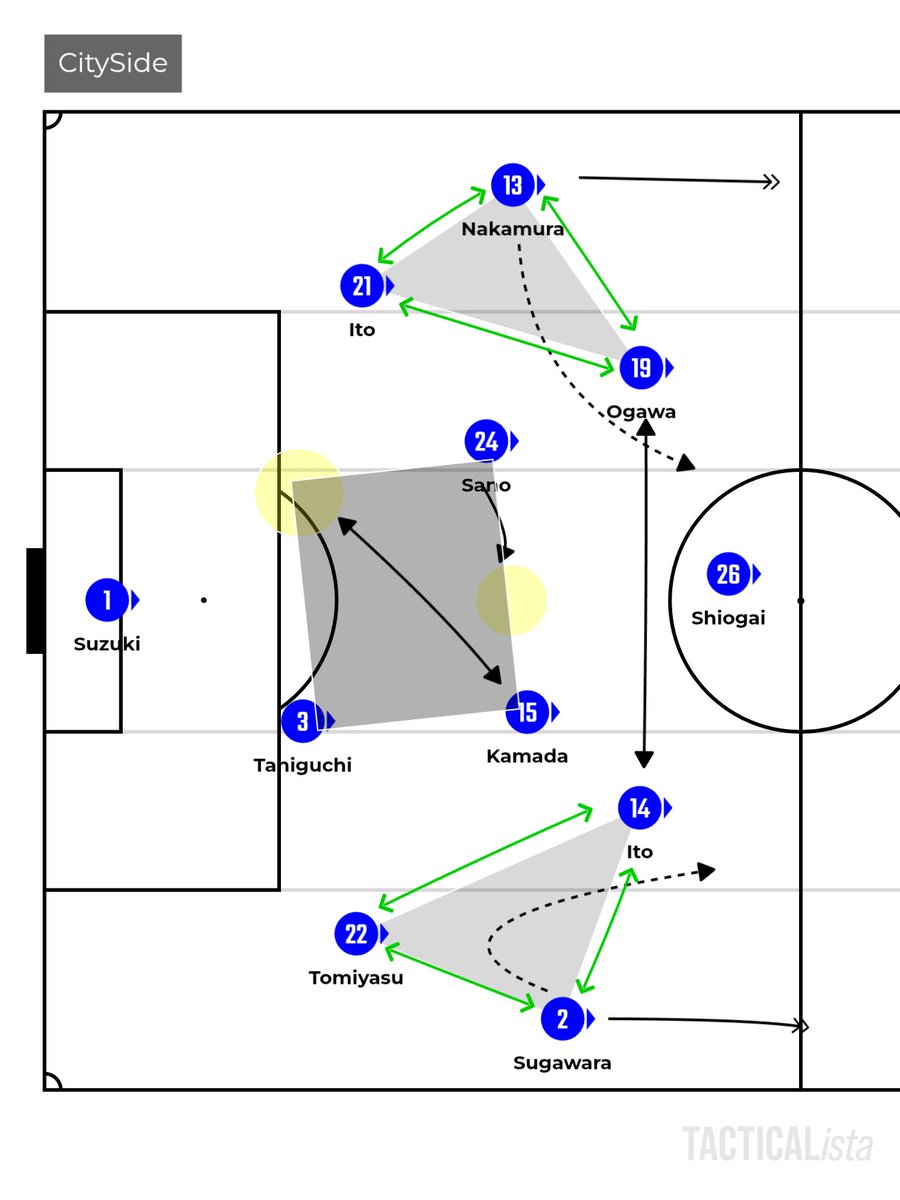

Japan in a 4-2-4 from goal kicks which transitions into a 3-2-5 with the WB’s advanced, Nakamura often inverting into the left half space as seen just before the call for the drinks break.

Japan off the ball pressing in a 5-4-1/5-3-2, when in the former the midfield line is very compact and narrow forcing The Dutch to pass to the dropping wingers with the WB’s ready to jump and engage on their first touch.

Cagey start.

1

2

22

2,147

Get Bouaddi and Wharton to pair with both ball carriers aka Gravenberch and Szoboszlai; squad rotations with 4 competitions next season and we’ll bring back what belongs to us… danger!

22

This is what happens when someone doesn't realize the outrageous number of different rotations the Pacers had to use due to injuries to players not named "Tyrese Haliburton"

Not to be that guy but some pacers fans on this app are wildly delusional…..

“Tyrese Haliburton” doesn’t take you from the second worst record in the nba back to the finals bro

1

4

139

-basically ensures that as long as tune break is relevant, they get to do EXTRA damage on top of their big damage rotations already. Even if they share units, the units in question have been shilled for basically EVERY ToA and WhiWa since they released, barring Phro, who-

1

1

Ironically, the Netherlands often looked more stable when De Jong was part of the back line rather than defending ahead of it. Japan recognized this, using Kubo's movements and Maeda's runs to attack the spaces created by his rotations and disrupt the Dutch defensive structure.

234

My med school (@RFUniversity) didn’t have a teaching hospital so I did away rotations too during my M4 yr for anes (2004 Match). I had lived all my life in northern IL/Chicago. I did an away rotation in TX - first time I ever visited. I have now been in TX since 2008

1

1

7

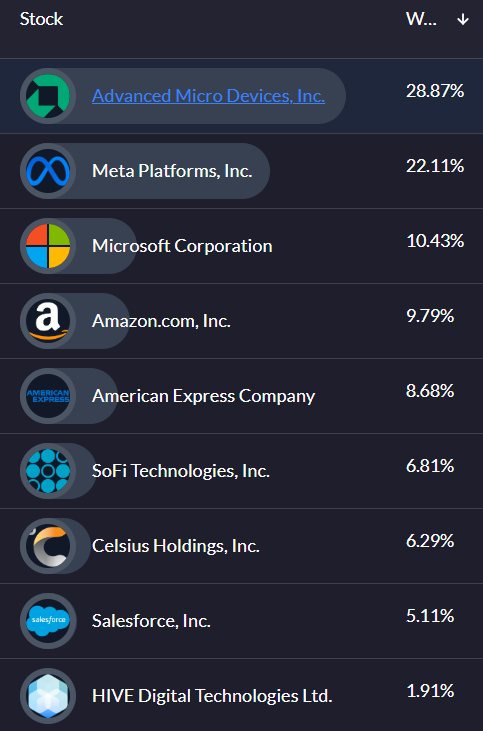

Here is what Qualtrim's Ai Generated Portfolio Analysis generated regarding my Compounding account.

$AMD 29% holding

$META 22% holding

$MSFT 10% holding

$AMZN 10% holding

$AXP 9% holding

$SOFI 7% holding

$CELH 6% holding

$CRM 5% holding

$HIVE 2% holding

Qualities

This portfolio is anchored by a set of world‑class, asset‑light software and platform businesses with high switching costs and durable moats. Microsoft, Salesforce, Meta, Amazon, and AMD are all deeply integrated into either enterprise workflows or consumer behavior. Microsoft’s productivity and cloud stack (Office, Windows, Azure, GitHub, etc.) enjoy entrenched network effects, subscription revenue, and strong pricing power, translating into high margins and excellent scalability. Salesforce sits at the heart of customer data and sales operations, with a mission‑critical CRM platform that tends to be very sticky due to data gravity, integration into business processes, and a subscription model that grows alongside customers. Meta’s family of apps benefits from unrivaled social network effects and an increasingly effective ad platform, giving it both pricing power and resilience; its massive user engagement and ongoing efficiency push in its ad systems and AI infrastructure support high incremental margins. AMD leverages a fabless model and technological leadership in CPUs and GPUs to address secular growth in data center, AI, and high‑performance computing, which can drive powerful operating leverage.

There is also a good blend of secular growth consumer and financial names with differentiated models. Amazon combines a dominant e‑commerce marketplace with a hugely profitable, scalable cloud business (AWS), where recurring and usage‑based revenue and deep integration into customers’ IT stacks create stickiness and long runways for growth. American Express has a strong brand, affluent customer base, and a closed‑loop network that gives it superior data on cardholder behavior, supporting risk management, premium pricing, and attractive fee and interest revenue across cycles. Celsius represents a high‑growth, brand‑driven consumer defensive play, with a lifestyle and fitness‑oriented brand that has shown strong velocity and distribution expansion, offering a potentially long runway if it can entrench itself as a staple in the energy/functional beverage category. SoFi brings a vertically integrated, digital‑first financial platform spanning lending, deposits, and investing, creating cross‑sell potential and recurring revenue from multiple products per member. HIVE adds an idiosyncratic, high‑beta exposure to digital assets and specialized computing, which, although volatile, is leveraged to secular themes in blockchain and high‑performance infrastructure.

Risks

The portfolio is heavily concentrated in a small number of large, growth‑oriented technology and platform businesses, creating significant exposure to sector‑specific risks such as regulatory pressure, changes in technology standards, and multiple compression if interest rates rise or sentiment towards growth cools. Meta, Microsoft, Amazon, Salesforce, and AMD are all under varying degrees of antitrust, privacy, or platform power scrutiny globally; any regulatory outcome that limits data usage, bundling, or business practices could impair their moats or margins. The weighting is also top‑heavy, with Meta alone representing a very large slice of the portfolio, increasing single‑name risk tied to shifts in digital advertising, user behavior, or execution in its capital‑intensive metaverse and AI ambitions. AMD faces intense competitive and pricing pressure from larger incumbents (notably NVIDIA and Intel), and is exposed to cyclical swings in semiconductor demand and capital spending.

On the consumer and financial side, Celsius and SoFi inject meaningful idiosyncratic and execution risk. Celsius’ valuation and growth story depend on sustaining rapid distribution expansion and brand relevance in a category dominated by giants like Monster, Red Bull, and Coca‑Cola; any stumble in marketing, regulatory scrutiny around ingredients/claims, or shelf‑space competition could quickly compress margins and growth. SoFi and HIVE add regulatory, credit, and macro sensitivity: SoFi’s lending operations are vulnerable to credit cycle deterioration, funding cost shifts, and changing student loan or banking regulations, while HIVE is highly leveraged to crypto prices, mining economics, and energy costs, making its cash flows volatile and hard to forecast. American Express, while high quality, is still cyclical, with sensitivity to consumer spending, credit quality, and travel trends. Overall, the portfolio’s tilt towards growth, tech, and a handful of thematic names makes it less resilient to sharp style rotations, regulatory shocks, or a prolonged period of higher rates than a more diversified, cash‑flow‑stability‑focused allocation would be.

1

1

97

Updated available socks!

These are a few I’ll be wearing in rotations until someone asks for something specific for me to wear. As you can see, some are brand new while others already have a couple days worn. Anything here has a set fee 10 each extra day worn. Feel free to dm more questions. Shipping in the states only!

47

2/3 The bigger picture: this is trying to turn emissions from a blunt subsidy into a forecasting market. If it works, Base gets a liquidity layer that adapts in real time to new launches, stablecoin rotations, and flow bursts.

That's a genuine competitive advantage in DEX wars — not just cheaper liquidity, but smarter liquidity.

1

3

1/3 Aerodrome moving to predictive allocation in July is the most interesting mechanism change in DeFi right now. Instead of weekly gauge votes that chase yesterday's volume, emissions get routed based on where liquidity is expected to be needed next.

The "80% efficiency" claim is about waste reduction — same emissions, less dead TVL, better depth where flow actually shows up. On Base, where demand is increasingly event-driven, weekly governance cycles were too slow.

Leaning positive but not calling it a moat yet. Dromos has the track record — Velodrome went from $14M to $80M TVL and $270M to $2.2B cumulative volume through mechanism redesign, not just emissions spend. That credibility matters.

The real edge isn't the mechanism itself — that's copyable. It's Aerodrome's embedded position on Base plus the existing network of voters, LPs, and projects already trained on the system. Predictive allocation strengthens that gravity, but only if it delivers.

One thing I'm watching carefully: who captures the value. If sophisticated allocators dominate the new system, it's efficient but concentrated. Good for the protocol, less clear for the average tokenholder.

What confirms the thesis — fee/TVL rising post-July without proportional emissions growth, and depth holding up during volatile rotations instead of getting more fragile.

1

2

They absolutely don’t understand how much contracts factor into playing rotations at the professional level💯

4

31m

My notion is that Japan should have taken all three points in the game.

Two points to highlight (not going to go deeper, will keep it brief):

1. Daichi Kamada is a machine, and was everywhere on the pitch.

- At one point, we would see him in the back-line to facilitate possession, the next moment, in a support role alongside Sano in midfield, and rarely, in between the lines to support the offensive phases. What a game he had!

2. The rotations from the two triangles between the wing-back, the wide centre-back and the winger (inside-forward) caused the Dutch OOP (out-of-possession) structure to falter on occasions.

- It is what we call "organised chaos". The best part was that neither of the three players (on each flank) occupied the same vertical channel.

Again, Japan should have gotten more out of the game.

1

8

21

2,015

32m

praying this goes to like 100m and we can print on gaming rotations on the scope

1

2

22

This is beyond strange. I do not think Jim Farley should’ve commented on this based on the minuscule percentage of Americans, who would actually work on a modern day, Car themselves! Only those who are skilled and know what they’re doing in auto mechanics would do their own oil change, spark, plugs, tire, rotations, etc. I would say 95% of the population takes a car to the dealer for Service. So what on earth is the issue? Has there been a huge ramp up in Home repairs ?

4

33m

Horrible in game changes from Koeman, Summerville should have played the 90

Not convinced with The Netherlands. Too static in possession and nowhere near enough rotations or 3rd man movements higher up the pitch. Static 4-3-3. Wide triangles on both sides but no interchanging between the 3 players makes it a lot easier to defend. Out of possession far too passive in a 5-4-1.

Netherlands 2nd goal comes from a simple Dumfries overlap on the right creating space for Summerville to cut inside. Can’t particularly say the same for the left as Van De Ven is at left back, he isn’t a natural LB so won’t particularly have good understanding on when to rotate with players in Netherlands left sided triangle and when to overlap and underlap in supporting attacks. (Not that anyone was consistently rotating in the Netherlands structure anyway). Combine Van De Ven simply not being a natural LB with Gakpo who isn’t the most successful at taking the opposition LB on 1v1 and it leads to the left side being extremely limited in what it can offer.

A draw a fair result.

🇳🇱🇯🇵

1

7

598

🍺 J'ai testé les 3 spécialisations de Merlin.

Le plan était simple :

👉 faire mes rotations

👉 réussir les Jonctions

La réalité a été un peu plus... compliquée. 🤣

#7DSOrigin #7DSO #7DS #ナナオリ #TheSevenDeadlySinsOrigin

📺 Nouvelle vidéo :

youtu.be/gS57lGHYVXw

23

36m

Frenkie De Jong: 73 useless rotations in 46 seconds, a million pointless side passes in 90 minutes, & at least 8 hair flips per minute. The shiniest & at the same time most useless toy in the box

32