29s

RT @scs: ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀ ⠀⠀⠀ ⠀ ⠀ ⠀

⠀⠀⠀ ⠀ ⠀ ⠀⠀ 𝗁𝗈𝗐 𝗂 𝗌𝗅𝖾𝖾𝗉 𝗐 𝗎⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀

254

2026.06.14

第18回U-15いわきサッカーリーグ2026

6/13結果

《1部》

平一中 3-1 昌平中セカンド

小名浜ニ中 2-2 古河電池FC

《2部》

O solo内郷 1-4 勿来FW・SCSセカンド

【勝敗表】

iwaki-fa.com/3/u15/iwaki/26/…

【日程表】

iwaki-fa.com/3/u15/iwaki/26/…

27

backstage_staff retweeted

Jun 10

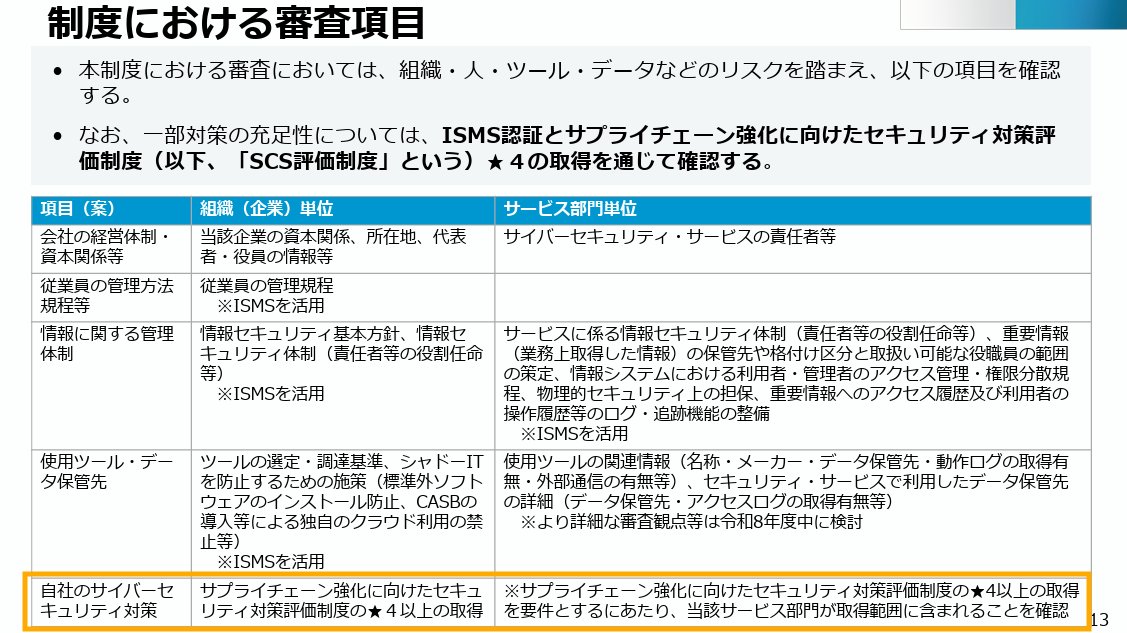

SCS評価制度と並行して、「サイバーセキュリティ・サービス認定制度」の整備が進んでいるようです。

SCS★4の技術検証事業者には、現行の「情報セキュリティサービス基準適合サービスリスト」の脆弱性診断サービス、ペンテスト含む、の登録要件を満たすことが必要。

一方、新認定制度では、技術・品質だけでなく、サービス事業者自身の運営体制、情報管理、人員管理等の信頼性も確認するとのこと。

さらに今回の中間とりまとめでは、ISMS認証だけでは対策水準に幅が出るため、共通に満たすべき最低限のサイバーセキュリティ対策水準を担保する目的で、SCS評価制度★4以上の取得も求める整理が示されています。

顧客環境や機微情報に深く触れる事業者には、「サービスの技術力」だけでなく、「事業者として信頼できるか」も問われる流れになりそう。

meti.go.jp/shingikai/mono_in…

43

225

16,307

RT @scs: ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀ ⠀⠀⠀ ⠀ ⠀ ⠀

⠀⠀⠀ ⠀ ⠀ ⠀⠀ 𝗁𝗈𝗐 𝗂 𝗌𝗅𝖾𝖾𝗉 𝗐 𝗎⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀

254

Deploy worldwide 😂😂😂. That’s why the strait is closed😂😂😂. Settle down 🐷 noy. They leave you hanging to dry every time China shows up in SCS 😂😂😂

2

5

RT @scs: ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀ ⠀⠀⠀ ⠀ ⠀ ⠀

⠀⠀⠀ ⠀ ⠀ ⠀⠀ 𝗁𝗈𝗐 𝗂 𝗌𝗅𝖾𝖾𝗉 𝗐 𝗎⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀

254

RT @scs: ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀ ⠀⠀⠀ ⠀ ⠀ ⠀

⠀⠀⠀ ⠀ ⠀ ⠀⠀ 𝗁𝗈𝗐 𝗂 𝗌𝗅𝖾𝖾𝗉 𝗐 𝗎⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀

254

41m

RT @scs: ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀ ⠀⠀⠀ ⠀ ⠀ ⠀

⠀⠀⠀ ⠀ ⠀ ⠀⠀ 𝗁𝗈𝗐 𝗂 𝗌𝗅𝖾𝖾𝗉 𝗐 𝗎⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀

254

RT @scs: ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀ ⠀⠀⠀ ⠀ ⠀ ⠀

⠀⠀⠀ ⠀ ⠀ ⠀⠀ 𝗁𝗈𝗐 𝗂 𝗌𝗅𝖾𝖾𝗉 𝗐 𝗎⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀

254

44m

RT @scs: ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀ ⠀⠀⠀ ⠀ ⠀ ⠀

⠀⠀⠀ ⠀ ⠀ ⠀⠀ 𝗁𝗈𝗐 𝗂 𝗌𝗅𝖾𝖾𝗉 𝗐 𝗎⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀

254

RT @scs: ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀ ⠀⠀⠀ ⠀ ⠀ ⠀

⠀⠀⠀ ⠀ ⠀ ⠀⠀ 𝗁𝗈𝗐 𝗂 𝗌𝗅𝖾𝖾𝗉 𝗐 𝗎⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀

254

ヴァンタ retweeted

Jun 13

55

427

12,485

RT @scs: ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀ ⠀⠀⠀ ⠀ ⠀ ⠀

⠀⠀⠀ ⠀ ⠀ ⠀⠀ 𝗁𝗈𝗐 𝗂 𝗌𝗅𝖾𝖾𝗉 𝗐 𝗎⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀

254

RT @scs: ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀ ⠀⠀⠀ ⠀ ⠀ ⠀

⠀⠀⠀ ⠀ ⠀ ⠀⠀ 𝗁𝗈𝗐 𝗂 𝗌𝗅𝖾𝖾𝗉 𝗐 𝗎⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀

254

📈 Earnings Deep Dive,

Delhivery Ltd

#Q4FY26 #Nifty #DELHIVERY

Delhivery achieves profitability and ₹10,000 crore revenue in FY26, delivers a billion parcels! 🚀💰

A deep dive into their Q4 FY26 Concall ⬇️

Delhivery Ltd marked a significant FY26, crossing ₹10,000 crore in revenue from services and delivering over a billion parcels, alongside 2 million metric tons of freight in PTL.

Q4 also saw strong sequential growth in Express volumes.

The company achieved a notable turnaround in profitability, with FY26 adjusted EBITDA reaching 7.3% (₹764 crore) and PAT at ₹347 crore.

Critically, it became free cash flow positive with ₹89 crore, a year ahead of its initial target.

This robust performance, coupled with a strong balance sheet of over ₹4,500 crore in cash, positions Delhivery for disciplined reinvestment into new growth pillars while maintaining capital efficiency and improving returns on invested capital.

🔹 Outlook & Guidance 🎯💡

- Management anticipates e-commerce industry growth of 15-20% in the medium term.

- The competitive landscape is seen as more rational, favoring scaled 3PL providers over 1PL.

- SCS projects must pass an internal hurdle rate, ensuring margin-accretive growth.

- Capex intensity is projected to remain low at around 4%, with AI/robotics not altering this trajectory.

- Transport ROIC is targeted to reach 25% driven by profitability improvement towards 10% adjusted EBITDA.

- Significant investment of ₹130–160 crore is planned for FY27 into new growth pillars, notably intracity logistics.

🔹 Q4 Performance Highlights 📊💰

- FY26 revenue from services reached ₹10,486 crore, with Q4 contributing ₹2,848 crore.

- The company delivered over a billion parcels in FY26, with Q4 Express volumes at 306 million parcels.

- PTL freight volumes hit 2 million metric tons in FY26, and Q4 saw ~549k tons, reflecting 20% growth.

- FY26 adjusted EBITDA stood at 7.3% (₹764 crore), and PAT was ₹347 crore (3.2%).

- Free cash flow turned positive at ₹89 crore, achieving this milestone one year ahead of schedule.

- Express business maintained normative margins of 16–18%, while PTL gross margins expanded from 14% to 28%.

- Supply Chain Services (SCS) revenue was ₹729 crore with a 10.9% service EBITDA margin, marking a decisive turnaround.

- Net working capital days materially improved to 11 days from 38 days three years ago, due to enhanced billing and client selection.

🔹 Management Tone & Strategy 🧭🛡️

- Management attributes strong performance to structural cost advantages and operating leverage.

- Strategic calls included exiting specific non-scalable businesses, like mother warehousing for quick commerce, and renegotiating client contracts.

- Working capital improvement stemmed from faster billing through AI/systems and disciplined client selection based on payment philosophies.

- AI is strategically deployed for operational efficiency in areas like claims automation and PTL paperwork reduction, without increasing tech team size.

- In-house developed AGVs are scaling up in mega gateways to enhance facility movement and address labor market tightness.

- Reinvestment into new growth pillars, particularly Delhivery Direct (intracity/intercity SME logistics), aims to externalize internal capabilities.

- CEO emphasizes a disciplined approach, rejecting past industry "burn/capex frenzy" and focusing on sustainable, profitable growth.

61

RT @scs: ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀ ⠀⠀⠀ ⠀ ⠀ ⠀

⠀⠀⠀ ⠀ ⠀ ⠀⠀ 𝗁𝗈𝗐 𝗂 𝗌𝗅𝖾𝖾𝗉 𝗐 𝗎⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀ ⠀⠀⠀ ⠀ ⠀ ⠀⠀⠀⠀⠀ ⠀ ⠀

254

shashivardhan retweeted

For SCs and STs, reservation is intended to address the historical and continuing social discrimination, exclusion, indignity, and servitude imposed on them because of their social status. Criteria for EWS reservation is economic disadvantage and financial backwardness.

3

9

42

559