Chandni retweeted

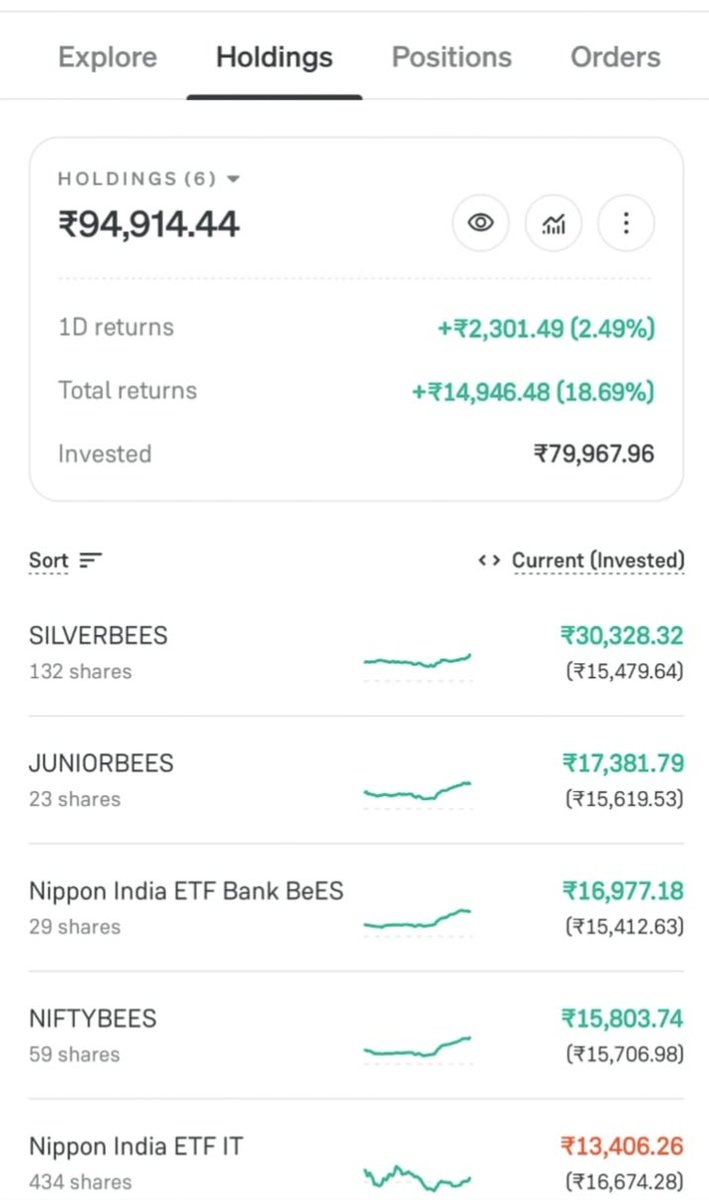

𝟭𝟭𝟰 𝗪𝗲𝗲𝗸𝘀 𝗼𝗳 𝗖𝗼𝗻𝘀𝗶𝘀𝘁𝗲𝗻𝘁 𝗦𝗜𝗣 ✅

114 weeks Every week invested

Market up 📈, market down 📉 — SIP continued.

No shortcuts. No FOMO. Just discipline and the power of compounding.

Goal: Financial Freedom by 2047

Time in the market > Timing the market.

#SIP #ETF #StockMarket #Compounding #WealthCreation

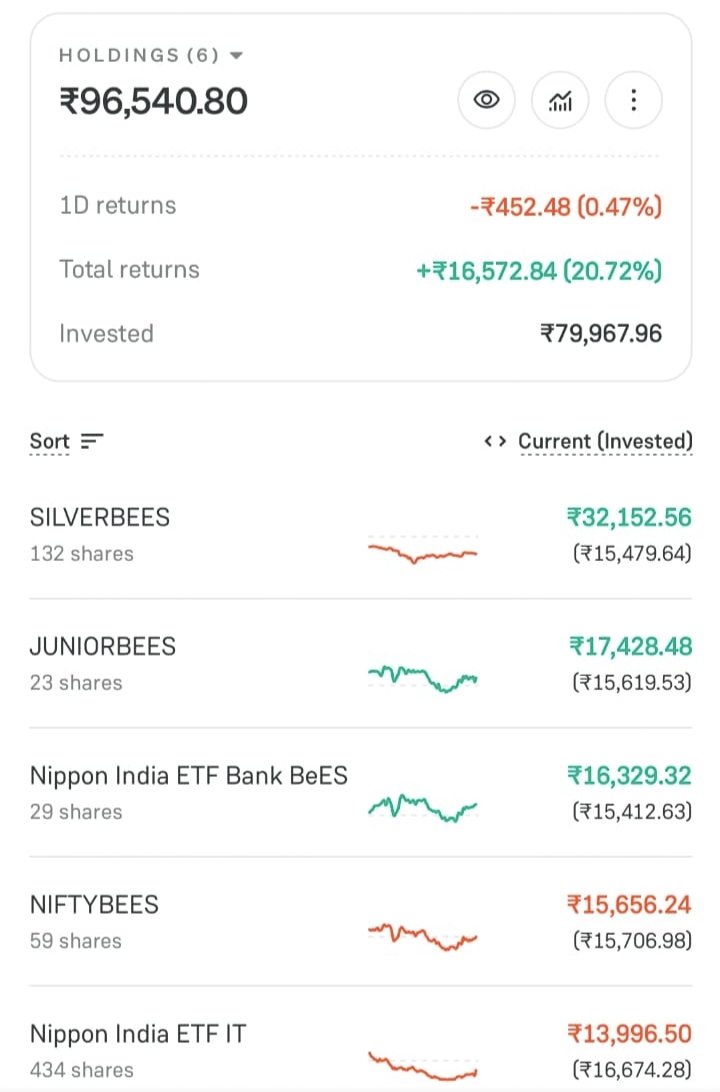

𝟭𝟭𝟯 𝗪𝗲𝗲𝗸𝘀 𝗼𝗳 𝗖𝗼𝗻𝘀𝗶𝘀𝘁𝗲𝗻𝘁 𝗦𝗜𝗣 ✅

For 113 weeks straight, I kept investing through market ups and downs, steadily building my ETF portfolio.

No shortcuts. No panic selling. No chasing the latest trends.

Just discipline, patience, and faith in the power of compounding.

Every SIP is a small step today towards financial freedom tomorrow.

The journey continues with a long-term vision: 2047 🇮🇳

📌 Time in the market beats timing the market.

Note: Added 4 stocks through Kite today 👍

#StockMarket #SIP #ETF #Investing #Compounding #WealthCreation #LongTermInvesting

13

31

107

1,602

NANA \(^_^)/ retweeted

18h

✨COMING SOON✨

Tie your ribbon, Sip your tea, Celebrate 127 Anniversary🧺🌿

Get ready for a Sweet Summer Picnic & Workshop hosted by @mouwpeceye!

Our special project 🎀STICKER-ING WITH TEA🎀 is coming your way.

Stay Tuned For The Next Official Poster, Chilzen🤎

11

62

126

11,325

Good time to start SIP in IT funds.

Prediction in the next 12 months:

- SpaceX's IPO will greatly temper the hype cycle

- OAI/Ant IPOs will force cash-flow reality

- Token costs will rise to meet cash-flow expectations

- Job loss doomerism will subside

- Humans will "become cool again"

- GCCs in India will thrive

1

Arnold Lane retweeted

7h

"please don't bring up politics around my liberal parents tonight"

me after one sip of water:

22

306

4,274

123,207

bruce takes the cup, holding it in one hand as the other placed his coat on the seat opposite hers——then he soon sat on the chair and began to sip gradually at the coffee. his gaze meeting hers.

while a sip was being taken, a almost full cup was handed to him .. her back resting against the back of her chair.

1

[ Being unable to feel the scalding hot temperature of his coffee, Yesod didn't need to wait for it to cool down. So, he took a loooonng sip of it. ]

Mm. Not bad.

1

1

5

What's harder?

A) Choosing a fund.

B) Continuing SIP during a market crash.

Most investors know the answer.

#SIP

1

#SundayRead | The SIP assets stood at Rs 17,12,126.14 crore in May 2026, constituting nearly 21% of the industry's AUM

#mutualfunds

economictimes.indiatimes.com…

14

your parents probably have a LIC policy they’ve been paying for 20 years. they think it’s an investment.

it’s not. here’s what it actually is.

an endowment plan bundles life insurance and a savings component together. sounds smart. one product doing two jobs. the problem is it does both jobs terribly.

real example. jeevan anand, one of LIC’s most popular plans. ₹50,000/year premium. 20 year term. total paid: ₹10 lakh. maturity amount: roughly ₹13-14 lakh. that’s approximately 3.5% annual returns. inflation is 6%. you just lost money while thinking you were saving it.

now look at the life cover. on that same ₹50,000/year premium you get maybe ₹8-10L of cover. a pure term insurance plan with the same premium gives you ₹1.5-2 crore of cover. same money. 15x more protection.

so why did your parents buy it? the LIC agent got 25-35% commission in year one. on a term plan he gets 5-7%. he didn’t sell them the wrong product because he was evil. he sold it because it paid him 5x more. the incentive was never your family’s wealth.

this has been going on for 50 years across crores of indian families. every year premiums go in. every year real returns stay below inflation. every year the agent renews his commission.

what your parents actually needed was simple. a term plan for protection. a mutual fund SIP for wealth building. keep insurance and investment completely separate. bundling them only benefits the person selling.

if your parents have an endowment plan right now, check the surrender value. compare it to what they’ve paid in. calculate what that money would be worth in an index fund.

the number will make you uncomfortable. but better uncomfortable now than broke at retirement.

3

Shoukat Lashari retweeted

Good morning Happy Sunday ❤️

Take a pause, sip your favorite drink, and give yourself the gift of peace today. 💕

#GoodMorning #HappySunday

15

3

16

153

👑 Earning 30 #B3TR rewards as a @mugshot_vet Pro member 🚀☕ Every sip hits different when you're stacking 10x.

👉 mugshot.eco

#MugshotPro #VeChain #VeBetterDAO

1

1

Sip, de colorear

Ya mañana tengo que justificar y eso

Y la otra tarea pesada 💔

En fin, estoy destrozada

Entre que me levanté temprano, medio trabaje y luego me fui al centro en tacones siento que me deshago

5