sjlogistics? also a major beneficiary as middle east activity starts in the mid stream.

1

1

38

From booking and documentation to vessel tracking and delivery, SJ Logistics ensures every process is handled with precision across global supply chains.

#SJLogistics #OceanFreight #FreightForwarding #GlobalLogistics #ContainerShipping

1

3

166

Jun 12

sirji #SJlogistics ka bhi kuch batao....chal kya raha hai kuch samaj nahi aa raha even after conversion of warrants by promoter🧐

1

114

RAJENDER PUNJANI retweeted

Jun 5

SJ Logistics

#SJLog

#SJLogistics

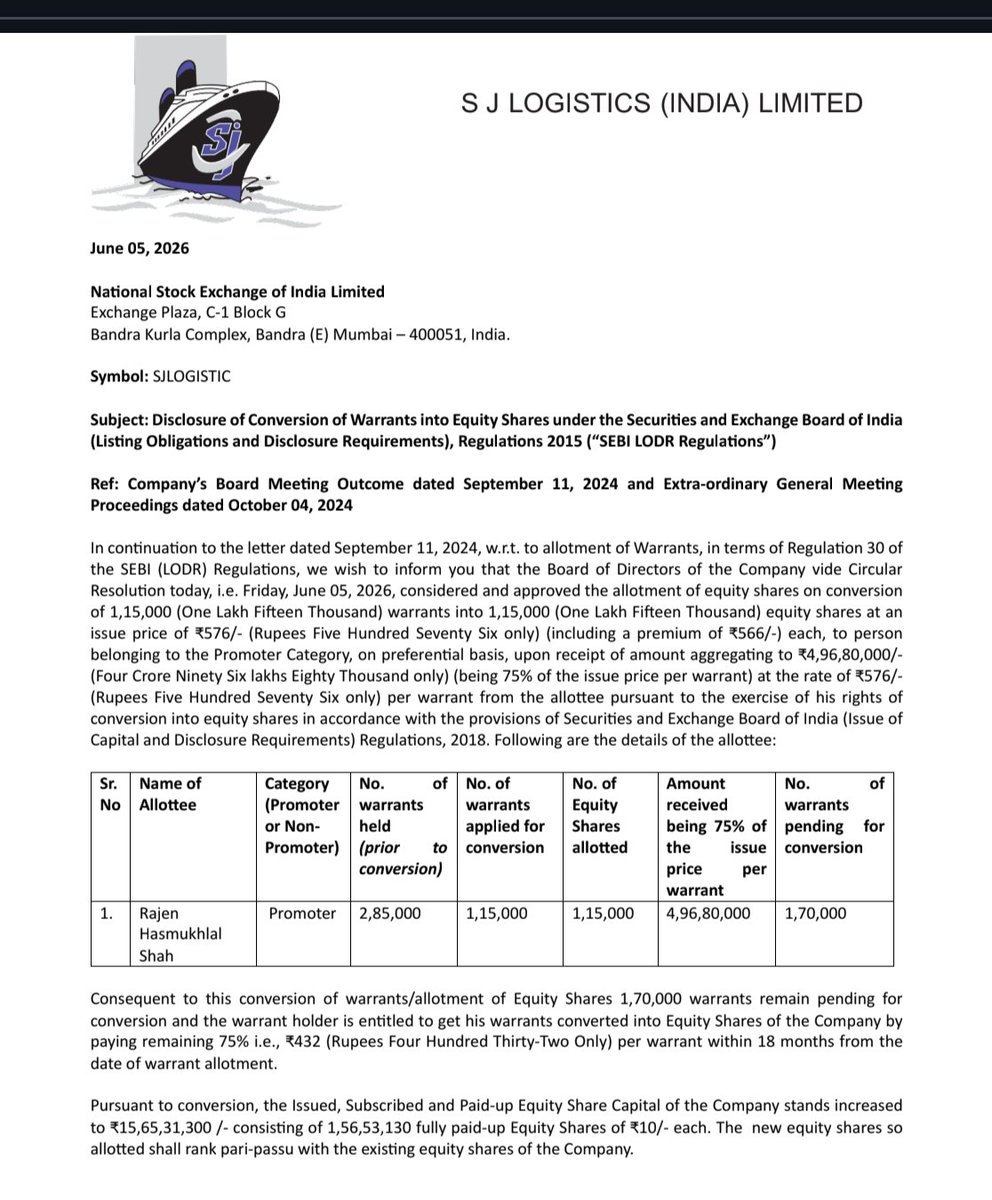

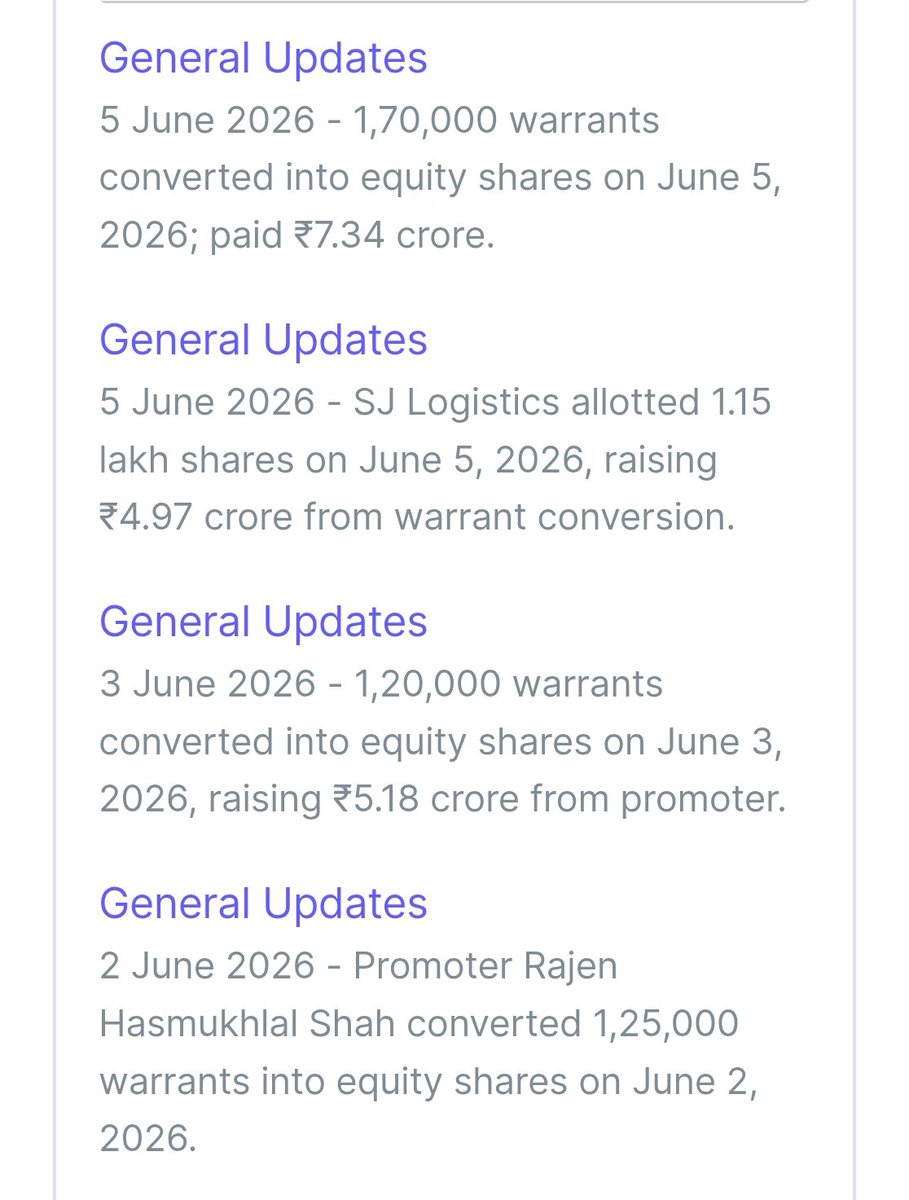

Further 1,15,000 warrants converted into shares by promoter

3rd time in last 5 days post results

Jun 3

SJ Logistics

#SJLog

#SJLogistics

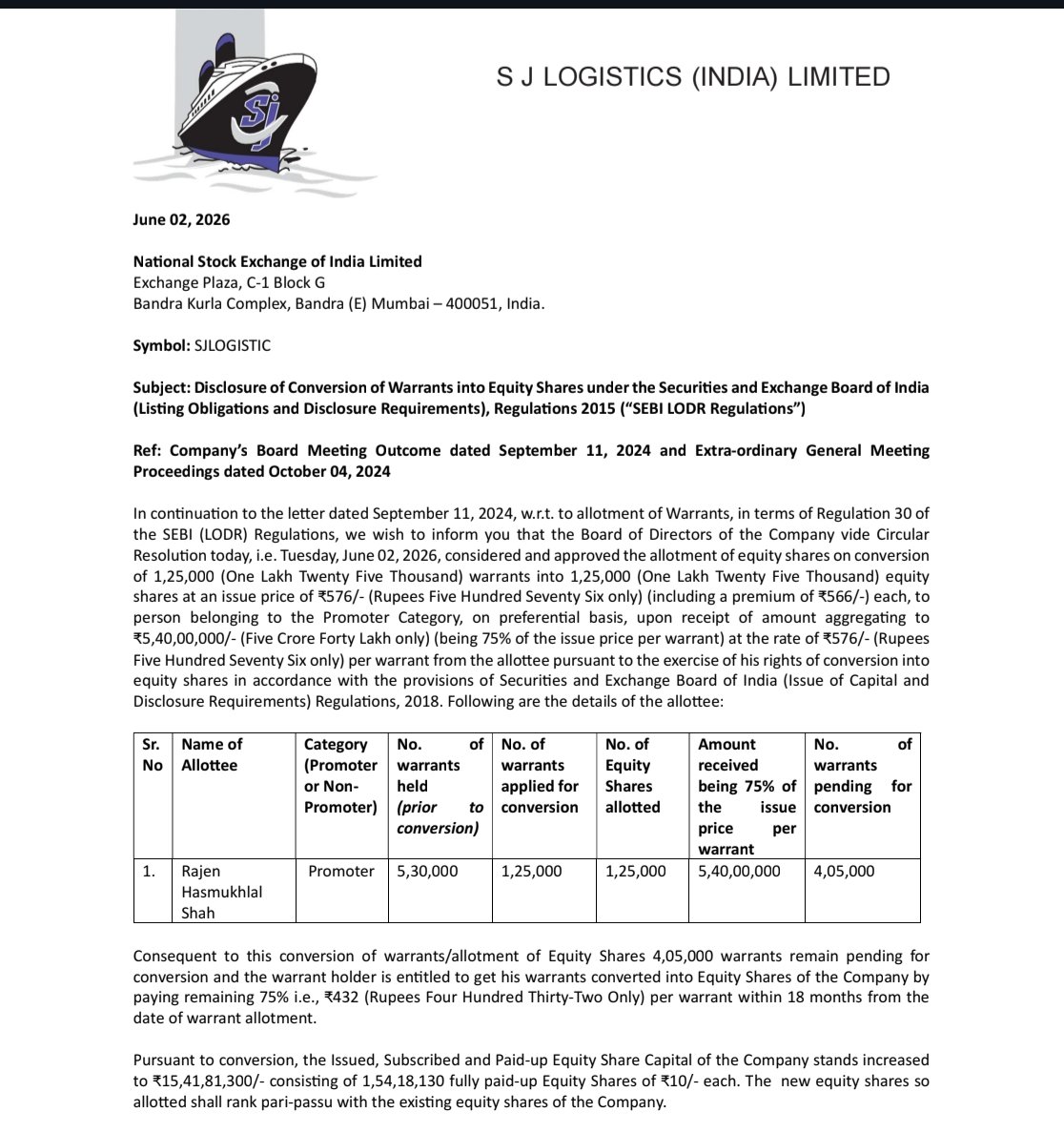

2,45,000 shares converted by promoter at 576rs

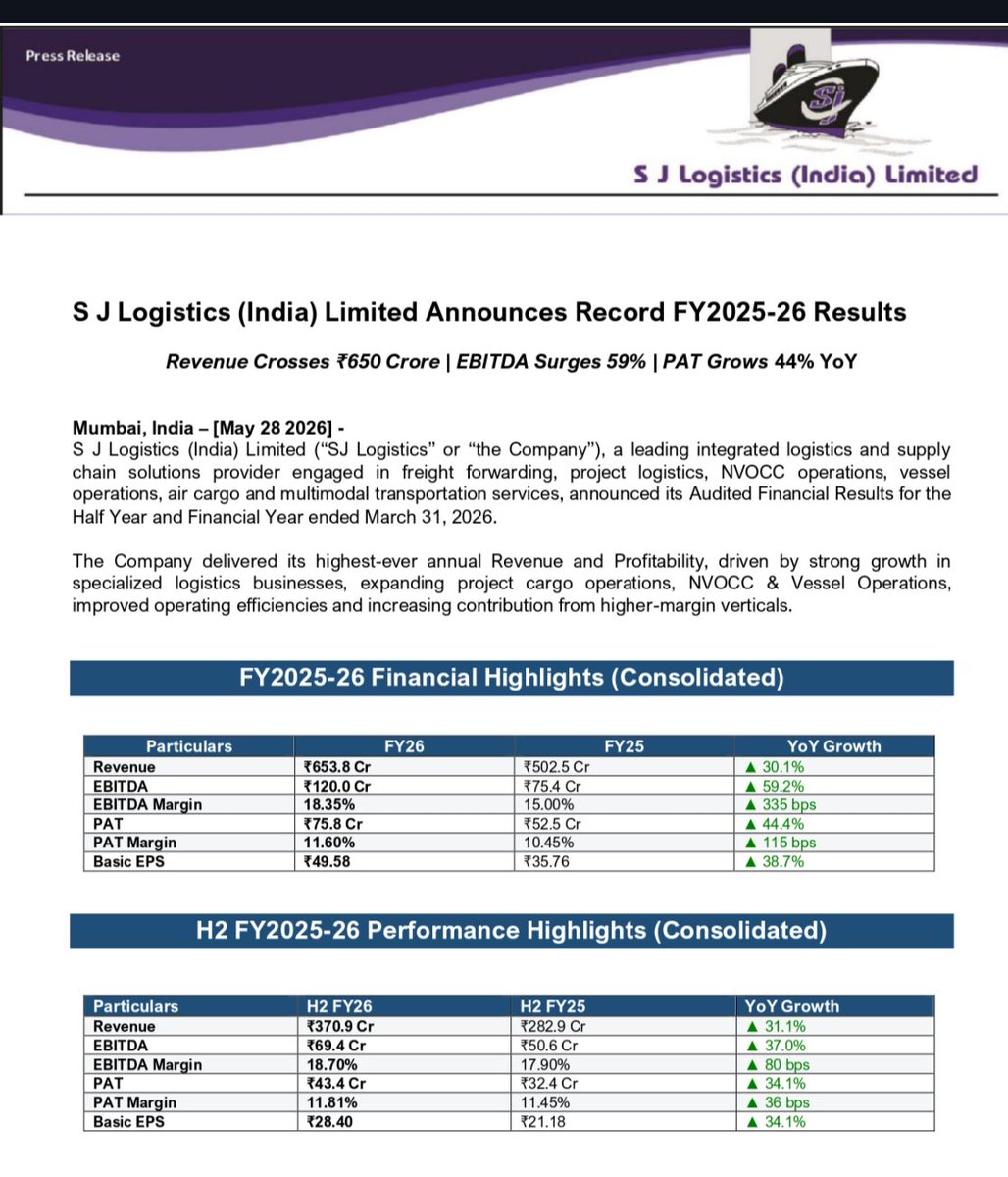

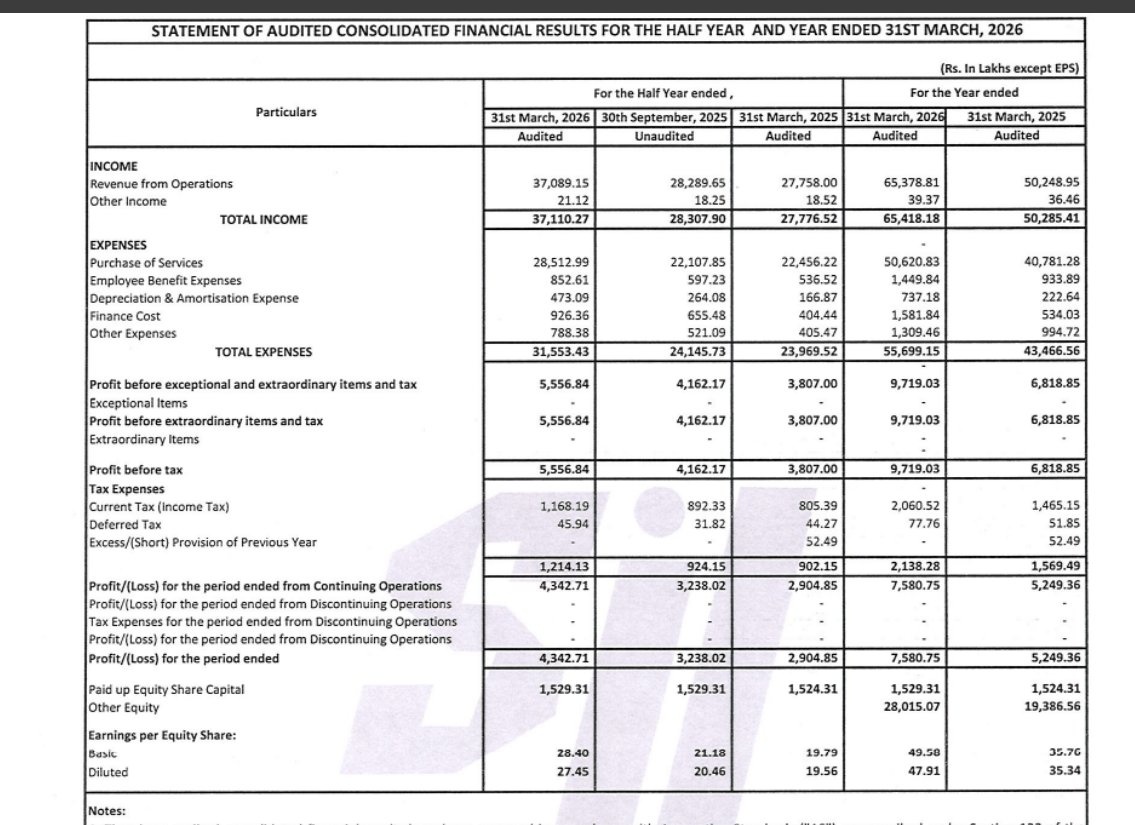

H2FY26:

Rev at 371cr⏫31%

EBITDA at 69cr⏫37%

OPM at 18.7% vs 17.9%

PAT at 43cr⏫34%

FY26:

Rev at 654cr⏫30%

EBITDA at 120cr⏫59%

OPM at 18.35% vs 15%

PAT at 76cr⏫44%

Valuations:

FY26 PAT 76cr

OCF at 21cr

Mkt cap 515cr

P/E 6.7x

EV/EBITDA at 5.2x

RoCE 32%

RoE 29%

D/E 0.38x

PEG at 0.06x

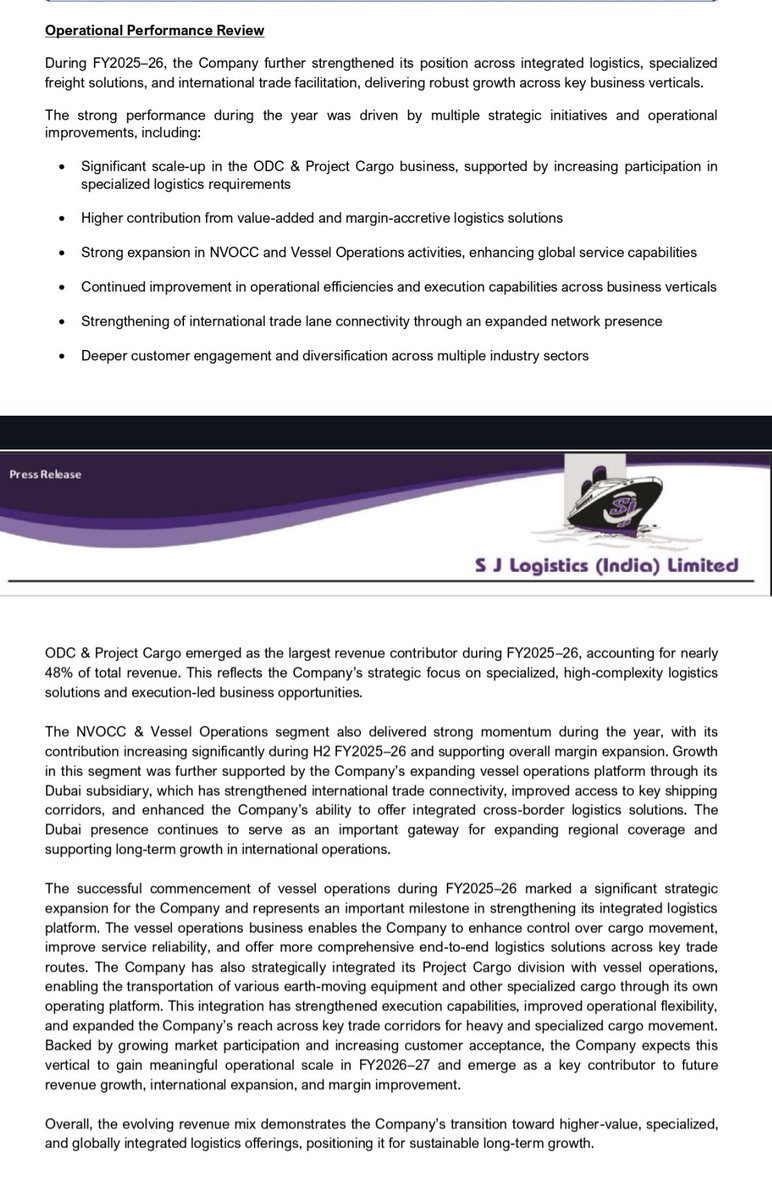

Scaling up NVOCC

Growth momentum should continue in FY27 with further scale up pf operations

Healthy orderbook in ODC and Project Cargo

Higher contribution from value added and margin accretive logistics business

International expansion

5

7

102

21,212

Effective logistics is about designing the right combination of air, ocean, and land transportation to meet business objectives without compromising efficiency.

#SJLogistics #SupplyChainManagement #GlobalTrade #FreightForwarding #LogisticsSolutions

1

1

180

TheMarathoner... retweeted

Growth isn’t accidental. It’s strategic.

Move smart. Grow stronger.

#SJLogistics #Logistics #Business #Growth #Expansion

1

1

3

263

Jun 8

#Q4FY26 concall pointers:

Knowledge Marine and Engineering

#KMEW

Q1FY27 is expected to be very strong as 50-60cr revenue is deferred from Q4FY26 to Q1FY27

Q1FY27 can do 100cr revenue with 40-43% OPM which is more than 2x over Q1FY26

30-35% CAGR on topline for FY27 and FY28

1400-1500cr orderbook with good pipeline

TVS Supply Chain Solutions

#TVSSCS

#TVSSupplyChain

Q4FY26 was a Highest ever quarter in terms of revenue, EBITDA, PBT and PAT in comps history

Q4FY26 Rev ⏫21%,

EBITDA ⏫30% almost

Deal pipeline strong for FY27

New deal wins and business momentum robust

Mid teen revenue growth guidance with margin expansion

PBT margins to further improve

Swamy 3PL to contribute in FY27, EPS accretive

SJ Logistics

#SJLog

#SJLogistics

Promoter converts more warrants into equity

Last set of conversion

1,70,000 shares converted at 576/Share

Ajmera Realty

#Ajmera

Witnesses good amount of promoter buying in June

25% pre sales growth guidance for FY27

FY26 was a record year of growth

1

13

256

31,569

This World Environment Day, we celebrate the balance between global trade and environmental responsibility. Sustainable logistics isn't just a goal; it's the future.

#WorldEnvironmentDay #SJLogistics #SustainableLogistics #GreenLogistics #SupplyChain

1

2

305

Jun 3

SJ Logistics

#SJLog

#SJLogistics

2,45,000 shares converted by promoter at 576rs

H2FY26:

Rev at 371cr⏫31%

EBITDA at 69cr⏫37%

OPM at 18.7% vs 17.9%

PAT at 43cr⏫34%

FY26:

Rev at 654cr⏫30%

EBITDA at 120cr⏫59%

OPM at 18.35% vs 15%

PAT at 76cr⏫44%

Valuations:

FY26 PAT 76cr

OCF at 21cr

Mkt cap 515cr

P/E 6.7x

EV/EBITDA at 5.2x

RoCE 32%

RoE 29%

D/E 0.38x

PEG at 0.06x

Scaling up NVOCC

Growth momentum should continue in FY27 with further scale up pf operations

Healthy orderbook in ODC and Project Cargo

Higher contribution from value added and margin accretive logistics business

International expansion

4

11

114

37,514

May 31

#SME

#SJLOGISTICS

SJ Logistics posted solid results

Walk the talk management till now 🔥

Cash flow from operations also became positive 👍

Jan 1

SJ Logistics (India) Ltd: Scaling New Heights 🚢

Solid Q2 FY26!

- Revenue: ₹157.1 Cr ( 26.5% YoY)

- EBITDA: ₹28.4 Cr ( 61.4% YoY)

- PAT: ₹18.1 Cr ( 42.5% YoY)

Operational leverage is kicking in, with profit growth significantly outpacing revenue.

A deep dive into it. 🧵

1

1

6

1,715

May 29

SJ Logistics (India) Ltd

Sector: Logistics & Supply Chain Solutions

Author: @fearfullygr33dy

SJ Logistics (SJL) is pivoting from pure freight forwarding to high-margin Project Cargo and integrated Vessel Operations.

Earnings Inflection: 44% PAT growth in FY26.

Valuation Gap: Trading at 6.8x PE despite 30% revenue CAGR.

Operational Pivot: Expansion into UAE-based vessel chartering to capture higher-margin cargo flows.

Things to watch out for:

Cash Flow Disconnect: FY26 CFO is only 28% of PAT. Profitability is not translating to cash; it is trapped in receivables. And in most cases this is because of large, repeat institutional customers being extend a larger credit line. And eventually trims bottomline. By 16Cr this year. However, receivable days in the 120–170 day range appears to be an industry-specific for project cargo, freight forwarding, and multimodal logistics in India.

Receivables Pressure: Receivables days at 134 days. Revenue growth is technically debt-funded (₹77 Cr increase in borrowings).

Rerating aspects:

Mainboard Migration: Necessary to attract institutional credit lines. And possibly have peer mainboard valuations.

CFO/PAT Conversion: Must improve from 28%. But mgmt says its by choice.

UAE Subsidiary: Success in chartering operations will confirm margin expansion thesis.

View

High-conviction inflection play. Current 6.8x PE offers significant safety, but the working capital cycle is the primary structural bottleneck. Monitor cash conversion ruthlessly.

Our Estimates:

Revenue | FY26 ₹653.8 Cr | FY27 Est ₹787.5 Cr

PAT | FY26 ₹75.8 Cr | FY27 Est ₹91.35 Cr

These are very conservative estimates because of 50% execution efficiency caused by capital stuck in receivables vs the real revenue capability of ₹1,575 Cr.

SEBI Disclaimer: For research only. SME stocks carry high liquidity risk. Not a SEBI-registered advisor. Consult a pro.

#SJLogistics #sme

1

11

1,130

May 29

SJ Logistics

#SJLogistics

#SJLog

Continues to deliver with good cash flows

Disciplined execution

Consistent performer with good H2FY26

Good growth vs H1FY26 and H2FY25

Rev at 371cr vs 278cr, H1 at 283cr

PBT at 56cr vs 38cr, H1 at 42cr

PAT at 42cr vs 29cr, H1 at 32cr

FY26 PBT at 97cr vs 68cr

FY27 PAT at 76cr vs 52cr

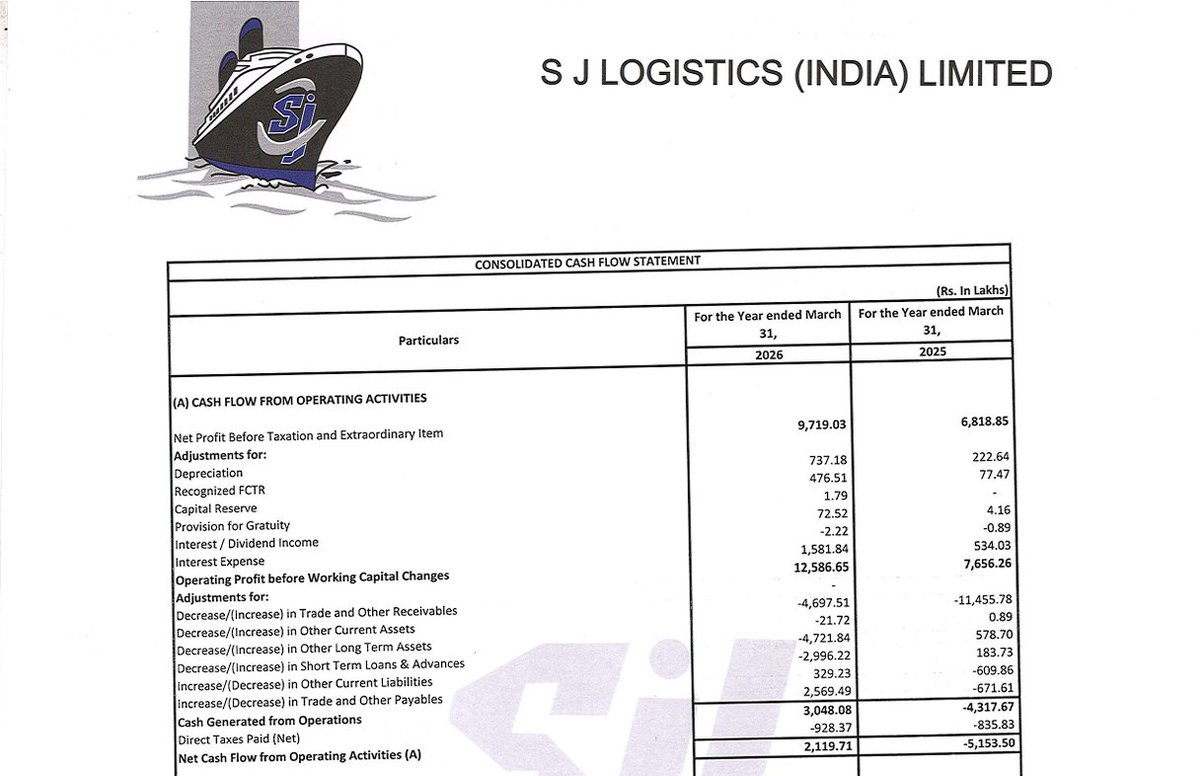

OCF at 21cr vs -52cr

Sathlokhar Synergies

#Sathlokhar

#SSEGL

Good Q4FY26

Good FY26

Highest ever set with good margin expansion

Rev at 277cr vs 186cr, Q3 at 271cr

EBITDA at 43cr vs 20cr⏫115%

OPM at 15.3% vs 10.6%

PBT at 41cr vs 21cr, Q3 at 39cr

PAT at 30cr vs 18cr, Q3 at 29cr

FY26 Rev at 820cr vs 370cr

FY26 PBT at 110cr vs 49cr

FY26 PAT at 82cr vs 34cr

More than 100% growth across rev, EBITDA, PBT and PAT

OCF at -162cr vs -96cr mainly due to inventory increase

Inventory at 138cr vs 51cr ,most of it should be executed in FY27

Receivables reduce sharply at 77cr vs 118cr

Other current assets spike up to 339cr vs 49cr. This needs clarification in tomorrow's concall

Hi Tech Pipes

#HiTechPipes

Good revenue uptick

Decent EBITDA growth

Higher finance costs and depreciation lead to flat PBT

Rev at 1480cr vs 733cr⏫102% YoY,⏫38% QoQ

EBITDA at 46cr vs 35cr⏫33% YoY,⏫11% QoQ

Finance costs at 16cr vs 7cr

Depreciation at 8cr vs 4cr

OPM down at 3.1% vs 4.7%

PBT flat at 23cr

Vinyas Innovative Technologies

#Vinyas

Good H2FY26 with good growth vs H1FY26 and H2FY25

Rev at 302cr vs 247cr, H1 at 212cr

EBITDA at 37cr vs 24cr, H1 at 21cr

PBT at 30cr vs 17cr, H1 at 13cr

OCF at -21cr vs 14cr

Danlaw Technologies

#Danlaw

Good Q4FY26

Rev at 80cr vs 62cr, Q3 at 62cr

PBT at 13cr vs 9cr, Q3 at 6cr

PAT at 9.5cr vs 6.5cr, Q3 at 4.4cr

OCF at 21cr vs 10cr

Taj GVK Hotels

#TajGVK

Good Q4FY26 with good QoQ and YoY uptick across all parameters

Rev at 159cr vs 125cr, Q3 at 136cr

PBT at 43cr vs 34cr, Q3 at 40cr

OCF at 173cr vs 116cr

#AshokLeyland

Rev at 14075cr vs 11857cr, Q3 at 11478cr

PBT at 1909cr vs 1671cr, Q3 at 1373cr

PAT at 1404cr vs 1245cr, Q3 at 796cr

OCF at 4792cr vs 7819cr

#EmamiPaper

Good Q4FY26 with solid QoQ and YoY uptick across profitability metrics

Rev at 496cr vs 474cr, Q3 at 500cr

Other income at 14cr vs 2cr

PBT at 46cr vs 4cr, Q3 at 29cr

PAT at 32cr vs 4cr, Q3 at 17cr

OCF at 197cr vs 44cr

#UdayJewellery

Solid Q4FY26 with big QoQ and YoY uptick across all parameters

Rev at 226cr vs 106cr, Q3 at 204cr

PBT at 15cr vs 3cr, Q3 at 8cr

PAT at 11cr vs 2cr, Q3 at 6cr

Inventory at 205cr vs 117cr

OCF at -107cr vs -18cr

#CordsCable

Rev at 266cr vs 233cr, Q3 at 236cr

PBT at 11cr vs 6cr, Q3 at 6.5cr

PAT at 8.2cr vs 4.3cr, Q3 at 5cr

OCF at 43cr vs 14cr

#PartyCruisers

Rev at 111cr vs 84cr, H1 at 36cr

PBT at 14cr vs 8.6cr, H1 at 3cr

PAT 10cr vs 6cr, H1 at 2.6cr

#IndNippon

India Nippon Electricals

Rev at 299cr vs 233cr, Q3 at 272cr

PBT at 35cr vs 25cr, Q3 at 33cr

OCF at 40cr vs 50cr

#Technocraft

Rev at 712cr vs 702cr, Q3 at 662cr

Good margin expansion QoQ and YoY

Other income at 14cr vs 29cr

PBT at 105cr vs 92cr, Q3 at 74cr

OCF at 243cr vs 276cr

#LordsChloro

Rev at 98cr vs 80cr, Q3 at 94cr

PBT at 6.2cr vs 3.6cr, Q3 at 4.1cr

OCF at 27cr vs 9cr

#ShivamChemicals

Rev at 152cr vs 130cr, H1 at 132cr

PBT at 5.2cr vs 2.1cr, H1 at 2.5cr

PAT at 4.2cr vs 1.5cr, H1 at 2cr

OCF at -6cr vs -14cr

#ThemisMed

Rev at 77cr vs 71cr, Q3 net 90cr

PBT at 9cr vs loss, Q3 at 10cr

9cr includes 7cr from associates/JV

OCF at -3cr vs 35cr

#BLKashyap

Rev at 364cr vs 294cr, Q3 at 324cr

Other income at 16cr vs 4cr

PBT at 27cr vs loss, Q3 at 16cr

OCF at 109cr vs 87cr

#SourceNaturalFoods

Rev at 23cr vs 18cr, Q3 at 22cr

PBT at 2cr vs 0.8cr, Q3 at 1.1cr

OCF at -2.4cr

#Balurghat

Rev at 32cr vs 26cr, Q3 at 28cr

PBT at 4.8cr vs 0.8cr, Q3 at loss

OCF at -4cr vs -8cr

Decent:

#Alkem-EBITDA below ests

#Hawkins-Rwv⏫18%, PBT ⏫14%

#HMVL

#KCP-Rev⏫6%, PBT ⏫15%

#PurpleWaveInfo-Rev flat, PBT ⏫36%

#AgarwalToughGlass-PBT⏫15%

#NaharSpng-PBT⏫11%

3

649

May 28

🚨 Q4FY26 Earnings Heat (27–28 May) - More Record Quarters Rolling In🔥

💥 BLOCKBUSTERS

• #AdityaInfotech #CPPlus: Rev ₹1422Cr | PAT ₹169Cr ( 207%)

→ Record quarter strong FY27 growth guidance

• #UniVastu: Rev ₹109Cr | PAT ₹10Cr ( 150%)

→ Highest ever quarter with healthy orderbook

• #SSEGL: EBITDA 115% | PAT ₹30Cr

→ Massive FY26 growth margin expansion

• #GPEco: FY26 PAT ₹43Cr vs ₹10Cr

→ Explosive H2 growth momentum

• #ShraddhaPrime: Rev ₹186Cr vs ₹48Cr | PAT ₹23Cr

→ Strong execution-led growth

• #LumaxIndustries: EBITDA 65% | OPM 10.3%

→ Highest ever quarter OCF ₹372Cr

✅ STRONG & SOLID

• #SJLogistics: PAT ₹42Cr

→ Consistent growth positive OCF

• #UdayJewellery: Rev ₹226Cr vs ₹106Cr

→ Strong QoQ/YoY momentum

• #AVTNPL: PAT ₹22Cr

→ Healthy profitability growth

• #TimeTechnoplast: PAT ₹134Cr

→ Stable execution quarter

• #GPPL: PAT ₹142Cr

→ Strong cash flow ₹510Cr

• #HiTechPipes: Revenue 102% YoY

→ Massive scale-up in business

• #TajGVKHotels: Strong hospitality growth

→ Healthy QoQ/YoY across metrics

• #EmamiPaper: PAT ₹32Cr vs ₹4Cr

→ Sharp profitability recovery OCF ₹197Cr

• #FrontierSprings: PAT ₹17Cr

→ Consistent growth visible

• #VinyasInnovative: PBT ₹30Cr

→ Strong H2 execution

📈 Other Strong Names:

#UniAbex #MarineElectricals #ParagonFine #Kapston #EPSIndia #EuroIndiaFresh #AdiSoft

Which stock impressed you the most? 👀

#Q4FY26 #Investing #LNPR #EarningsSeason

4

12

64

10,262

May 28

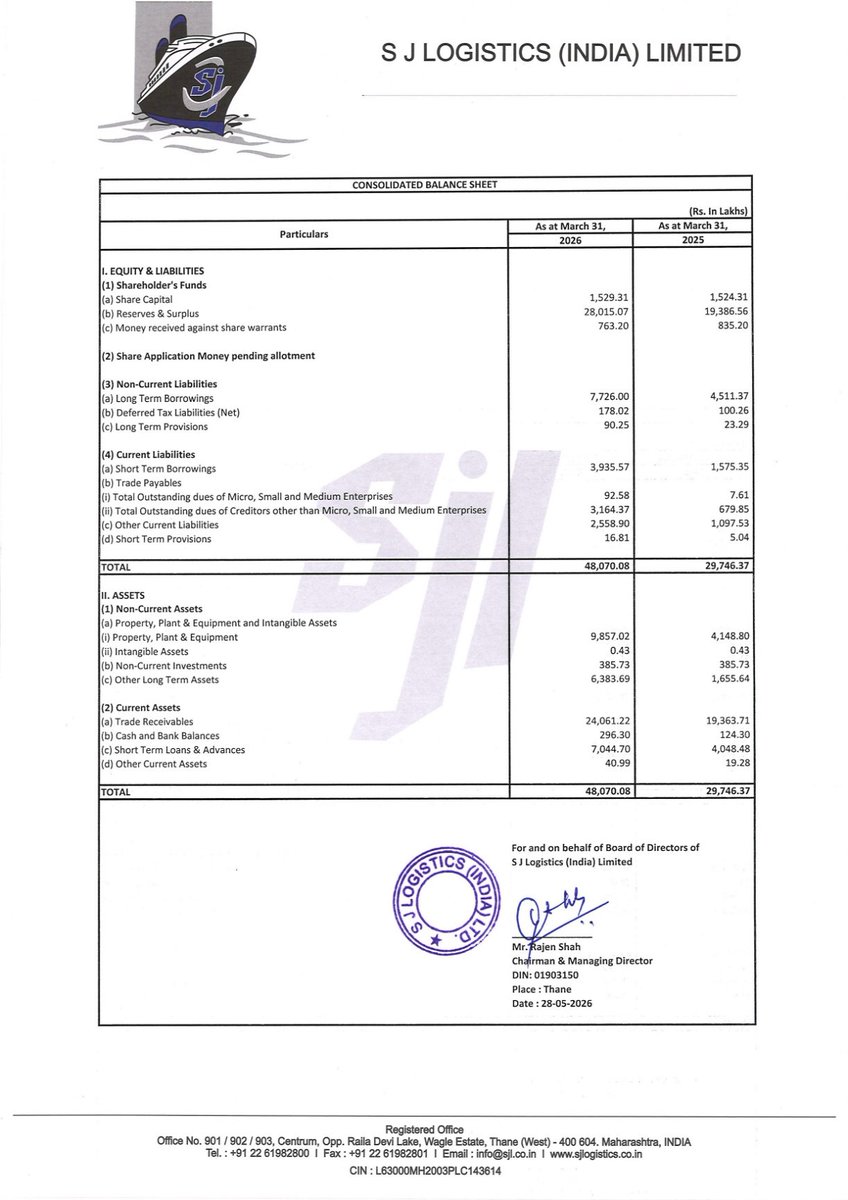

S J LOGISTICS (INDIA) LTD H2FY26 RESULTS

#H2Results #FY26 #StockMarket #Nifty #SJLogistics

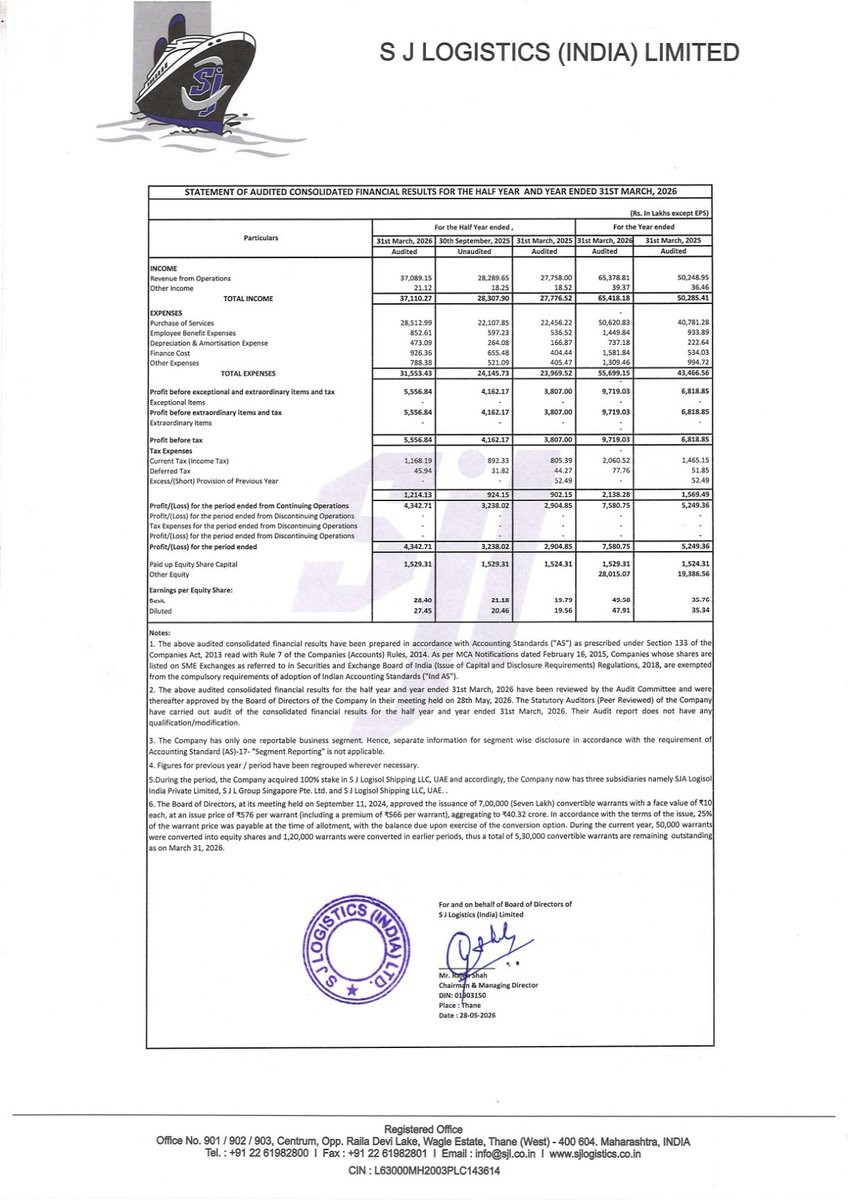

🟢 Revenue: ₹370.89 Cr vs ₹277.58 Cr

( 33.62% YoY)

🟢 EBITDA: ₹69.35 Cr vs ₹43.60 Cr

( 59.07% YoY)

🟢 EBITDA Margin: 18.70% vs 15.71% YoY

🟢 PBT: ₹55.57 Cr vs ₹38.07 Cr

( 45.96% YoY)

🟢 PAT: ₹43.43 Cr vs ₹29.05 Cr

( 49.50% YoY)

🟢 Other Income: ₹0.21 Cr vs ₹0.19 Cr YoY

🗣️ Management Update: The company delivered strong half-yearly growth across revenue and profitability, supported by healthy expansion in logistics demand and improved operating efficiency. Margin expansion also reflects better cost control and scale benefits.

Overall performance indicates consistent business momentum with improving earnings quality.

Can S J Logistics sustain this high double-digit growth in FY27? 🤔

#LogisticsStocks #SMEStocks #IndianStockMarket #StocksToWatch

5

5

354

🚢 S J Logistics FY26 Results

💰 Revenue ₹654 Cr 🔼30% YoY

📈 PAT ₹75.8 Cr 🔼43% YoY

🧾 EPS ₹49.5 | Diluted ₹47.5

💎At ₹339, P/E ~7x

🌍 Clean audit UAE expansion

Recently added to my portfolio✨

⚠️ Watch: receivables, debt & cash conversion

#SJLogistics #shipping #SMEs

1

1

5

679

#SJLogistics FY26: Revenue ₹653.7 Cr ( 30%), EBITDA ₹120.4 Cr ( 59%), PAT ₹75.8 Cr ( 44%). PAT margin expanded to 11.6%. OCF stayed positive at ₹21.2 Cr but moderated YoY. At CMP ₹340, FY26 diluted PE ~7.2x. Strong growth, cash-flow watch.

May 28

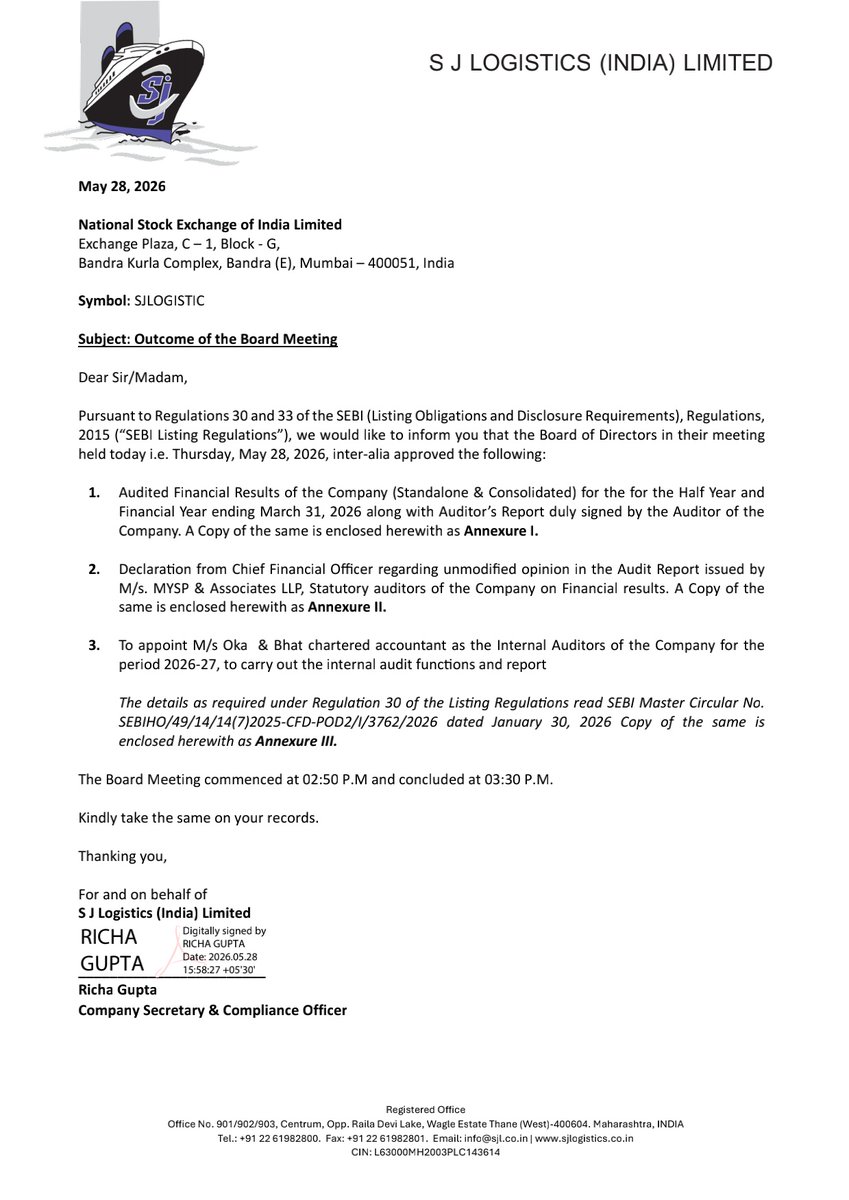

📌 S J Logistics (India) Limited informed the exchange about its approval for the financial results for the period ended March 31, 2026. #SME #SJLOGISTIC 📄🧾

1

14

1,056

🚨#SJLogistics FY26 results:

FY26 vs FY25

👉Revenue 654cr vs 502cr ⬆️ 30% YOY

👉PAT 76cr vs 53cr ⬆️ 43% YOY

👉EPS ₹47.91 vs ₹35.34 ⬆️ 37% YOY

👉Stock trades at 6.8 PE

👉Trade receivables 240cr vs 193cr👎

👉Borrowings increased👎

👉Cashflow from operations 21cr vs -51cr👍

28 Aug 2025

🚨#SJLogistics Q1 FY26 concall -

Management guided for 35-40% Yoy growth and PAT margins increase from 11% to 12-13% in FY26

2

19

2,572

May 28

S J Logistics (India) Limited (SME) H2FY26 Results:-

#H2FY26 #Stockmarket #Nifty #SJlogistics

H2FY26 vs H2FY25

Revenue 370.89 Cr vs 277.58 Cr ( 33.62% YoY)

EBITDA 69.35 Cr vs 43.60 Cr ( 59.07% YoY)

EBITDA Margin 18.70% vs 15.71% YoY

PBT 55.57 Cr vs 38.07 Cr ( 45.96% YoY)

PAT 43.43 Cr vs 29.05 Cr ( 49.50% YoY)

Other Income 0.21 Cr vs 0.19 Cr YoY

1

6

3,852