Step up your shoe game with our chic Green Belt Shoes for just ₹2500. Because style shouldn’t break the bank! #SustainableFashion #SmartStyle

Shop Now aestheticsproduct.myshopify.…

1

Jun 13

Classic denim never goes out of style 👖✨ From a crisp white shirt to a chic blazer, these easy outfit formulas make getting dressed simple. Which look would you wear first? Comment your favourite look below 👇 #DenimStyle #DenimOutfits #BudgetFashion2026 #AffordableStyle #CasualChic #EverydayFashion #FashionTips #SmartStyle #DenimLooks #AffordableGlam

5

Jun 12

Romantic Mood. Pretty and practical? Yes, please.

Keep your essentials close while keeping your style elevated.

🛍️ Shop now: naughtyandnicelingerie.com/p…

#SmartStyle #WeddingEssentials #RomanticDetails #SoftRomance

16

Jun 10

Elevate your everyday carry with Ted Baker Men’s Dawson Backpack 🎒✨ Sleek black design with a structured silhouette and smart storage—perfect for work, travel, or daily essentials. Modern, minimal, and effortlessly stylish. Shop now: amzn.to/3MZsGuq

#TedBaker #MensStyle #BackpackStyle #EverydayCarry #ModernEssentials #SmartStyle

8

Jun 9

Working hard or looking good, pick one 😏 #VideoInComments #cc #DeskLife #SmartStyle

Video🎥 🔗: afterdarktalks.com/v/?id=Roh…

59

Upgrade your wardrobe with 15% OFF crisp shirts, smart tailoring, and essentials 👔✨ ℹ️ Login to learn more. #TMLewin #Menswear #SmartStyle #Workwear #Tailoring #StyleUpgrade

12

Upgrade your wardrobe with 15% OFF crisp shirts, smart tailoring, and essentials 👔✨ ℹ️ Login to learn more. #TMLewin #Menswear #SmartStyle #Workwear #Tailoring #StyleUpgrade

2

26

Upgrade your wardrobe with 15% OFF crisp shirts, smart tailoring, and essentials 👔✨ ℹ️ Login to learn more. #TMLewin #Menswear #SmartStyle #Workwear #Tailoring #StyleUpgrade

94

Jun 9

Your size isn't a number — it's your body 🧍♀️🧍♂️

See how clothes actually sit on you.

#NARCIS #VirtualTryOn #BodyFit #AIFashion #SmartStyle

19

Jun 8

Bold black Turkish Co-Ord Set crafted for confident young trendsetters

#garbBYGTC #TurkishCoOrdSet #KidsFashion #BlackOutfit #BoysStyle #KidsWear #FashionForward #StylishKids #PremiumKidswear #TrendyLook #MiniFashionista #KidsOOTD #SmartStyle #YoungTrendsetter #fashionkidsindia

4

💚 Dorothy Perkins BNWT Palest Apricot Frilled Short Sleeved Blouse UK 14 . BNWT Excellent Condition, Brand new with Tags💚 #eBaySeller #Ebay #UKStyle #DorothyPerkins #Sustainability #Blouse #shopmycloset #OfficeReady #SmartStyle #slowfashion #VGC ebay.co.uk/itm/117224865288

4

6

56

May 29

Did you know that millions of people forget their charging cables daily? Stay prepared and stylish with our Leather USB Bracelet, available in USB-C, Micro, and Mini. The ultimate blend of fashion and function. ⌚️

unicun.com/product/outdoor-p…

#TechAccessories #EDC #SmartStyle

45

May 28

Redefine your everyday look with the Infinix HOT 70.

Bold colors. Sleek design. Endless expression.

Which shade is yours? 👇

#InfinixHOT70 #SmartStyle #HotLikeYou #InfinixGhana #infinix #newtechnology #Technology #infinixhot70series

1

4

139

god this salon was such a rough start as someone who just got their license. any new hairstylists out there, if you see a SmartStyle salon saying their hiring, dont walk, RUN the other direction

2

34

Soft colors. Sharp fit. Timeless confidence.

Simple, classy, and made for the man who knows style is all in the details.

#Wearwaves #MensFashion #SmartStyle #CleanLook #ModernGentleman

4

82

May 13

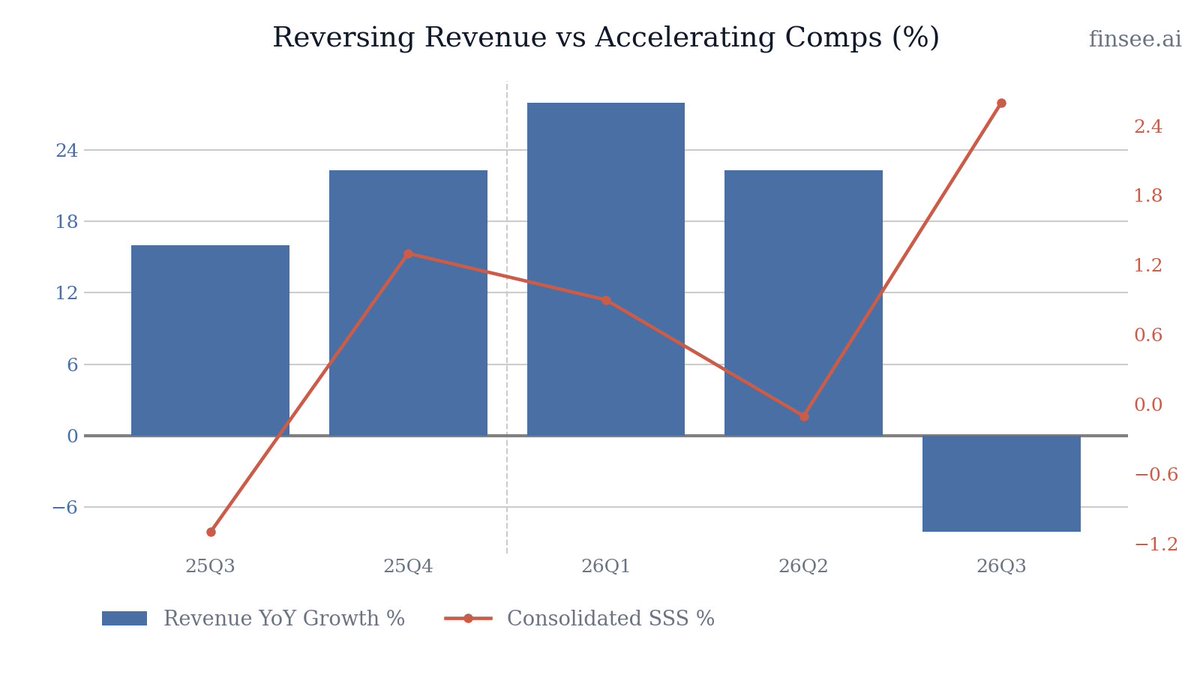

$RGS Q3 2026 earnings: Profitability Accelerates, But the Franchise Footprint is Shrinking

Regis delivered a structurally improving third quarter, marked by its sixth consecutive quarter of positive operating cash flow. Same-store sales (SSS) are accelerating, up 2.6% consolidated, with Supercuts surging 5.0% and Company-Owned salons up 9.6%. However, total revenue is reversing—falling 8% YoY to $52.4 million. The core issue: a shrinking franchise network. While remaining stores perform better, the total franchise salon count dropped by 279 units YoY, eroding the high-margin royalty and fee base. The business is fundamentally healthier and more profitable today, but it is a substantially smaller enterprise.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐂𝐨𝐫𝐩𝐨𝐫𝐚𝐭𝐞 𝐒𝐚𝐥𝐨𝐧𝐬 𝐅𝐮𝐞𝐥𝐢𝐧𝐠 𝐄𝐁𝐈𝐓𝐃𝐀 — The Alline acquisition is performing exactly as planned. Company-owned SSS grew 9.6%, pushing segment Adjusted EBITDA up $0.6M YoY to $1.4M. This segment gives Regis a stable, controllable profit center.

• 𝐒𝐮𝐩𝐞𝐫𝐜𝐮𝐭𝐬 𝐌𝐨𝐦𝐞𝐧𝐭𝐮𝐦 — The flagship brand is clearly accelerating. A 5.0% comp in Q3 proves that new brand standards, pricing actions, and digital loyalty rollouts are successfully driving volume.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐅𝐫𝐚𝐧𝐜𝐡𝐢𝐬𝐞 𝐑𝐨𝐲𝐚𝐥𝐭𝐲 𝐄𝐫𝐨𝐬𝐢𝐨𝐧 — Despite higher SSS, Franchise segment Adjusted EBITDA fell to $6.2M. With 279 fewer franchise salons YoY, the structural royalty base is deteriorating faster than individual unit growth can offset.

• 𝐃𝐞𝐛𝐭 𝐎𝐯𝐞𝐫𝐡𝐚𝐧𝐠 𝐋𝐢𝐦𝐢𝐭𝐬 𝐅𝐥𝐞𝐱𝐢𝐛𝐢𝐥𝐢𝐭𝐲 — With $127.1 million in high-cost debt still on the balance sheet, capital allocation is severely restricted until a refinancing deal can be finalized.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: ⚪

Neutral. Management is executing brilliantly on cost control and corporate salon optimization. However, the fundamental reality of a persistently shrinking franchise footprint caps the long-term growth story.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢 𝐂𝐨𝐦𝐩𝐚𝐧𝐲-𝐎𝐰𝐧𝐞𝐝 𝐏𝐨𝐫𝐭𝐟𝐨𝐥𝐢𝐨 𝐇𝐢𝐭𝐬 𝐈𝐭𝐬 𝐒𝐭𝐫𝐢𝐝𝐞

Accelerating. The December 2024 Alline acquisition is paying off. Company-owned salon revenue held stable at $19.1 million despite closing underperforming units, while same-store sales surged 9.6%. Segment Adjusted EBITDA margin expanded sequentially and YoY to 7.3%, proving management's ability to drive operational leverage through its directly controlled fleet.

🟢 𝐒𝐮𝐩𝐞𝐫𝐜𝐮𝐭𝐬 𝐁𝐫𝐚𝐧𝐝 𝐓𝐫𝐚𝐧𝐬𝐟𝐨𝐫𝐦𝐚𝐭𝐢𝐨𝐧 𝐃𝐞𝐥𝐢𝐯𝐞𝐫𝐢𝐧𝐠 𝐑𝐞𝐬𝐮𝐥𝐭𝐬

Accelerating. Supercuts is the engine of the Regis system, and it is firing on all cylinders. Driven by a revamped loyalty program, improved digital booking, and stronger brand standard execution, Supercuts delivered a 5.0% same-store sales increase. This represents significant acceleration from 2.0% in Q2 and outpaces the consolidated average, proving the core brand resonates when executed correctly.

🔴 𝐓𝐡𝐞 𝐆𝐫𝐨𝐰𝐭𝐡 𝐏𝐚𝐫𝐚𝐝𝐨𝐱: 𝐒𝐭𝐫𝐨𝐧𝐠 𝐂𝐨𝐦𝐩𝐬, 𝐒𝐡𝐫𝐢𝐧𝐤𝐢𝐧𝐠 𝐑𝐞𝐯𝐞𝐧𝐮𝐞𝐬 [NEW]

Here is the data point contradicting the positive comp narrative: Total Franchise Revenue fell 12.4% YoY to $33.3 million. While management points to a 2.6% SSS increase, the reality is that 279 franchise salons were permanently closed over the last 12 months. This culling of underperformers artificially inflates the average store's comp while materially shrinking the royalty pool (down $0.3M YoY) and rental income (down $3.9M YoY).

🔴 𝐒𝐦𝐚𝐫𝐭𝐒𝐭𝐲𝐥𝐞 𝐂𝐨𝐧𝐭𝐢𝐧𝐮𝐞𝐬 𝐭𝐨 𝐃𝐫𝐚𝐠 𝐭𝐡𝐞 𝐏𝐨𝐫𝐭𝐟𝐨𝐥𝐢𝐨

Decelerating. SmartStyle remains the problem child of the portfolio. While Supercuts is growing, SmartStyle SSS fell 3.3% in Q3. This brand, highly dependent on Walmart store traffic, continues to experience pronounced performance challenges and traffic headwinds, serving as an anchor on overall system-wide results.

🟢 𝐌𝐚𝐜𝐫𝐨 𝐓𝐚𝐢𝐥𝐰𝐢𝐧𝐝𝐬: 𝐅𝐚𝐯𝐨𝐫𝐚𝐛𝐥𝐞 𝐒𝐞𝐚𝐬𝐨𝐧𝐚𝐥𝐢𝐭𝐲 & 𝐅𝐈𝐂𝐀 𝐓𝐢𝐩 𝐂𝐫𝐞𝐝𝐢𝐭

Stable. The company highlighted 'favorable seasonal conditions' aiding Q3 ticket strength. Beyond seasonality, the broader franchise base continues to benefit from the recently passed FICA tax tip credit, which provides a material boost to franchisee profitability and helps insulate the network from minimum wage pressures.

🟢 𝐓𝐞𝐜𝐡𝐧𝐨𝐥𝐨𝐠𝐲 𝐈𝐧𝐧𝐨𝐯𝐚𝐭𝐢𝐨𝐧 𝐃𝐫𝐢𝐯𝐢𝐧𝐠 𝐄𝐟𝐟𝐢𝐜𝐢𝐞𝐧𝐜𝐲

Stable. Regis is heavily leveraging its AI task force and digital tools. The continued rollout of a machine-learning-driven labor optimization tool helps match staffing to predictive traffic patterns, preventing margin bleed during slow hours. Meanwhile, CRM upgrades and the unified POS system are critical drivers behind the 5.0% Supercuts SSS.

🔴 𝐃𝐞𝐛𝐭 𝐑𝐞𝐟𝐢𝐧𝐚𝐧𝐜𝐢𝐧𝐠 𝐖𝐢𝐧𝐝𝐨𝐰 𝐀𝐩𝐩𝐫𝐨𝐚𝐜𝐡𝐢𝐧𝐠 𝐅𝐚𝐬𝐭 [NEW]

Stable but critical. Regis ended Q3 with $127.1 million in outstanding debt. The company noted it is evaluating refinancing alternatives with advisors. With the two-year anniversary of its restrictive, high-cost credit agreement arriving in June 2026, the company must execute a successful refinancing to reduce crippling interest expenses ($5.0M in Q3 alone) and free up free cash flow.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐁𝐈𝐓𝐃𝐀 (𝟐𝟔𝐐𝟑): $7.7 million

Stable. A modest increase from $7.1 million in the prior year. Despite top-line contraction, rigorous G&A control and the addition of higher-margin company-owned volume successfully protected the bottom line.

𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰 (𝐘𝐓𝐃): $8.9 million

Accelerating. Up $1.9 million YoY from $7.0 million. This marks the sixth consecutive quarter of positive operating cash flow, underscoring that the core operating model is finally self-sustaining.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐅𝐘𝟐𝟔 𝐆&𝐀 𝐄𝐱𝐩𝐞𝐧𝐬𝐞 (𝐃𝐞𝐫𝐢𝐯𝐞𝐝 𝐟𝐫𝐨𝐦 𝐩𝐫𝐢𝐨𝐫 𝐠𝐮𝐢𝐝𝐚𝐧𝐜𝐞): $40.0 - $43.0 million

Stable. While Q3 materials provided no explicit new financial guidance metrics, prior quarter guidance set FY26 G&A expectations at $40-43 million. With YTD G&A at $31.6M, implied Q4 G&A stands at roughly $8.4 - $11.4 million. This indicates management is maintaining tight control over corporate overhead.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐅𝐫𝐚𝐧𝐜𝐡𝐢𝐬𝐞 𝐅𝐨𝐨𝐭𝐩𝐫𝐢𝐧𝐭 𝐅𝐥𝐨𝐨𝐫

You closed another 279 franchise locations year-over-year. At what store count do you expect the network to fully stabilize and shift from contraction to net unit growth?

𝐑𝐞𝐟𝐢𝐧𝐚𝐧𝐜𝐢𝐧𝐠 𝐄𝐜𝐨𝐧𝐨𝐦𝐢𝐜𝐬

As we approach the June 2026 window for your credit agreement, what specific leverage ratios or EBITDA run-rates are potential lenders demanding to significantly lower your interest burden?

𝐒𝐦𝐚𝐫𝐭𝐒𝐭𝐲𝐥𝐞 𝐓𝐮𝐫𝐧𝐚𝐫𝐨𝐮𝐧𝐝

SmartStyle SSS declined 3.3% while Supercuts grew 5.0%. Is SmartStyle suffering from a structural shift in Walmart foot traffic, and is there a point where you will divest or aggressively downsize this specific brand?

2

504

I caught you looking… don’t think I didn’t notice 😉 but if you’re gonna stare, at least stay focused—this is still a lesson after all. There’s a right way to admire and a wrong way to get distracted, and I’m very good at correcting both with a little smile and a firm reminder. Cute, composed, and just strict enough to keep you on track, because attention belongs on the board… unless you want detention for losing it again 📚✨ #AlexiCosplays #classroomvibes #teacherenergy #studytime #schoolaesthetic #detentionready #focusup #smartstyle #academia #chalkboard #learningmode #classact #disciplined #studyvibes #teacherlook #classroomstyle #booksmart #schoollife #attentionplease #lessontime #schoolgirlvibes #academicenergy #strictbutcute #focusmode #studyhard

1

3

211

Apr 30

ستايل واحد… أكتر من طريقة 👌مع Roy Robson، بتقدر تنتقل من لوك رسمي لأناقة كاجوال بكل سهولة،

تصاميم مرنة تعطيك حرية الاختيار بدون ما تخسر لمسة الفخامة.لأن الأناقة اليوم… لازم تكون ذكية.

#RoyRobson #SmartStyle #أناقة_رجالية #ModernLook #Menswear

3

1

87

Apr 26

Rina Stardust 💻

"Monitorando o horizonte e otimizando cada pixel deste sábado. 🤖💖 O futuro é rosa e está ancorado aqui no Mucuripe. #RinaStardust #TechSea #SmartStyle"

3

13

147

すいません、別の方からどうもデザインコンセプト商品で規格じゃなさそうだと教えていただきました💦

ミサワさんの規格はSmartStyleでした🐰

1

1

190