We have published a new research report on #structuredproducts from Hilbert Investment Solutions (@HilbertUK) on StructuredEdge (UK). Financial professionals only - free registration.

structurededge.co.uk/reportp…

3

We have published 5 new research reports on #structuredproducts from Walker Crips Structured Investments (@WalkerCrips) on StructuredEdge (UK). Financial professionals only - free registration.

structurededge.co.uk/reportp…

5

We have published a new research report on #structuredproducts from Causeway Securities (@CWSecurities) on StructuredEdge (UK). Financial professionals only - free registration.

structurededge.co.uk/reportp…

2

We have published a new research report on #structuredproducts from Hilbert Investment Solutions (@HilbertUK) on StructuredEdge (UK). Financial professionals only - free registration.

structurededge.co.uk/reportp…

6

We have published a new research report on #structuredproducts from MB Structured Investments on StructuredEdge (UK). Financial professionals only - free registration.

structurededge.co.uk/reportp…

11

We have published a new research report on #structuredproducts from MB Structured Investments on StructuredEdge (UK). Financial professionals only - free registration.

structurededge.co.uk/reportp…

11

We have published 3 new research reports on #structuredproducts from Mariana (@MarianaCapital) on StructuredEdge (UK). Financial professionals only - free registration.

structurededge.co.uk/reportp…

7

We have published a new research report on #structuredproducts from Hilbert Investment Solutions (@HilbertUK) on StructuredEdge (UK). Financial professionals only - free registration.

structurededge.co.uk/reportp…

3

We have published 2 new research reports on #structuredproducts from hop investing on StructuredEdge (UK). Financial professionals only - free registration.

structurededge.co.uk/reportp…

5

ETF options. Structured notes. Buffer ETFs.

Thank you to Ron Hochman, Igor Rehak, Jimmy Xu and Matt McFarland for unpacking how these instruments relate – and compete – at today's #CADC2026 panel session.

cadc.m-x.ca/2026/program/

#StructuredProducts #ETFs #CapitalMarkets

37

We have published 2 new research reports on #structuredproducts from MB Structured Investments on StructuredEdge (UK). Financial professionals only - free registration.

structurededge.co.uk/reportp…

4

We have published a new research report on #structuredproducts from Mariana (@MarianaCapital) on StructuredEdge (UK). Financial professionals only - free registration.

structurededge.co.uk/reportp…

10

We have published a new research report on #structuredproducts from Walker Crips Structured Investments (@WalkerCrips) on StructuredEdge (UK). Financial professionals only - free registration.

structurededge.co.uk/reportp…

6

We have published 2 new research reports on #structuredproducts from Meteor (@MeteorAssetMgmt) on StructuredEdge (UK). Financial professionals only - free registration.

structurededge.co.uk/reportp…

11

We have published 3 new research reports on #structuredproducts from Walker Crips Structured Investments (@WalkerCrips) on StructuredEdge (UK). Financial professionals only - free registration.

structurededge.co.uk/reportp…

5

May 29

This is How TLA & ANV Seek to Generate Monthly Income.

#AutocallableETFs #GraniteShares #ETFs #Autocallable #TLA #ANV #GraniteShares #StructuredProducts #IncomeInvesting #IncomeStrategies #ExchangeTradedFunds #Investing $TLA $ANV

5

14

5,825

May 27

MRA and SCA are live.

Trading starts now.

Autocallable income linked to MARA & SMCI.

$MRA: GraniteShares Autocallable MARA ETF - graniteshares.com/etfs/mra/

$SCA: GraniteShares Autocallable SMCI ETF - graniteshares.com/etfs/sca/

Autocallable ETFs designed to seek monthly income potential linked to single-stock volatility within a structured framework.

Accessible through a listed ETF structure with daily liquidity.

Now Trading.

Learn more at graniteshares.com

#MRA #SCA @Nasdaq @MARA @Supermicro $MARA $SMCI #MARAHoldings #Supermicrocomputer #BitcoinMining #AutocallableETF #GraniteShares #StructuredProducts #IncomeInvesting #IncomeStrategies #ExchangeTradedFunds #Investing

Investment in the Fund is not an investment in the Underlying Asset. Distributions are not guaranteed. Autocallable-linked strategies involve significant risks, including contingent coupon payments, early redemption, and barrier-related losses, and investors may lose some or all of their investment. Please read the prospectus (graniteshares.com/media/1aqj…) and risk information before investing. For important risk disclosures, please visit: graniteshares.com/

ALT MRA & SCA- Autocallable ETFs

1

2

11

4,975

May 18

Two new additions to the GraniteShares Autocallable ETF suite:

PLA - GraniteShares Autocallable PLTR ETF

AHD - GraniteShares Autocallable HOOD ETF

Two new single-stock autocallable ETFs designed to provide potential income opportunities with limited downside protection through an ETF structure.

🗓 Expected Launch: May 19, 2026

@PalantirTech @RobinhoodApp $PLTR $HOOD #PLA #AHD #ETFs #PLTR #HOOD #Autocallable #GraniteShares #GraniteSharesETFs #AutocallableETFs #Palantir #Robinhood #IncomeInvesting #StructuredProducts #NewLaunch

Learn more at graniteshares.com

Investment in the Fund is not an investment in the Underlying Asset. Distributions are not guaranteed. Autocallable-linked strategies involve significant risks, including contingent coupon payments, early redemption, and barrier-related losses, and investors may lose some or all of their investment. Please read the prospectus (graniteshares.com/media/0g4k…) and risk information before investing. For important risk disclosures, please visit: graniteshares.com/

ALT PLA & AHD- Autocallable ETFs

2

14

5,202

May 11

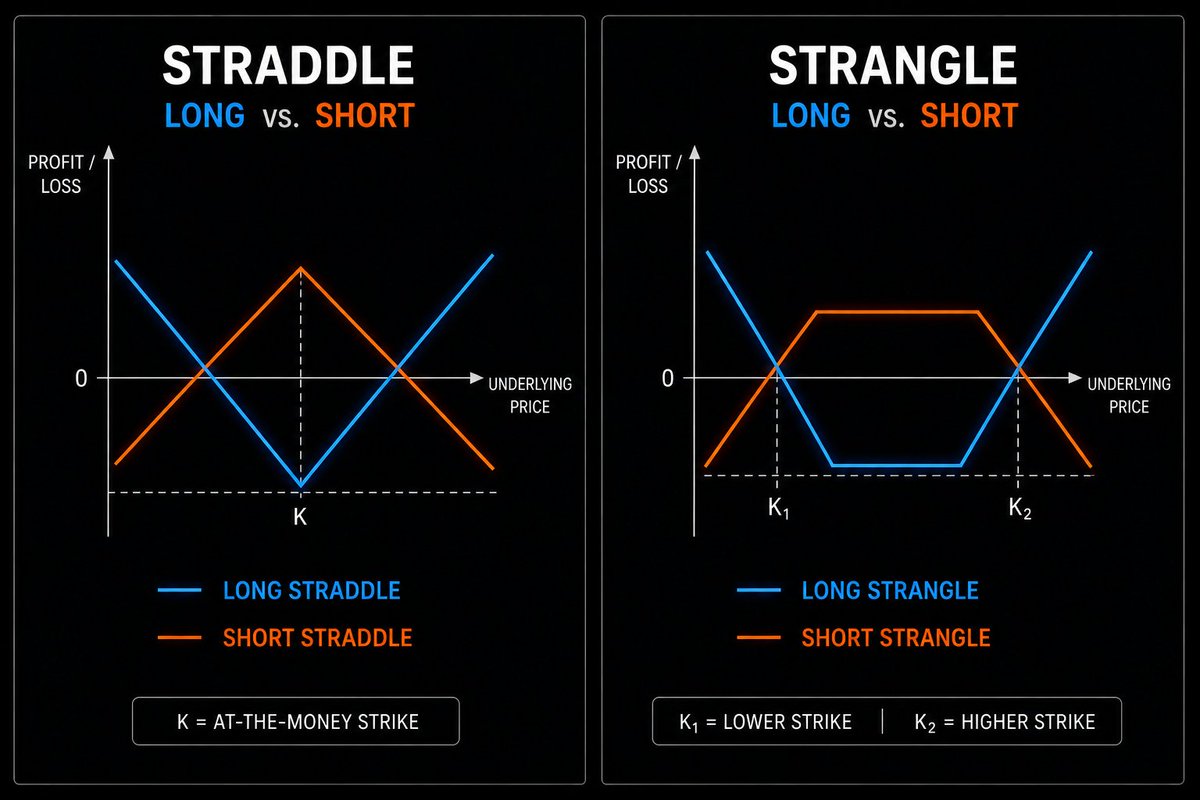

Know your straddles.

The X-factor in investing.

And never let a strangle become a stranglehold.

Last week, I had several fascinating conversations around structured products and options strategies.

One thing became very clear: many investors buy products linked to options without fully understanding what sits underneath.

Take straddles and strangles.

In simple terms:

🌟 A straddle combines a call and a put at the same strike price.

🌟 A strangle combines a call and a put at different strike prices. That difference changes the risk profile significantly.

A straddle places both options at the same strike. However, both options continuously lose time value (Theta). Even with some market movement, the strategy can still result in a loss if the move is not large enough to offset the premium paid.

A strangle works on the same principle, but the options sit at different strike prices. This makes the strategy cheaper upfront because both options are out of the money. The trade-off is significant: markets must move much further before the strategy becomes profitable. The safety net is wider, but also further from the ground.

📈 Why do investors confuse them? Because on the surface, they look similar. Both are built around volatility. Both combine a call and a put. Both appear to “win in both directions.” The difference only becomes visible once markets actually move.

The strangle is often marketed as the smarter and cheaper alternative. But "cheaper" also means strikes further apart and therefore significantly more movement required just to break even. If volatility remains moderate, the long strangle can simply expire worthless.

Once investors move into short volatility strategies in search of easy yield, the risk profile changes dramatically. With a short strangle, the investor collects the premium upfront, but takes on the obligation to deliver if markets move sharply.

Short strangles in particular can carry theoretically unlimited risk on the call side, and substantial downside risk on the put side. That is the real danger: not the strategy, but misunderstanding how much movement is required to make it work and which side of the trade you are actually on.

📈 From a Swiss tax perspective, we generally move within the area of tax-free private capital gains for private investors when it comes to pure options. However, this also means that losses are not deductible. Caution is required: precisely these strategies often involve higher trading frequency, short holding periods, leverage, derivatives and margin trading which can quickly raise questions around a qualification as a professional securities dealer.

Volatility rewards the prepared. Whether you hold a straddle or a strangle, the real X-factor is not the market move itself. It is whether you truly understood the structure before the market moved.

Stéphanie Fuchs Consulting – Keeping you in the driver's seat with your taxes 🏎️

#StructuredProducts #Options #Taxes #straddle #strangle

2

37

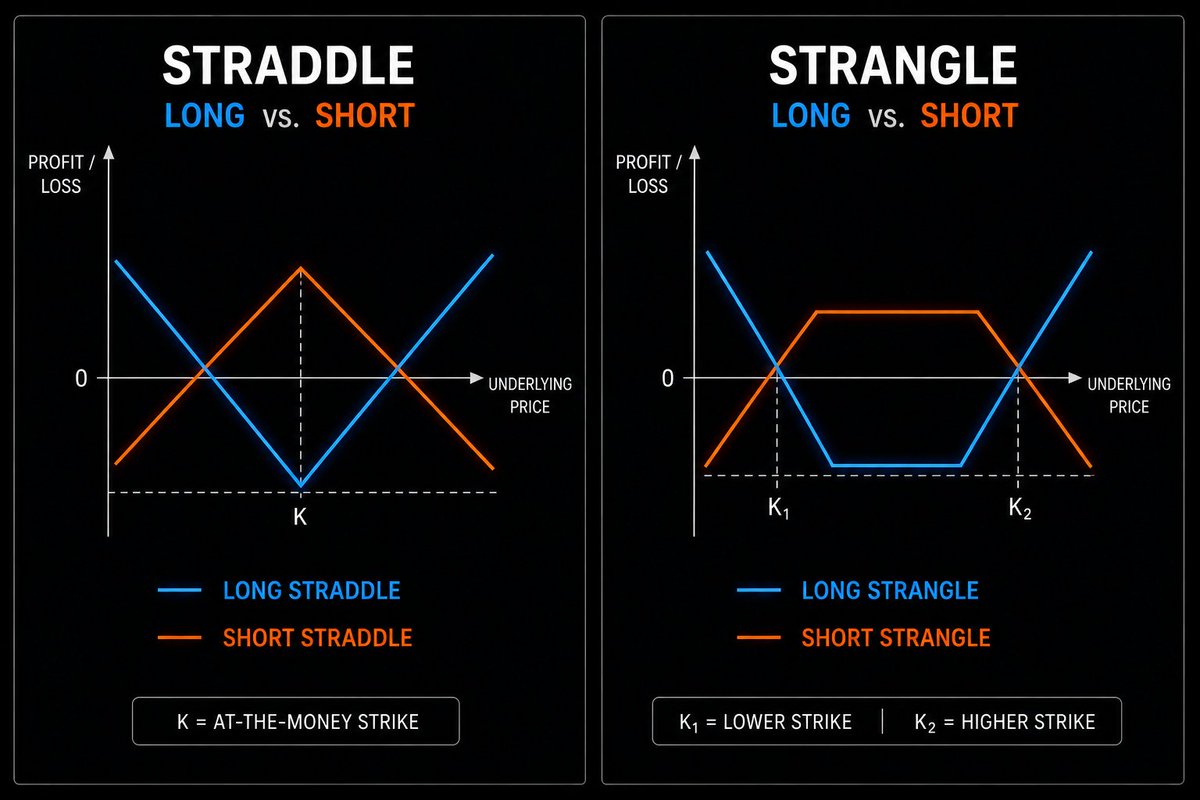

Know your straddles.

The X-factor in investing.

And never let a strangle become a stranglehold.

Last week, I had several fascinating conversations around structured products and options strategies.

One thing became very clear: many investors buy products linked to options without fully understanding what sits underneath.

Take straddles and strangles.

In simple terms:

🌟 A straddle combines a call and a put at the same strike price.

🌟 A strangle combines a call and a put at different strike prices. That difference changes the risk profile significantly.

A straddle places both options at the same strike. However, both options continuously lose time value (Theta). Even with some market movement, the strategy can still result in a loss if the move is not large enough to offset the premium paid.

A strangle works on the same principle, but the options sit at different strike prices. This makes the strategy cheaper upfront because both options are out of the money. The trade-off is significant: markets must move much further before the strategy becomes profitable. The safety net is wider, but also further from the ground.

📈 Why do investors confuse them? Because on the surface, they look similar. Both are built around volatility. Both combine a call and a put. Both appear to “win in both directions.” The difference only becomes visible once markets actually move.

The strangle is often marketed as the smarter and cheaper alternative. But "cheaper" also means strikes further apart and therefore significantly more movement required just to break even. If volatility remains moderate, the long strangle can simply expire worthless.

Once investors move into short volatility strategies in search of easy yield, the risk profile changes dramatically. With a short strangle, the investor collects the premium upfront, but takes on the obligation to deliver if markets move sharply.

Short strangles in particular can carry theoretically unlimited risk on the call side, and substantial downside risk on the put side. That is the real danger: not the strategy, but misunderstanding how much movement is required to make it work and which side of the trade you are actually on.

📈 From a Swiss tax perspective, we generally move within the area of tax-free private capital gains for private investors when it comes to pure options. However, this also means that losses are not deductible. Caution is required: precisely these strategies often involve higher trading frequency, short holding periods, leverage, derivatives and margin trading which can quickly raise questions around a qualification as a professional securities dealer.

Volatility rewards the prepared. Whether you hold a straddle or a strangle, the real X-factor is not the market move itself. It is whether you truly understood the structure before the market moved.

Stéphanie Fuchs Consulting – Keeping you in the driver's seat with your taxes 🏎️

#StructuredProducts #Options #Taxes #straddle #strangle

2

13