Jun 11

Stay aware:

Financial structuring becomes significantly more effective when tax and zakat considerations are addressed from the early stages.

Distribution structuring, cash flow organization, foreign investor implications, and exit planning

all directly influence returns, feasibility, and overall investment efficiency

Early assessment of these elements provides greater clarity, strengthens the structure, and supports long-term business stability.

Early tax and zakat review strengthens the structure and protects its sustainability.

#الزكاة #الضرائب #الهيكلة_الضريبية #TaxStructuring #Compliance

2

Jun 11

خلّك منتبه:

تتأثر كفاءة الهيكلة المالية بوضوح معالجة الجوانب الزكوية والضريبية منذ المراحل الأولى

هيكلة التوزيعات، وتنظيم التدفقات النقدية، وفهم أثر المستثمر الأجنبي، والتخارج،

كلها عناصر تنعكس مباشرة على العوائد، والجدوى، وكفاءة الهيكل الاستثماري

المعالجة المبكرة لهذه الجوانب تمنح وضوحًا أكبر، وتعزز كفاءة الهيكلة، وتدعم استقرار الأعمال على المدى الطويل.

مراجعة الأثر الضريبي والزكوي مبكرًا تعزز قوة الهيكلة وتحمي استدامتها

#الزكاة #الضرائب #الهيكلة_الضريبية #TaxStructuring #Compliance

4

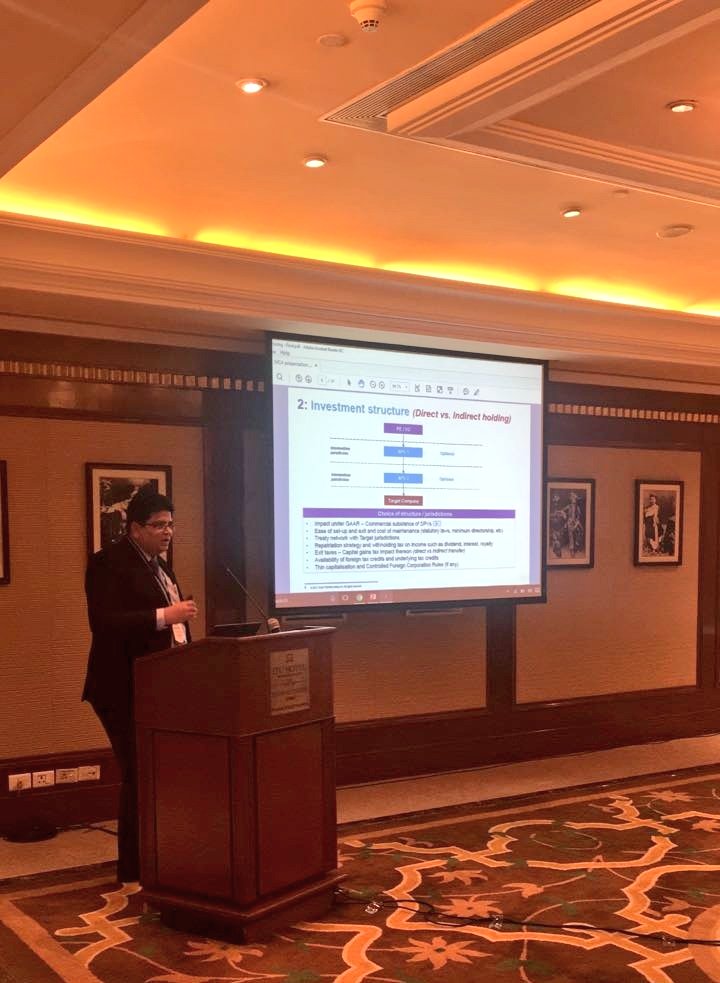

🔴#LiveNow

Session 2: Tax Strategy for PE/VC Fund Structures

Wrapping up Day 1 of VCCircle Tax Impact in Private Equity and M&A Transactions in 2026 Masterclass, Vishal Lohia, Partner, Dhruva Advisors India Pvt. Ltd., walks through the typical AIF structure, regulatory considerations including co-investment vehicles, accredited investor only funds and LVF regulations, key tax considerations for Cat I and II AIFs, feeder funds, and topics including QIB, dissolution, sponsor/manager obligations, Press Note 3, FOCC, trust to company conversions, continuation vehicles, and the April 2026 SEBI amendment on retention of funds beyond the liquidation period.

#VCCTaxImpactMasterclass #TaxStrategy #PrivateEquityIndia #MergersAndAcquisitions #CrossBorderTax #GIFTCity #TaxStructuring #FundStructuring

2

2

318

3 Aug 2025

𝐓𝐡𝐞 𝐩𝐮𝐫𝐞𝐬𝐭 𝐟𝐨𝐫𝐦 𝐨𝐟 𝐚𝐫𝐭: 𝐃𝐄𝐀𝐋𝐒

Sharpen your gut feeling

with the magic 10/20 tax thresholds and AI

Deals are an art form.

They are difficile.

And every detail counts.

You show your cards too early

You miss an indemnity clause

And what seemed closed

is far from clean

I have been part of many deals – with global insurers, private banks, commodities traders, pharmaceutical companies, and smaller ventures with limited resources.

The key lesson was always the same: it is taxes and gut feeling that make or break a deal.

It is tempting to quote

the trader from the screen

or the lawyer who wins by instinct or a lucky hand in poker

But deals do not follow scripts

They follow logic

timing

and form

That is why in today’s 𝐈𝐧𝐯𝐞𝐬𝐭𝐨𝐫 𝐒𝐮𝐧𝐝𝐚𝐲 𝐒𝐮𝐦𝐦𝐞𝐫 𝐄𝐝𝐢𝐭𝐢𝐨𝐧 𝐢𝐧 𝐓𝐡𝐞 𝐀𝐫𝐭𝐬 𝐚𝐧𝐝 𝐓𝐚𝐱𝐞𝐬

we are looking at the magic of the 10/20 thresholds

In Swiss tax law, these two numbers change the nature of your deal.

𝐀𝐭 𝟏𝟎 𝐩𝐞𝐫𝐜𝐞𝐧𝐭

you enter the world of qualified participations

▪️ For private investors, dividend income becomes partially tax-exempt under the "Teilbesteuerungsverfahren"

▪️ For corporate shareholders, the participation relief (Beteiligungsabzug) may apply

𝐀𝐭 2𝟎 𝐩𝐞𝐫𝐜𝐞𝐧𝐭

you enter the risk zone of indirect partial liquidation

If a private individual sells shares to a company

and the target distributes substance within five years

part of your tax-free gain may be reclassified as taxable income

𝐀𝐧𝐝 𝐢𝐟 𝐲𝐨𝐮 𝐚𝐫𝐞 𝐮𝐬𝐢𝐧𝐠 𝐜𝐨𝐧𝐯𝐞𝐫𝐭𝐢𝐛𝐥𝐞 𝐥𝐨𝐚𝐧𝐬

both thresholds matter.

Be sure to ask your borrower:

▪️If your loan is part of an overall financing amount above CHF 500k

▪️And issued to over 10 lenders at identical conditions

▪️Or to over 20 lenders at varying conditions

Should this be the case,

the loans may be requalified as bonds

bringing withholding tax consequences into play on interest payments

and potentially on the conversion discount.

𝐀𝐈 𝐜𝐚𝐧 𝐬𝐮𝐩𝐩𝐨𝐫𝐭 𝐲𝐨𝐮𝐫 𝐠𝐮𝐭 𝐟𝐞𝐞𝐥𝐢𝐧𝐠

if you give it the right input:

▫️ Are you the buyer or seller?

▫️ Are you acting privately or via a company?

▫️ Who is the counterparty?

▫️ What is the participation percentage (10/20% relevant)?

▫️ Are convertible loans involved – and is conversion planned?

▫️ Will reserves be distributed after the transaction?

Then ask:

Are there tax consequences under Swiss law

due to the participation structure

or a risk of indirect partial liquidation?

AI can support your gut feeling.

𝐁𝐮𝐭 𝐢𝐟 𝐲𝐨𝐮𝐫 𝐝𝐞𝐚𝐥 𝐢𝐬 𝐭𝐚𝐤𝐢𝐧𝐠 𝐬𝐡𝐚𝐩𝐞 – 𝐭𝐡𝐢𝐬 𝐢𝐬 𝐭𝐡𝐞 𝐦𝐨𝐦𝐞𝐧𝐭 𝐭𝐨 𝐭𝐚𝐥𝐤 𝐭𝐨 𝐮𝐬.

Because when it comes to structure and consequences, details decide.

Stéphanie Fuchs Consulting – Keeping you in the driver’s seat with your taxes 🏎️

#InvestorSunday #SwissTax #IndirectPartialLiquidation #ParticipationRelief #PartialTaxation #ConvertibleLoans #NonBankRules #PrivateInvestors #TaxStructuring #StéphanieFuchsConsulting #artofthedeal

1

2

45

Sharjah has announced the establishment of the Communication Technologies "Free Zone" (Comtech) in Kalba, initiated by Dr. Sheikh Sultan bin Muhammad Al Qasimi. This new zone aims to enhance Sharjah’s position in communication technologies, driving economic development and attracting investments and skilled professionals. Here's what businesses need to know:

Benefits:

- Streamlined financial regulations for accounting and auditing.

- Potential tax breaks, including VAT and corporate/excise tax exemptions.

- Modern infrastructure, skilled workforce, and business-friendly environment.

Considerations:

- Maintain proper bookkeeping and conduct audits for compliance.

- Understand tax benefits and stay updated on regulations.

- Develop robust AML programs and comply with regulations.

Success Factors:

- Leverage simplified setup processes and tax advantages.

- Stay compliant with local and international regulations.

- Maximize tax benefits with expert tax structuring.

Partner with Us:

Our firm can guide you through accounting, tax, compliance, and advisory services in the Comtech Free Zone. Let's help you succeed!

97143231738 | 971 54 327 8971 | info@amaudit.ae| amaudit.ae

#AMAudit #Sharjah #Comtech #CommunicationTechnologies #FreeZone #Kalba #Investment #Tech #Business #Accounting #Auditing #TaxBreaks #VATExemptions #VAT #CorporateTax #ExciseTax #Consultancy #Finance #AML #Compliance #FreeZoneBenefits #SimplifiedSetup #Infrastructure #Workforce #TaxAdvantages #Regulations #TaxStructuring

1

4

113

24 Feb 2023

Masterclass on #TaxStructuring in #Africa: Early-bird registration is now open!

The 2-day exclusive #masterclass on 22-23 May'23 will provide African tax practitioners to learn the most pressing issues in #internationaltax & #transferpricing.

Register now: link.ibfd.org/3IRB4Ya

2

2

444

2 Apr 2022

New beginnings! 🚀🚀🚀 origin-sw.com/

#familyoffice #originsw #taxstructuring #financialconsulting #ventures #investment #geneve #barcelona #newbeginnings

1

24 Jul 2021

Pleased to welcome Charles Briand to #TeamSPB's Tax Strategy & Benefits Practice Group based in France with @SPBParis - focussing on corporate and transaction #tax, cross-border M&A, #taxstructuring and more.

Read more here ➡️ bit.ly/3zgwNWr

1

1

20 Jul 2021

Pleased to welcome Charles Briand to #TeamSPB's Tax Strategy & Benefits Practice Group based in France with @SPBParis - focussing on corporate and transaction #tax, cross-border M&A, #taxstructuring and more.

Read more here ➡️ bit.ly/3zgwNWr

1

23 Nov 2020

We look forward to introducing the panel sessions on #Renewables & Future #Energy this Thu & Fri at @IMARC_Mining. Our team is well place to assist with finding #investors, implementing more #sustainable operations, undertaking a #modernslavery statement or #taxstructuring.

2

A warm welcome to Dr. Pia Dorfmueller, our new #Tax partner in Frankfurt. Bringing a wealth of expertise in #internationaltax & #taxstructuring, Pia’s arrival accelerates our strategy to offer full-spectrum tax advice in Germany and around the world. ow.ly/TE7f30qMg2T

1

1

28 Nov 2019

Concurrent sessions with @Worrells_Solve, Nick Sinclair from TOA Global and Andrew Henshaw & John Storey from Velocity Legal. #IPANC19 #SaveaBusiness #BuildingCulture #TaxStructuring

1

5

24 Oct 2019

Walking to the @Novogradac #OpportunityZone Conference in Chicago for insights, & chance to pitch investment w/ @ErieDDC in #Erie-this is certainly a great omen on the way! @Novogradac @LettieriDC @JohnMPersinger @FlagshipOppZone @twachter @ChipWachter @BrettWiler #taxstructuring

2

17

7 Aug 2019

Next Friday, August 9, Ana Claudia Utumi will be panelist at the Seminar of Taxation of Financial and Capital Markets, speaking about "Tax impacts in transactions involving directly and indirectly local investment funds. #capitalmarketstaxation #investmentfunds #taxstructuring

1

1

2

11 Apr 2019

@thelegal500: "Clientspraise @twobirds for its 'competent,driven and business-minded approach'; the team is well-versed in the taxstructuring elements of real estate transactions and developments, and alsohandles matters in the private equity and technology sectors... (1/2).

1

1

のれんは税務上と会計上で計上額に差異が生じ得ます。買収ストラクチャリングやPPA等に長けたアドバイザーとしっかり相談しましょう。 #MandA #WARC #financialadvisor #PPA #goodwill #purchasepriceallocation #taxstructuring

bit.ly/2PAAeA2

2

17 Nov 2018

Effective #TaxManagement, #TaxStructuring and #TaxAdvisory services in #London #UK

Contact us: bsassociate.co.uk/

Call 02071835956 for #ExpertAdvice.

#TaxInvestigations #EmploymentTax #InternationalTax #ExpatriateTax #CorporateTax #PersonalTax #IndirectTax

1

15 Nov 2017

We are at the hotel Grand in New Delhi for the MasterClass on #MnA - #DealStructuring & #TaxStructuring, in collaboration with @IndianVCA.

1

3

5

11 Nov 2017

Register now for the Masterclass on #MnA #DealStructuring and #TaxStructuring, in association with @IndianVCA, in New Delhi on 15 Nov. bit.ly/2jiM0EJ

2

1

8 Nov 2017

Ravi Mehta, our partner provides insights on #TaxStructuring drivers & #investment structures from a #taxation perspective during a #MnA #transaction at the @IndianVCA MasterClass today in Mumbai.

3

3