Jun 10

The Excel glow-up nobody warned me about: 📊

BEFORE — 2 to 4 days to build something heavy with VBA macros & nested formulas. 😶🌫️

NOW — a few hours with Claude doing the heavy lifting. ⚡

What used to eat my entire week now fits in an afternoon. 🤖

AI didn't take my job. It gave me my time back. 😌

#AI #Claude #Excel #Productivity #FutureOfWork #TechAtWork #RealTalk

1

43

Jun 4

Technology is expanding what’s possible for people with disabilities, from communicating with loved ones to navigating the world with greater independence. Learn how tech is enhancing accessibility in this week’s #TechAtWork. bit.ly/4e4IKVp

2

113

Broadcom dn 14% in after hours

Weaker-than-expected revenue in its fiscal second-quarter earnings report

No raise in company’s full-year target of $100 billion in AI chip sales.

Stk up 38% YTD

Crowdstrike dn 11.2% in after hours

Good qtr, but not beating the upper end of market estimates

Annual Recurring Rev $255.8 million,up 32% YOY but missed optimistic est of $275b

Stk up 65% YTD

This is what happens when cos cant exceed the very lofty bar set by investors

Yesterday IGV ETF dn 4.3%

Wipro ADR dn 3.8%

Infosys ADR dn 4.7%

In our markets: TCS dn 8.4%, Infosys dn 3.8% HCL dn 5.2% Wipro dn 2.7% (yesterday)

#TechAtWork #CNBCTV18 #Broadcom #Crowdstrike

1

1

9

1,374

May 25

The important part from what JPM highlights is

"More than price paid, see this acquisition as a sign that organic growth opportunities are drying up and management is being forced to evaluate unusual acquisitions to bulk up rather than thoughtfully add capabilities."

This was the feedback with the Wipro-Olam deal too !

@nimeshscnbc @jpmorgan #TechAtWork #StocksInNews

May 25

JPM on LTM

Downgrade to N, TP cut to Rs 4500 from Rs 5100

LTM announced that it has issued an offer to acquire Randstad’s technology and consulting services business in Europe and Australia.

Revenues of these entities (€469m) have declined sharply in the past two years while estimate business operates at much lower 4-5% Ebitda margins, given its onshore-heavy nature, which should be materially margin-dilutive.

LTM has also announced concomitant contracts to take over and build a GCC for Randstad in India and a reverse contract to Randstad to support LTM’s subcon needs

While, across three contracts, management doesn’t see any EPS dilution, estimate acquisition alone could drive 2% EPS dilution due to amortization costs and lower interest income.

Moreover, don’t see obvious horizontal service line or vertical synergies, given its focus on digital engineering and cybersecurity rather than core IT Services, which LTM focuses on.

Cross-sell opportunities as they exist should be limited by different buying centers for engineering and IT services

Acquisition price appears to be modest at €160m on a EV/Sales basis (0.34x), but not on implied profit multiples (8x EBITDA, 13-15x EBIT), given global/EU peer multiples.

More than price paid, see this acquisition as a sign that organic growth opportunities are drying up and management is being forced to evaluate unusual acquisitions to bulk up rather than thoughtfully add capabilities. Fear management distraction, due to closure of the acquisition by 3Q27 and ekeing out of synergies after that, could weigh on execution.

Moderate organic revenues/EPS by 1-2%, cut target PE multiple from 21x to 19x

@CNBCTV18News @Reematendulkar

3

1

4

3,182

May 22

Just in: LTM to acquire Randstad's Technology & Consulting Services business in Europe & Australia

Enterprise Value: Up to EUR 160 million

Revenue of acquired co (consolidated):

• CY 2023: EUR 609 Million

• CY 2024: EUR 541 Million

• CY 2025: EUR 469 Million

Alert - Rev of acquired has declined 23% in two years.

Valuation: LTM is paying ~0.34x revenue on current topline.

The deal would expand LTM's presence in Europe, primarily across Aerospace & Defence, Automotive, Utilities, and BFS sectors.

Randstad gets a long-term IT partner for its GCC

#LTM @ltm_ofcl @CNBCTV18News #TechAtWork

1

3

15

1,755

May 22

And to add: I read today Starbucks has retired an AI inventory tool across North America after it reportedly miscounted & mislabeled store items.

Eg some feedback from store managers

- AI App struggled to differentiate between similar items, such as confusing oat milk with dairy products or peppermint syrup bottles.

- To work correctly, products had to be lined up perfectly on shelves. In small, cramped backrooms, the AI often couldn't "understand" the depth of fridges.

Supervisors said they could perform manual counts in 15 minutes while the "faster" AI often took 45 minutes due to troubleshooting

That said, while this specific tool failed, Starbucks is still moving forward with other AI initiatives.

This perhaps underscores the view that AI fails when the environment hasn't been structured to meet it half way

reuters.com/business/starbuc…

CNBC-TV18 #TechAtWork #Starbucks

May 21

HCLTech Report warns 43% of enterprise AI initiatives may fail

This is based on a global survey of 467 senior executives responsible for AI investments across enterprises with more than $1 billion in annual revenue- "The AI Impact Imperatives, 2026"

The risk is not driven by lack of experimentation or access to tools, but by the difficulty of translating ambition into consistent, enterprise-wide outcomes.

expectations around returns are tightening.

Nearly half of enterprise leaders expect measurable value from AI investments within 18 months

Collision between speed and preparedness is becoming one of the most defining challenges facing enterprise leadership teams today

#HCLTech #CNBCTV18 #TechAtWork

5

8

61

28,852

May 21

From improving efficiency to investing in reliable electricity, technology companies are protecting consumers, modernizing the grid, and supporting local economies. Learn how tech is strengthening America’s energy infrastructure in this week’s #TechAtWork. bit.ly/3PDDShQ

3

211

May 21

HCLTech Report warns 43% of enterprise AI initiatives may fail

This is based on a global survey of 467 senior executives responsible for AI investments across enterprises with more than $1 billion in annual revenue- "The AI Impact Imperatives, 2026"

The risk is not driven by lack of experimentation or access to tools, but by the difficulty of translating ambition into consistent, enterprise-wide outcomes.

expectations around returns are tightening.

Nearly half of enterprise leaders expect measurable value from AI investments within 18 months

Collision between speed and preparedness is becoming one of the most defining challenges facing enterprise leadership teams today

#HCLTech #CNBCTV18 #TechAtWork

11

24

135

64,445

May 7

As we celebrate #NationalSmallBusinessWeek, tech is investing in AI tools, e-commerce platforms, and new resources that empower entrepreneurs and support local economies. Explore how tech is strengthening small businesses in this week’s #TechAtWork. bit.ly/3RsjpNl

3

157

Apr 24

2 things I found interesting in the Infosys concall

CEO Salil Parekh

"We do see sometimes a particular sort of competitor doing “pricing, which seems sort of unusual”. But this is something that's happened over the course of the years for different reasons. Just now, it may be linked with the clients' mind to AI productivity.

So every now and then, we see a competitor doing something which looks outside the range of what we think the models can do today."

The takeaway is in some deals the math of the deal doesn’t add up. Either they're pricing at a loss, or making promises AI simply cannot keep yet

CFO Jayesh

“AI projects come at a better pricing, and therefore, it reflects in a better margin. Of course, it also has a higher cost compared to the regular project because the talent is a premium talent at this point in time.”

Question: Is AI really a big margin expander?

#Infosys #CNBCTV18 #Infosysconcall #4QWithCNBCTV18 #TechAtWork

8

5

75

16,459

Apr 23

Cyient announces buyback

Tender buyback

Price of Rs 1,125/sh (CMP 935)

Buyback size Rs 720 crore.

Buyback of up to 6.4 million equity shares of ₹5 each or 5.76% of equity

#Cyient #4QWithCNBCTV18 #CNBCTV18Market #TechAtWork

1

17

2,161

Apr 23

📉 FY26 Annual Revenue Growth - full scorecard TCS: -2.4% - First negative growth year since inception Wipro: -1.6% - Revenue declining for 3rd consecutive year

HCL Tech: 3.9% - Missed own guidance of 4–4.5% Infosys: 3.1% - Growth at lower end of its guidance of 3-3.5%

FY27 Guidance

Infosys

Revenue: 1.5% – 3.5%

EBIT margin: 20% – 22%

HCL Tech: Revenue: 1% – 4%

EBIT margin: 17.5% – 18.5%

@CNBCTV18Live #4QWIthCNBCTV18 #CNBCTV18 #TechAtWork #Infosys #TCS #Wipro #HCLTech

3

2

14

3,968

Apr 16

Wipro Q4 expectations -@CNBCTV18News poll

Q4FY26eQOQ

$ Rev up 1.1% at $2666m vs $2635.4m

CC rev growth at 0.4-0.5%

Growth is entirely attributed to the Harman DTS acquisition, which is expected to contribute approximately 1.5% to 2%.

EBIT % at 17.1% vs 17.6%

*** CNBCTV18 poll

Key focus on

#1: Q1FY27 guidance

CLSA/J.P. Morgan/Morgan Stanley/UBS Expect a -2% to 0% QoQ CC

Nomura/Citi expect-1% to 1% QoQ CC

#2: Buyback announcement

#3: Organic growth, since growth has been led by M&A.

Co recently announced $1b , 8 yr strategic transformation deal with Olam Group and as a part of it co will acquire 100% stake in Mindsprint Pte. Ltd for $375 million cash

#Wipro #CNBCTV18 #CNBCTV18Market #4QWithCNBCTV18 #TechAtWork #Stocksinfocus

1

2

13

2,980

Apr 16

Snap Inc (Snapchat's parent) is laying off ~1,000 employees

This is 16% of its full-time workforce — while closing 300 open roles.

CEO Evan Spiegel cites 'rapid advancements in AI' to boost efficiency and cut costs by over $500M.

WSJ headline "Has the Era of the Mega-Layoff Arrived?"

Basically saying cos are opting for single, sweeping cuts rather than smaller "waves" of layoffs. Historically, mass layoffs were seen as a sign of mismanagement or crisis. Today, they are often viewed as a "bold" strategic move

#SnapLayoffs #TechLayoffs #TechAtWork

1

1

6

1,535

Anthropic released a new AI model called Claude Mythos

Kotak says Mythos model exhibits a step-jump in benchmark performance vs incremental/moderate improvements in the recent past.

MOSL says

See this as a meaningful development.

Mythos shows that model capabilities are moving ahead quickly with AI now extending beyond coding, ERP into areas like cybersecurity.

Anthropic Feb Claude update sent IT stocks tanking

Nifty IT index was dn ~25% over Feb & March 2026

Will Mythos trigger another round of pain for IT stocks? Or have markets already absorbed the core narrative of AI-driven disruption and therefore repeated positive AI headlines may not have the same shock awe factor?

#Anthropic #TechAtWork @CNBCTV18News #CNBCTV18Markets

3

9

62

15,780

Whats your view on TCS?

1 yr returns

TCS dn 22%

Infosys dn 4%

HCLT up 6%

Nifty IT dn 17%

Stk trades at 15-16X FY28e PE

This compares with 20-22X pre covid and ~28-32X post covid highs

Valuations and underperformance is a tailwind but will growth & commentary deliver?

#TCS #TechAtWork #4QWithCNBCTV18

Apr 9

#4QWithCNBCTV18 | TCS Q4FY26 Earnings Estimates

- Revenue expected to grow 1.5% QoQ to $7,619.5M

- Topline may get 30-40 bps boost from Coastal Cloud & ListEngage acquisitions

- EBIT margin estimated at 25.4%; Profit projected up 29% to Rs 13,727 cr

@reematendulkar

@CNBCTV18News @TCS #CNBCTV18Market #Earnings #TCS

9

5

37

16,802

With the sector having sharply underperformed, and sharp PE compression, can IT cos guide their way out of pessimism?

While IT revenue growth will be modest for Q4FY26 and FY27, the real story for IT this qtr will be the margin and EPS growth given the INR depreciation.

Street expects a double digit EPS growth for FY27 after a low single digit growth in FY26.

#QSQT #4QWithCNBCTV18 #Earnings #TechAtWork

Apr 7

#QSQT | IT Sector In Focus As #Q3FY26 #Earnings Season Begins

Key Overhangs This Quarter 👇

* #AI fears

* West Asia conflict

* Rupee depreciation: Down 2.8% on avg & 5.5% on closing basis

@Reematendulkar #CNBCTV18Market #QuarterSeQuarterTak

1

12

2,393

IT sector sees EPS upgrades

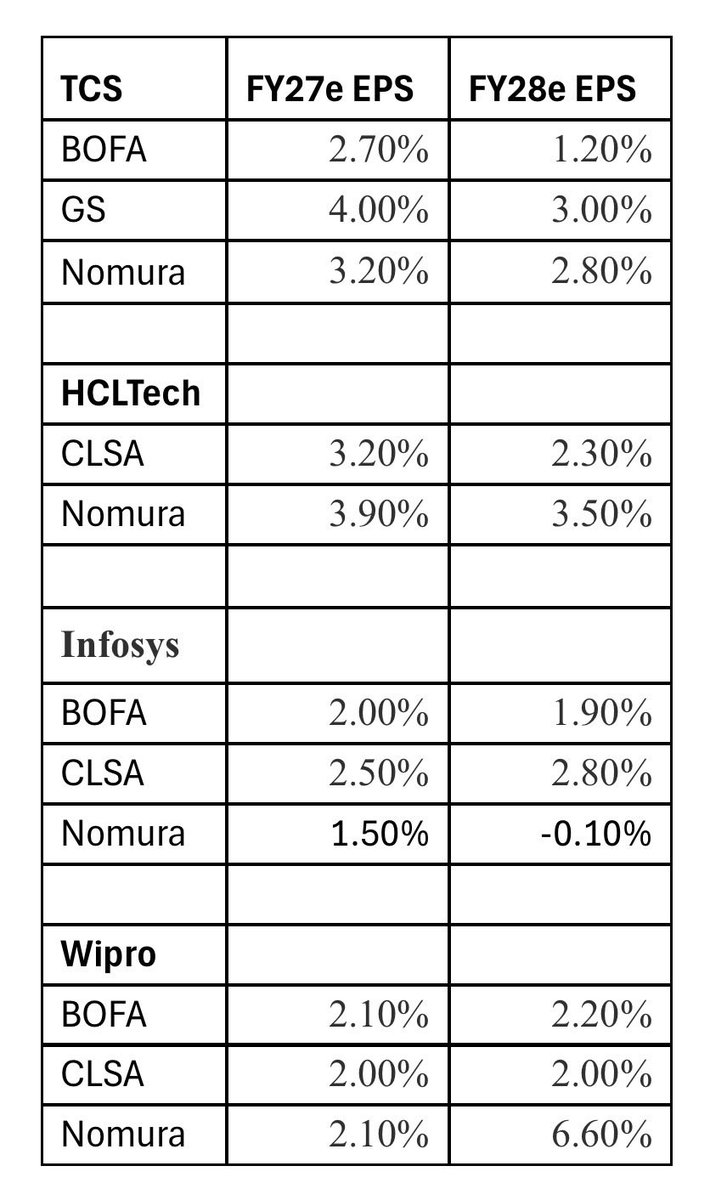

While most sectors have seen EPS downgrades due to the conflict, the INR depreciation has resulted in EPS upgrades of 2-4% for the IT sector for FY27 and to a lesser extent FY28 @CNBCTV18Live #TechAtWork

1

11

77

19,928

Wipro: Using M&A to buy growth?

Wipro has secured a multi-year strategic transformation deal with Olam Group

Contract size: Total potential: $1b

Committed spend: $800m

Duration: 8 years

As a part of this deal, Wipro will acquire 100% stake in Mindsprint Pte. Ltd for $375 million cash

Mindsprint is Olam’s IT arm with 2025 Rev of $135.6m

Positives

Olam is strong in food and agri supply chains

Guaranteed long term & sticky Revenues by locking in customer (Olam)

Negatives

Mindsprint Rev of $135m for 8 yrs = $1.08b which is the Rev, so no Rev beyond this acquisition

Wipro to take on 3200 Mindsprint employees & often captive buys have lower margins

#Wipro #CNBCTV18 @CNBCTV18News #TechAtWork

1

2

10

2,738

Mar 24

First of the Indian IT Previews out for Q4FY26 out

JPM says

For the first time in eight years (since cloud/digital deflation over 2015-18), the focus on revenue guidance will be crucial given the wide-spread pessimism. This will be key step to allay investor fears of AI compression and signal confidence and growth acceleration

FY27 guidance expectations

Infosys: 2–5% growth

HCLT: 3–6% growth

Wipro: -2% to 0% QoQ

4Q should be a healthy quarter but below earlier expectations for some.

CC QOQ

TCS 0.6%

Infosys -0.7%

HCL -1.6%

Wipro -1.3%

LTM 1.5%

Given that visibility on the inflection point to reflation remains distant, we moderate our medium-term growth recovery assumptions

Large caps seen at 3% vs 4% earlier

Midcaps seen at 5% vs 6% earlier

This drives ~25% cuts to target PE multiples.

Sharp INR depreciation vs USD helps cushion earnings downgrades.

@jpmorgan @CNBCTV18News #CNBCTV18market #CNBCTV18live #Infosys #TCS #Wipro #HCLTech #TechAtWork

6

18

104

36,031