Make an impact on pain medication use after closing the venotomy.

VASCADE MVP® Venous Vascular Closure System helped reduce pain medication use by 51% post-AF ablation* in the AMBULATE trial (1). Patients in the closure device group indicated 25% less pain* during supine bedrest, which potentially led to the reduction of pain medication use (1).

Learn more about vascular closure for EP procedures:

bit.ly/4v1osmQ

Or contact us to request more information:

bit.ly/3SggIPr

#VascularClosure #VASCADEMVP #VASCADE #Electrophysiology

*Compared to manual compression

1

22

The VASCADE vascular closure system is elegantly simple. Using bioabsorbable collagen, it offers rapid hemostasis. With dual radiopaque marker bands for precise fluoroscopy guidance, you can confidently deploy this device, knowing exactly where it's headed.

Watch the full webinar here: bit.ly/4uYJxOK

#CloseWithConfidence

30

Jun 10

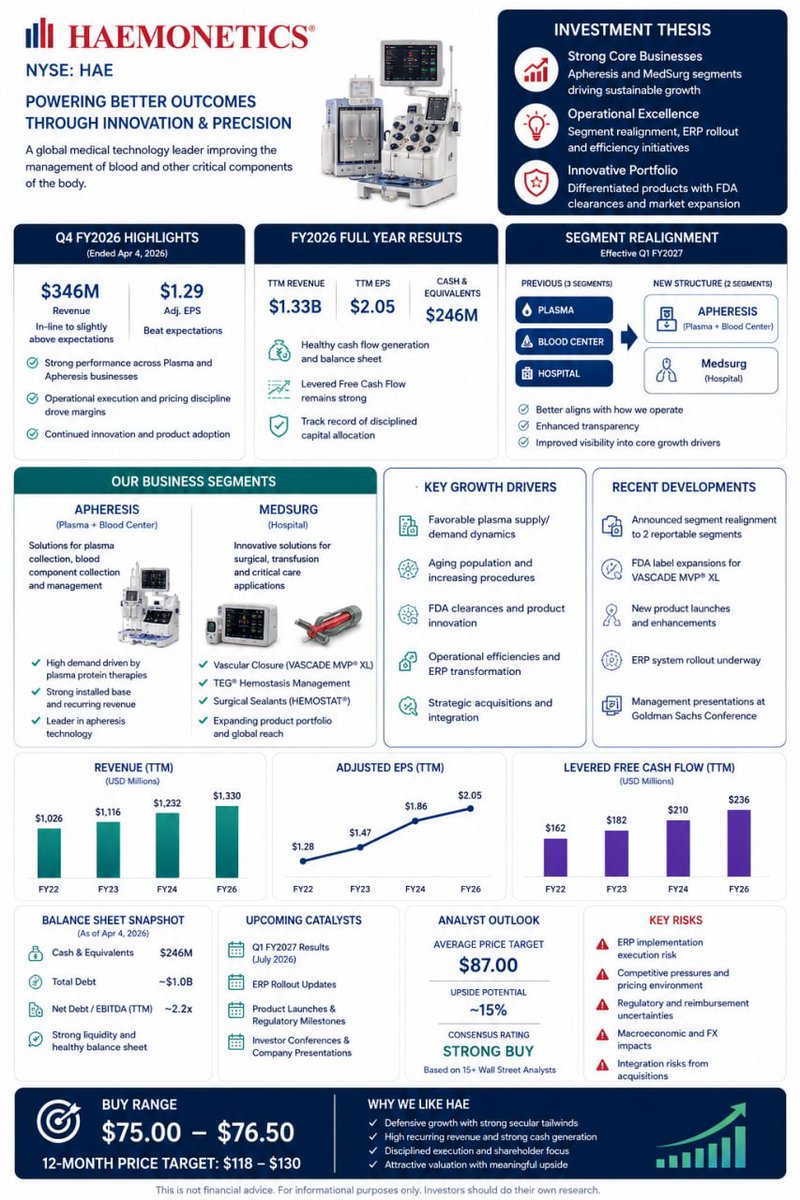

$HAE: Q4 FY2026: Revenue of approximately $346 million (in line with or slightly above expectations), adjusted EPS of $1.29 (beat expectations). Solid performance for the full year, with growth driven by the Plasma/Apheresis business. TTM revenue of approximately $1.33 billion, EPS of $2.05. Cash reserves of approximately $246 million; has debt but healthy cash flow (strong leveraged FCF).

Announced an update to its financial reporting segments, shifting from three (Plasma, Blood Center, Hospital) to two (Apheresis, combining Plasma and Blood Center; MedSurg, formerly Hospital). This enhances transparency and management alignment, and the market has interpreted it positively as a better way to showcase core businesses.

Other: FDA label expansions (vascular closure products such as VASCADE MVP XL), new product launches, ERP system rollout (execution risks but long-term benefits), and appearances at conferences including those hosted by Goldman Sachs. A history of acquisitions and integrations supports platform expansion.

Core thesis: A story of steady growth in medical devices, with a focus on plasma collection, blood management, and hospital interventions (vascular closure, hemostasis, etc.). Strong demand for Apheresis (plasma product shortages improved collection efficiency), while innovative MedSurg products (such as TEG and VASCADE) provide differentiation. The divisional restructuring enhances visibility, and organ/blood-related demand is expected to remain stable in the long term.

Key Focus Areas

Execution of new segment reporting (starting Q1 FY2027), ERP rollout progress, and product adoption rates.

Improvements in gross margin and operational efficiency, macro healthcare spending, and supply chain.

Competition, regulation (FDA), and currency impacts.

Buy Price: $75–$76.5

#HAE #MedicalDevices #Apheresis #BloodManagement #MedSurg #HealthcareStocks #GrowthStocks

88

Jun 10

$HAE:

What are the latest earnings results?

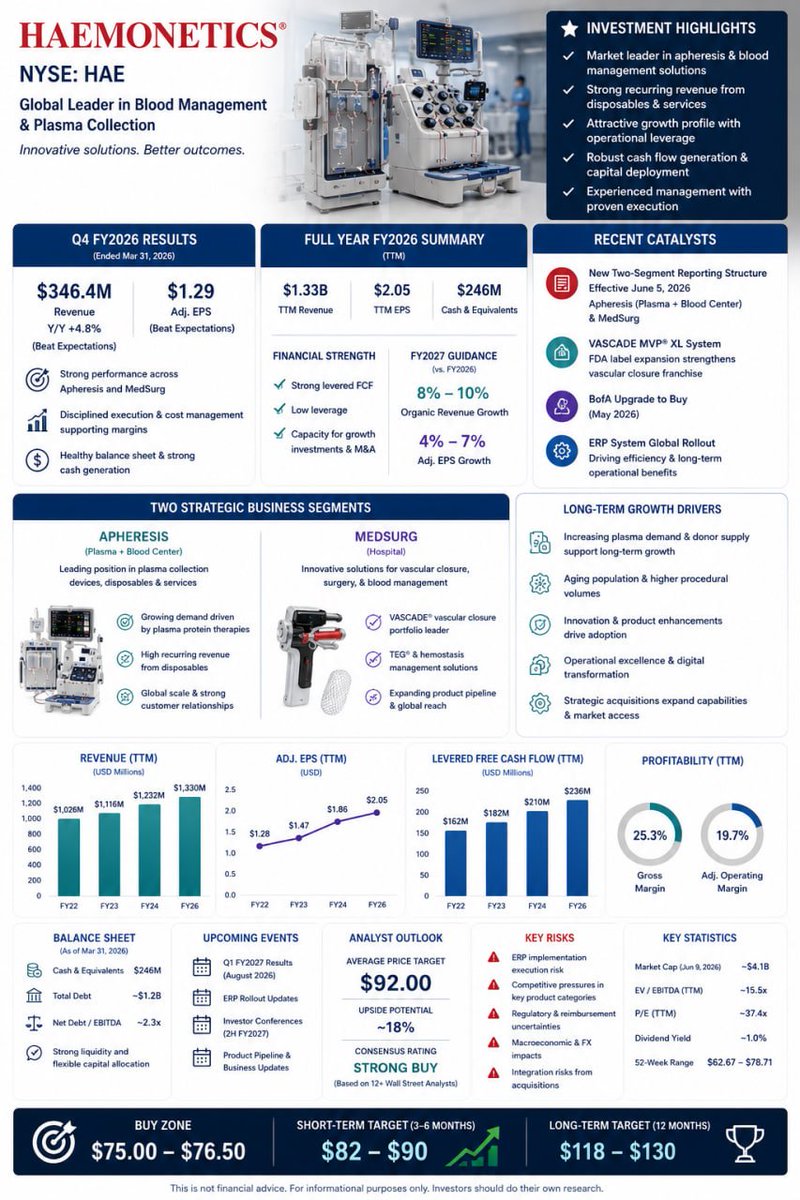

Q4 2026 (ended March 2026) revenue was $346.4 million (up 4.8% year-over-year, beating expectations), with adjusted EPS of $1.29 (slightly above expectations). The company is guiding for organic growth of 8–10% and adjusted EPS growth of 4–7% for FY2027.

Recent catalysts/events?

Announced a new two-segment financial reporting structure on June 5 (Apheresis combined with Plasma Blood Center); FDA label expansion for the VASCADE MVP XL system; BofA upgraded to Buy in May; global rollout of the ERP system is underway.

A global medical technology company focused on blood management and plasma collection. Key products include plasma collection devices and consumables (Apheresis), hospital surgical and vascular closure products (MedSurg), and blood center solutions. The company recently restructured its reporting segments into two main categories (Apheresis MedSurg) to better reflect business management.

Key Points

Core Businesses: Apheresis (plasma collection, primary growth driver) MedSurg (vascular closure, surgical products).

Financials: Stable cash flow, high-margin consumables model; Q1 operating margin fluctuated but overall execution was solid; FY2027 guidance is optimistic.

Product Pipeline: Label expansions for new products such as VASCADE; ERP digital transformation to enhance efficiency.

Market: Strong demand for plasma (driven by immunoglobulins, etc.); significant room for growth in vascular closure penetration in the hospital sector.

Investment Rationale and Growth Drivers:

Strong organic growth in the plasma business renewed growth from FDA label expansions for vascular closure products long-term efficiency gains from ERP transformation.

Competitive Advantages: High recurring revenue from medical devices, global leadership in plasma collection, and a clinically validated product portfolio.

Valuation Attractiveness: Current EV/EBITDA and P/E ratios are reasonable relative to mid-single-digit growth and cash generation capabilities, particularly within the stable medical device sector.

Short-Term (3–6 months): $82–90

#HAE #BloodManagement #Apheresis #MedSurg #PlasmaCollection #VASCADE #MedicalDevices

262

Mar 30

$HAE

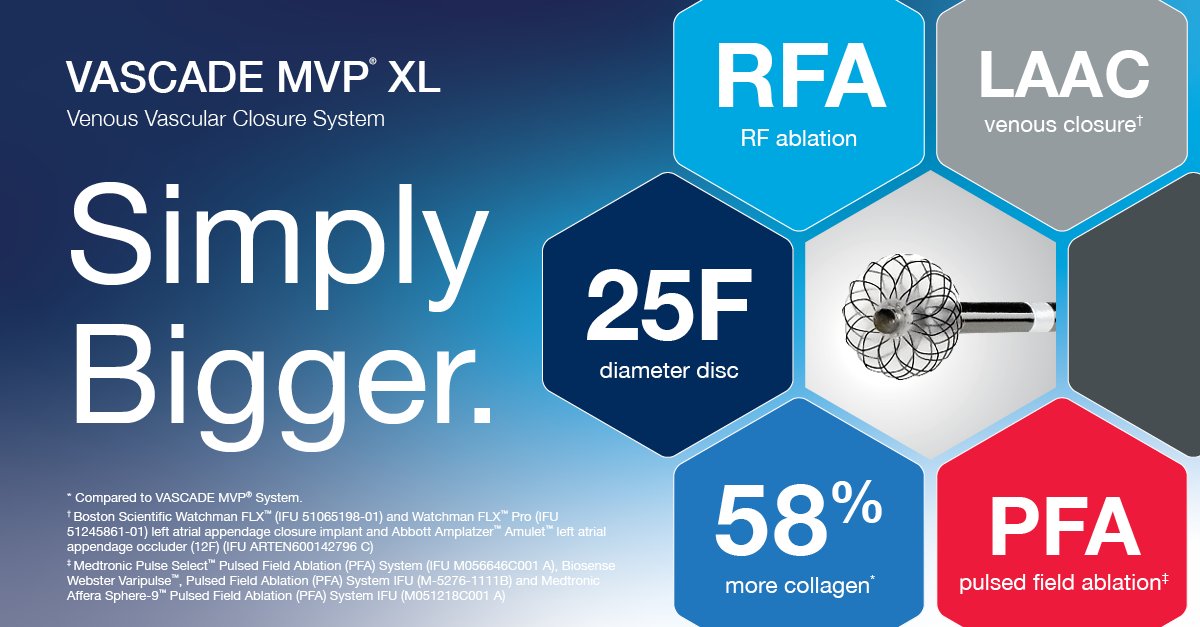

Haemonetics Receives FDA Approval for Expanded Labeling of the VASCADE MVP® XL Venous Vascular Closure System

- VASCADE MVP XL now approved for larger sheaths used in market-leading PFA and LAAC technologies

stocktitan.net/news/HAE/haem…

1

1

223

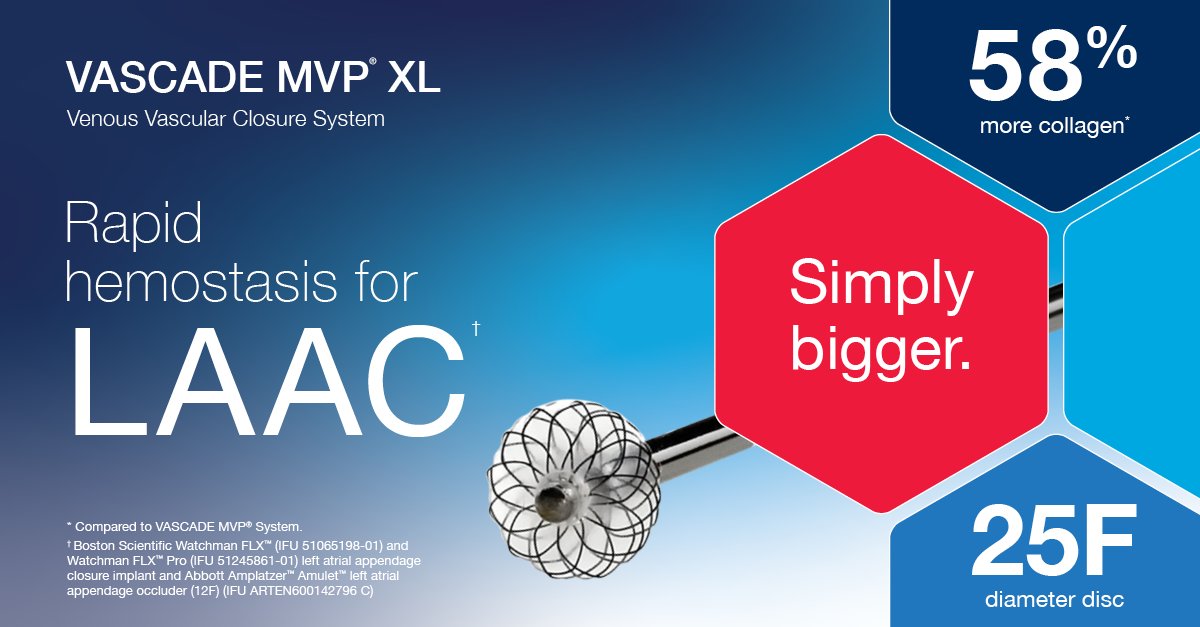

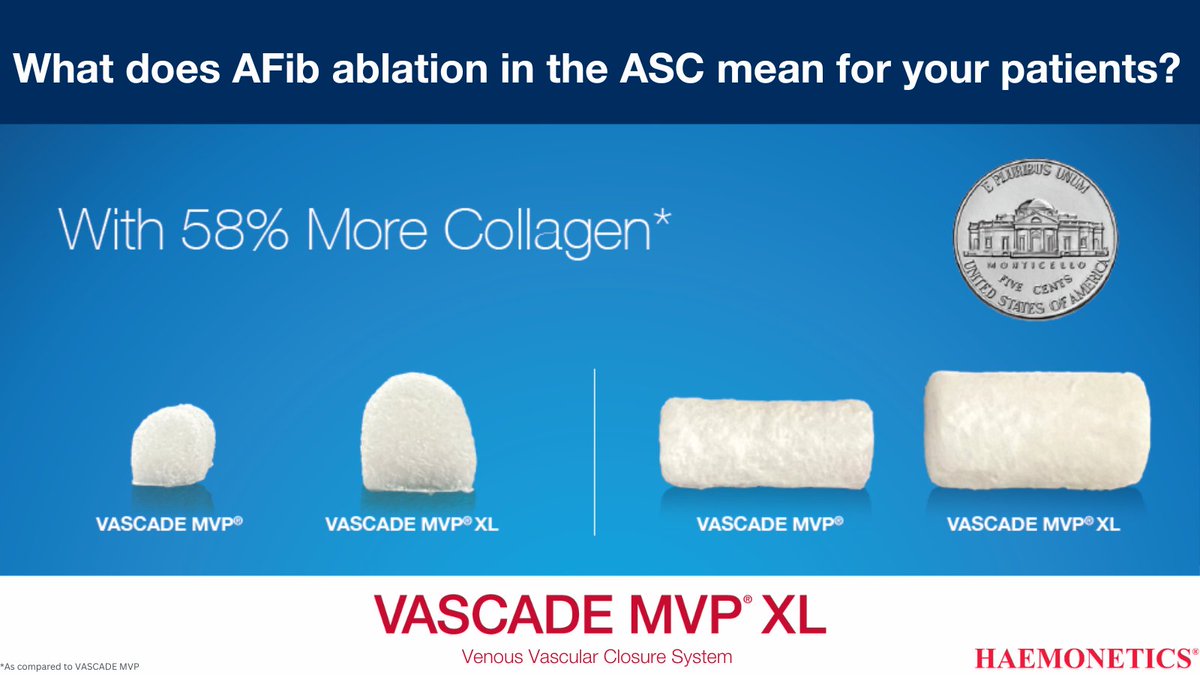

Where does your ASC fit in the next chapter of EP care?

Utilize VASCADE MVP® XL, the simply bigger version of VASCADE MVP®. Ready for use following AFib Ablations.

The VASCADE MVP® XL Venous Vascular Closure System offers the advantages of VASCADE MVP® Venous Vascular Closure System with 58% more collagen!

Discover how VASCADE MVP® XL can make a difference in your ASC today!

bit.ly/4s2xI8k

1

3

63

Reduce time to ambulation, improve patient satisfaction, & reduce opioid use with VASCADE MVP. With no permanent sutures, balloons, or intravascular footplates, it just might be your new closure device of choice.

Learn about our closure products: bit.ly/4rDtEvN

1

2

41

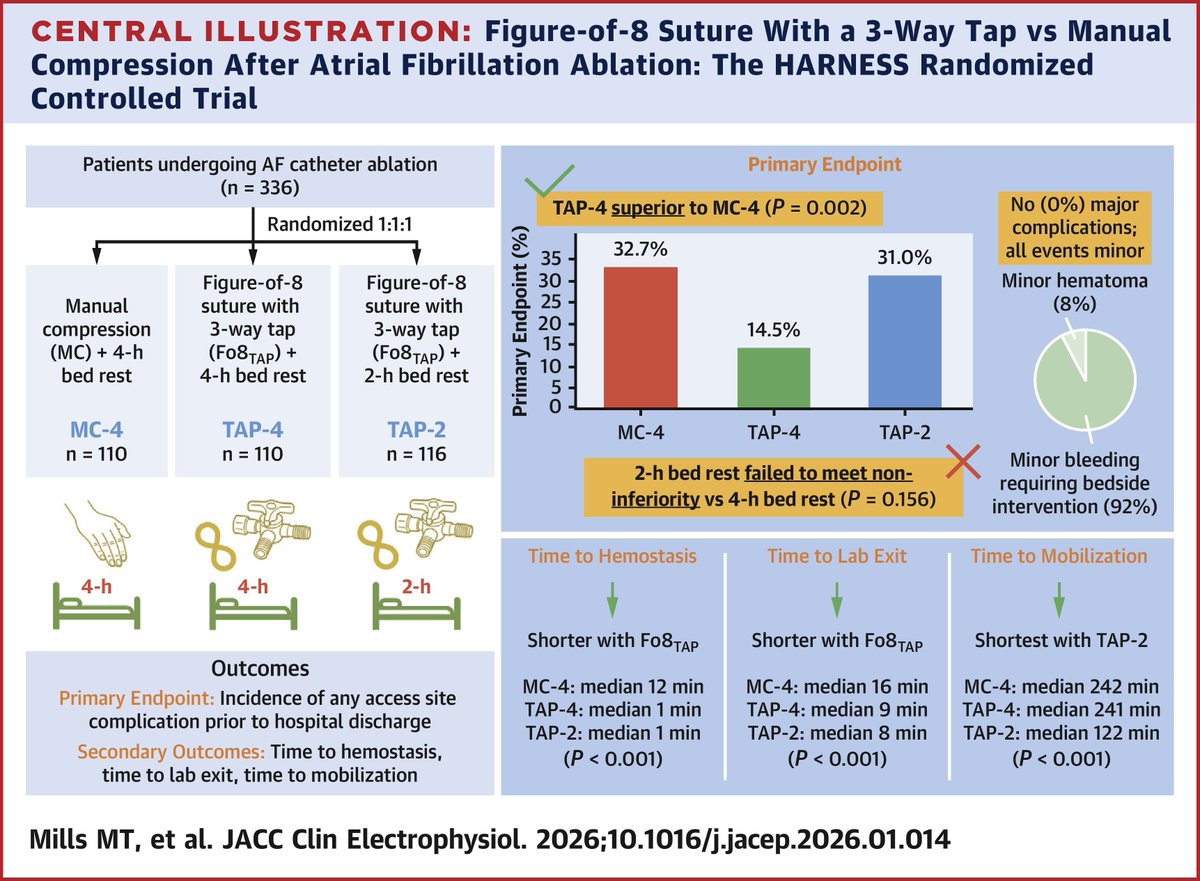

🧵We been using Figure-of-8 sutures for most AF ablation cases. Excellent results for simple/low cost intervention.

The HARNESS data makes it harder to justify routine use of vascular closure devices (e.g., Vascade) when added cost is ~$600–900 per case.

FO8: Simple. Reproducible. Low cost.

#EPeeps #AFablation #ValueBasedCare

2

6

19

5,464

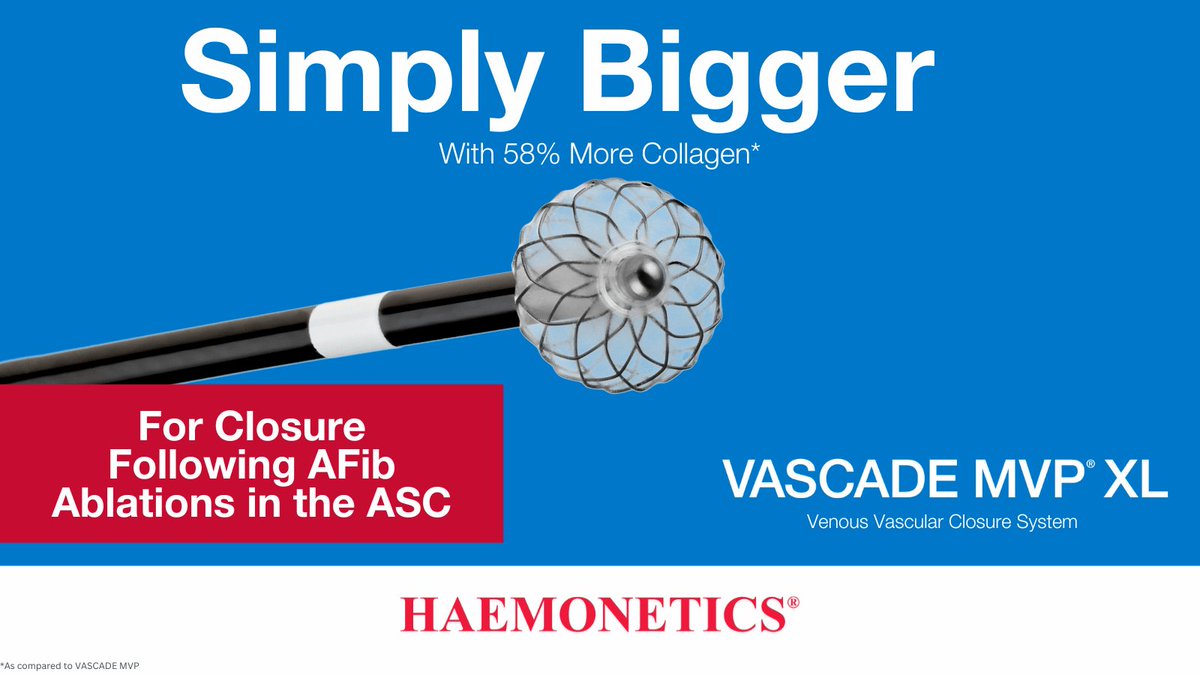

More collagen. Larger disc. Case Closed.

The VASCADE MVP® XL System provides confidence in vascular closure following Pulsed Field Ablation (PFA) & Left Atrial Appendage Closure procedures, providing proven performance without compromising simplicity.

Learn More: bit.ly/3OmuNck

3

92

Ready to experience a new innovation in venous closure for LAAC? The VASCADE MVP® XL System is simply bigger with 58% more collagen compared to VASCADE MVP® with the same simplicity & ease of use.

Learn more: bit.ly/4kBOj0q

1

2

141

Are you ready for AFib Ablation in the ASC?

VASCADE MVP® XL is an innovative closure system and simply bigger with 58% more collagen compared to VASCADE MVP® and may be used for AFib Ablations.

Reach out to your local Haemonetics rep to learn more! bit.ly/4btVchT

1

3

116

Are you in Boston for AF Symposium? Stop by booth #101 to say hello, grab a coffee and hear about the VASCADE MVP XL venous vascular closure system and our portfolio of procedure enabling technologies.

#AFS2026

2

3

149

Are you evaluating how AFib ablations fit into your ASC strategy?

The VASCADE MVP® XL System enables confident closure following AFib procedures with its larger disc and 58% more collagen.

Choose the device Designed for EPs. Proven by EPs.

bit.ly/45nM0aW

1

2

125

Coming soon to an ASC near you, AFib Ablations!

Utilize the VASCADE MVP® XL System for closure following an AFib ablation. It’s simply bigger with 58% more collagen compared to VASCADE MVP® with the same simplicity & ease of use.

Learn more: bit.ly/44PdaXX

1

2

89

How do you plan to close your AFib patients in the ASC?

Utilize the VASCADE MVP® XL System for closure following an AFib ablation. It’s simply bigger with 58% more collagen compared to VASCADE MVP® with the same simplicity & ease of use.

Learn more: bit.ly/3MN6685

1

3

129

Are you evaluating how AFib ablations fit into your ASC strategy?

The VASCADE MVP® XL System enables confident closure following AFib procedures with its larger disc and 58% more collagen.

Choose the device Designed for EPs. Proven by EPs.

bit.ly/4ppSPk6

2

132

Procedural efficiency meets peace of mind. In this step-by-step video, Dr. Christian Heeger shows just how straightforward venous closure can be with VASCADE MVP® system after cryo balloon ablation. Observe in this case how there were:

✔️No sutures.

✔️No major complications.

✔️No overnight stays.

One device. One goal: Safe. Simple. Proven.

Watch now! bit.ly/3XwSvDM

2

123

Designed for EP Procedures. Proven by EPs.

VASCADE MVP® Venous Vascular Closure System has been intensely studied in five EP-clinical trials, including four trials studying paroxysmal and persistent AF ablation patients, and same day discharge (1-5).

The AMBULATE randomized clinical trial, showed a 63% improvement in patient satisfaction, which is driven by early ambulation, and a 51% reduction in pain medication use (**,1).

Read the AMBULATE RCT publication: bit.ly/3LytaXs

** Compared to manual compression

1

3

151

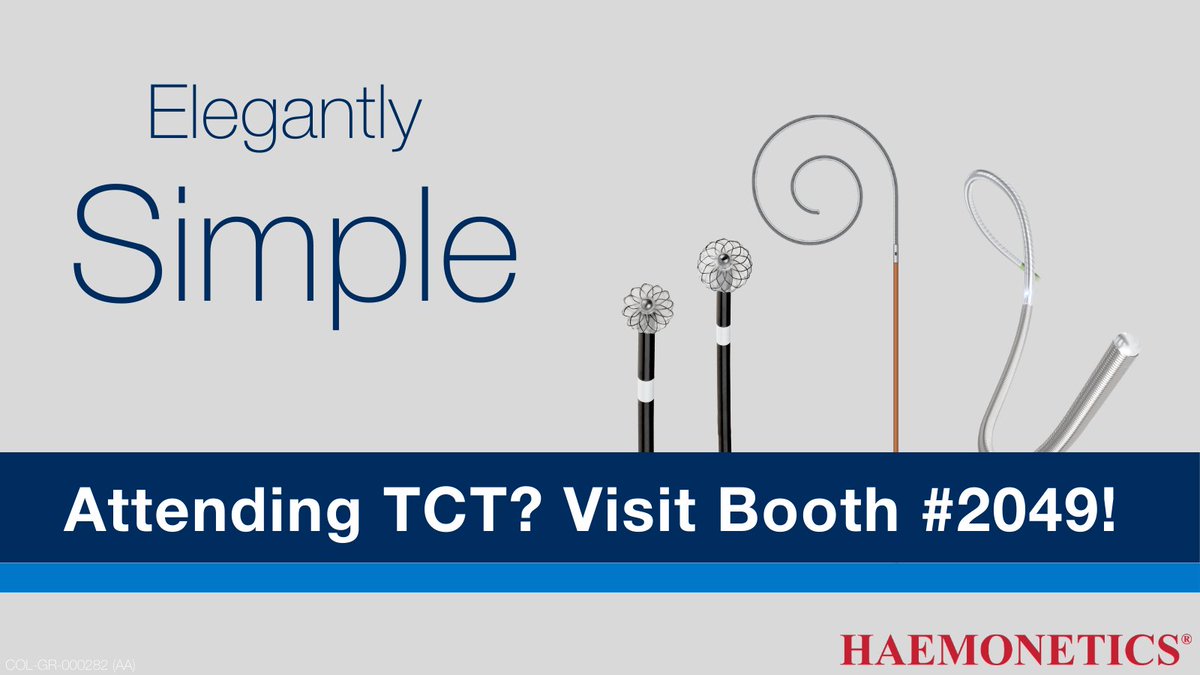

We look forward to seeing everyone at #TCT2025 in San Francisco tomorrow! Swing by booth #2049 for a cup of coffee and a demonstration of SavvyWire Guidewire with ARi Insight, OptoWire Guidewire, and VASCADE vascular closure system.

#OneWirePCI #SavvyForTAVI #TCT2025

1

4

61