Check out New ADVANCE Dress Size S/M Lace Wine Burgundy Adj Strap Embr Tie-back Knee Lngth ebay.io/m/rbxi3G #eBay via @eBay

It will not be a nothing. Those lines will draw down as the equity price goes lower. Employee, ex management is a very small amount of the stock- funds holding will bust the bids, but into index buying for free float adj. Marginal buyer after the multiple triggers will be gone.

26

Jeff Lichtstein retweeted

Jun 15

🏡 Maui is looking for a second chance.

After his family welcomed a baby, they no longer had time for him. Now Maui is adjusting to kennel life after growing up in a home since puppyhood—it’s not where he wants to be

Maui gets along with everyone & is ready for a family again

6

185

158

1,267

CW Hawes retweeted

May 27

"breathtaking, adj. Those mornings when we kiss and surrender for an hour before we say a single word.” – David Levithan

Scenic View of Snow-Capped Mount Hood Leaving the Gorge Art Print #travelingWA #buyart #Beauty #Washington #MTHood #sceniclandscape #snowcapped #grape #vinefields #washingtonside #bluesky #artisagiftoflov #itis #mystyle #gentleday #photographicart #DMSDesigns #ClearSkyLIne #sprintimecrossroads #pointA2B #StoryStyle #storytelling #uandme #iMissU #Love #hugs #itsfixable #haveabrilliantday #loveheals #playtime #worktime #lifetime #mylovinselah #moringvibes #coffeetime #LoveFaithSoul #DMSFineArt #towels #MarySharptonArt #myart #decor #Prints #Apparel #DianaMarySharpton #phonecovers #fineart4sale #puzzels #showercurtains #bathroomdecor

Artist Deck: dianamary-sharpton.pixels.co…

Shower Curtain: fineartamerica.com/featured/…

2

184

189

1,306

adj. Que todavía está mamando. U. t. c. s.

Ella es una perfecta cretina.

2

28

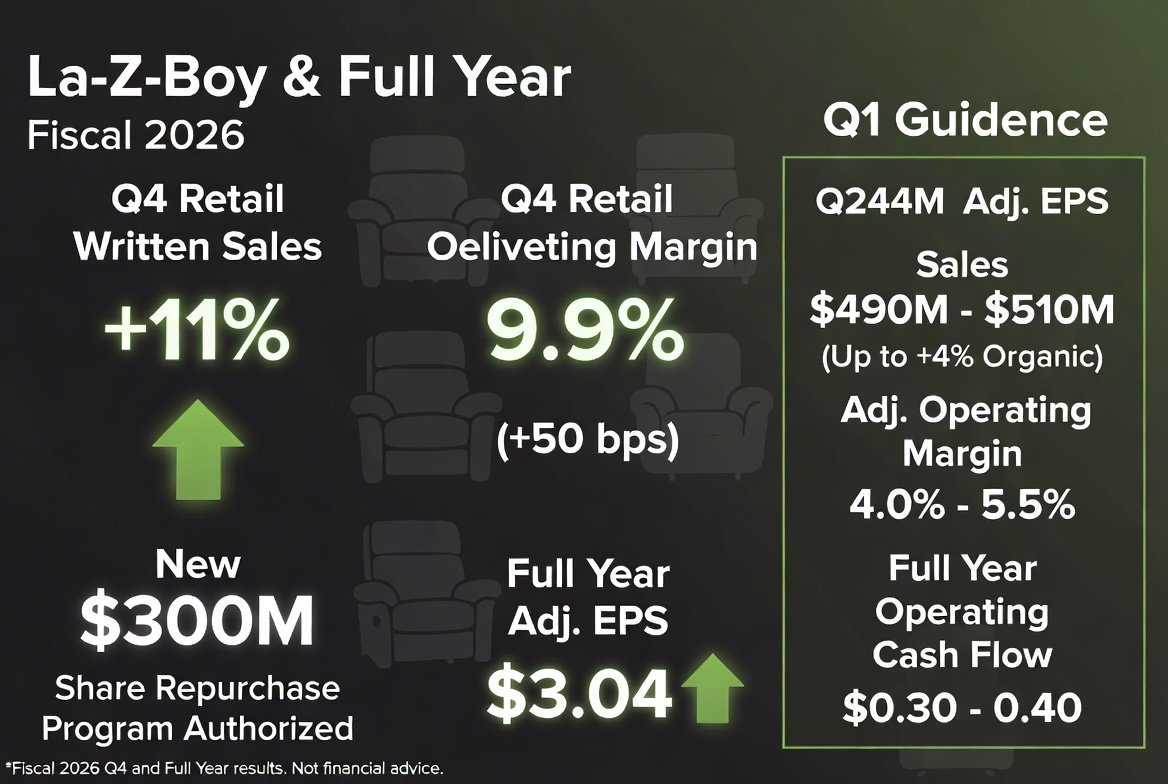

🛋️ LA-Z-BOY CRUSHES Q4 — 54% EPS BEAT, 37% EARNINGS GROWTH ON FLAT REVENUE | $LZB

La-Z-Boy delivered a stunning Q4 2026 double beat, crushing EPS estimates by 54% with 37% YoY earnings growth while keeping revenue flat — a pure margin execution story from the iconic furniture manufacturer.

EPS: $1.26 vs $0.82 est ✅ ( 53.66% beat, 37% YoY) 🚀

Revenue: $570.34M vs $569.23M est ✅ ( 0.19% beat, 0.00% YoY)

Q1 FY27 Guide:

Sales: $490M–$510M

Adj. Operating Margin: 4.0%–5.5%

Strategic Context: The 54% EPS beat on perfectly flat revenue is one of the most impressive margin execution stories of the entire 2026 earnings season — La-Z-Boy generated 37% more profit YoY without growing its top line by a single dollar. This signals dramatic improvement in manufacturing efficiency, product mix shift toward higher-margin items, or supply chain cost reductions that are flowing directly to the bottom line. In a housing market where $LEN posted -31% EPS YoY and $OPEN deepened losses, La-Z-Boy's ability to maintain revenue and dramatically expand margins is genuinely impressive — consumers may not be buying new homes, but they appear to be investing in furniture for their existing homes. The Q1 guide of $490M–$510M represents a modest sequential revenue step-down from Q4's $570M, typical for La-Z-Boy's seasonal pattern, with the 4.0%–5.5% adjusted operating margin guidance reflecting continued cost discipline. The 54% EPS beat suggests La-Z-Boy's management has implemented structural operational improvements that create a higher earnings floor — the kind of quiet turnaround that value investors find compelling in mature consumer discretionary names.

#LZB #LaZBoy #Furniture #Consumer #Earnings #Beat #MarginExpansion #HomeGoods #Manufacturing

35

$SNOA Q4 EARNINGS

❌ Adj. EPS $(0.33) missed $(0.24) est

YoY improved from $(0.48)

❌ Sales $5.561M missed $5.565M est (slight)

YoY ↑ 48.14% from $3.754M

264

April Jones *query trenches* retweeted

Malleable

(adj.) able to be pounded; capable of being molded; adaptable

#vocabulary #WordoftheDay

1

7

44

612

$LZB FISCAL 2026 Q4 EARNINGS

✅ Adj. EPS $1.26

YoY ↑ from $0.92

✅ Sales $570.338M (flat YoY)

Adj. operating margin 9.9% ( 50 bps)

FULL YEAR HIGHLIGHTS

✅ Adj. EPS $3.04

✅ Sales $2.126B ( 1% YoY)

Operating cash flow $204M ( 9%)

KEY MOVES

✅ New $300M share repurchase program authorized

✅ Retail segment written sales 11% Q4 / 8% FY

Q1 2027 GUIDANCE

Sales $490–510M (up to 4% organic)

Adj. operating margin 4.0–5.5%

254

La-Z-Boy ($LZB) reported EPS of 1.26(Adj) beating estimate of 0.82 for Q4 2026. Revenue 570.338 Million Vs 569.226264 Million expected.

Don't just watch LZB move, predict it! Build your own custom AI trading models for LZB today by downloading the FundSpec App on the Apple App Store or Google Play Store!

20

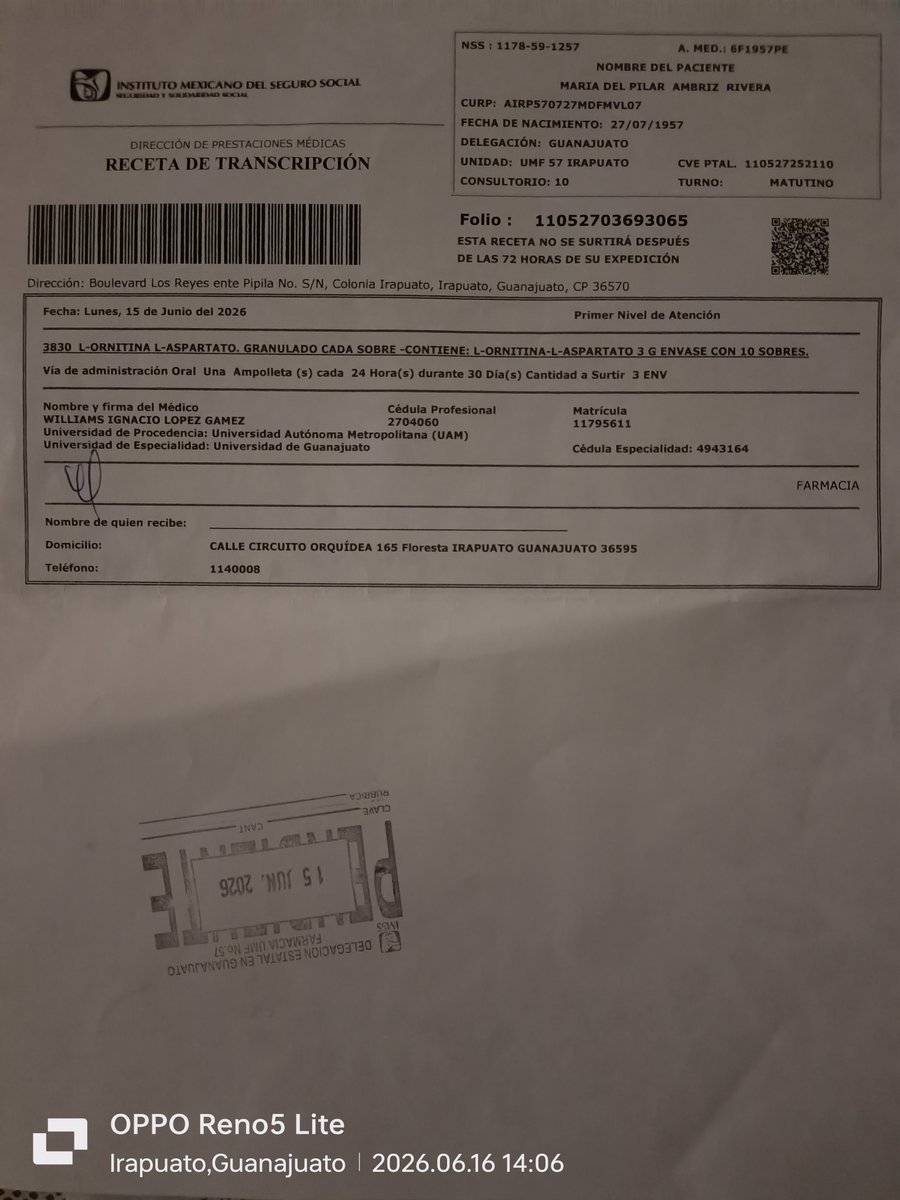

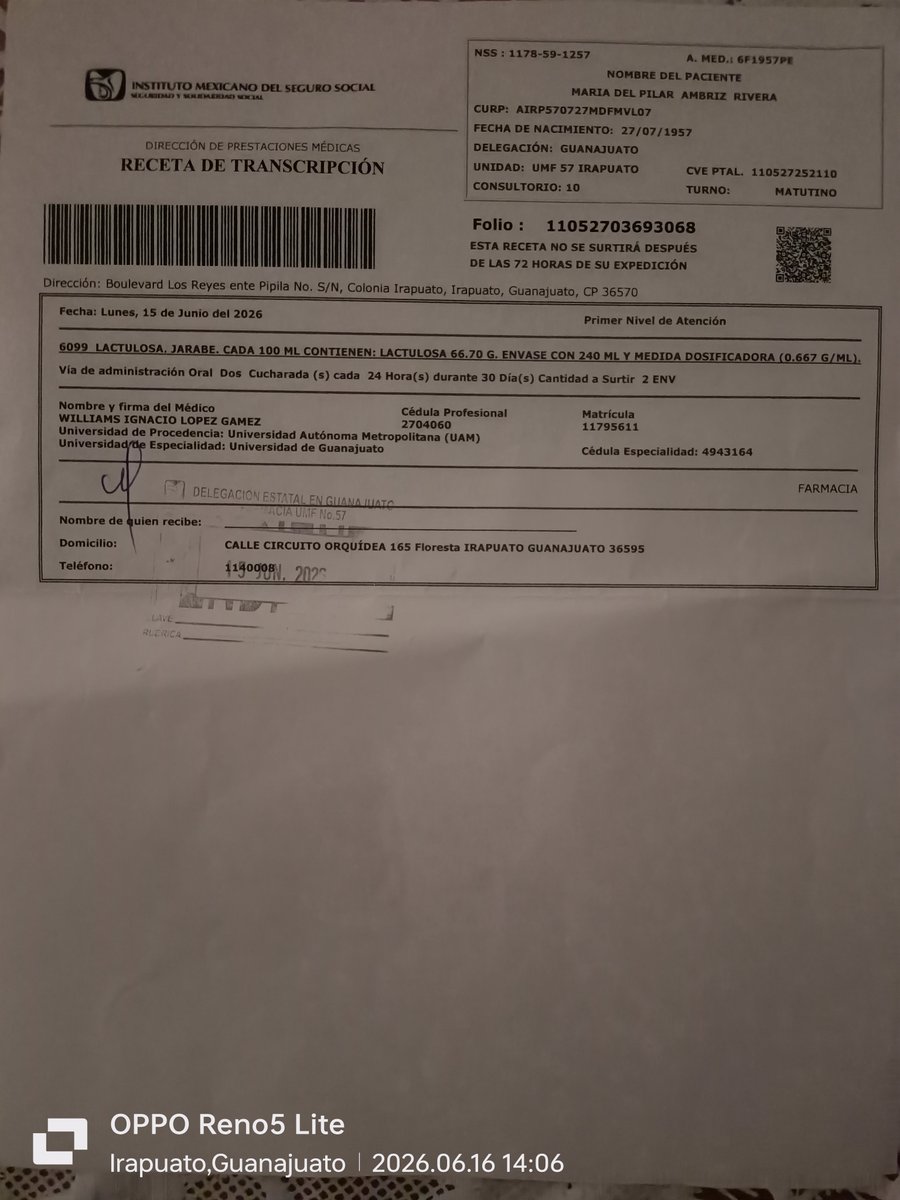

BT 🌞 nuevamente solicito su apoyo x mes a fin de conseguir medicina para mi esposa tiene Cirrosis Hepática no alcohólica L-Ornitina L-Aspartato y Lactulosa jarabe, adj. Recetas con datos Paciente NSS Clinica X Favor y gracias

Farm no hay

@Tu_IMSS

1

1

76