AK Panwar retweeted

MCD in News 📺

Showcasing our commitment to a cleaner, greener and more organised Delhi.

@LokNiwasDelhi @gupta_rekha @CMODelhi @praveshwahi

#Mcd #Mcdcares #Mcdnews #Delhi #CleanDelhi #GreenDelhi

10

2

6

1,365

"6/18発売 【乙女ドルチェ・コミックスCMOD】

身代わり姫は隣国の勇猛王に溺愛される(3)

amzn.to/43qvBRK

【FWコミックスオルタ】

フリースキルで最強冒険者 ~ペットも無双で異世界生活が楽しすぎる~(3)

amzn.to/4fGYyAh

【B.Pilz COMICS】

だしちゃいましょう先輩!

amzn.to/3S1Y0Lk

《AD》《PR》"

15

Jun 13

"6/18発売 【乙女ドルチェ・コミックスCMOD】

身代わり姫は隣国の勇猛王に溺愛される(3)

amzn.to/43qvBRK

【FWコミックスオルタ】

フリースキルで最強冒険者 ~ペットも無双で異世界生活が楽しすぎる~(3)

amzn.to/4fGYyAh

【B.Pilz COMICS】

だしちゃいましょう先輩!

amzn.to/3S1Y0Lk

《AD》《PR》"

29

@nishkumar1977 sir can you share chart on CMOD (LSE ETF). I think it can be the best proxy to the ongoing commodity bull run.

1

1

297

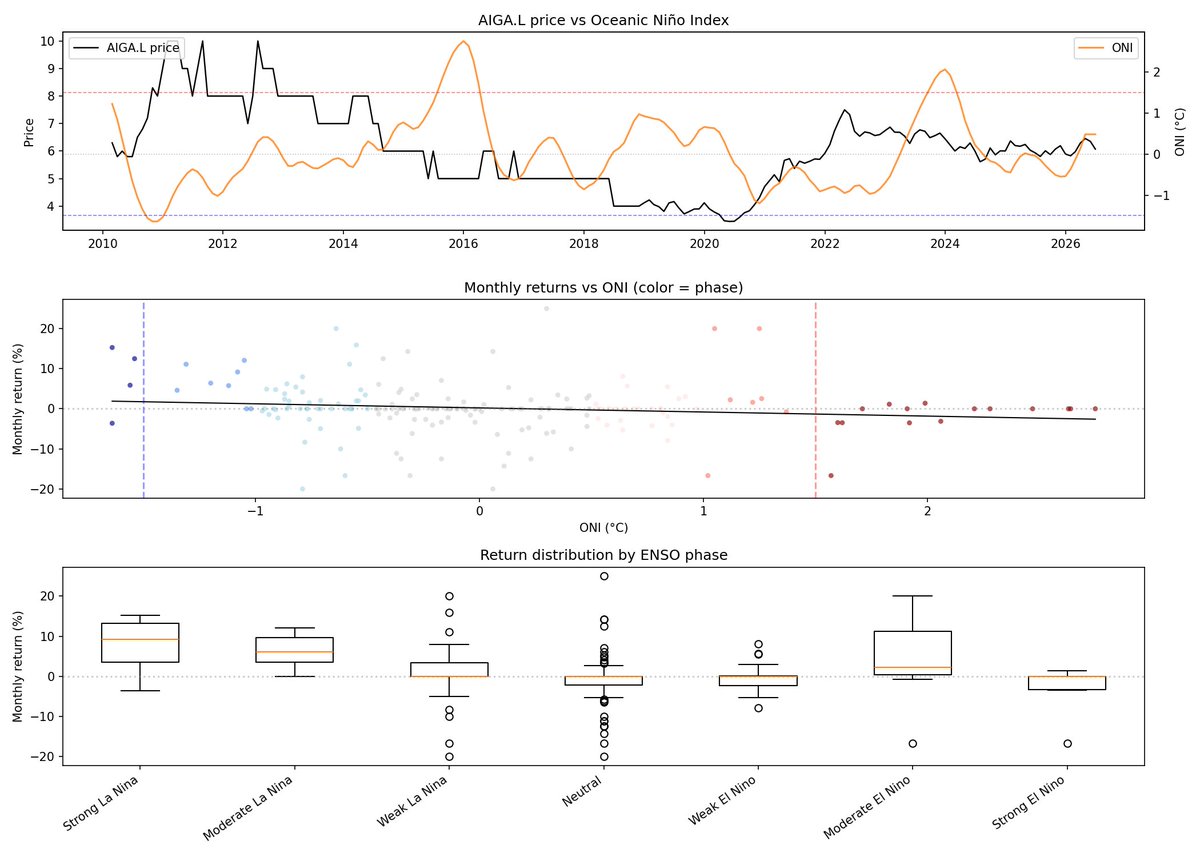

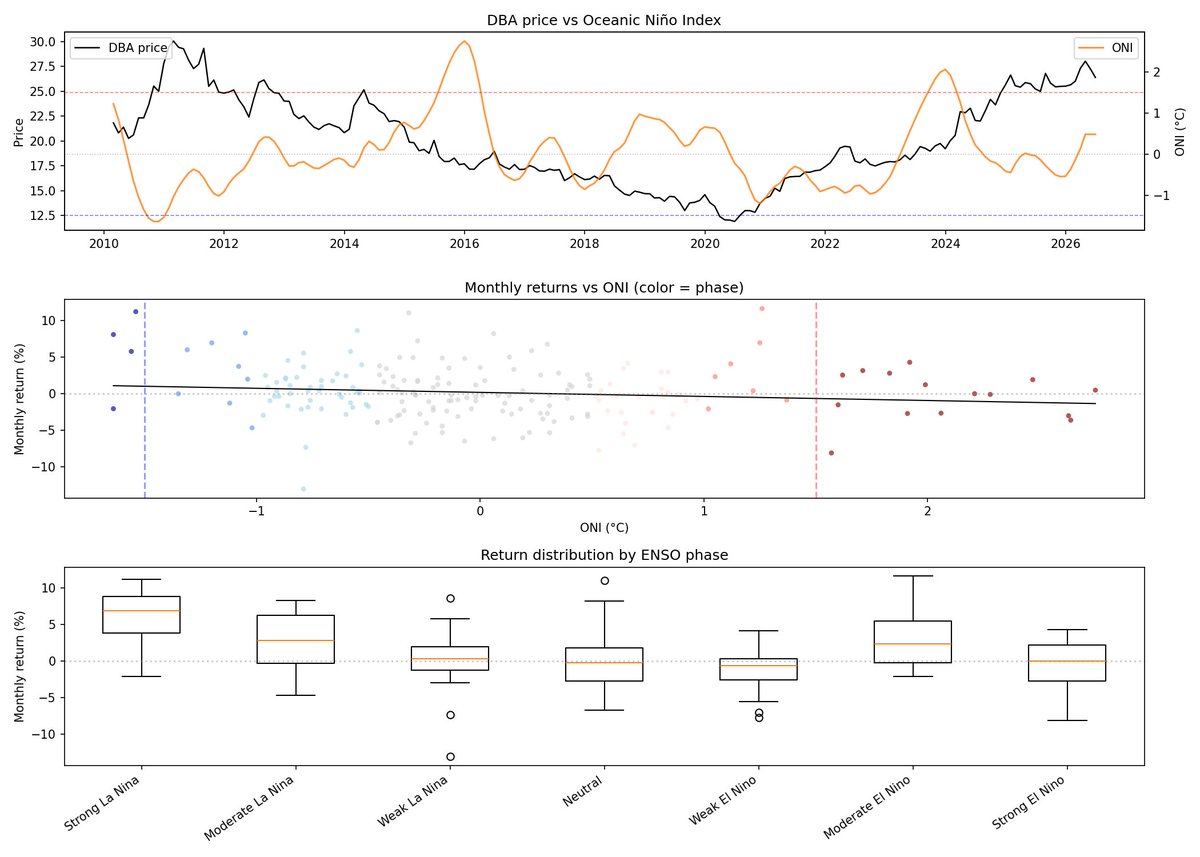

So, since this year we were bracing up for some "stronger than normal" El Nino event, i was interested in verifying how historically commodities (grains etc - especially the ones with strong exposure to India / SEA given those are the main areas hit) behave when this happens.

Despite El Nino (and in particular stronger El Nino) not only increasing temperatures in the area and increasing the chances of violent weather events that are indeed disruptive to agriculture, it seems that not only the market completely prices in, in most cases, these events, but that even overprice them, with El Nino event generally have no/negative influence on agricultural prices (using CMOD as one of the proxies, but since it's still very heavy gold and energy, tested against other more pure "grains / agriculture" tilted ETFs such as AIGA and DBA).

If anything, it's "La Nina" that has a relatively noticeable positive correlation with commodity prices (although no strong La Nina were recorded in recent times - after 2016, so we're basing our data points here mostly on Moderate and Weak events).

A strong El Nino also always (almost, 86%) translates in a rebounce in the shape of a "La Nina" within 2 years, however the strength of the latter is not statistically correlated to the strength of the former.

This is to say, essentially, that this mental exercise (and token usage as you can imagine) was... just that. There seem to be not a trade here for now.

To be noted that even for "La Nina" that seems to be strongly correlated to positive returns, there are fewer events and they all happened in a very specific time, namely late 2010, so it sucks for extrapolating generalized conclusions.

Commodities once again confirmed worst / most convoluted asset class to trade (even worse than forex imo).

7

1

34

6,461

बीजेपी दिल्ली से घमंडी अकडू असंवेदनशील मुख्यमंत्री रेखा गुप्ता को तुरंत हटा दे वरना BJP की सरकार केंद्र से भी चली जाएगी दिल्ली में आए दिन खून हो रहे है पावर कट लग रहे है और CM 1 लाख की कुर्सी पे बैठ के REEL बनाते रहती है

@dtc_union @dtchq_delhi @BJP4Delhi @gupta_rekha @cmod

Jun 3

जैसी #दिल्ली की मुख्यमंत्री #घमंडी और #अकड़ से भरी ठीक वैसा ही #DTC का मुखिया बदतमीज़ और असंवेदनशील और गैरजिम्मेदार

#DTC_अस्थाई_कर्मचारियों के बदले 300 रुपये वाले #मज़दूर लाने की बोल रहा था और आज 1000 रुपये प्रतिदिन वाले #होमगार्ड को उनके कार्यस्थल पर नहीं भेज रहा

DTC बचाओ

30

32

188

May 22

بازی hades 2 برخلاف تصورم رو تنظیمات high روی winlator cmod اجرا شد با 100 fps و میتونم از تجربه این بازی زیبا در گوشی روان لذت ببرم 🙂↔️

9

272

May 20

One thing I would bring to your attention is that gold is just gold. Meanwhile the other 2 are ETFs. Why not buy a broader commodity ETF? Something like Invesco Bloomberg Commodity UCITS ETF USD CMOD

1

2

134

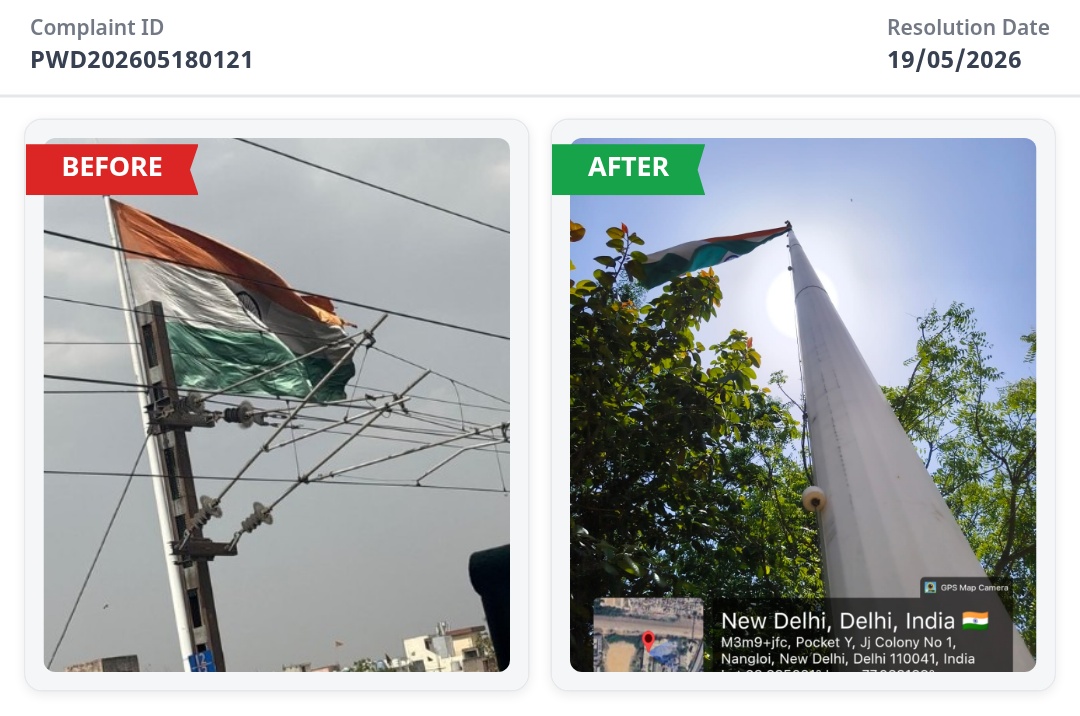

May 18

The flag near nangloi metro station is torn please change it. Our flag is country's most prominent symbol of sovereignty, unity, and identity.

@DelhiPolice @MCD_Delhi

@gupta_rekha @LtGovDelhi

@DelhiPwd @dcpouter

@ps_nangloi @CMOD @akshya_patra

2

2

165

May 11

#FF11

winlator CMODでFF11が動くと聞いてインストールしてみた!

インストールとアプデに24時間くらい掛かったw

サブ機のXPERIA 1 IVだとプレイオンラインビューアーが重くてログインするのに10分掛かるけどプレイ自体は問題なさそう

エンブリオストーリーまだ手付けてないからこれで遊んでみる

5

1,990

Same Delhi police sent notice to @talk2anuradha for defending general merit and tackling Bhim Army post! What is happening under your rule @gupta_rekha ji? Why is Delhi police not upholding law madam? @cmod

2

11

49

1,657

May 4

Community Moderator (CMOD)

As a mod I manage Discord server / Telegram group and keep it active and safe.

What i actually do to keep the community strong and healthy

• Remove spam or scammers

• Answer questions

• Keep conversations active

• Enforce rules

1

6

80