43m

General Motors Co. Deep Dive Scan - GM

Generated: 2026-06-15 09:48 PDT

Ticker: GM

Company: General Motors Company

Status: Research scan only. NFA.

Executive Read

GM is trading like a profitable legacy-auto value/capital-return story with new optionality layered on top: EV scale, Super Cruise/autonomy, and GM Energy/grid storage. The setup is cleaner than the old "legacy automaker is dead" narrative, but the stock is also near its 52-week high area, so the next move depends on whether buyers can reclaim the mid-$80s and hold above the $80-$81 base.

My read: GM is fundamentally stronger than the market usually gives it credit for. The company has real earnings power, raised 2026 EBIT-adjusted guidance, and still has a shareholder-return story. But it is not a clean growth multiple unless investors start valuing GM Energy, bidirectional charging, and Super Cruise as real platforms instead of side quests.

Live / Reference Snapshot

- Latest GM price: ~$83.91

- Intraday range: ~$82.03-$84.89

- Open: ~$82.79

- Market cap: ~$77.8B

- P/E shown by live feed: ~30.6x

- Latest trade timestamp: 2026-06-15 16:33 UTC

- Recent IR close, June 12: $81.50

- Recent 52-week high area: ~$87.62

Fundamental Picture

Q1 2026 Results

GM reported Q1 2026 revenue of $43.6B, net income attributable to stockholders of $2.6B, and EBIT-adjusted of $4.3B. That is strong enough to keep the company in "cash machine" territory even while the EV/autonomy transition remains expensive.

2026 Guidance

GM raised full-year 2026 EBIT-adjusted guidance to $13.5B-$15.5B, up from $13.0B-$15.0B, helped by lower expected tariff costs after a U.S. Supreme Court tariff decision. The company now expects gross tariff costs of $2.5B-$3.5B, down from $3.0B-$4.0B.

Updated 2026 guide:

- Net income attributable to stockholders: $9.9B-$11.4B

- EBIT-adjusted: $13.5B-$15.5B

- Automotive operating cash flow: $16.8B-$20.8B

- Adjusted automotive free cash flow: $9.0B-$11.0B

- Diluted EPS: $10.62-$12.62

- Adjusted diluted EPS: $11.50-$13.50

The key tension: EBIT guidance improved, but automotive operating cash flow guidance is lower than before. That keeps the story from becoming a clean victory lap.

Business Stack

1. North America Trucks / SUVs / Commercial

This is still the engine room. GM's full-size trucks, SUVs, vans, and commercial demand support the earnings base. The bull case starts here: high-margin ICE and fleet/commercial strength funding EV, autonomy, and energy optionality.

Risk: if macro slows or pricing weakens, the profit base can compress quickly.

2. EV Portfolio

GM remains a meaningful U.S. EV player, but investors are no longer willing to reward EV losses just because they sound futuristic. The bullish angle is not "GM becomes Tesla." It is "GM sells enough EVs, batteries, and charging products to protect share and create energy-adjacent revenue."

GM's battery strategy is becoming more diversified: LMR chemistry for better EV energy density, LFP possibly shifting toward storage products, and sodium-ion for industrial grid storage.

3. GM Energy / Vehicle-to-Grid

This is the newer upside story. GM is activating vehicle-to-grid capabilities for certain current EV/home-energy customers, working on commercial storage with sodium-ion batteries, and trying to connect EVs, home backup, and grid balancing.

The Verge reported GM says there are over 250,000 bidirectional-capable Chevy, Cadillac, and GMC EVs on U.S. roads, theoretically enough combined battery capacity to power 120,000 homes for up to a week. That is a real narrative hook, especially with AI data-center electricity demand stressing the grid.

Risk: investors may not pay for this until GM proves revenue, margins, and customer adoption.

4. Autonomy / Super Cruise

GM killed Cruise as a standalone robotaxi effort, but it has not abandoned autonomy. The strategy has shifted toward personal-vehicle autonomy first: Super Cruise, hands-free miles, and eventually eyes-off highway driving.

Business Insider reported GM has passed 1B hands-free miles with Super Cruise and plans eyes-off highway driving in 2028. Former Tesla Autopilot leader Sterling Anderson is central to the product strategy. That gives GM a credible autonomy angle, though it is slower and less theatrical than Tesla's robotaxi narrative.

Risk: GM spent heavily on Cruise, shut it down, and still has to convince investors the rebuilt autonomy effort can produce financial returns.

Technical Map

Box Theory / Darvas Setup

GM is pressing near the top of its recent range.

- Box top / breakout zone: $85.00-$87.62

- First resistance: $84.90-$85.00

- Major resistance: $87.62 52-week high area

- First support: $81.50-$82.00

- Key support: $80.00-$79.00

- Failed-break line: sustained loss of $79.00

Bull Case

- GM holds above $82.

- Price reclaims $85 with volume.

- Break above $87.62 opens a fresh 52-week high breakout.

- Guidance strength and buyback/capital-return narrative remain intact.

Bear Case

- GM rejects $85.

- Price loses $81.50-$82.

- A break below $79 turns the recent rebound into a failed-break setup.

- Macro/auto-credit worries or tariff/cash-flow concerns overpower the improved EBIT guide.

Catalysts To Watch

- Next earnings update and whether EBIT guidance holds.

- U.S. auto pricing and incentive trends.

- Truck/SUV demand and dealer inventory.

- EV margin progress and battery-cost commentary.

- GM Energy adoption: V2G, home backup, commercial storage.

- Super Cruise / eyes-off highway milestones.

- China performance and international profitability.

- Buybacks/dividends and capital return pace.

Risk Notes

- Auto earnings are cyclical. Strong profits can reverse fast if pricing/incentives move against GM.

- EV and autonomy are still capital-intensive and competitive.

- Cruise shutdown reduced robotaxi burn, but also damaged the old autonomy growth narrative.

- Cash flow guide is not as clean as EBIT guide.

- Near 52-week highs, the stock needs confirmation; chasing into resistance is lower quality than buying a retest or confirmed breakout.

My Read

GM is not the flashiest trade in autos, but it may be one of the more honest ones. The company has earnings, cash flow, guidance, and shareholder returns. The market question is whether GM can bolt enough credible future-facing businesses onto that base to deserve a higher multiple.

I would treat $85 as the first decision line and $87.62 as the breakout line. Above that, GM becomes a momentum/value breakout. Below $81.50-$82, it is back to range trading. Below $79, the setup weakens.

NFA.

X Draft

GM Deep Dive: GM ~$83.91, pressing the $85-$87.62 breakout zone after Q1 revenue $43.6B and 2026 EBIT-adj guide raised to $13.5B-$15.5B. Watch $82 support / $79 fail line. My read: real cash machine, but needs GM Energy Super Cruise proof for multiple expansion. NFA

Sources

- GM Q1 2026 press release / financial highlights: investor.gm.com/static-files…

- GM investor relations stock information: investor.gm.com/shareholders…

- SEC filing copy of GM Q1 2026 release: sec.gov/Archives/edgar/data/…

- Business Insider, GM autonomy / Super Cruise strategy: businessinsider.com/gm-cruis…

- The Verge, GM Energy / V2G / sodium-ion storage: theverge.com/transportation/…

- Live quote reference: OpenAI finance feed, GM, 2026-06-15 16:33 UTC.

2

48

(7/12) I also really like the incremental margin dynamics here. They consistently generate low 90% incremental gross margins and 50% incremental adj EBIT margins. Even on a GAAP basis, very solid incremental margins, >30% for incremental GAAP EBITDA

1

1

Mes prévisions 2026 (prudentes en espérant qu'elles seront dépassées)

💶 CA 2026 : 41 M€ ( 20 %)

📈 EBIT : 19,6 M€💰

💰RN : 12,5 M€ ( 25 %) soit un PER de 45 ce qui est tendu

📏PEG autour des 1,8

▶️Au niveau valorisation, le titre n'est pas spécialement donné mais lorsqu'on regarde les valo de SOITEC ou STMICRO (Oui je sais, ce n'est pas pareil mais cela reste le même secteur 😁😅) ... ou les valeurs US, c'est presque raisonnable 😅

1

2

58

La rentabilité est élevée

🔹Marge EBIT de 40,7 %

🔹Marge nette de 30 %

Le groupe entame 2026 avec 17 clients en production série d'eChucks (15 en 2025) :

➡️ Base de revenus récurrents

➡️ Exposition directe au boom IA / semi-conducteurs

1

3

160

Les chiffres 2025 :

💶 CA : 34,7 M€ ( 31,5 % vs 26,4 M€ en 2024)

📈 EBIT : 13,9 M€ ( 43 %)

💰 RN : 10,1 M€ ( 46,2 %) soit 30 % de marge nette

👌👌

1

3

222

Yes, och givet Clara bara bidrar Q2-Q4 blir det väl runt 13 mkr. Kräver ändock att core-CAG minskar EBIT med 7% yoy trots positiv kalendereffekt för att ”bara” nå 82m.

Räknar man mer rättvist kommande fyra kvartal (Clara helt inkluderat) skulle jag gissa på 90 mkr. Låt oss se!

1

2

139

It showed up for me at low EV/EBIT and high ROIC. Only shortly before price started to move.

1

1

33

🛡️ Comp #CMP wygląda spokojniej, ale bardzo solidnie.

Obszary działalności:

🔐 cyberbezpieczeństwo 🧾 urządzenia fiskalne

Q1:

📈 przychody: 27% do ponad 213 mln zł 📈 EBIT: 25 mln zł 💰 zysk netto: 18,7 mln zł 📈 zysk netto: 37% 📊 ROE: ponad 15,66%

9/10

1

15

🏢 Echo Investment #ECH rozczarowało Q1.

💰 zysk netto: 10,3 mln zł 📊 oczekiwania: min. 11 mln zł 📈 EBIT: 77,3 mln zł 💵 kurs: 5,11 zł po spadku sesyjnym

Rynek nieruchomości komercyjnych pozostaje trudny.

Presję zwiększają koszty finansowania.

8/10

1

17

TENOM, Oct 23 — Farah Pardani, wife of Ebit Irawan Ibrahim Lew or Ebit Lew, told the Magistrate’s Court here... f.mtr.cool/hnnnmqktwq

Of 25 organizational attributes tested, workflow redesign had the biggest effect on EBIT impact from gen AI.

Not model selection.

Returns live in the operating architecture above the model. (McKinsey, 2025)

2

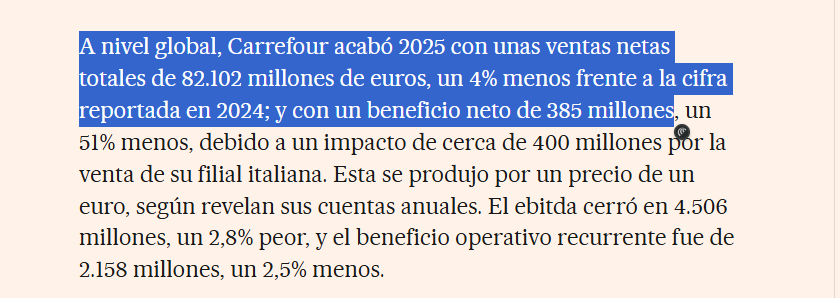

Revisa la fuentes donde coge eso gemini, porque ya te digo que el margen neto de Carrefour no es del 4%. Ese número corresponde más al EBIT. El resumen que te ha puesto es un batiburrillo de cosas que no se parece en nada a la realidad.

7

That is the face of the democrat party and how low they have sunk already. What a dirty monsters. Tell me this zlut did not know you could not use EBIT at the beauty shop. Stop voting democrat.

1

3