ゆみ🍀 retweeted

【情報解禁】

「ちょっとやってみようか」と

重い腰を上げてソロライブイベやります。

FREEZE!!

~インターネットイモムシ君の逆襲~

場所は大好きAgeha Baseさんです。

8/16です。

ご来場お待ちしております✨

【チケット予約開始は6/15 22時から!】

tiget.net/events/498262

4

5

7

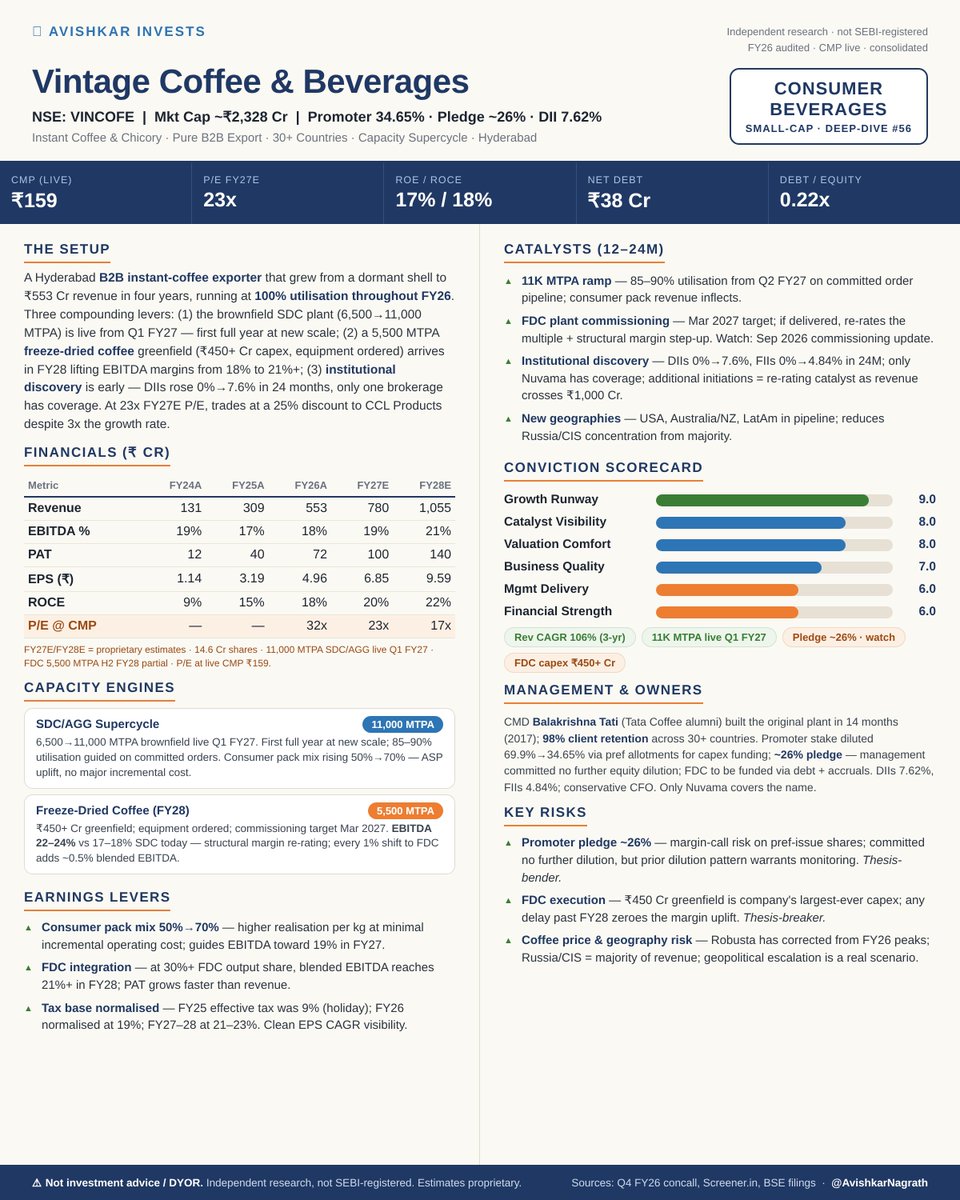

Vintage Coffee Business Deep Dive

India has CCL Products. Almost nobody talks about the company that's growing 3x faster.

Vintage Coffee & Beverages is a Hyderabad B2B exporter supplying private-label instant coffee to 30 countries — Russia/CIS, Africa, the Middle East, Southeast Asia. It started as a dormant listed shell in 2021. Four years later: ₹553 Cr revenue, 100% capacity utilisation throughout FY26, and two of the clearest growth catalysts I've found in the consumer space. Here's what's actually happening ↓

What it does

Pure B2B, export-first — no brand, no consumer retail, no complexity. Vintage supplies customised instant coffee in whatever format the buyer wants (bulk 25-kg boxes, consumer sachets, branded jars). Clients are institutional: large importers, private-label distributors, food manufacturers. The company has a 98% client retention rate over multiple years. Not because of lock-in contracts — because of quality, fast turnaround, and packaging flexibility that the big players can't match at this price point.

Two products: spray-dried agglomerated instant coffee (the Vintage Coffee plant), and instant chicory for Russia and Africa (Delecto Foods). Both are exports-led, both are B2B, and both ran at 100% utilisation through FY26.

**Why the next two years are different**

FY26 was the last year the company was capacity-constrained. From Q1 FY27, they're running on a 11,000 MTPA spray-dried/agglomerated plant — a brownfield expansion from 6,500 MTPA, delivered ahead of schedule. That's the first lever: simple volume compounding at a capacity 70% larger than FY26.

But the real re-rating is freeze-dried coffee (FDC).

Spray-dried coffee earns 17–18% EBITDA margins. Freeze-dried earns 22–24% — because it's a premium format, harder to produce, and commands 2x the price per kg. Vintage has ordered equipment for a 5,500 MTPA FDC greenfield (₹450 Cr capex), targeting commissioning by March 2027. If it delivers, FY28 blended EBITDA margin lifts from 18% toward 21% , and the company re-rates from a volume story to a margin story simultaneously.

**The institutional angle**

Two years ago, DIIs owned 0% of VINCOFE. Today they own 7.6%. FIIs went from 0% to 4.8% over the same period. Only one brokerage — Nuvama — covers the name. Market cap is ₹2,328 Cr. It's below the radar of most small-cap funds.

The thesis isn't that this stock is undiscovered. It's that institutional discovery is still in the early innings — and that as revenue crosses ₹1,000 Cr and FDC de-risks the margin story, additional analyst coverage and broader participation becomes the re-rating engine on top of earnings.

**The number that should make you pause**

Promoter stake has halved — from 69.9% to 34.65% — via multiple preferential allotments over three years. Each allotment funded productive capex (the brownfield, the Sep 2025 pref issue of ₹184 Cr for FDC). But the pattern is real, and there are roughly 26% of shares under pledge. Management has committed publicly (Q2 FY26 and Q4 FY26 concalls) to no further equity dilution — FDC to be funded via debt and internal accruals. That commitment is the line to watch.

The FDC capex itself is the other flag: ₹450 Cr is the largest project in company history. A delay past FY28 zeroes the margin uplift in the model. Trigger to watch: commissioning announcement by Sep 2026.

A compounding capacity story with a genuine margin re-rating ahead — in a sector that's still largely undiscovered by the institutional market. The risks are real and known. The opportunity is in understanding both.

Disclaimer: Not investment advice. Independent research, not SEBI-registered. Please DYOR

1

🇬🇧 🇪🇺Kevin Wilson 🇪🇺 🇬🇧 🚫 No DMs retweeted

Jobs for young adults is a pressing issue of our times.

One possibility is that a freeze or reversal of the state pension age could release jobs for younger adults.

It could also give a respite to senior citizens being worked to death.

What do you make of the Minister's reply?

42

292

536

9,467

There are four matches on today, so the plan is to watch football while tackling a long-overdue round of cleaning. The Morocco vs. Brazil match this afternoon was so entertaining that the vacuum cleaner ended up running in the same spot for about five minutes before anyone noticed. Apparently cows sometimes freeze while grazing so they can listen for sounds around them. Felt a bit like a cow this afternoon, haha.🐮

Looks like rain later tonight. A little cooler weather would be nice too.

4

RT @AzzisDallasWing: i’m crying what could’ve made her freeze for that long 😭😭

AZZI’S DALLAS WING

AZZI’S DALLAS WING

154

Matt Mako retweeted

❗️ACE OF THE SKIES ENTRANT❗️

The second to enter this year’s AOTS is Don Freeze!

After a impressive showing at Aniversario he looks to freeze out the competition in Power Pro’s most dangerous match!

Tickets for all 3 nights of Trios are on sale now at powerprolucha.com

9

19

401

adrina⋆𓏲ּ𝄢🪽’s 🆙 retweeted

what did azzi tell her for her to freeze like that 😭

AZZI’S DALLAS WING

2

14

751

13,359

Lol no you can't. Nobody except an actual gun nerd thinks of "the iconic and very specific safety lever of the AK-style platform" when he pulls this out for a few seconds in an action scene. And even that's on freeze frames or aforementioned high res display images.

USA ❤️🇺🇸 ✝️🙏 retweeted

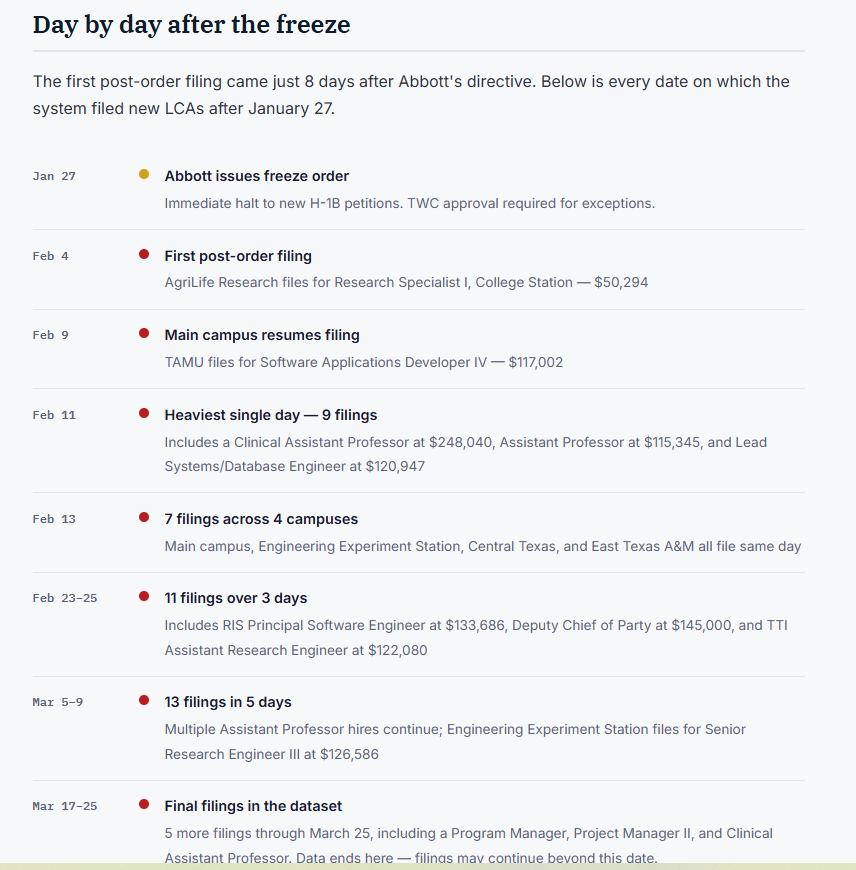

Texas A&M Filed 57 Certified H-1B Applications After Abbott's Freeze Order

Governor Abbott ordered an immediate halt to new H-1B petitions on January 27, 2026. Federal records show the Texas A&M University System kept filing anyway — 61 applications in 58 days, 57 of them certified by the DOL.

guestworkervisas.com/tamu_h1…

39

326

531

8,883

𝙨𝙠𝙮𝙧𝙖 retweeted

14h

everyone freeze this is peak

11

111

1,239

39,262

ok time to freeze frame this every millisecond and see if i can find myself

2

8

171

RedGrapes retweeted

JB Pritzker was prepared to lock in a 40-year tax freeze for politically connected mega-developers on the backs of Illinois homeowners getting crushed by property taxes.

The billionaire governor serves the billionaire class.

25

110

454

5,774