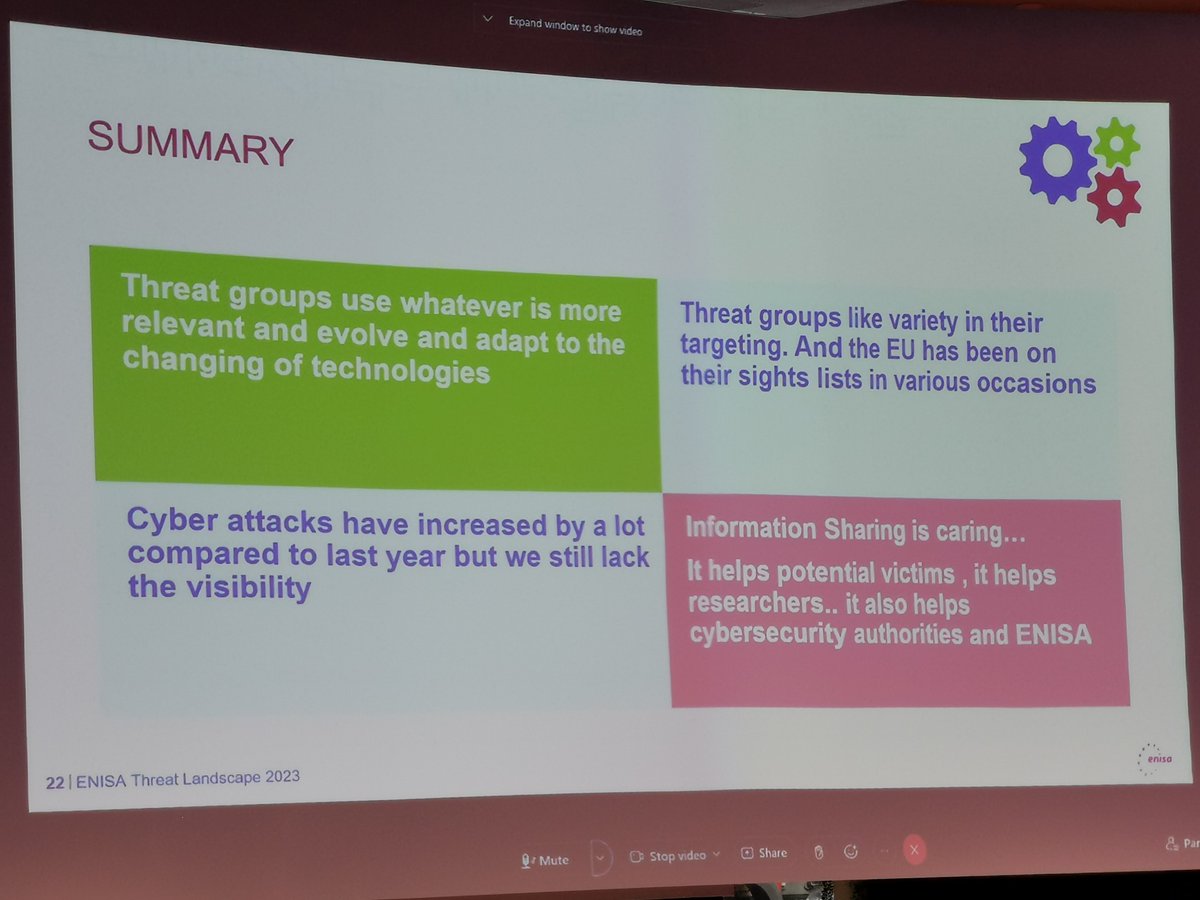

10 Jan 2025

#Evo, $Evo,@Evo - Goldman Sachs raised Evolutions target share price with a buy to 1 670 SEK, on 26 April 2024 and the other day they lowered it to 1 000 SEK due to lowered growth than expected.

More loose speculation seem to be behind adjusting their recommendation to current share price conditions than a quality based analysis with conclusions regarding future slower growth potential.

What is really new except a couple of temporary challenges:

1. Workforce and studio limitations - temporary slowing growth - has nothing to due with slowed demand

2. Hackerattacks in Asia - normal problems to be handled if you have business on the internet - has nothing to due with slowed demand - just yet to be quantified and officially mitigated.

3. Uncertainties with revision of license in UK- not material, out of the 3 % revenue from UK more than 95 % are coming from licensed operators. - Not a material problem and it has no bearing on other authorities.

Evo is blocking illegal traffic and those players will likely find their way back to Evo through other licensed operators.

There is of course no reason for a gambling commission to revoke a license and make 95 % of Evos legal players illegal or incitamentized to be illegal in that market.

You just need to block a behavior that doesn't support channelization and ultimately don't provide the government with taxes.

Conclusion: The lower growth than expected is in no way related to weaker demand its mainly related to limitations in the available workforce in Georgia due to strikes and in some part hacker attacks in Asia.

The effects has also materialized in the report with fewer reported game rounds, but still the company has been able to increase revenues since Evo focused their service to the more profitable customers in certain affected markets.

In the Q3 report in 2023 the market was also disappointed but only one quarter later Evolution showed the market it had capability of quickly ramping up their workforce and initiating new studios resulting in a quick ramp up of workforce between Q3 2023 and Q4 2023. Analysts like Goldman where happy and quickly increased their share price targets...

Is there any reason why they shouldn´t be able to mitigate the same challenge again, they already done it one time - repetition is not the hardest thing to accomplish.

Is there really any likely fundamentals that motivates Goldman going back and forth in their opinion of the future - especially since its pretty obvious they are not reading it correctly - I say history will most likely repeat itself both when it comes to Evos coming ramp up of both workforce and products and that will again affect Goldman with revised valuations and target prices.

In the Q/A after the Q3 2024 the CEO of Evolution was very clear with the fact that Evolution was investing heavily in their growth and still had great margins which he by the way didn´s see any structural changes in going forward - I guess Goldman wasn´t on the call.

2

54

5,388

28 Dec 2024

Detta är mina hackerattacks och solstormssäkrade maskiner

28 Dec 2024

Klar fördel med veteranbil.

Dataläcka hos Volkswagen – 800 000 elbilar drabbade (via @omni_red) omni.se/a/gwybzA

2

19

770

1 Feb 2024

Gradi se savremeni svet vetrenjača, a gde je Don Kihot? Da li se svet izokrenuo i da li su ga zamenili zlonamerni hakeri? Potencijalni sajber napadi na vetroparkove i kako ih na vreme zaštititi. I ne samo njih.

#Energy #WindFarms #HackerAttacks #Vulnerability #CyberSecurity

interestingengineering.com/e…

3

166

23 Jan 2024

What are the TOP10 cubersecurity trends nowadays❓ Learn from Apostolos Malatras who represented @enisa_eu during "6Gsec CP²"👏 #cybersecurity #hackerattacks #6G #AI

3

5

423

25 Nov 2023

blocktempo.com/htx-is-attack…

🌐🔒 Invest with Confidence: Atlantis Exchange Sets the Standard for Security in FinTech! 🔒🌐

🚨 In a landscape where cybersecurity threats are on the rise, our commitment to safeguarding your investments has never been SO STRONGER. Check out the latest report on hacker attacks and see why Atlantis Exchange stands out: blocktempo.com/htx-is-attack…

@justinsuntron

@cz_binance

@heyibinance

@a16zcrypto

✅ Atlantis Exchange, a registered entity with the U.S. Department of the Treasury, proudly upholds the pillars of legality, compliance, and security. Our innovative FinTech solutions have not only disrupted the industry but have also withstood the test of time. Over the past two years, our robust security measures ☂ have proven highly effective, ensuring zero incidents of hacking or theft!

💡 In stark contrast, a majority of crypto exchanges lack the crucial elements of governmental legitimacy and compliance. These platforms frequently succumb to diverse hacking attacks, resulting in staggering losses of multi-million dollars in users' funds.

💰 For retail cryptocurrency traders seeking swift profits, the risks are evident. Many crypto exchanges compromise on security, leaving millions of hard-earned assets vulnerable to overnight obliteration.

🤝 At Atlantis Exchange, we understand the value of your investments. By prioritizing legality and compliance, we set a foundation that not only protects your assets but also establishes trust in the volatile world of cryptocurrencies.

🛡 Your security is our priority. Don't settle for less. Choose Atlantis Exchange and experience a level of protection that goes beyond expectations.

💼 Join us, where legality, compliance, and security converge to create a fortress for your investments. The term "韭菜" in Chinese may describe many, but with Atlantis Exchange, you can redefine your crypto journey with confidence!

#AtlantisExchange

#legitimacy

#legality

#Compliance

#investments

#confidence

#crypto

#CryptocurrencyTraders

#FinTechSolutions

#cybersecurity

#HackerAttacks

#Huobi

#HTX

18

19

48

5,838

23 Nov 2023

#BlackFriday: the risk of #hackerattacks increases significantly.

#Phishing becomes more sophisticated.

🌐Be wary of suspicious websites

🔗Don't click on ambiguous links

💻Protect your devices

💳Use a virtual card for online purchases

bit.ly/HWGSababa

2

2

129

20 Sep 2023

✅ColdStack follows the highest standards in #backup & #recovery.

📌It makes you confident that all of your data will be safe if there are any #hardware issues, information leaks or #hackerattacks.

All for the lowest possible price!

2

3

22

1,618

9 Sep 2023

Beware of impostor apps in the Google Play Store. Fake Telegram apps have been stealing data from millions of Android users.

Read: thehackernews.com/2023/09/mi…

👀 Check Out Old Tweets Of @TodayCyberNews

#infosec #hacking #hackerattacks #CyberSecurity

2

12

1,753

7 Sep 2023

🌐 Experts record a two-fold increase in the number of attacks on corporate networks

⚡️ According to RTK-Solar, in the first half of 2023, the contribution of cryptominers to network traffic doubled. The share of cyberattacks using SSL encryption to hide malicious activity has increased by 53%

⚡️ The most popular method of penetration is still network attacks.

⚡️ According to RTK-Solar, over the past year, the amount of damage to large Russian companies from cyberattacks has increased by a third on average and amounted to at least 20 million rubles.

👀 Check Out Old Tweets Of @TodayCyberNews

#infosec #hacking #hackerattacks #CyberSecurity

ALT 🌐 Experts record a two-fold increase in the number of attacks on corporate networks ⚡️ According to RTK-Solar, in the first half of 2023, the contribution of cryptominers to network traffic doubled. The share of cyberattacks using SSL encryption to hide malicious activity has increased by 53% ⚡️ The most popular method of penetration is still network attacks. ⚡️ According to RTK-Solar, over the past year, the amount of damage to large Russian companies from cyberattacks has increased by a third on average and amounted to at least 20 million rubles. 👀 Check Out Old Tweets Of @TodayCyberNews #infosec #hacking #hackerattacks #CyberSecurity

2

8

1,150

17 Apr 2023

Reports of #hackerattacks are mounting, and in the coming years companies will be required by law to protect themselves against cyber crime.

phoenixcontact.com/en-ca/ind…

#industrialsecurity #industrialcommunication #industrialnetworks

1

2

65

🌐 The more complex the online world, the more complex #hackerattacks and #cybercrime become.

🎓 Therefore, it is more important than ever to train experts in this field: Three German #universities have programmes on #cybersecurity. 👇

#StudyInGermany

spkl.io/60114wLRP

5

8

2,083

2 Feb 2023

🌐 The more complex the online world, the more complex #hackerattacks and #cybercrime become.

🎓 Therefore, it's more important than ever to train experts in this field: Three German #universities have programmes on #cybersecurity. 👇

#StudyInGermany

deutschland.de/en/topic/know…

4

10

1,975

9 Dec 2022

Q. What's a hacker's favorite season?

A. Phishing season🎣

We have your back - STAY INFORMED 👇

#phishing #hackerattacks #infosec #cybercrime

youtube.com/watch?v=8XMsWRYL…

3

8

RT kaspersky "Q. What's a hacker's favorite season?

A. Phishing season🎣

We have your back - STAY INFORMED 👇

#phishing #hackerattacks #infosec #cybercrime

youtube.com/watch?v=8XMsWRYL…"

1

1

2

1 Dec 2022

Q. What's a hacker's favorite season?

A. Phishing season🎣

We have your back - STAY INFORMED 👇

#phishing #hackerattacks #infosec #cybercrime

youtube.com/watch?v=8XMsWRYL…

2

4

16 Nov 2022

Cyberattacks remain a constant threat. People around the world should be prepared for #cybersecurity incidents.

Rest assured Kaspersky has your back!

Learn from our experts on our Daily Blog 👉

#atp #atpgroups #cyberattacks #hackerattacks kas.pr/xh9b

2

2

16 Nov 2022

Q. What's a hacker's favourite season?

A. Phishing season!

Phishing season is always open. Want to be prepared? Here are 10 Symptoms indicating an Hacker attack 👉 kas.pr/j7yk #phishing #hackerattacks #infosec #cybercrime

5

3 Sep 2022

Most of the servers involved—succumbed to #HackerAttacks|

#HKPF:

🔵exchanged intelligence w/ 🇨🇳security dept

🔵received INTERPOL’s assistance in finding🇭🇰victims overseas

🇨🇳authorities arrested 12 suspects for committing 31 naked-chat scams in🇭🇰(defrauded victims of HK$366,500)

2

3

12

3 Aug 2022

❌¿Cuáles son las señales de aviso a las que debes prestar atención?❌

¡No te pierdas el post de nuestro blog! ow.ly/uL5P50K8oCR

.

.

.

#ciberseguridad #PandaSecurity #cybersecurity #seguridad #security #hackerattacks #vulnerability #virus #Pandasecurity

2

20 May 2022

🤖En España el delito de sextorsión afecta a 6.000 personas y sólo tres de cada diez denuncian ante las autoridades. 👉 ow.ly/rm6Z50JcM2P

#ciberseguridad #PandaSecurity #hackers #Hacker #cybersecurity #security #seguridad #hackerattacks #vulneravilidad #vulnerability

1

1