Big bull retweeted

3 Mar 2025

#hellox #MondayMotivation #hotwifeannu #anamikasingh #Queen

@annusingh378 .

@mishu_cam @Cam_Mansi @DIMPLE_48 @sizzlingdivya_ @VanessaSha24645

14

30

178

23,112

Jun 6

6.6.2026💫✨Saglıq,şans,yüksəliş,bərəkətlə ürəyimizdə olan istəklər həyata keçsin✨🪄🍀 #Manifesting #HelloX

12

53

759

Helloとしてこれからより一層コンタクトセンター向けAI事業のHelloXにリソースもお金も投下していきます

3

656

Finally on X! 🚀

Here to push boundaries, share insights, and grow the MTs Coin ecosystem. Let’s connect and build the future together! 💡🪙

#MTsCoin #HelloX #DigitalFrontier #Innovation

7

2

16

576

আজকের সন্ধ্যাটা এমনই মনোরম। প্রকৃতির সাথে কিছুটা সময ় কাটাচ্ছি। আপনাদের সন্ধ্যা কেমন কাটছে?

#RelaxingTime #Mindfulness #CommunityUpdate #HelloX

2

2

36

Apr 23

His darling son/ dear boy is a Fri king idiot. Charles needs to smell the roses, Henry will be his downfall. Henry is a walking minefield, doesn’t need Hellox or whatever they are called.

2

123

Apr 22

Mark wanted me to be a sheep, so I chose Musk’s 'X' to remain a Lioness. 🦁

Facebook was a crowded market of lies; I'm here for the silent whispers of Truth.

The Intellectual Laboratory is now officially open on X! 🧠🔬

#HelloX #FreeSpeech #AngelinaBlaze"

2

3

7

Hello X 👋🏽

Finally posting after opening this account in 2022… better late than never 😌✨

I’m looking for who will take me around X 🌝

Say hi, I don’t bite 💕

#FirstPost #HelloX #NewHere #FreshStart #SoftLaunch

2

2

6

177

Apr 10

Seeking reality, fueled by patience, headed toward success. Simple thoughts from a simple girl."

#HelloX #Growth

#GoodMorningX

3

2

23

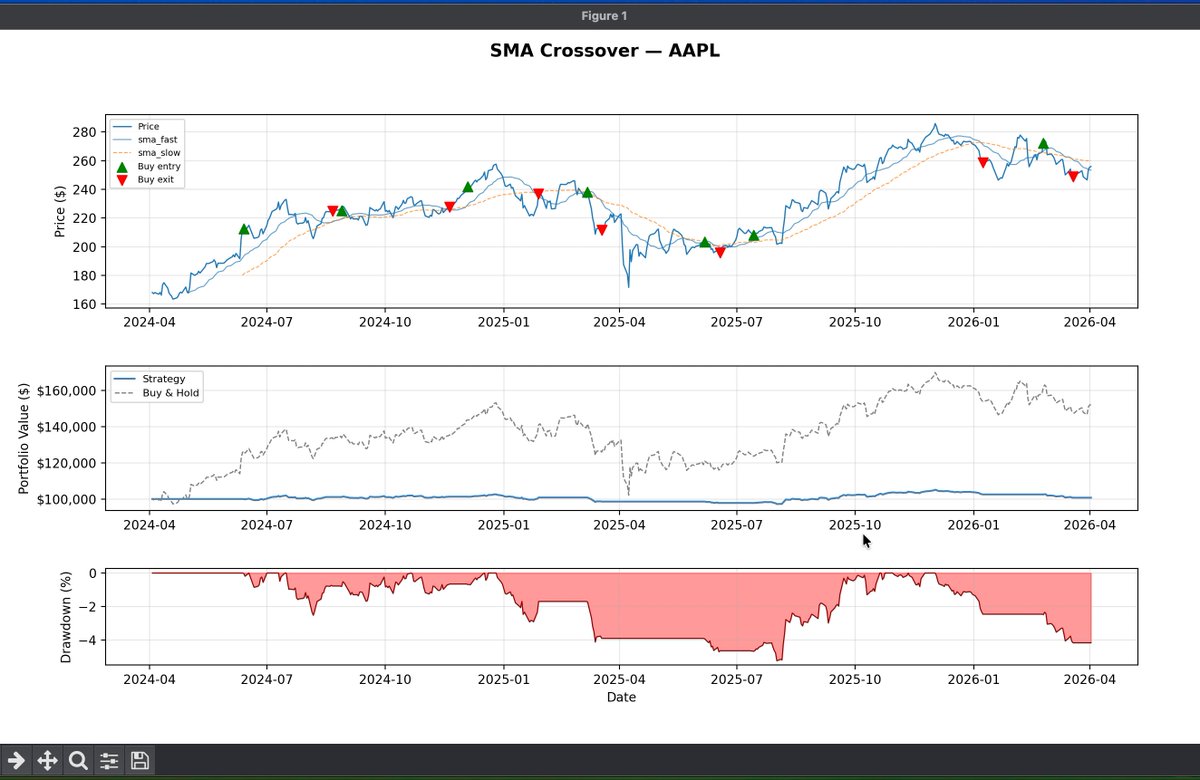

i'm 19, and I just built my first algorithmic trading backtester from scratch in Python.

I don't think I completed any online tutorials properly, but I started reading ML books on trading, focused on current algo traders' experiences, and got started.

My first version showed 800% annualized returns. I thought I was a genius. Turns out I had look-ahead bias in every single signal; the model was peeking at future prices to make today's decisions. Fixed it. Real results are way more boring. That's the point.

Here's what's actually inside it:

- 4 strategies: SMA Crossover (20/50-day), RSI Mean Reversion (14-period, 30/70 thresholds, built the EWM math myself), MACD (12, 26, 9) via histogram crossovers, and Bollinger Bands (20-period, ±2 std dev) with midline exits.

- The engine runs event-driven, bar-by-bar. Every signal is shifted 1 bar forward so the model only acts on what it actually knew at the time. 3 position sizing methods including Kelly Criterion. 5% stop-loss, 10% take-profit, 20% max per position. 0.1% commission 0.05% slippage baked into every trade.

- Output: 10 metrics: Sharpe, Sortino, Calmar, Max Drawdown, Win Rate, Profit Factor, printed in a color-coded terminal table. One CLI command runs all 4 strategies on any ticker and exports a comparison chart.

Just getting started. If you work in systematic trading or quant research, I'd love to learn from you.

Open to feedback, it was my first project, definitely not expecting it to be impressive, but I got my foot in the door!!

#MyFirstTweet #HelloX #AlgoTrading #QuantFinance #Python

1

2

49

"Hi, I’m Ifedimma,

I'm new to this space, I'm a ghostwriter and fashion designer. I love crafting stories, creating style, and sharing honest book reviews 📚. I’d love to connect with people and book lovers, If you don't mind. Let's Connect, Thank you.#LetsConnect #HelloX

1

1

4

90