7 Oct 2025

The path forward for $SMLR:

1. Vote NO to the acquisition.

2. Divest from QuantaFlow. Use proceeds to purchase

Bitcoin and pay down Coinbase loan.

3. Gut the medical business. Minimize overhead.

4. Implement a share buyback program, buying

whenever diluted mNAV < 1.00.

4

8

1,738

11 Nov 2024

I don’t believe the core business is dying. It is actually expanding with pending approvals for their Quantaflow product.

4

106

19 Oct 2024

I have spent last two weeks diving into #SMLR in a lot more detail as I wanted to better understand what they are about and whether this vehicle is indeed an undervalued alternative to expose yourself to @saylor‘s playbook.

Also @_adrian's recent Space with @SemlerEric was very informative and compelled me to put together an investment thesis on the stock. It goes without saying that the following is not investment advice, but simply documents my analysis how SMLR's market capitalisation could play out in the coming quarters.

TLDR-VERSION:

- Based on the company‘s growth prospects in the detection of peripheral artery disease (PAD) and its existing strong operating cashflow, its capacity to issue debt for the purchase of #Bitcoin is very compelling

- I ran three "BTC build-up via debt issuance" scenarios until Q4 2028.

- Depending on the scenario you look at, the company could see a 3x (bear case) to 15x (bull case) increase of its valuation by end of 2028

- Assuming inflation of 7.5% p.a. for USD in the next 4 yours, you would still end up with a real multiplier of 2.3x (bear) and 11.6x (bull)

ANALYSIS:

I looked at the following aspects:

1- The nature and the cost of its PAD core product, QuantaFlo, compared to established incumbent products

2- Academic research on the efficacy of QuantaFlo, compared to established incumbent products

3- The size and growth of the PAD market

4- The politics and regulatory trends around preventative diagnostics in the US

5- Its strategic positioning as a SaaS

6- its operating cashflows in the past and forecasts based on existing analyst reports and the anticipated market growth in the PAD segment

7- Its ability to issue convertible debt to acquire Bitcoin

8- Risks to its core business and ability to execute the “flywheel”

On that basis, I constructed a quarterly financial model until Q4 2028 to simulate revenues, operating costs, operating cashflows, interest coverage ratios, convertible bond issuances and #bitcoin purchases. It is important to note that the model is partial, i.e. it puts the emphasis on SMLR's actual ability to issue debt, which in turn is the main drive for the BTC Hodling strategy.

The ability to issue debt is determined by its growth in operating cashflows to cover the debt service and the interest rate that investors into SMLR convertible bonds will demand.

On these two points there is currently a clear divergence from its big brother #MSTR:

- On the one hand, its operating cashflow is far healthier and highly scalable if revenues start going back up and by using an interest coverage ratio of 2.5x we can determine how much debt it can draw per quarter without overburdening the company's financial health.

- On the other hand, the company suffers from the lack of an options market which investors could otherwise play to lock in arbitrage profits by exploiting volatility differences between bitcoin and the stock itself.

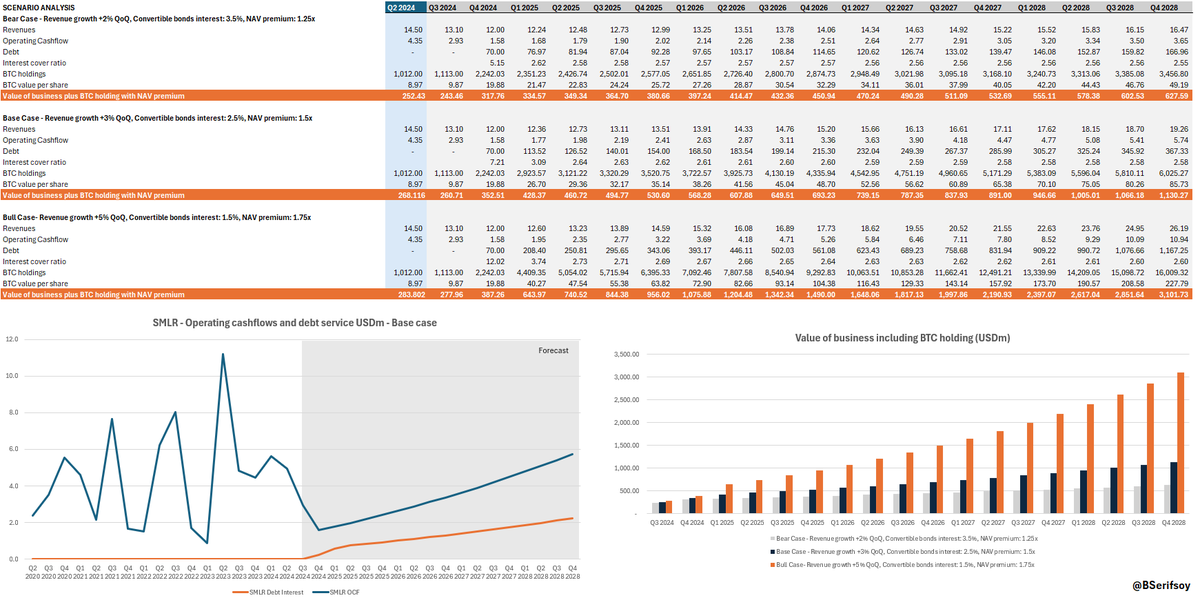

I have run three scenarios, a bear, base, and a bull case (see below charts and table).

The scenarios vary in three core assumptions:

- QoQ revenue growth: 2% / 3% / 5% for bear / base / bull scenario

- Convertible bond interest rate: 3.5% / 2.5% / 1.5%

- NAV premium for BTC holdings: 1.25x / 1.5x / 1.75x

Beyond that the model assumes that bitcoin's price will increase QoQ by 3% until Q4 2028, which I hope people agree is reasonable.

Those that know me a bit will know that my name is pronounced "Bearish", so I will stick with the most cautious set of assumptions, but feel free to adopt a different name for yourself 😉

Even in the pessimistic scenario, the strength of SMLR's cashflow will lead to a significant build up in bitcoins, from currently about 1,000 to close to 3,500 by end of 2028.

If investors also reprice SMLR to include a small NAV premium of 1.25x (compared to 0.22x at the moment when stripping out the core business's standalone valuation), we should see a valuation of over USD 600m compared to under 200m at the moment. Even allowing for rampant USD inflation of 7.5% in the coming years, this would yield 2.3x multiple

Now, the real excitement would happen if both SMLR starts penetrating the PAD market more deeply and its additional products come online. Assuming a 5% quarterly revenue growth rate in the bull case, this would substantially improve operating cashflows.

Add to this the turbo charger that an options market in SMLR would deliver, we can comfortably assume that its convertible bonds could be issued at 1.5% instead of 3.5% in the bear case.

That massively increases its ability to issue debt (from 166m in the bear case to USD 1.2bn in the bull case) and with that SMLR would purchase a far larger number of bitcoins (over 16,000 coins compared to 3,500 in the bear case).

In parallel to that the BTC value of each share (holding its current 7m shares constant), would rise from currently about USD 10 a share to USD 227 per share (and to USD 49 per share in the bear case).

There are many more facets to this which I won't belabour, but overall this is exciting and consequently I have built a significant position in SMLR alongside MSTR. I don’t expect SMLR to explode imminently, as there are still aforementioned issues that the company has to work through, but as I am a long-term hodler I believe this should be a profitable trade in the years to come

FURTHER DEEP DIVE ON THE ABOVE POINTS:

Ad 1

Quantaflo is essentially a testing device for detecting peripheral arterial disease (PAD). It is non-invasive and relatively inexpensive, making it very attractive for clinics and insurers looking to identify cardiovascular risks early. It is an FDA "cleared" (as opposed to "approved") product, which requires it to demonstrate "substantial equivalence" to a legally marketed predicate device. Clearance is a quicker route but it is prone to scrutiny. As Eric mentioned in the Space, he feels that there is some political meddling possible, the "Elizabeth Warren-short" so to speak. Its costs are way below those of the more established products, such as the Ankle-Brachial Index (ABI), which is considered the gold standard.

In terms of actual costs, it offers a monthly subscription model to healthcare providers, where they pay USD 200-500 per month, plus a small fee per actual test. Compare that to ABI, where a Doppler ultrasound device needs to be used and where testing costs USD 1,000-3,000 . The actual ABI test then requires a technician's time so that each test costs USD 100-150 for each test. It also requires additional training and maintenance costs compared to QuantaFlo

Ad 2

There is an ongoing debate in the medical community about the efficacy of QuantaFlo and having reviewed a number of publications on scholar.google.com the picture that emerges is that QuantaFlo is highly effective especially in the early stages of PAD-diseases, but ABI is able to capture more complex arterial blockages better. In terms of detection rates, QuantaFlow shows 85-90% efficacy for mild and moderate PAD cases. ABI in contrast delivers 90-95% accuracy for moderate to severe PAD cases.

So, overall it is not the silver bullet that will dominate the entire market anytime soon, but it appears to be a highly cost-effective way to avoid PAD issues early on, something that the healthcare sector and insurances should cherish as early prevention at a low cost would avoid significantly higher treatment costs later. I am however, no medical nor health care insurance sector expert - so this is just a general high-level assessment

Ad 3

The global market for PAD products is estimated to be around USD 5bn in 2023 and is estimated to grow by 6% p.a. As Semler makes USD 55m in Revenues, this represents less than a 2% market share, although the market size also includes drugs for PAD, which Semler is currently not involved in. In any event, Semler sits in an attractive niche and can expect to gain market share from its innovative, low-cost and highly scalable product from more expensive incumbent testing products.

In the recent Space, Eric highlighted that SMLR will soon penetrate the heart disease space with a similar proposition which would open up this much larger market for the company. For the purpose of this analysis, I have not dived into this, but it can be implicitly assumed to be included in the "bull case" scenario

Ad 4

It was very interesting to listen to Eric on this point, because previously I had assumed that a Democratic administration would favour a value-based care, preventative medical strategy and a Republican administration would favour more traditional fee for service model. However, he appears to indicate that the current regime has not been very supportive of FDA-cleared products such as QuantaFlo. This is an area that I need to understand better after the elections.

Ad 5

Semler's strategic positioning as a SaaS in the medical diagnostics sector mainly for heart disease, but also in Alzheimer’s, and in diabetes management should be highly lucrative as it provides massive operational gearing once market share is gained in its sectors.

A preventive and value-based health care sector in the US should be all over these type of services, however, interests are clearly highly entrenched, so it remains to be seen, how Semler's marketing team can penetrate the space effectively. It would be good to understand their marketing and sales approach in more detail

Ad 6

Regarding operating cashflows, I have already said quite a lot and having read analyst reports of the only issuing stock broker (Lake Street Capital Markets) it is clear that they have a superb cash generative machine, with a gross margins of 90%. If the market grows by 6% I would expect as "bear" that SMLR should at least be able to deliver 8%, however, higher revenue growth rates are quite plausible as well, which would directly feed into SMLR's nascent flywheel

Ad 7

As a starting point, each of the scenarios assumes that SMLR will be able to issue USD 70m of debt (and buy bitcoin with it) by end of Q4.

From Q1 2025 onwards, the ability to issue debt will markedly vary from scenario to scenario as higher revenue growth will translate into higher operating cashflow which in turn will allow to issue more debt at varying attractive interest rates levels.

On the last point, I will say that it is currently unlikely that SMLR will benefit from dramatically low interest rates UNTIL bank start offering options on the stock, so for now I believe that the average interest rate for convertible bonds of small listed firms (3.5-4%) is the most plausible assumption.

In the bull case, we would assume that banks see the opportunity to earn money from options trading earlier and start offering stock options. It is difficult to estimate when this would be but an indicator is clearly current trading volumes, which have picked up significantly since SMLR's announcement to buy BTC.

Ad 8

The key risks in SMLR are in my opinion:

1) Its core product loses further market share, perhaps due to a combination of changes in the regulatory regime (preventative care takes a back seat) and new entrants with more precise measurement of PAD at the same/lower cost. This is possible but at the same time they are coming up with new innovations so that I am not overly concerned that this would dent their ability to generate cash

2) Its small-ish size means that investors and banks overlook the opportunity in SMLR. Without a functioning options market, the debt build up is still possible but far less attractive for SMLR. Then it would revert to just buying BTC out of the operating cashflow directly, without being able to use leverage. This is the biggest "risk" in my mind

3) BTC price falls persistently. No further comment 😉

11 Oct 2024

Having learned from the best in our trade - especially after today’s monumental day for #MSTR - I have decided to initiate a new position, which I have nostalgically christened “Kerrisdale Plus”:

🥁Short Microstrategy / Long Semler🥁

Ok - I would never short mstr, but hear me out: When looking for an attractive vehicle that carries bitcoin, #SMLR is a massively cheaper alternative to his big brother #MSTR or the fake sushi store aka #Metaplanet.

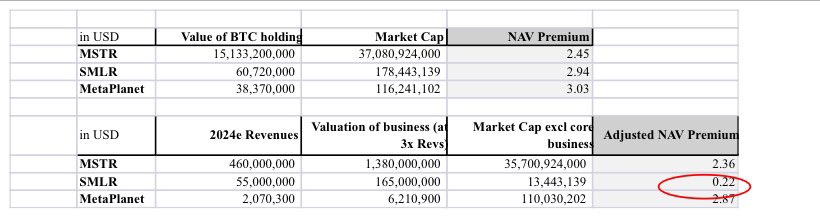

There is merit in taking a closer look at their NAV premia (calcs were done this morning prior to the explosion).

The below table first calculates the standard NAV premium by dividing market cap by the value of the #btc holdings. Here all three are fairly close to each other, with Mstr being actually the cheapest, with a 2.45x premium.

However, when taking into account that each company’s market cap is at least partially derived from its respective core business, that portion needs to be stripped out before dividing the remaining company value by its btc holdings to arrive at a comparable NAV premium across each firm.

Assuming simplistically a 3x P/S valuation across each of the three businesses and adjusting the NAV for that amount shows you that

Metaplanet and Microstrategy still trade way above 2x, whereas Semler is at a dirt cheap 0.22x (see bottom table). The reason for that is that Semler has a serious revenue and bottom line from its operations relative to its btc holdings and market cap.

On that basis, I would indeed overweight Semler out of the three.

One major issue with Semler is that it currently lacks the magic sauce, which is a functioning options market. That would enable it to write cheap convertibles and acquire btc onto its hitherto pristine balance sheet. In my view it is a matter of time until options will become available as trading volumes continue to rise.

Keen to hear other thoughts and obviously not financial advice.

Happy weekend!

14

15

93

20,528

10 Jun 2024

1st layer into #SMLR. Love the stock and nabbed it at $34.00.

Cash flow giant, and at current value it's EV is still only 218M vs MC of 285 M, so roughly 20% of the company is the cash on hand.

Following #MSTR with #BTC conversion and being immediately rewarded and the cash-hoard is now being given a multiple.

Strong (and growing) free-cash-flow with no debt (until this 150M offering) with easy ability to cover interest. I prefer this than a risky acquisition with the cash hoard.

Gross Margin of 90% w/ OPEX shrinking to nearly 16% with healthy operating margin of 33%

Stock getting beat up over reimbursement declines from CME for asymptomatic peripheral arterial disease. But they'r expanding outside of Medicare Advantage payer which I believe is wise -

And Expanding their PAD QuantaFlo medical device diagnosis possibilities beyond peripheral arterial disease with expected 501(k) acceptance in 2H 2024.

I baked in a lot of bad news with a -2% maturity, decline of net profit of 2.5% per year for next 10 years, and a discount rate of 5%, the NPV still is around 340M which gives it a value around $44.

BTC-Share only $8 at these prices but if they use the 150M for #BTC purchase, that'll improve significantly.

If they're given wider application for Quantaflow that'll unlock the company multiple on it's own, without considering the multiple on the Bitcoin treasury.

@werkman

3

2

23

7,233

6 Feb 2023

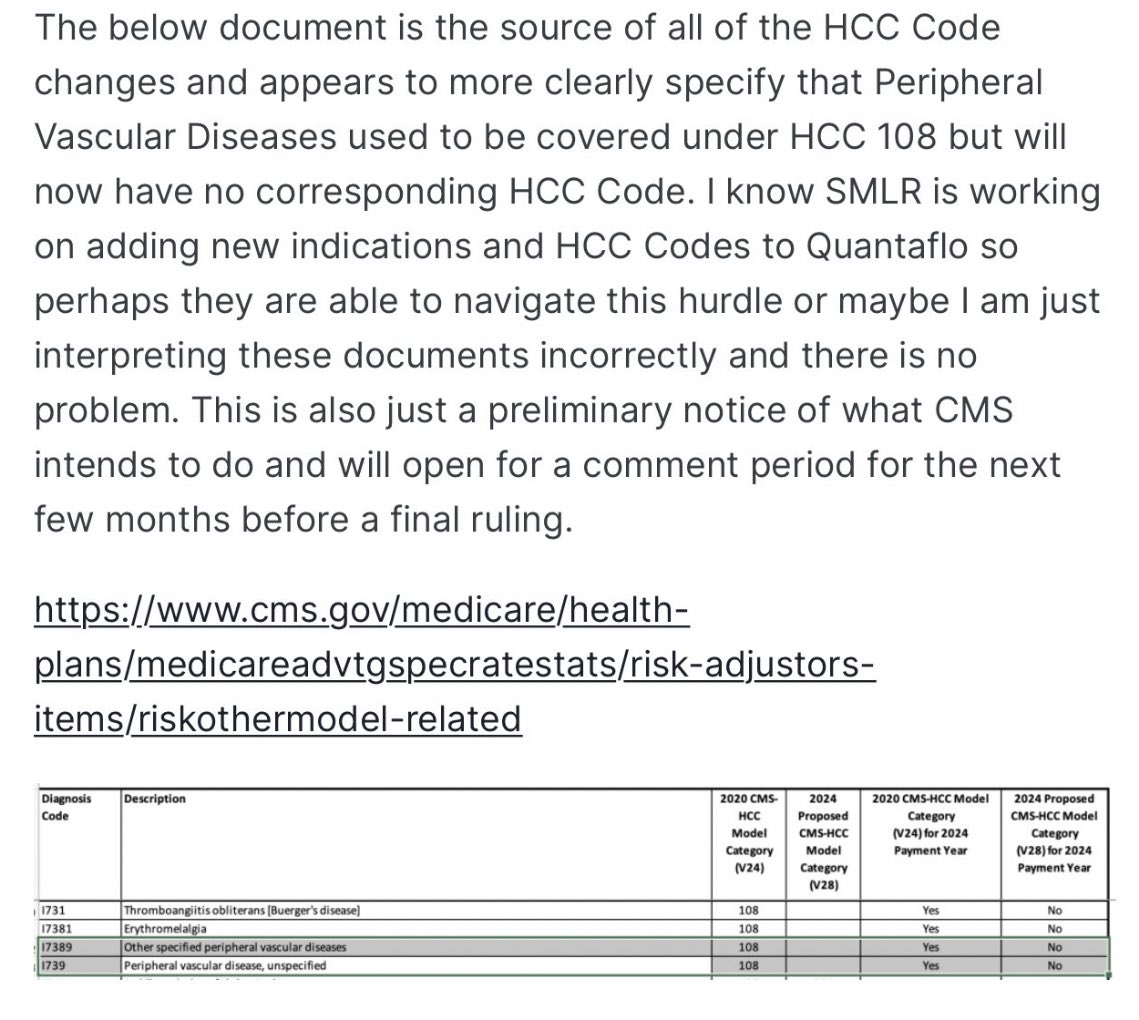

Reimbursement concerns for Quantaflow after HCC code change

No updates from $SMLR

h/t @YankyBanash

6 Feb 2023

There was a change in the new code for medical providers regarding pad. This may affect that Quonteflow may not be covered no more.

3

9

3,986

24 Jan 2023

Heureux d'être certifiés GREAT PLACE TO WORK ! #quantaflow #greatplacetowork #comptage #analysedeflux

2

60

22 Dec 2022

Toutes les équipes de Quantaflow vous souhaitent d'excellentes fêtes de fin d'année ! quantaflow.com

2

92

2 Mar 2022

I’m not the world’s foremost expert, but I know enough here to feel it’s fair to say that products claiming to diagnose AD are far more plentiful than those that have proven to reliably do so.

FWIW, I’d make sure to pay a price for $SMLR based strictly on QuantaFlow.

1

2

17 Sep 2020

"Nous sommes heureux de réaffirmer notre partenariat avec le colloque @Magdus_Outlet & impatients de pouvoir présenter les récentes informations sur la fréquentation des centres commerciaux & nos solutions de gestion de la présence en cette période de crise sanitaire."Quantaflow

ALT Guillaume NOBLET, Directeur Général Adjoint chez Quantaflow

3

3

28 Apr 2020

Quantaflow helps you be ready for re-opening after lockdown with its real-time application!

bit.ly/2yBMYE0

#shoppingcentres #RealTime #occupancy

1

3

13 Feb 2020

10th European @Magdus_Outlet Conference, March 25th in Paris: very pleased to get the precious support of @quantaflow_fr/@quantaflow ! Information and registrations on: magdus2020.com/welcome/

#outlet #shoppingcentres #DataAnalytics

2

3

7 Feb 2020

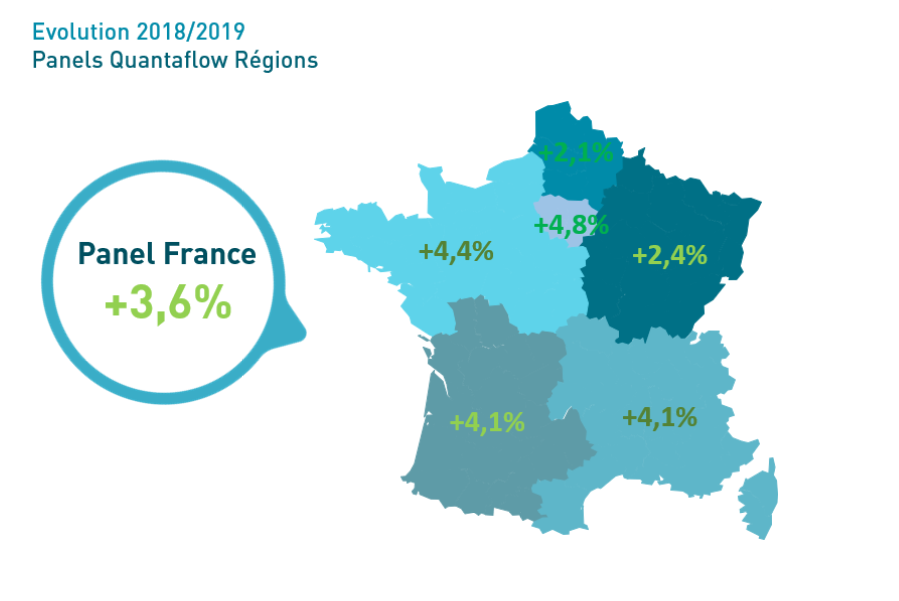

Soldes d’hiver : les centres commerciaux font fréquentation égale à l’an passé [CNCC / Quantaflow]. L'opus des 4 semaines 2020 n'est en retrait que de 0,3% par rapport à 2019. La région francilienne superforme ( 2,6%) par rapport aux autres régions (-1,2%) lsa-conso.fr/soldes-d-hiver-…

4

3

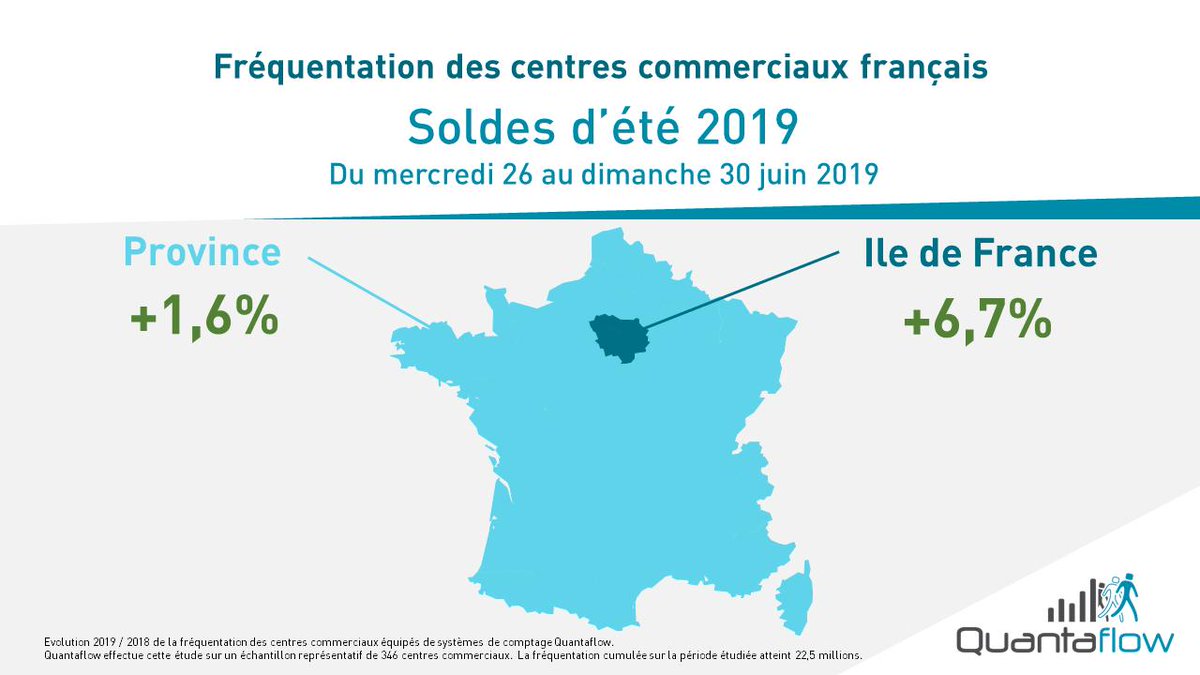

2 Jul 2019

Les soldes d'été 2019 progressent de 3,3% par rapport à 2018 mais c'est l'Ile de France qui se démarque nettement avec 6,7% #quantaflow #SoldesEte2019

1

2

3

10 Jun 2019

Eurocommercial selects Quantaflow for footfall analysis in its French and Belgian centres • Quantaflow buff.ly/2F1AAgI

2

3

5 Jun 2019

Best way to start #SIEC2019 - scrumptious food and great company @Magdus_Outlet @chrisigweintl @quantaflow @quantaflow_fr @CNCC_Officiel

2

13 May 2019

Avril 2019: les chiffres clés de la #frequentation des #centrescommerciaux • Quantaflow buff.ly/2Eh1Qrt

3

10 Apr 2019

I have arrived and am looking forward to catching up with everyone!

@ICSCEurope @Chainels @quantaflow @coniq @across_magazine @TacticsMag

#retail #property #conference #PropTech #networking

1

17 Dec 2018

Gilets jaunes : - 10% de fréquentation en centres commerciaux pour le "5e acte" (CNCC/Quantaflow). Soit le 5e week-end de contre-performance depuis le début de la crise. La perte de CA - irrécupérable - est estimée à 2 milliards d’euros. #GiletsJaunes lsa-conso.fr/gilets-jaunes-1…

2

2