Jun 13

APAR Industries - In FY21, revenue was only 6400 cr. FY26 = revenue had reached 23000 cr.

This means revenue grown = 3.5x in 5 years with a CAGR of around 29%. Q4 FY26 revenue alone was 6,603 cr which was almost equal to the entire FY21 annual revenue.

The business mix is roughly 50% Conductors, 25% Cables and 25% Transformer Oils.

APAR is considered one of the strongest conductor manufacturers globally and exports to more than 100 countries. The future of the conductor business is directly linked to India's power infrastructure expansion.

India is aggressively adding renewable energy capacity. Most solar and wind projects are located far away from major consumption centers. Power needs to be transmitted from regions such as Rajasthan, Gujarat and Ladakh to cities like Mumbai, Delhi and Bengaluru.

This requires large transmission networks. Every transmission line requires conductors.

The opportunity is not limited to new transmission lines. A large part of the existing grid also needs upgrading. Many transmission lines are undergoing reconductoring. Older conductors are being replaced with higher capacity conductors.

The company achieved a record installation of 1949 circuit km during FY26.

Managemnet saying- Mumbai is emerging as one of India's largest data center hubs. Data centers require enormous amounts of power. As transmission infrastructure expands to support this demand, APAR becomes an indirect beneficiary of the data center boom.

The company has already supplied cables to multiple U.S. data center projects. Management is targeting approximately $500 million of U.S. revenue within the next 3 years.

HVDC is another important pillar of the long term growth story. India is increasingly investing in HVDC transmission corridors. HVDC technology is critical for transporting large amounts of electricity over long distances. It is particularly important for renewable energy evacuation.

Management confirmed that several large HVDC projects have already been awarded. However, actual supplies and revenue recognition are expected to begin mainly in FY27 and FY28. As a result, a large portion of the HVDC opportunity is still not reflected in current financial numbers.

Very few listed companies have meaningful participation across Conductors, Cables, Transformer Oils, HVDC, Renewable Energy Evacuation and U.S. Data Centers simultaneously. Most competitors are focused on only one or two of these themes.

FY26 capex was 740 cr. For FY27, capex has been increased to approximately 1500 cr. Around 400 cr is being invested in Conductors. Around 200 cr is being invested in Oils. Around 850 cr is being invested in Cables.

Conductors are already operating at around 90-95% utilization. Cables are operating at around 85-90% utilization. The Oil segment is operating at around 65-70% utilization.

Current CWIP is 33% of current fixed assets.

Companies generally do not undertake such aggressive expansion unless demand visibility is strong.

Management indicated that this capex could support an additional 3000-5000 cr of annual revenue over time.

Current cable revenue is approximately 6000 cr. The long term goal is to reach around 10000 cr in cable revenue.

Public shareholding is gradually decreasing quarter by quarter.

Share price continoulsy going upwards.

These type of growing stocks are better to add when they fall 30% from highest price.

2

18

1,143

Not at all. There is some case for reconductoring, and repair or replacement of some existing pylons. Also, as the North Hyde fire revealed, replacing aged substation kit. But this is normal depreciation replacement, not multiplying the cost by 6 as planned.

19

self proclaimed grid experts with zero actual t&d experience acting like reconductoring is some novel trick Utilities Don’t Want You to Know About must have been fun for you

1

3

45

Jun 11

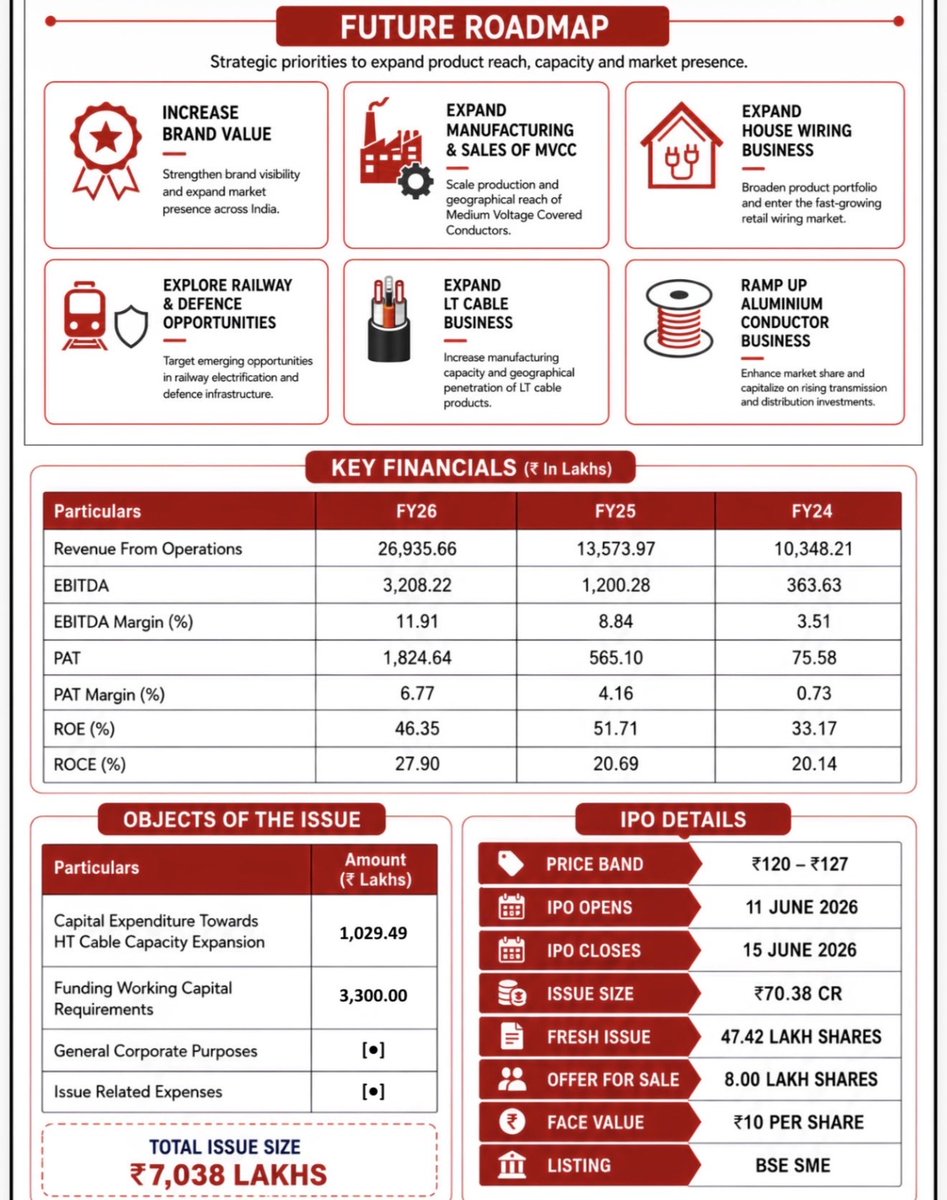

Susan Electricals : Growth Expansion Reasonable Valuation

The company sits in a segment where demand is not one-time.

Every grid upgrade, every old cable replacement, every reconductoring project and every push towards safer power distribution needs wires, cables, conductors and MVCC products.

That is the tailwind.

Now the company is using IPO proceeds to expand LT & HT cable capacity from 7,500 km to 12,000 km p.a.

A 60% capacity jump.

The financials also show a visible shift:

Revenue has moved from ₹103 cr to ₹269 cr

PAT has moved from ₹0.76 cr to ₹18.25 cr

EBITDA margin has improved from 3.51% to 11.91%

At the upper band, the IPO is valued at around 14x FY26 earnings and nearly 8x FY27E earnings as per working capital-linked estimates.

Anchor participation includes names like Motilal Oswal Finvest, SageOne, Shine Star Build-Cap and Arthasanchay.

3

4

30

4,562

Jun 11

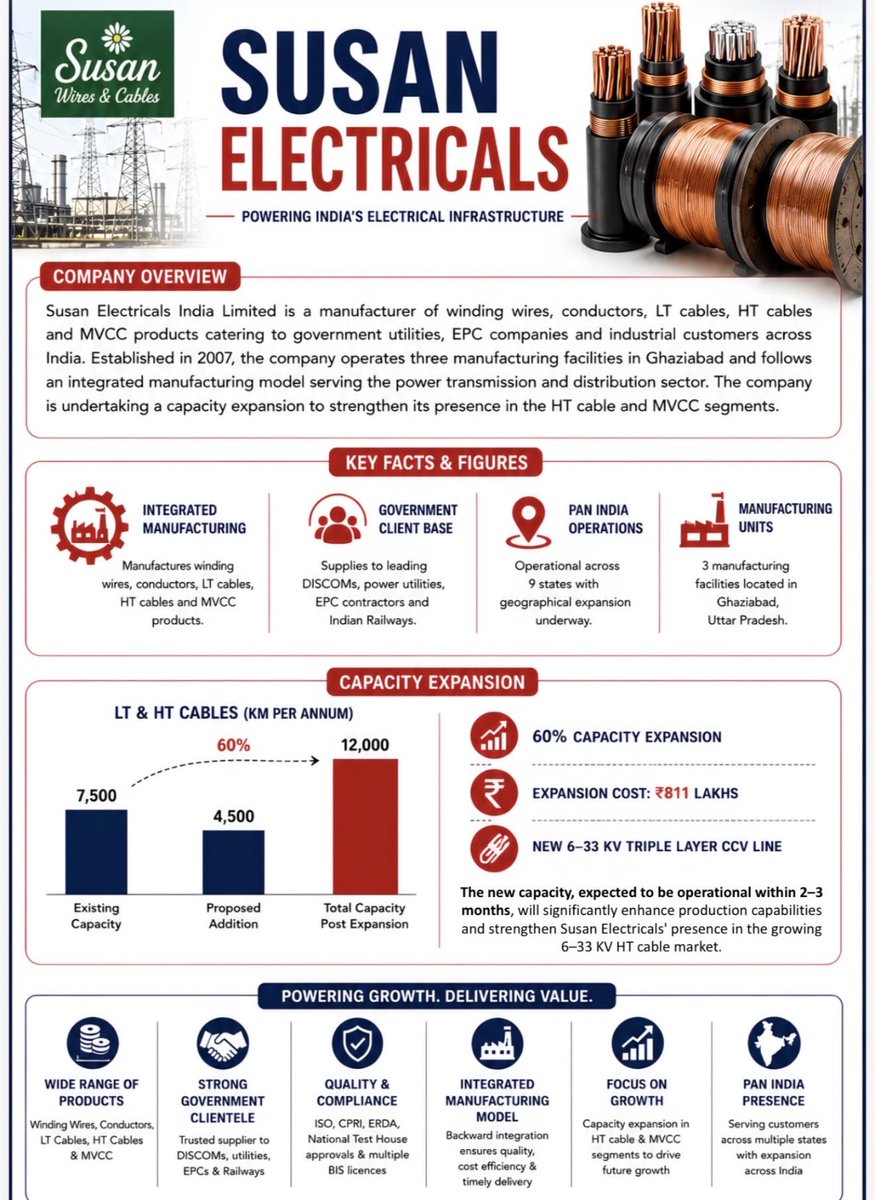

Susan Electricals IPO: Undervalued, High Growth, Good Anchors

The company manufactures winding wires, conductors, LT cables, HT cables and MVCC products for government utilities, EPC players and industrial customers.

Established in 2007, Susan Electricals operates 3 manufacturing facilities in Ghaziabad and follows an integrated manufacturing model.

Key growth trigger: Capacity expansion.

LT & HT cable capacity is planned to rise from 7,500 km p.a. to 12,000 km p.a. — a 60% jump.

The company is also adding a new 6–33 KV Triple Layer CCV Line, with an expansion cost of around ₹811 lakh.

Financially, the company has shown strong momentum:

Revenue: ₹103 cr in FY24 → ₹269 cr in FY26

EBITDA: ₹3.6 cr → ₹32.1 cr

PAT: ₹0.76 cr → ₹18.25 cr

EBITDA Margin: 3.51% → 11.91%

PAT Margin: 0.73% → 6.77%

Valuation also looks interesting.

At the upper price band, Susan Electricals is priced at roughly 14x FY26 earnings.

As per working capital data and expected FY27 numbers, it is priced at nearly 8x FY27E earnings.

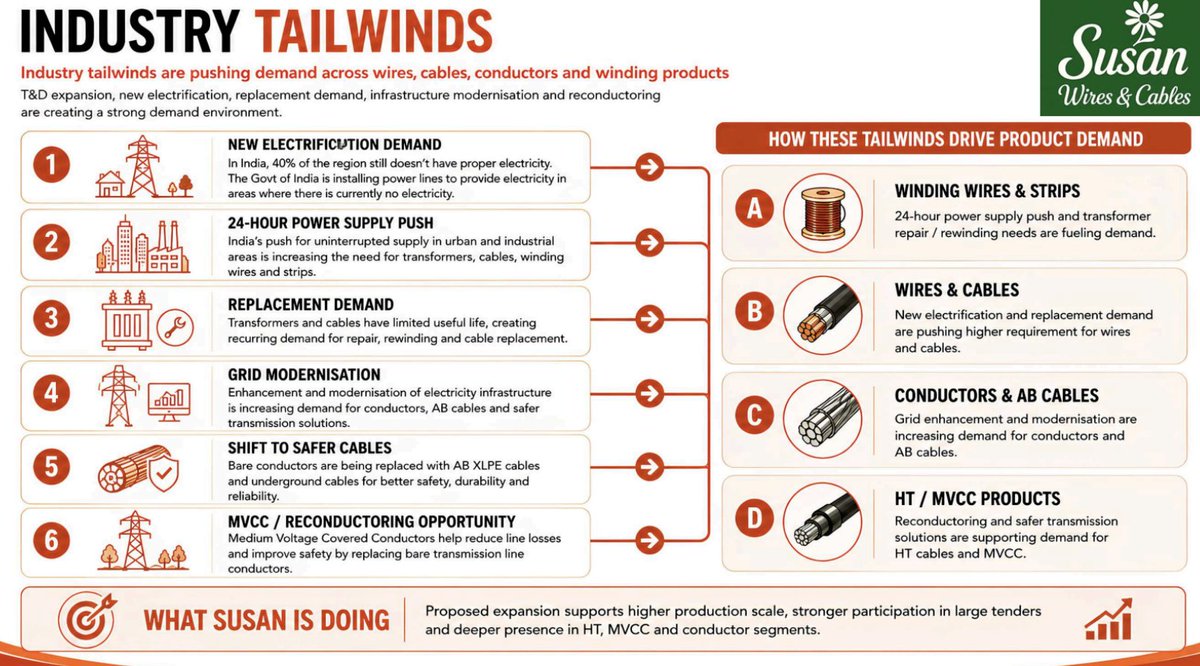

The broader tailwinds are strong:

Grid modernisation, infrastructure enhancement, replacement demand and reconductoring are creating demand for wires, cables, conductors and MVCC products.

The roadmap is also clear:

• Expand MVCC manufacturing & sales

• Enter/expand house wiring business

• Explore railway & defence opportunities

• Expand LT cable business

• Ramp up aluminium conductor business

• Build brand value

Anchor book includes names like Motilal Oswal Finvest, SageOne, Shine Star Build-Cap, Arthasanchay and others.

IPO Details:

Price Band: ₹120–₹127

Issue Size: ₹70.38 cr

Fresh Issue: 47.42 lakh shares

OFS: 8 lakh shares

Listing: BSE SME

1

2

11

4,950

A community-scale DG solar project (the size needed for a median like what you photographed) is not economically viable if it needs to pay for substation upgrades as well as miles of reconductoring and/or new distribution/subtransmission line construction.

PPAs only go so high.

1

3

37

Hi spideydoh! Upon checking, mayroong naka-schedule na power interruption sa Brgy. Holy Spirit between 11:00PM (Wed., 06/10/26) and 4:00AM (Thu., 06/11/26) due to replacement of pole and line reconductoring works along Saint Anthony and Saint Peter Streets in Brgy. Holy Spirit, Quezon City.

Let us know if you have any inquiries or Meralco concerns, magpadala lamang sa amin ng PM.

You can refer to our About section for the Meralco Privacy Statement.

1

76

Jun 10

Tailwinds

Electrification, 24-hour power supply, grid modernisation and reconductoring are driving demand.

Susan Electricals is positioning itself right in this tailwind.

1

2

170

Jun 2

3/ Core Transmission Biz Strong

Key wins Q4:

• 17 Cr ERS order from MSETCL

• First direct EPC order in Uttarakhand (~23.5 Cr)

• 27.9 Cr reconductoring EPC order from GETCO

• Largest-ever tools order bk of ~22.7 Cr

Advait moving from products to higher-value EPC execution.

1

1

2

773

May 29

11/ Final Crux :

The market still views APAR as a conductor transformer oil company.

Mgmt is building something much larger.

A company leveraged simultaneously to:

⚡ Grid Expansion

⚡ Renewables

⚡ Data Centers

⚡ HVDC

⚡ Reconductoring

⚡ CTC

⚡ US Infrastructure

Very few Indian industrials sit at the intersection of all these themes.

And that's what makes APAR one of the most interesting power infrastructure stories today.

Must study , a niche long term bet with near term hurdles 💡

4

607

Powering the future. Powering Kampala. ⚡

Our teams are making major strides reconductoring 132kV transmission lines around Kampala, a key component of the Kampala Metropolitan System Improvement Project.

Works on the 132kV Kampala North – Lugogo transmission line are nearing completion. This critical upgrade will strengthen and improve power transmission within the Greater Kampala Metropolitan Area, supporting a more reliable electricity network for homes, businesses and industries.

These moments capture the commitment, skill and resilience of the teams working on the ground every day to keep Uganda connected and powered.

#KampalaMetroProject.

4

21

45

4,626

May 28

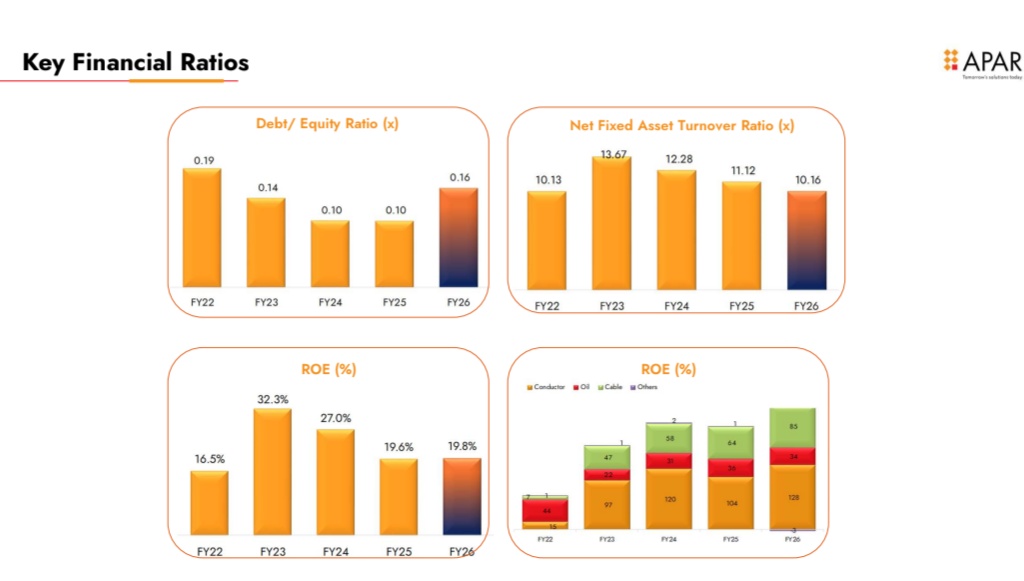

Apar Industries Ltd.📞 Q4 & FY26 Concall Summary #APARINDS

🟡 MANAGEMENT PROJECTION :

Management announced aggressive FY27 capex of 1,500 crores versus 740 crores in FY26, with ~850 crores allocated to cables, ~400 crores to conductors, and ~200 crores to oils. Conductor volume growth guidance stands at ~10% for FY27 while cables business is targeted to sustain ~25% CAGR. Medium-to-long-term conductor EBITDA guidance remains at 35,000-36,000 per tonne plus tailwinds. Cable business is targeting 10,000 crores revenue through expanded capacities in data-center cables, MV cables, solar, wind, railways, and defense. Current conductor capacity utilization already stands at 90-95% while cables operate at 85-90%, supporting the need for accelerated capex. Management also expects strong FY27-FY28 growth in the US driven by data centers, utilities, reconductoring, and renewable-energy infrastructure.

🔴 Red Alert :

Management warned of near-term slowdown due to sharply higher aluminum, copper, polymer, freight, and war-premium costs following Middle East disruptions. Specialty polymer shortages from Abu Dhabi and freight inflation are already affecting specialty cable margins and volumes. Several customers are delaying project execution and delivery schedules because of volatile metal prices and manpower shortages linked to elections. Export shipments to the Middle East were severely disrupted during March-April, especially in transformer oils and conductors. Competition is also increasing domestically as large players expand capacities, while Chinese pricing pressure continues in global markets. Additionally, conductor exports to the US now face 50% Section 232 tariffs, although management believes uncertainty reduction is a positive structural change.

🟢 Green Alert :

Apar delivered record FY26 revenue of 22,902 crores with EBITDA rising 23% to 2,067 crores and PAT increasing 19% to 977 crores. Q4 revenue grew 26.7% YoY to 6,625 crores while EBITDA reached 584 crores. The conductor division crossed the historic 10,000 crore milestone with FY26 revenue of 12,712 crores and order inflow of 11,450 crores. Conductor order book remains extremely strong at 7,671 crores. Premium conductor products contribution improved to 45.8% for FY26 and reached 49.3% during Q4. Cable division also delivered strong FY26 growth of 25.8% with revenues touching 6,220 crores while EBITDA margins crossed 10%. US cable revenues surged 46.7% during FY26 supported by data-center demand. The company also supplied cables to 3 major US data-center projects worth ~15 million dollars and continues receiving larger RFQ pipelines.

🔵 Blue Alert :

Apar is transforming from a conventional conductor and cable manufacturer into a global energy-transition and high-end electrical infrastructure platform spanning premium conductors, HVDC systems, data-center cables, specialty polymers, renewable-energy cables, transformer oils, EV infrastructure, reconductoring solutions, and ultra-high-voltage transmission infrastructure. The company is aggressively positioning itself around long-duration global themes including renewable energy, AI-driven data centers, grid modernization, EVs, and high-voltage transmission expansion in both India and the US.

🧠 Deep Insight :

The biggest structural story at Apar is its positioning at the center of global electrification and AI infrastructure expansion. The US data-center opportunity is becoming especially important because AI data centers require significantly higher cable intensity and higher-specification products versus conventional facilities. More importantly, Apar appears to be evolving from a commodity-linked manufacturer into a technology-heavy premium electrical infrastructure player where product mix increasingly drives margins rather than only metal prices. The strong premium conductor mix, growing HVDC participation, and expanding US utility relationships all support this transition. Management’s decision to sharply frontload capex despite near-term uncertainty also signals very high confidence in long-term demand visibility across transmission, renewable energy, and data-center infrastructure. If geopolitical disruptions normalize and Apar executes the current capex cycle efficiently, the company could continue compounding as one of India’s most important global electrical-infrastructure exporters over the next 5-7 years.

2

2

577

May 28

#APARINDS

Apar Industries Ltd | Earnings Call Summary (Extract) - Mar-2026 Qtr | Disc: AI generated, please verify

Management Guidance and Outlook

■ Conductor Profitability: Management reiterated its medium-to-long-term EBITDA guidance for the conductor division to be in the range of INR 35,000 to INR 36,000 per metric ton, plus any tailwinds from commodity prices. This is supported by an increasing mix of premium products, reconductoring opportunities, and a growing share of copper products.

■ Volume Growth Targets: The company is targeting a 10% YoY volume growth for the conductor business and a 25% CAGR for the cables business, which is in line with its strategic goal of making the cables division a INR 10,000 crore business.

■ US Market Growth: Despite short-term cost pressures, the company expects significant growth in the US market in FY27 for both cables and conductors, driven by improved tariff clarity and strong underlying demand from data centers and grid upgrades.

■ Overall Outlook: While acknowledging short-term volatility and cost pressures that may lead to a temporary slowdown, the management expressed a bullish long-term view. The fundamental drivers for energy infrastructure, including T&D expansion, renewable energy evacuation, data center growth, and EV infrastructure, remain robust and provide a strong growth runway for the company.

3

754

May 27

Advait Energy Transitions Ltd presented its Q4FY26 & FY26 financial results, showcasing robust growth across its business segments. 📈

𝗞𝗲𝘆 𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗛𝗶𝗴𝗵𝗹𝗶𝗴𝗵𝘁𝘀 (𝗖𝗼𝗻𝘀𝗼𝗹𝗶𝗱𝗮𝘁𝗲𝗱):

- 𝗙𝗬26 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: ₹715 Cr, an 80% YoY increase.

- 𝗙𝗬26 𝗘𝗕𝗜𝗧𝗗𝗔: ₹84 Cr, up 64% YoY.

- 𝗙𝗬26 𝗘𝗕𝗜𝗧𝗗𝗔 𝗠𝗮𝗿𝗴𝗶𝗻: 11.7% (compared to 12.9% in FY25).

- 𝗙𝗬26 𝗣𝗔𝗧: ₹58 Cr, a 75% YoY increase.

- 𝗤4𝗙𝗬26 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: ₹228.20 Cr, up 18% YoY.

- 𝗤4𝗙𝗬26 𝗘𝗕𝗜𝗧𝗗𝗔: ₹28.78 Cr, up 49% YoY.

- 𝗤4𝗙𝗬26 𝗣𝗔𝗧: ₹19.96 Cr, up 55% YoY.

𝗢𝗿𝗱𝗲𝗿 𝗕𝗼𝗼𝗸 & 𝗚𝗿𝗼𝘄𝘁𝗵:

- The company's order book crossed ₹1,304 Cr as of March 31, 2026, marking a significant milestone. 🌟

- Order book grew by an impressive 159% YoY.

- Power Transmission Solutions (PTS) segment contributes 64% of the order book.

- New & Renewable Energy (NRE) segment accounts for 36% of the order book.

- The order book has seen a 107% CAGR over the last four years.

𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰 𝗜𝗻𝗶𝘁𝗶𝗮𝘁𝗶𝘃𝗲𝘀 & 𝗘𝘅𝗽𝗮𝗻𝘀𝗶𝗼𝗻:

- 𝗣𝗧𝗦 𝗕𝘂𝘀𝗶𝗻𝗲𝘀𝘀: Plans to strengthen by expanding installed capacity via greenfield projects, expected to be operational by Q4FY27. New niche products are also being introduced.

- 𝗡𝗥𝗘 𝗦𝗲𝗴𝗺𝗲𝗻𝘁: Advait has entered the Battery Energy Storage System (BESS) manufacturing space. 🔋

- 𝗣𝗮𝗿𝘁𝗻𝗲𝗿𝘀𝗵𝗶𝗽𝘀: Collaborating with global technology leaders for indigenous electrolysers & fuel cells using proven technologies.

▸ MoU with Power to Hydrogen, Inc. for AEM electrolyser-based green hydrogen projects.

▸ MoU with VJ Industries for hydrogen storage systems.

▸ MoU with CENMAT for PEM & AEM electrolyser technologies.

𝗞𝗲𝘆 𝗗𝗲𝘃𝗲𝗹𝗼𝗽𝗺𝗲𝗻𝘁𝘀 𝗶𝗻 𝗤4𝗙𝗬26:

- Successfully secured supply of ERS order worth ~₹17 Cr from MSETCL.

- Received first direct EPC order in Uttarakhand for Reconductoring worth ~₹23.5 Cr from PTCUL.

- Secured EPC order worth ~₹27.9 Cr from GETCO for Reconductoring.

- Largest order book in tools business during Q4: Approx ₹22.7 Cr from various EPC Clients.

- Received NABL lab approval at the Kadi manufacturing facility.

- OPGW Product supplies approval received from 3 new State Utilities Boards.

𝗡𝗲𝘄 𝗠𝗮𝗻𝘂𝗳𝗮𝗰𝘁𝘂𝗿𝗶𝗻𝗴 𝗙𝗮𝗰𝗶𝗹𝗶𝘁𝘆:

- A new multi-integrated manufacturing facility at Gangad, Gujarat, is under development for new product lines & capacity expansion, expected to be fully operational by Q4FY27. 🏭

𝗠𝗮𝗿𝗸𝗲𝘁 𝗢𝘂𝘁𝗹𝗼𝗼𝗸:

The company notes significant investment opportunities exceeding ₹50 lakh Cr in the power & energy sector through 2032, aligning with its vision to contribute to India becoming the 3rd largest economy.

𝗢𝘁𝗵𝗲𝗿 𝗨𝗽𝗱𝗮𝘁𝗲𝘀:

- The company migrated & got listed on the NSE stock exchange, enhancing share liquidity.

- Market capitalization stood at ₹1,825 Cr as of March 31, 2026. 📊

📊 ADVAIT ENERGY TRANSITIONS LTD | 🏷️ Investor Presentation

🌐 Details: wegro.app/yxNEug

⚡️Instant stock alerts on WhatsApp - Try FREE 👉 wegro.app/go

2

231

May 19

$DUKR May 20th close for submission

Department of Energy (DOE) rebranded the third round of its Grid Resilience and Innovation Partnerships (GRIP) program as SPARK (Speed to Power through Accelerated Reconductoring and other Key Advanced Transmission Technology Upgrades). Applications are due May 20th Duke Robotics just rushed their NASDAQ uplisting - they need the public profile and capital to meet cost-sharing requirements for these federal grants

May 15

$dukr good timing in Grid Resilience⚡️

Department of Energy (DOE) rebranded the third round of its Grid Resilience and Innovation Partnerships (GRIP) program as SPARK (Speed to Power through Accelerated Reconductoring and other Key Advanced Transmission Technology Upgrades).

Applications are due May 20th

Duke Robotics just rushed their NASDAQ uplisting - they need the public profile and capital to meet cost-sharing requirements for these federal grants

1

3

1,866

May 15

Because you want to hasten global warming?

It takes years to develop fossil fuel infrastructure.

EVs are already cheaper to make than combustion vehicles in other countries.

100% of new vehicle sales should be EVs.

The time and money spent on fossil fuel infrastructure should be spent installing 220V outlets in renter parking spots and reconductoring the grid.

electrek.co/2026/04/18/in-th…

2

2

303

May 5

Advanced reconductoring is technically building new wires tbf

1

1

8

538

May 5

Our reporter @ceboudreau has a scoop today: The White House has been sitting on an EO since last fall that would push FERC to require grid operators and utilities to identify where advanced transmission technologies like dynamic line rating and advanced reconductoring could be deployed instead of building new wires.

3

18

56

6,986

UETCL is carrying out essential maintenance works, including reconductoring of transmission lines, as part of efforts to improve power reliability across the greater Kampala area. ⚡️

If you are within the affected locations, please take note of the safety dos and don’ts shared and cooperate with our teams on the ground. #TransmittingForTransformation

4

6

20

1,587