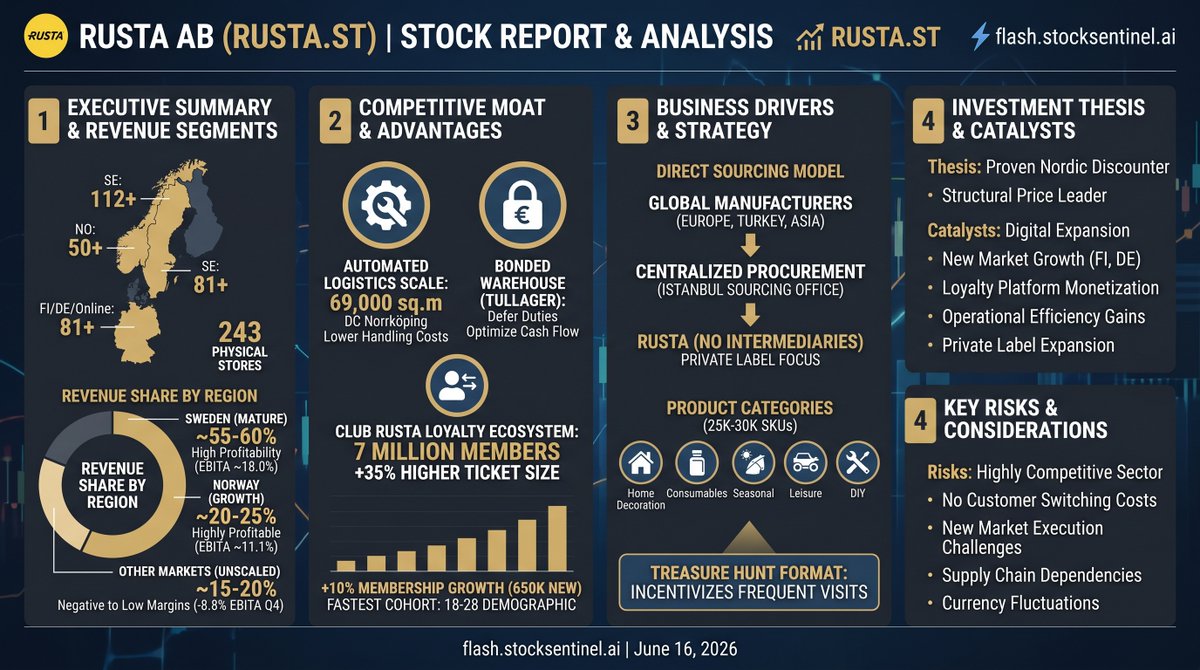

Rusta AB (publ) $RUSTA.ST is a dominant Scandinavian variety discount retailer leveraging a highly efficient direct-sourcing model and a growing network of 243 stores to maintain structural price leadership. The business is aggressively targeting continental expansion with a strategic pipeline of up to 80 new store openings planned over the next three years. Although a recent earnings miss caused a sharp share price decline, the stock continues to command a premium valuation multiple compared to its regional competitors. This premium pricing hinges on market expectations that recent supply chain investments, including a newly authorized bonded warehouse, will drive significant long-term margin expansion. Will the incoming leadership team be able to successfully scale the unproven German operations and justify this optimistic market valuation?

12

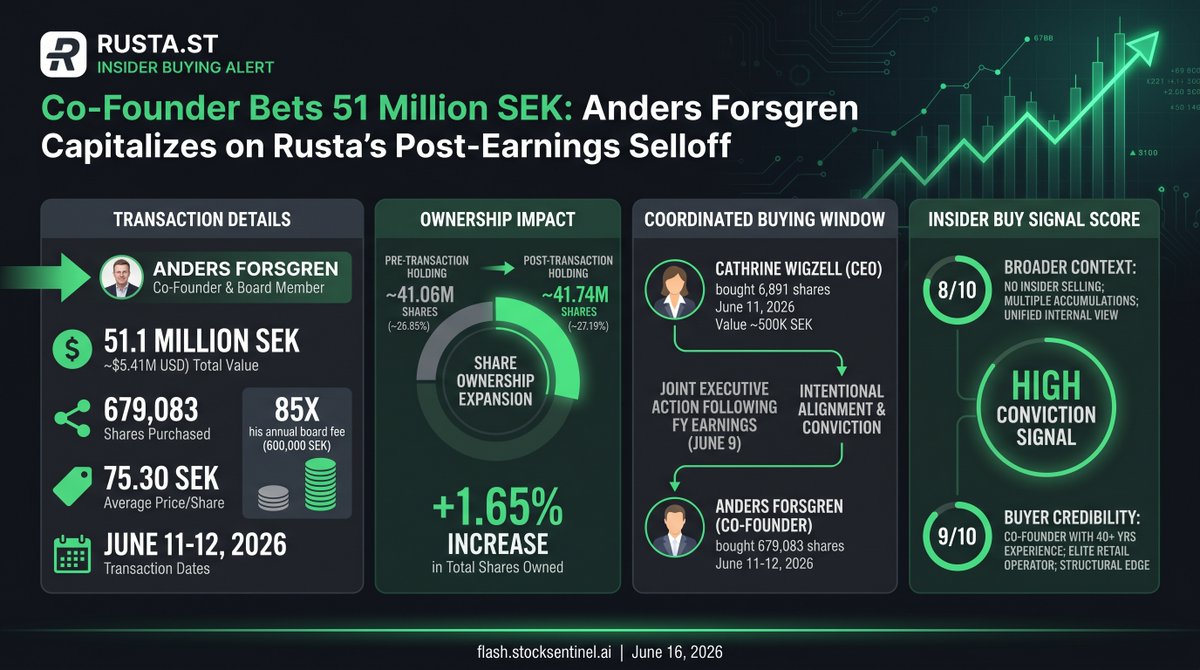

Rusta AB $RUSTA.ST co-founder and board member Anders Forsgren recently executed a massive open-market purchase, acquiring 679,083 shares for a staggering 51.1 million SEK. This multimillion-dollar investment was strategically timed immediately following a sharp drop in the share price triggered by a recent post-earnings selloff. Deploying such a substantial amount of out-of-pocket capital underscores an elite level of conviction in the long-term profitability of the vertically integrated business model he helped create. Combined with concurrent buying from the newly appointed CEO, this coordinated executive action strongly suggests that leadership views the current market distress as an unjustified discount on the true operational value of the retailer.

14

A meaningful $5.4M co-founder buy just hit $RUSTA. That does not guarantee upside, but the post-earnings timing usually means something deserves a closer look. 📈 Full research is free at flash.stocksentinel.ai

auth.flash.stocksentinel.ai/…

14

Det kostar att städa upp efter vänsterns lekstuga, inte minst att rusta upp försvaret som framförallt Göran Persson avvecklade.

1

32

DURU retweeted

Hakem Emanuela Rusta, güzelliğiyle dikkat çekmeye devam ediyor.

1

23

139

16,828

Tyskland idag och Tyskland i dåtid är två olika länder. Jag har faktiskt ganska gott förtroende för det moderna Tyskland att rusta sig till tänderna. Ska vi ha ett fritt Europa tror jag det är en nödvändighet att Tyskarna hittar hem till sitt urtillstånd som är kriget.

1

8

bi tane rus kadin arkadasimi zorla yerinden kaldirmaya calisti baska rusta ustumuze yurudu harbi korkunclar

1

2

65

Jag önskar sången - FloorFyllo - med superstar pop gruppen 🩷 @ateens_ 🩵 på @sverigesradio @TV4 @svt @tv2kosmopol kl 20:00 19 juni och 18 januari kl 19:03 tack. I Love Them All. Bild på min spis fläkt glas saker köpta på Rusta ca 8 år sedan SEK 10:- styck superrea efter Jul 🎄

11