14 Dec 2025

Define how an LLP is a separate legal entity

If you would like more information, please visit the page.

helloauditor.com/define-how-…

#llp #limitedliabilitypartnership #legalentity #businessstructure #entrepreneurship #businesslaw #liabilityprotection #separateentity

ALT #LLP #LimitedLiabilityPartnership #LegalEntity #BusinessStructure #Entrepreneurship #BusinessLaw #LiabilityProtection #SeparateEntity #BusinessFormation #LegalFramework #Partnerships #CorporateLaw #SmallBusiness #BusinessAdvice #Startups #LegalDefinitions #BusinessOwnership #FinancialProtection #TaxBenefits #BusinessCompliance 📢 𝐏𝐥𝐞𝐚𝐬𝐞 𝐅𝐨𝐥𝐥𝐨𝐰 & 𝐒𝐡𝐚𝐫𝐞 -𝐇𝐀 𝐓𝐨𝐮𝐫 𝐨𝐧 𝐒𝐨𝐜𝐢𝐚𝐥 𝐌𝐞𝐝𝐢𝐚 𝐏𝐚𝐠𝐞𝐬: 📞 𝗖𝗮𝗹𝗹 𝗖𝗲𝗻𝘁𝗿𝗲 : 99 62 39 39 39 🌐 𝗪𝗲𝗯𝘀𝗶𝘁𝗲 : helloauditor.com ✉️ 𝗘𝗺𝗮𝗶𝗹 : hello@helloauditor.com 👍 𝗙𝗮𝗰𝗲𝗯𝗼𝗼𝗸 : facebook.com/helloauditor 📸 𝗜𝗻𝘀𝘁𝗮 : instagram.com/helloauditors 💼 𝗟𝗶𝗻𝗸𝗲𝗱𝗜𝗻 : linkedin.com/in/helloauditor 🐦 𝗧𝘄𝗶𝘁𝘁𝗲𝗿 : x.com/helloauditor 💬 𝗪𝗵𝗮𝘁𝘀𝗔𝗽𝗽 : wa.me/9962393939 📢𝗪𝗔 𝗖𝗵𝗮𝗻𝗻𝗲𝗹 : wa.me/channel/0029Vb5szFSJJhzeVBsQro0c

10

24

29 Jan 2025

#ITCHotels share price live updates: ITC Hotels spins off as #separateentity

#SharePrice #Industry #Finance #MarketUpdates

641

9 Apr 2024

Peter Lawwell was at celtic in the early 90's and was part of the cover up. Peter Lawwel is still at Celtic today and came up with the term #SeparateEntity

He was still trying to cover it up.

9 Apr 2024

Solicitors say “significant progress” has been made as Celtic look to settle legal claims relating to historical abuse at its feeder club

Sky Sports News understands more than 20 former players of Celtic Boys Club are seeking damages, amounting to millions of pounds

2

3

505

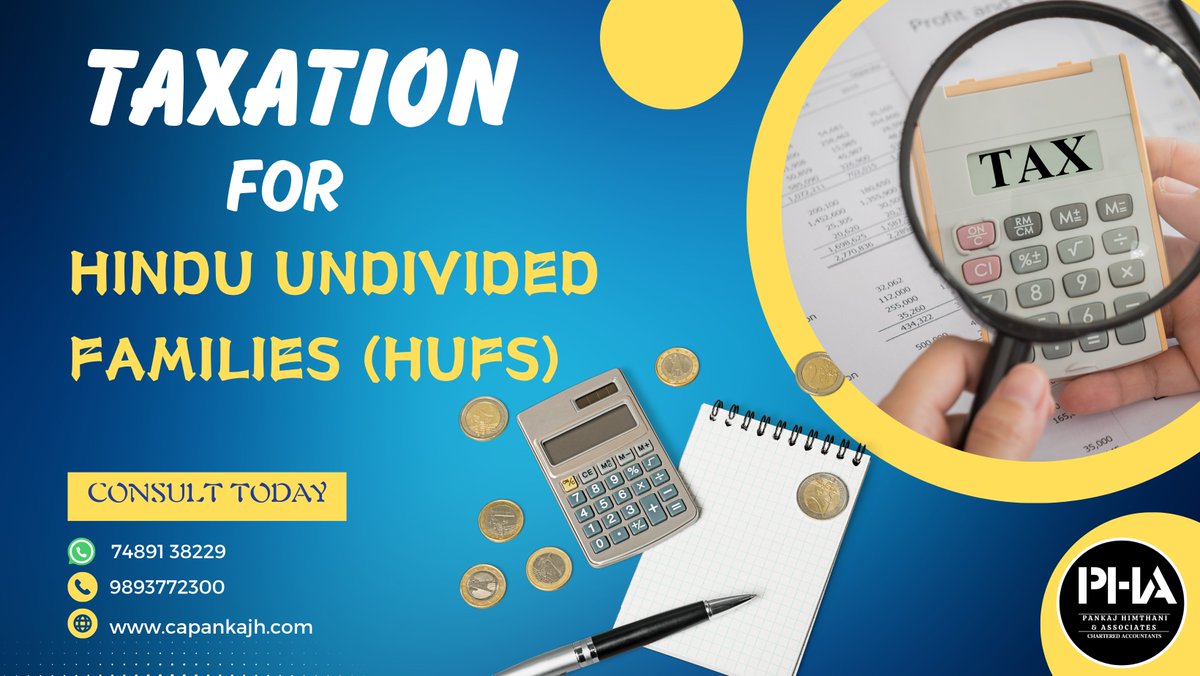

1 Mar 2024

HUF being an independent legal entity is treated separately from its members and has its separate PAN card, creating a separate stream of income.

A Trader can trade in both the account for saving the taxes.

Taxation for HUF

-HUFs are subject to income tax based on the applicable slab rates.

-Basic Exemptions of Rs. 2.5 lacs is available for HUF

-Rebate under Section 87A is not available in case of HUF

-Deductions u/s 80C, 80D, 80DD, 80DDB, and 80TTA can be enjoyed by the HUF.

FAQs:

1. Can a single person form an HUF?

No, HUF formation requires at least two members, including the Karta.

2. Can a daughter be the Karta of an HUF?

Yes, as per recent amendments, a daughter can be the Karta if she is the eldest coparcener.

3. Can HUF income be taxed in the hands of an individual member?

No, HUF income is taxed separately, and individual members cannot be taxed for HUF income.

4. Can an HUF be dissolved?

Yes, HUF can be dissolved with the consent of all its members through a formal deed.

#HUF #Separateentity @Mitesh_Engr @paresh9000

3

558

2 May 2022

Talking about lies your club has hid a big lie for 40 year @separateentity

3

4 Apr 2022

#ElonMusk should acquire @RobinhoodApp.

Then people may feel better about securing their #Doge with #Robinhood's #CryptoWallets.

By doing so, not only would #Elon be able to direct and oversee to #DogeCoin security... he will also have a #SeparateEntity designed to do just that.

1

1

3 Mar 2022

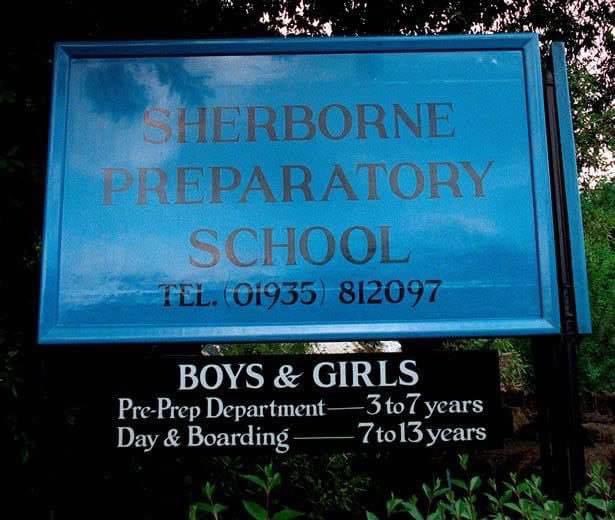

Oh 👀 For £95 you can buy a blazer with the very SAME RED GRIFFIN that was Lindsay’s #Predator 🐉 logo #SherbornePrep

#SharedHeritage

NOT #SeparateEntity

In April 1998 it was Lindsay who set SP up with charitable status

From Sept 1998 it was just SP minus RL. Nothing was NEW 💰

5

5

1 Mar 2022

3

30 Oct 2021

Actually thought they were doing the decent thing and calling out the abuse and coverup ..#oneclub #separateentity

1

3

30 Oct 2021

❤️ that you KEEP raising SE👍

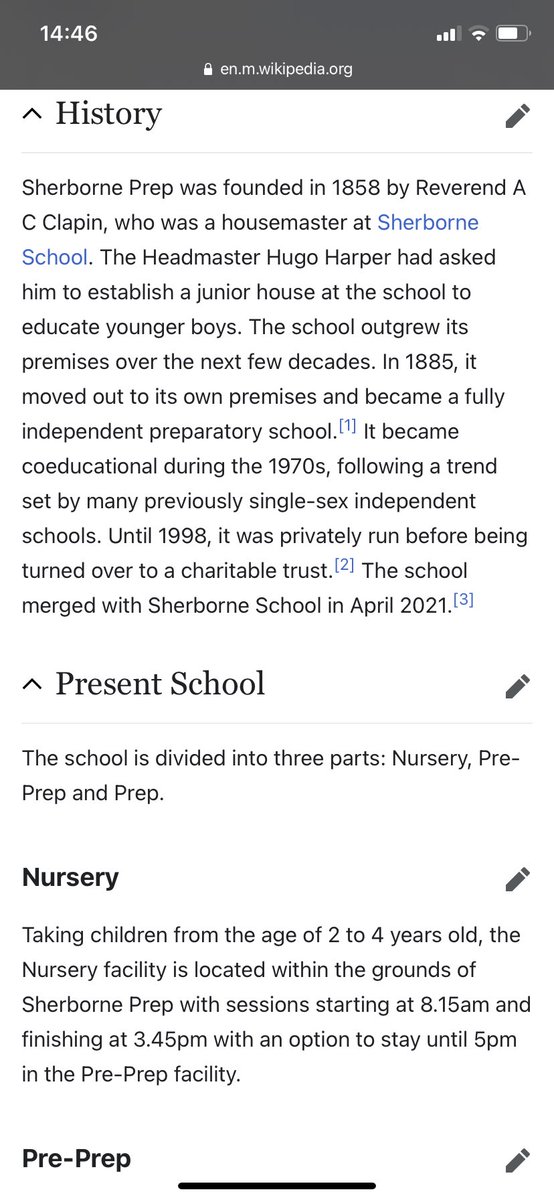

#SherborneSchools, like so very many elite boarding schools, claim #SeparateEntity to try to desperately distance themselves from CSA

Quite ridiculous

When you look at Wikipedia SS established #SherbornePrep THEMSELVES in 1858

en.wikipedia.org/wiki/Sherbo…

2

18 Oct 2021

BRAVO 👏 Gordon Woods speaks about the APPALLING insult to CSA survivors that is #SeparateEntity

Blown apart by #SharedHeritage

1858

@DinoNocivelli @law_remedy @Richard_Scorer @ScottishCAI

Boarding School Survivors are looking for similar Class Action

en.wikipedia.org/wiki/Sherbo…

My interview this morning with @SoniaPoulton from 1:02 onwards.

brandnewtube.com/watch/IBfSt…

1

2

16 Oct 2021

#SeparateEntity blown apart 💥

Ditto #SherborneShame

#SharedHeritage goes right back to 1858. You’ll see this with many Prep (feeder schools, called Preparatory in full) schools connected to top Public Schools in U.K.

Your exposure and fight really help!

en.wikipedia.org/wiki/Sherbo…

16 Oct 2021

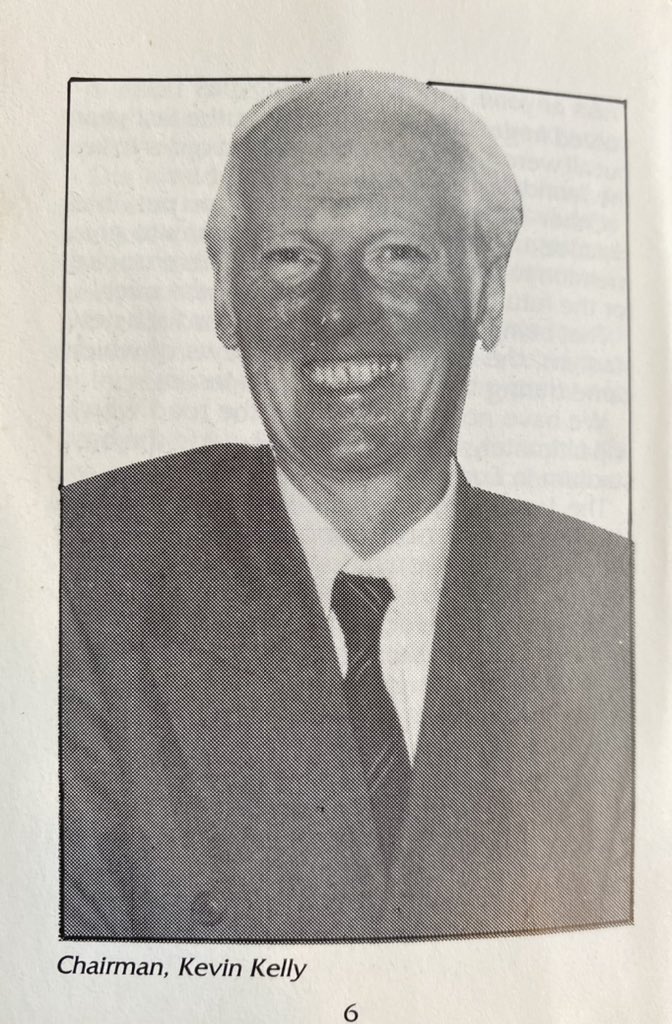

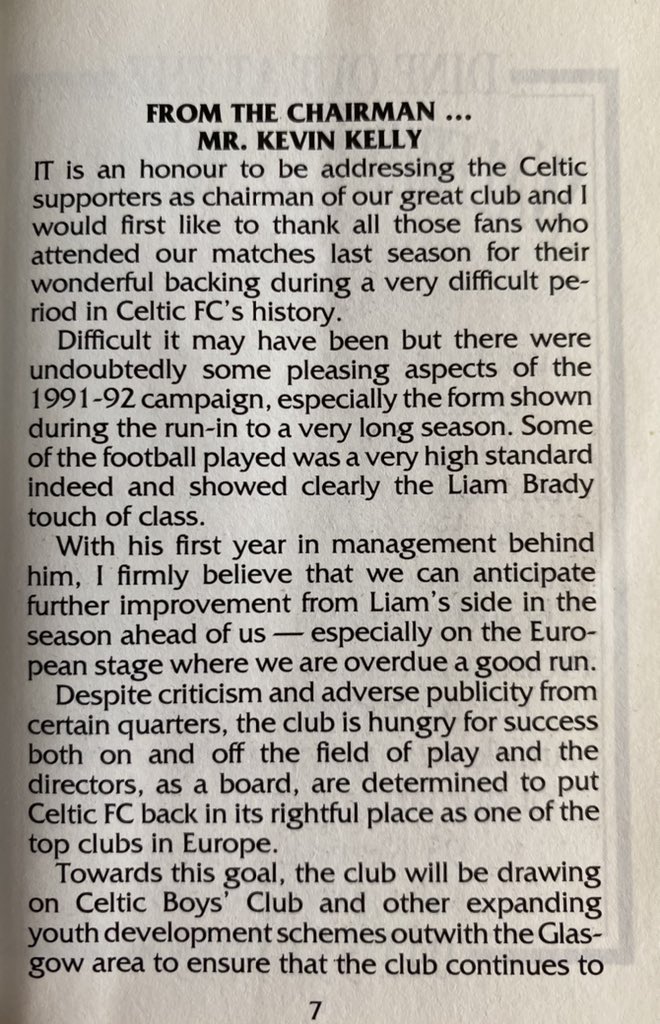

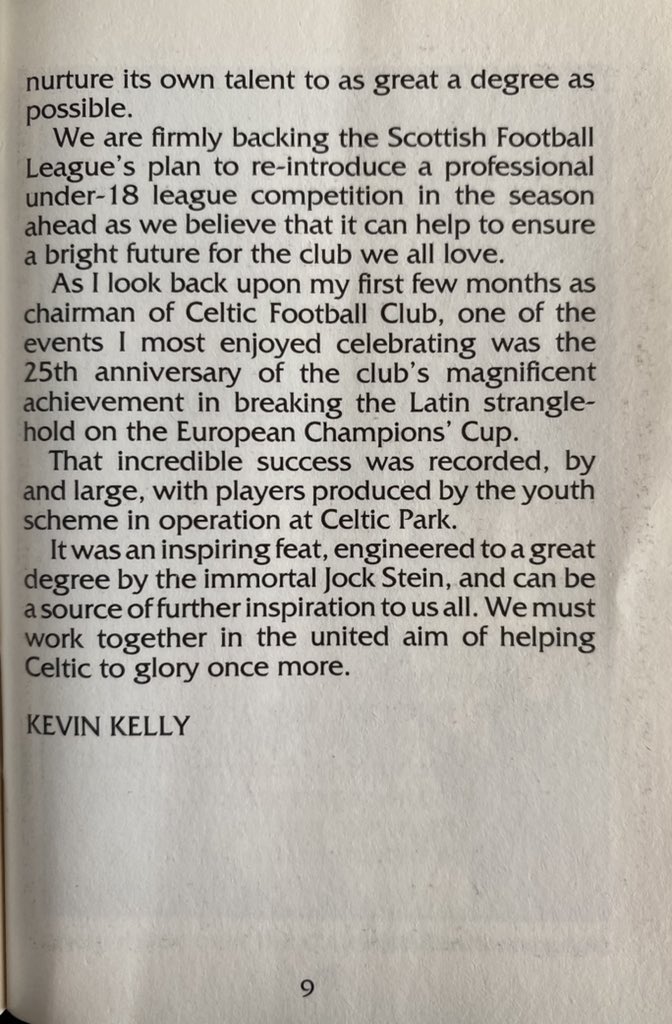

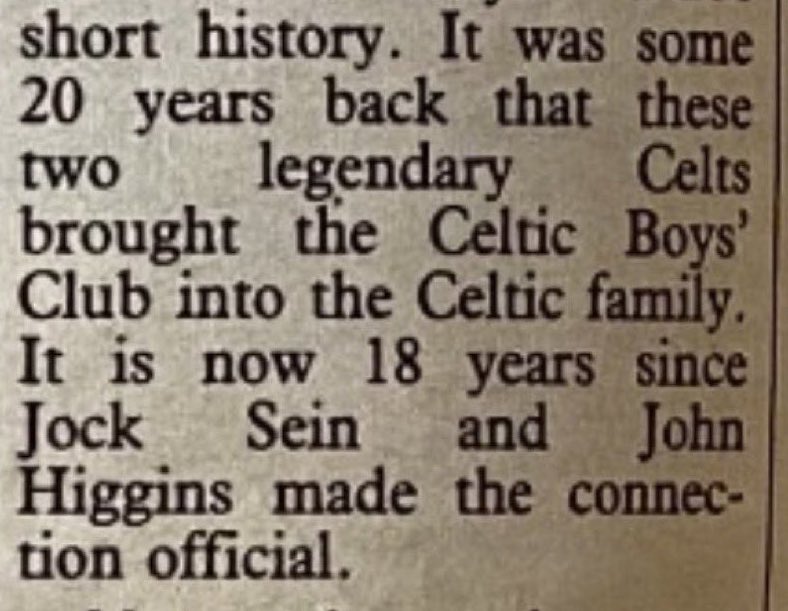

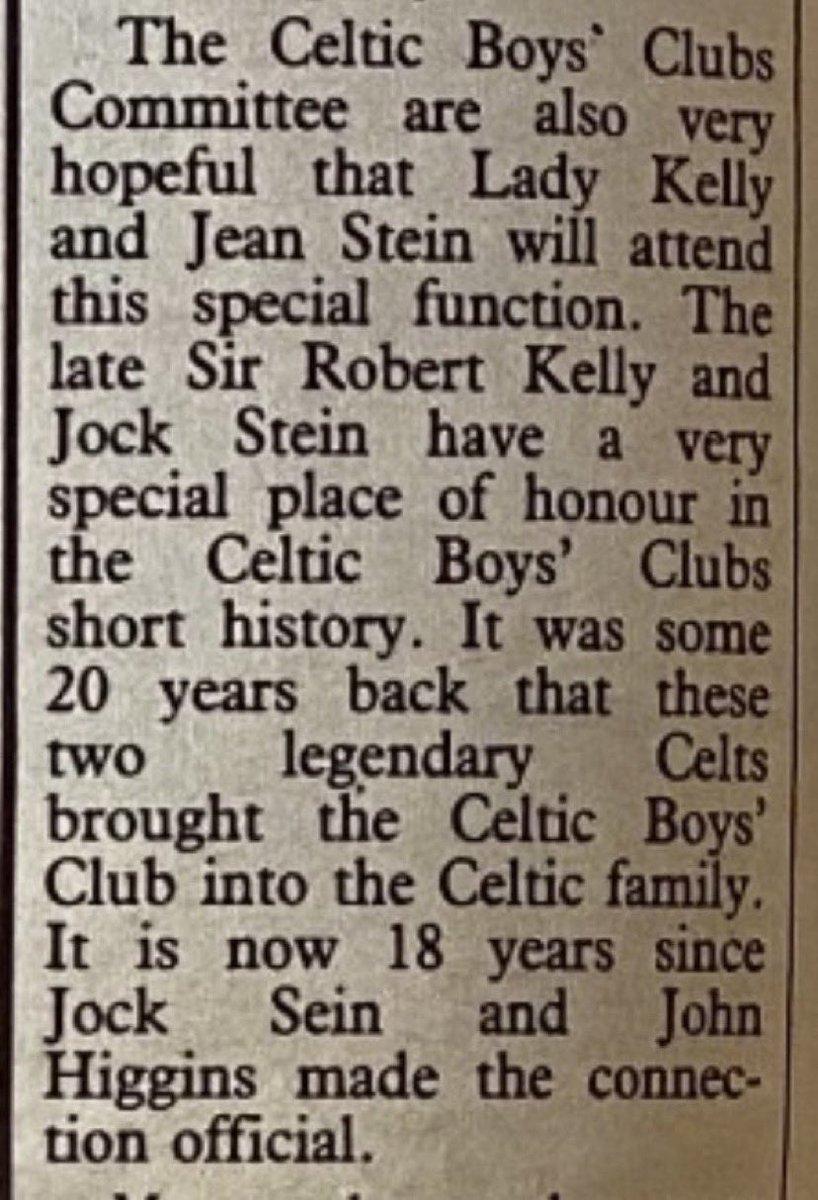

Celtic Football Club chairman Kevin Kelly tells you very clearly here that Celtic Boys Club was part of the Celtic youth system.

Kelly paved the way for Paedophiles to walk freely within the Celtic structure.

1

3

2

15 Oct 2021

#SeparateEntity Blown Apart 💥

15 Oct 2021

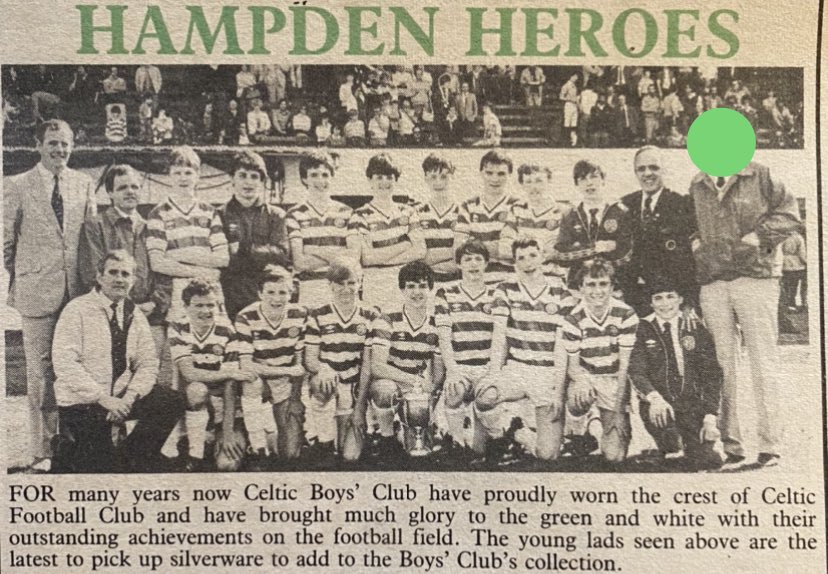

This front page clip of a Celtic view shows Celtic Boys Club at Celtic park.

Read the text - That doesn’t sound like a separate entity does it?

2

12 Oct 2021

Absolute 💩

#SeparateEntity is a legal device, a smokescreen to desperately distance institutions from CSA. It’s totally abhorrent and an insult to CSA Survivors, so transparent is it as a legal ploy.

Considering we were #AlumniToo or in Celtic’s case #FCToo

#SharedHeritage

12 Oct 2021

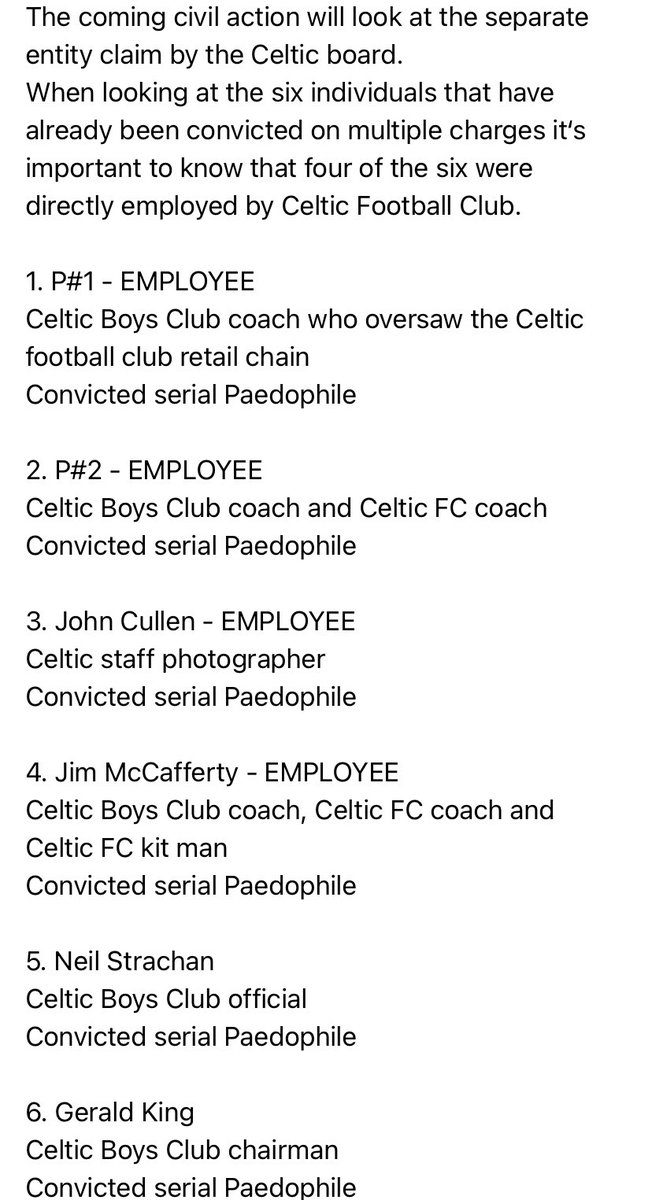

Should the separate entity stance matter given that most of the paedophiles were directly employed by Celtic football club.

1

1

3

7 Oct 2021

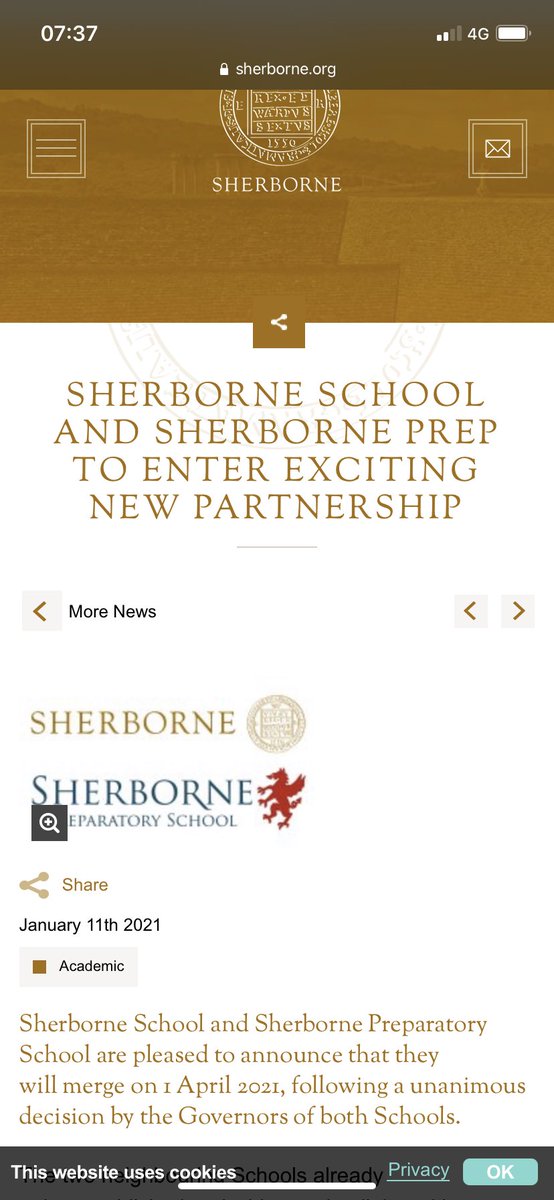

#SherborneSchool & #SherbornePrep always talk about the #Sherborne FAMILY of Schools here actually MERGING this year.

Check out the language!

#SeparateEntity Blown Apart 💥

#SharedHeritage

Not so separate now! @DinoNocivelli @Richard_Scorer @law_remedy

sherborne.org/news/2021-01-1…

6 Oct 2021

This official Celtic football club publication says that Celtic Boys Club being taken into the Celtic family was made OFFICIAL in 1970.

1

2

2

12 Sep 2021

This👇👇👇

VERY #SherborneShame @DinoNocivelli @Richard_Scorer @law_remedy @GordonW09225415

‘College chiefs said that due to a change of ownership in 1996,…

They said the allegations relate to a period of time “prior to the current college structure”

#SeparateEntity legal 💩

12 Sep 2021

patmills.wordpress.com/2021/… My latest blog commenting on the latest newspaper account about the De La Salles and my old school St Joseph's College, Ipswich.

2