A monitored wallet is a research lead, not a magic button.

Before copying, ask:

✅ What is the current exposure?

✅ How concentrated is the trade?

✅ Does the wallet cut losers?

✅ Can your sizing survive the drawdown?

Copy signal. Keep control. NFA.

This is exactly when portfolio design matters more than predictions. BOJ, Fed, energy prices, carry trades — any of these can shake markets short term. But the real danger is being overextended when volatility hits. Cash, diversification and position sizing decide whether you panic or get options.

2

One thing worth remembering:

Leverage can increase opportunities, but it also increases risk. Responsible position sizing and risk management remain essential.

#leverup #dokdopioneer

3

Am I the only one that still loves a good mall shopping day?! 👀

Comment "SHOP" to have the links (and sizing details) to shop all the items featured sent directly to you!

Everything was low-key giving on this shopping trip! is always a staple for ...

3

Yes, even if the growth is largely/already priced in (or even stretched), it can still stay on the list.

My selection is driven purely by business momentum, management commentary, order books, sectoral tailwinds, and execution capability from the latest concalls — not by whether the stock looks “cheap” on P/E, EV/EBITDA, or other multiples today.

Valuations reflect market expectations, but markets can remain irrational longer than we expect, especially in high-quality compounders or thematic plays. If the actual growth trajectory exceeds what’s currently baked in (higher order wins, margin expansion, market share gains, etc.), the stock can still deliver strong returns from here.

That said: I monitor for signs where expectations have become unrealistically high (e.g., flawless execution assumed forever with zero margin of safety).

For portfolio allocation, I personally layer in position sizing and entry discipline — the list itself is an opportunity watchlist for deeper study, not a “buy now” signal.

Growth at a premium is fine if the growth materialises and sustains.

The real risk is when growth disappoints, not the high starting valuation itself.

Example : Today if u see my thread on Cupid Vs Anondita valuations, Anondita is attractive compared to Cupid, but for right reasons.

So Cupid is part of the list and not Anondita, now going forward if the growth rate of Anondita betters than that of Cupid with improved visibility I will have no hesitation to remove Cupid and put Anondita in the list.

Hope this helps.

1

7

✨ SALE ✨ RAMA SALON - NIKKIE HAIR now on HAPPY WEEKEND SALE!

📌 maps.secondlife.com/secondli…

Naturals, Colorful & Chromatic HUDs (300 colors)

Styler HUD w/ animations, tint picker, 5 materials, glow, full bright

New sizing: 4 head 4 body

#RamaSalon #SL #Secondlife

10

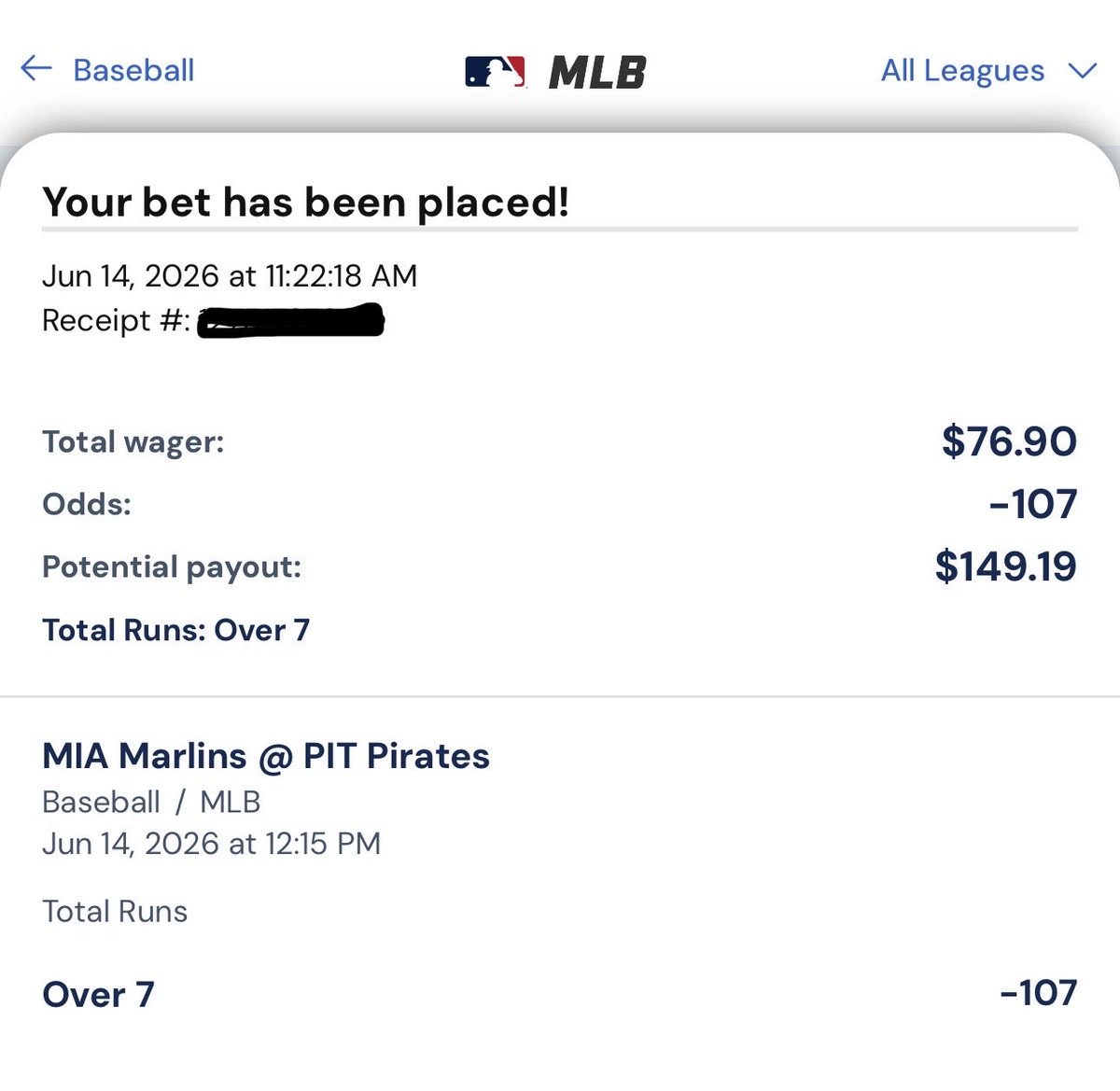

Free Play Update ❌

Today’s MLB Over 7 (Marlins @ Pirates) didn’t cash. 6 runs scored 👎🏽

That’s betting — not every EV spot hits, even when you’re on it personally.

Variance is real, especially on totals. The process (line shopping, volume, Kelly sizing) is what matters long-term.

🚨 MLB FREE PLAY - Marlins @ Pirates ⚾

Over 7 Total Runs (-107) 💥

Already hammered this personally 😈

(max bet size via BetRivers/Kambi)

Expecting some offense in this matchup. Line shopping across books as always.

Thoughts? Over or Under? 👇🏽

#MLBPicks #FreePicks #SportsBetting

20

BESS? Very toxic price action for sizing, but insane if the Revenue story isn’t a doodle.

81

<blockquote class="wp-block-quote is-layout-flow wp-block-quote-is-layout-flow">

<p>Over 2,000 years ago, Aristotle had some bars about the kids these days: “Young men have strong passions, and tend to gratify them indiscriminately,” the great philosopher wrote in <em>Rhetoric</em>. “They are changeable and fickle in their desires, which are violent while they last, but quickly over… They have exalted notions, because they have not yet been humbled by life or learnt its necessary limitations.”</p>

</blockquote>

<p>Later in the same chapter, he had some words for their elders: “They are small-minded, because they have been humbled by life: their desires are set upon nothing more exalted or unusual than what will help them to keep alive.”</p>

<p>He could have been reading my email. </p>

<p>A striking number of my readers—older, almost uniformly—skipped past the data entirely and went straight to character: younger generations complain too much. They spend recklessly. They don’t sacrifice. They <em>whine</em>.</p>

<p>What was notable wasn’t the anger. It was the precision of the deflection. No one challenged the <a href="federalreserve.gov/releases/…">Federal Reserve data</a> showing that Baby Boomers control roughly 52% of U.S. household wealth while representing about 20% of the population. No one argued that Millennials are, in fact, thriving. The response to a structural argument about wealth and power was, almost invariably, a moral argument about character.</p>

<figure class="wp-block-image size-large"><img loading="lazy" decoding="async" data-src="fortune.com/img-assets/wp-co…" alt="" class="lazyload wp-image-4505791" src="fortune.com/img-assets/wp-co…" width="1024" height="683" original-width="1200" original-height="800"></figure>

<p><a href="statista.com/statistics/1376…" target="_blank" rel="noreferrer noopener"></a>That pattern has a name in psychology. And understanding it—alongside what actually makes Boomers different from every dominant class that preceded them—tells you more about where America is stuck than any balance sheet. Is it whiny to try to understand this psychology, or is it a form of self-knowledge?</p>

<h2 class="wp-block-heading" id="two-kinds-of-threat--and-why-theyre-not-symmetrica">Two kinds of threats—and why they’re not symmetrical</h2>

<p>In 2023, researchers <a href="pubmed.ncbi.nlm.nih.gov/?ter…]">Stéphane Francioli</a>, <a href="pubmed.ncbi.nlm.nih.gov/?ter…]">Felix Danbold</a><span style="box-sizing: border-box; margin: 0px; padding: 0px;"><a href="pubmed.ncbi.nlm.nih.gov/?ter…]" target="_blank">,</a> and <a href="pubmed.ncbi.nlm.nih.gov/?ter…]" target="_blank">Michael North</a> published a <a href="pmc.ncbi.nlm.nih.gov/article…" target="_blank">peer-reviewed study</a> in </span><em>Personality and Social Psychology Bulletin </em>examining precisely what makes Boomers and Millennials hostile toward each other. The findings map almost perfectly onto the reader mail in this reporter’s inbox.<a href="pmc.ncbi.nlm.nih.gov/article…" target="_blank" rel="noreferrer noopener"></a></p>

<p>Both generations express genuine animosity toward the other. But the <em>nature</em> of that animosity is fundamentally different, and the difference is not incidental.</p>

<p>Millennials’ hostility toward Boomers is driven primarily by what <a href="http://chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/oscarybarra.lsa.umich.edu/Ma…">intergroup threat theorists</a> call <strong><a href="oar.princeton.edu/rt4ds/file…">realistic threat</a></strong>—specifically, the fear that Boomers’ delayed transmission of power hampers their life prospects. The Federal Reserve data on housing, wealth, and debt give that fear its material texture. Millennials aren’t upset about Boomer values. They’re upset about Boomer advantages, and the structural conditions that have made those advantages self-perpetuating.</p>

<p>Boomers’ hostility toward Millennials runs in the opposite direction. Their animosity is driven primarily by <em>symbolic threat</em>—perceived conflict over culture, values, and worldview. Not economics or data. The feeling that a generation coming up behind them is challenging something essential about what America is, what hard work means, what success is supposed to look like.</p>

<p>This asymmetry is a predictable feature of dominant-group psychology, older even than Aristotle. When you hold the material advantages, you don’t feel materially threatened — because you aren’t. What you feel threatened by is the <em>narrative</em> that your advantages might not be entirely earned. That is a different kind of threat that produces a different kind of defense.</p>

<h2 class="wp-block-heading" id="the-meritocracy-is-the-message">The meritocracy is the message</h2>

<p>One word I used in a previous headline was particularly triggering: “hoarding,” as in, hoarding wealth, hoarding real estate, hoarding political power and opportunity. Seen through the lens of psychology, this verb begs the question of what Boomers are actually being asked to defend.</p>

<p>It isn’t just wealth. It’s the story they’ve told about wealth—that it arrived through discipline, sacrifice and superior decision-making. And many vivid stories I’ve been told show that story isn’t entirely wrong. Many Boomers did work hard. Many did save diligently. But the story has a significant omission: they also came of age during the single most favorable economic environment in American history. Postwar manufacturing at its apex. Housing that cost 2x or 3x annual income, not 10x. Defined-benefit pensions, subsidized public universities, and a tax structure that rewarded wages as much as assets are all features of history, not current economic life.</p>

<p>Researchers who study <em><a href="http://chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/as.nyu.edu/content/dam/nyu-a…">system justification theory</a></em>—the psychological tendency to defend existing social arrangements as fair and legitimate, even when they aren’t—have found that this impulse is strongest among people who have benefited most from the system. The more you’ve gained from an arrangement, the more motivated you are to believe the arrangement is just. Not because you’re dishonest, but because the alternative — accepting that luck and timing played a decisive role in your success — is genuinely destabilizing to the self.</p>

<p>A fair objection deserves airing here: a framework in which both agreement and angry disagreement confirm the thesis risks explaining everything and therefore nothing. If every defensive email is just “system justification in action,” the argument becomes unfalsifiable. That’s why the asymmetry documented by Francioli and his colleagues matters. The claim isn’t that Boomers got angry—anyone might. It’s that the anger ran almost exclusively through one channel (character and values) while leaving the other (the data) untouched, exactly as intergroup threat theory predicts for a materially dominant group. Had readers attacked the numbers and ignored the character question, the theory would have been wrong. But they didn’t do that.</p>

<h2 class="wp-block-heading" id="not-just-any-privileged-class">Not just any privileged class</h2>

<p>Here is where the Boomer defensiveness becomes harder to dismiss—and, strangely, easier to understand.</p>

<p>Every dominant group in history has reached for the same psychological toolkit. Roman senators, English landowners and mid-century American corporate aristocracies — all told versions of the same story: <em>we have what we have because we earned it</em>. System justification is ancient. Generational condescension goes back to the Greeks.</p>

<p>But Boomers are not simply the latest iteration of a recurring historical pattern. The specific configuration of advantages they accumulated — and the mechanisms by which they accumulated them—has no real precedent. This matters, because it means the defensiveness isn’t just psychologically understandable. It’s also, in a structural sense, more consequential than prior versions of the same reflex.</p>

<p>Start with the scale. Boomers hold an estimated $85 trillion in wealth—not merely more than prior American generations at the same life stage, but more than any cohort in recorded economic history by a vast multiple. Many of them would seemingly like to think they earned this simply by working harder than anyone who came before, but they entered the housing and equity markets just before both began 40-year appreciation cycles, and they were the largest generation in American history to do so. They didn’t just accumulate wealth—they sat on top of two of the most powerful asset-appreciation engines in modern economic history during their prime earning years. <a href="smartasset.com/financial-adv…" target="_blank" rel="noreferrer noopener"></a></p>

<p>Then there’s the democratic dimension, which gets almost no attention. Previous dominant classes held power through class, race or institutional control—not raw democratic headcount. Boomers were the largest voting bloc [by eligibility or participation?] in American history for nearly four consecutive decades, from roughly 1978 until the mid-2010s. That means the policies that shaped housing markets, the tax treatment of capital gains, the defunding of public universities and the dismantling of defined-benefit pensions were debated and passed during a period when Boomers were the decisive electoral constituency. They didn’t just benefit from the system. They voted for it repeatedly at the precise moment when their demographic weight and financial self-interest were in perfect alignment. No prior privileged class had that combination of democratic legitimacy <em>and</em> self-interested policymaking available simultaneously at this scale.</p>

<p>Finally, consider what the gap actually looks like on the other side. In most prior periods of wealth concentration, the non-wealthy simply had less. What’s structurally novel now is that younger generations don’t just have less wealth—they carry the majority of the debt. Federal Reserve data shows Millennial and Gen <a href="fortune.com/company/twitter/" target="_blank">X</a> mortgage debt is nearly double that of Boomers in absolute terms. More than a third of all student loan borrowers are Millennials, and the <a href="stlouisfed.org/on-the-econom…">St. Louis Fed explicitly documents</a> a generational “clear increase in debt holdings” for younger generations. “Specifically, both Gen Xers and millennials held more debt than Baby Boomers.” Student debt—which exploded during the very decades of Boomer political dominance—has no real historical parallel in prior generational transitions. The floor has been actively lowered, not just the ceiling raised.</p>

<h2 class="wp-block-heading" id="the-cloaking-mechanism">The lattés and avocado toast</h2>

<p>There’s another concept in social psychology called <em>motivated invisibility</em> — the tendency of dominant groups to render their advantages structurally invisible, not through explicit denial but through reframing.<a href="journals.sagepub.com/doi/10.…" target="_blank" rel="noreferrer noopener"></a></p>

<p>The most durable reframe in Boomer wealth discourse is the pivot to younger-generation spending behavior: avocado toast, streaming subscriptions, the failure to delay gratification. One reader deployed this argument almost reflexively—a near-word-for-word echo of criticisms that have circulated for a decade. “Wealth is NOT a fixed amount,” they wrote to me. “Want some wealth? Go earn it and save it and accumulate it, rather than always upgrading to the latest iPhone and swilling lattés and avocado toast.” The kicker on the email brought it back to that other epithet: “you’re a whiny turd who figured out who to string some sentences together and vie for cliques.”</p>

<p>But the spending-habits argument is durable precisely because it accomplishes what the data cannot: it relocates the problem from structure to individual. If the gap is about <em>choices</em>, then no one needs to feel uncomfortable about <em>conditions</em>. The system is fine. The kids just need to cut back on lattés.</p>

<p>This is system justification in action, and it is not unique to Boomers, or to this moment. Research consistently shows that members of dominant groups across race, class, and—now, generation—reach for the same mechanism when their advantages are named. <a href="pmc.ncbi.nlm.nih.gov/article…" target="_blank" rel="noreferrer noopener"></a></p>

<h2 class="wp-block-heading" id="the-honest-caveat">The honest caveat</h2>

<p>Serious coverage of this topic requires the acknowledgment </p>

<p>Serious coverage of this topic requires the acknowledgment that Boomers are not monolithic. Per a <a href="pewresearch.org/short-reads/…">Pew Research Center analysis</a>, Boomer households collectively held $77 trillion in 2022—and the top 10% of those households held 71% of it. A white-collar Boomer who bought a San Francisco home in 1985 and maxed a 401(k) is in a categorically different position from a working-class Boomer who rented their whole life and watched their pension disappear.</p>

<p>The structural argument is real—but the villain of this story, to the extent there is one, is not a generation. It is a cohort within a generation: college-educated, propertied, politically engaged, and concentrated in expensive coastal metros. They shaped the policy environment in their own interest during the decades when their demographic weight gave them the power to do so. And they are, not coincidentally, the people most likely to be reading <em>Fortune</em>—and writing back.</p>

<p>The scolding reflex, it turns out, doesn’t even stop at the generational boundary. It operates within the generation, too. One Boomer reader described protesting the Vietnam War at 18 and feeling “angst about selling out”—”then I grew up,” he wrote. He told me he isn’t rich, but he “worked my way up to making enough to make sure my kids weren’t hungry.” His verdict on his peers was harsher than anything Millennials sent me: “I am not rich, but I am not complaining. And I can’t believe that so many in my generation of Flower Children are such losers.” The character argument, in other words, is not really about age. It is a portable script, and it gets deployed downward—at whoever has less—regardless of birth year.</p>

<p>Another reader put it more cleanly than most: “The bigger issue is not old versus young. It is a broken American system that has made housing unaffordable, healthcare unaffordable, retirement insecure, and work feel unstable for nearly everyone.” That framing is neither wrong nor incompatible with the structural argument about how we ended up in a place where everyone feels stuck, and like everyone else is whining about it.</p>

<p>That is a harder emotional position than defensiveness. It requires disaggregating two things that Boomer identity has long held together: the real effort and the real tailwind. It requires acknowledging that you can deserve what you earned and still have been given conditions that made earning easier — conditions that were then, through the very political power that prosperity enabled, systematically withdrawn from the people who came after.</p>

<p>Jon from the Channel Islands sees an even larger force gathering behind the generational one. The Boomer/Millennial wealth debate, he argued, is being overtaken by a capitalism-and-AI-driven concentration that will make the current gap look modest—wealth flowing not from young to old but from nearly everyone to the owners of the machines. The combatants in the generational war, in his telling, are arguing over a shoreline that is about to be redrawn entirely: “It is like they are scratching their heads wondering why the water has suddenly drained out of the bay,” he wrote, “oblivious to the tsunami that is coming in shortly, to swallow them up.”</p>

<p>Only a few readers asked the question that none of the angry emails even approached. My favorite: “How do we build a country where younger people can rise without older people being discarded?” That is a political question, not a generational one. The answer isn’t unknowable, but the people with the most power to shape it have spent the better part of a decade arguing about whether the question is fair.</p>

<p>This story was originally featured on <a href="fortune.com/2026/06/14/why-a…" target="_blank">Fortune.com</a></p> fortune.com/2026/06/14/why-a…

32

22m

To expand on this btw, people are ORGANICALLY making UGC with it which is like a complete fuckin bull signal.

I sidelined myself early on but because of this I may end up sizing in large. Will keep yall updated.

29

Retail P retweeted

The Air Jordan 7 OG “Playoffs” will RETURN on February 20, 2027! ❤️💜

ALL-STAR WEEKEND. Full-family sizing.

36

361

2,768

100,986

Dommm retweeted

2026 Air Jordan 9 OG detailed look! 🏀🔥

Releasing on August 29 in full-family sizing.

11

129

926

20,991

before i order any eternal sunshine tour merch, how does the sizing compare to merch from the swt??? i wanna make sure i get the right sizes since imma be ordering online

7

But thin books mean orders are restricted.

> order sizing is restricted to book depth

4