Antrell Not as a human title but as a Pre Creational Frequency one which only activates once the simulation itself realigns with the Real Sunstream from beyond the Dome.....

24

Jun 5

One person was seriously hurt in a crash on Sunstream Parkway on Friday morning, according to Virginia Beach police. wtkr.com/news/in-the-communi…

256

Theo Platt (Scottish, b.1960)

"Sunstream," 2025

Oil on canvas

48 x 47 in

21

78

1,470

On tonight's episode of @SyfySistas' Two Moons and a Microphone Tanya & guests discuss the iconic children of Cutter & Leetah: Ember, Suntop/Sunstream & Goldruff.

Who is your favorite of Cutter & Leetah’s cubs? Tune in and discuss in the comments!

Watch: youtube.com/watch?v=OOlh8Cbv…

1

5

15

267

May 19

#RenewableEnergy solutions provider Sunstream Green Energy completed a ₹7 billion (~$72.67 million) refinancing with @TheOfficialSBI for an over-250-MW #solar portfolio developed over three years across 17 sites in #Maharashtra.

mercomindia.com/sunstream-se…

1

1

86

May 15

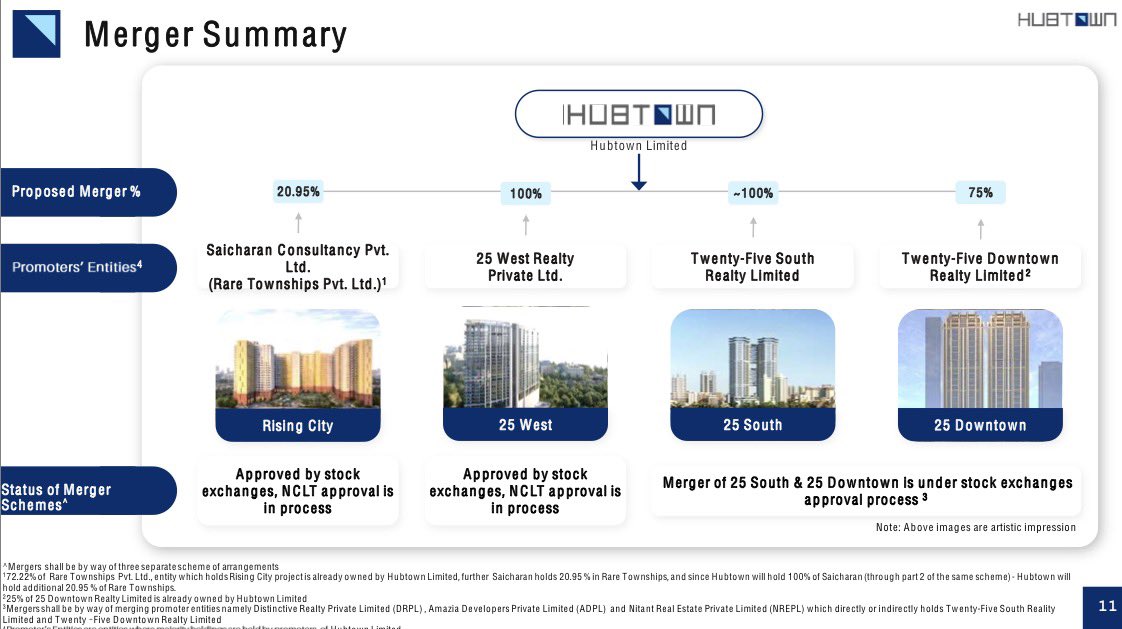

HUBTOWN LIMITED

The biggest balance sheet event in Mumbai real estate for FY26.

Hubtown just released FY26 operational highlights and Q3 investor presentation. Headline pre-sales of Rs 4,382 crore. Collections of Rs 1,910 crore.

But the real story is buried in three merger schemes.

WHAT IS BEING MERGED

Four promoter entities folding into listed Hubtown via three separate schemes of arrangement.

1. Saicharan Consultancy (Rising City, Ghatkopar): additional 20.95 percent

1. 25 West Realty (Bandra): 100 percent

1. Twenty-Five South Realty (Prabhadevi): close to 100 percent

1. Twenty-Five Downtown Realty (Mahalaxmi): 75 percent

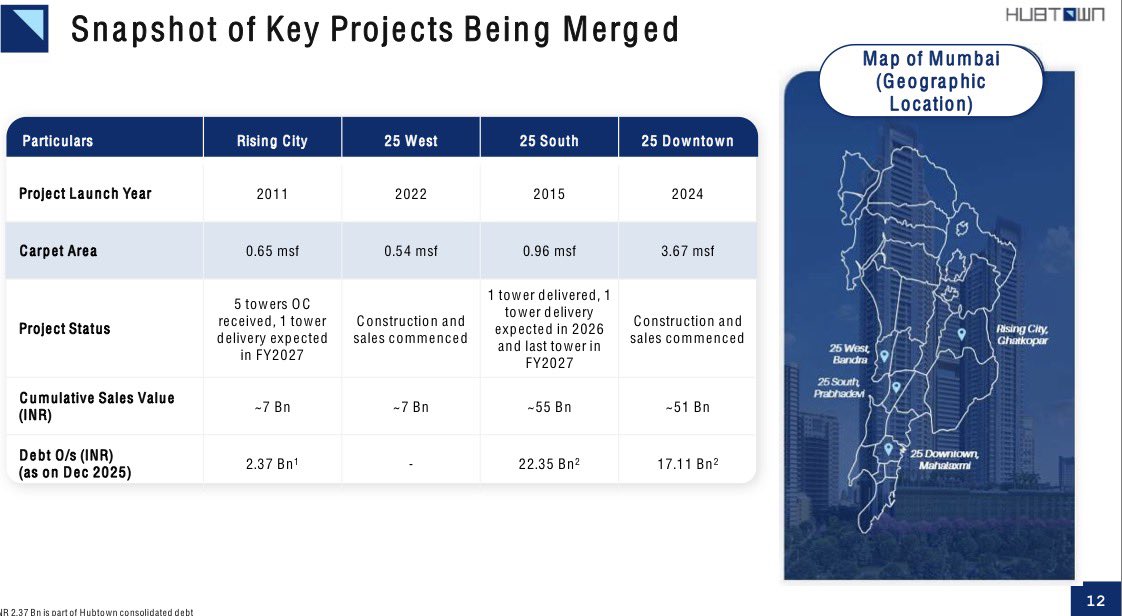

Total carpet area coming on listed books: 6.0 plus msf

Cumulative sales value of these four projects: Rs 12,000 crore plus

25 West and Rising City schemes have been approved by stock exchanges. NCLT approval pending.

25 South and 25 Downtown scheme is still under stock exchange approval.

WHAT THIS DOES TO THE BALANCE SHEET

Standalone listed Hubtown debt at Dec 2025: Rs 1,127 crore (down from Rs 2,302 crore in March 2017).

Merger entity debt: Rs 3,947 crore

25 South: Rs 2,235 crore

25 Downtown: Rs 1,711 crore

25 West: Nil

Proforma combined gross debt: Rs 5,074 crore (includes accrued interest and redemption premium)

Proforma net debt: Rs 4,696 crore

Proforma debt to equity: 1.96

Standalone debt to equity: 0.48

Average cost of debt: 15.15 percent.

WHY MANAGEMENT THINKS THIS WORKS

25 South is 90 percent plus sold at Rs 5,586 crore total sales value. Collections till date Rs 4,657 crore. Balance receivable around Rs 929 crore. Completion targeted FY27.

That cash is meant to service the 25 South debt of Rs 2,235 crore.

25 Downtown is 3.67 msf, only 14 percent complete. Just 50 percent inventory of launched towers sold. Rs 5,100 crore total sales value booked so far, only Rs 508 crore collected. Tower 5 approval received.

This is the long tail cash flow engine.

THE PROFORMA OPERATING NUMBERS

9MFY26:

Area sold 0.88 msf

Units sold 479

Pre-sales Rs 3,603 crore

Collections Rs 1,507 crore

9MFY25:

Pre-sales Rs 2,498 crore

Collections Rs 1,063 crore

44 percent growth in pre-sales. 42 percent growth in collections.

FY26 full year pre-sales of Rs 4,382 crore versus FY25 of Rs 3,921 crore. 11.7 percent annual growth at the proforma level.

Q3FY26 alone delivered Rs 2,086 crore pre-sales, driven largely by 25 Downtown bookings (Rs 2,313 crore in 9M from 106 units in Mahalaxmi).

THE CASH FLOW TENSION

9MFY26 operating cash flow pre-interest post-tax: Rs 650 crore positive.

9MFY26 finance costs: Rs 962 crore.

Post-interest operating cash flow: minus Rs 312 crore.

Finance cost is eating the entire operating cash flow.

Equity and warrant infusion of Rs 103 crore plus fresh debt of Rs 373 crore in 9MFY26 kept free cash flow at Rs 164 crore positive.

The cost of debt at 15.15 percent is the binding constraint. Until the debt stack gets refinanced cheaper or paid down from 25 South collections, operating earnings will stay capital structure constrained.

WHAT IS IN THE OPTIONALITY BUCKET

Sunstream City, Mulund-Thane: 141 acres freehold, 26.63 msf development potential. Hubtown stake 40.67 percent. Approvals secured. Yet to launch.

25 Estates, Khalapur: 174 acres, 2.66 msf weekend homes. Advanced planning.

Hubtown Rising City Phase 2: 1.95 msf commercial pipeline in Ghatkopar.

Breach Candy plot: 0.24 acres in South Mumbai. Advanced planning.

Hubtown Commercial off BKC: 2.55 acres in 50:50 JV.

None of these are in current sales numbers.

WHAT TO WATCH

1. NCLT timeline for the first two schemes (25 West and Rising City)

1. Stock exchange approval for the 25 South and 25 Downtown scheme

1. 25 South handover trajectory in FY27. This is the cash unlock event.

1. Sales velocity at 25 Downtown given 2.56 msf unsold inventory

1. Debt servicing capability on the proforma Rs 5,074 crore book

1. Any refinancing of the 15.15 percent average cost of debt

Dis: This post is for educational purposes only

3

14

2,712

Lmao ok this is reallllly getting fishy. Just constantly dumping $SNDL right before the SUNSTREAM USA assets get rolled into the books.

What is going on?!

Who is paying DanTheETFMan to do them a favor and dump these shares?

@AdvisorShares watching you cunts.

3

170

May 8

Pourquoi PADFA II pre-selectionne une entreprise qui est INACTIVE, SUNSTREAM CAMEROUN??

2

2

275

$SNDL

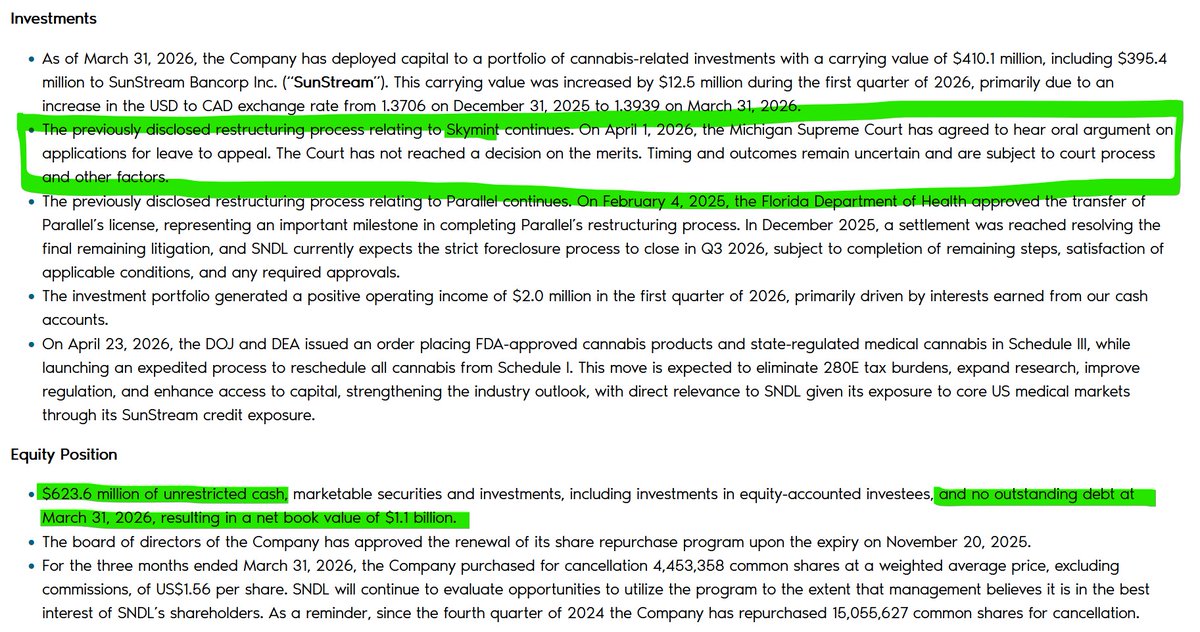

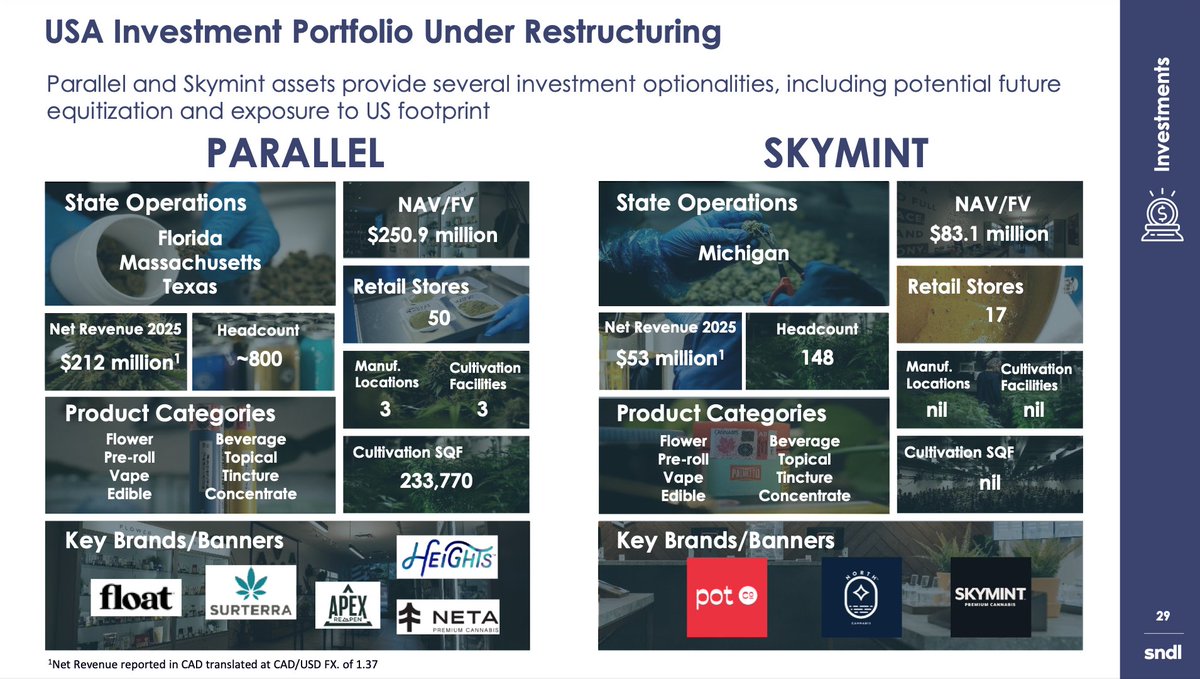

-- Part 1. APPRECIATING SKYMINT TAKE OVER. And your other question will be about Skymint. The Medical Cannabis Recreational part of Cannabis $SNDL Portfolio. ( Parallel/Surterra is STRICTLY Medical Cannabis. ) Skymint is: BOTH. Today's update on Skymint: "The previously disclosed restructuring process relating to Skymint continues. On April 1, 2026, the Michigan Supreme Court has agreed to hear oral argument on applications for leave to appeal. The Court has not reached a decision on the merits. Timing and outcomes remain uncertain and are subject to court process and other factors." Explanation: Important context: The actual transfer of Skymint is essentially done. SunStream (SNDL’s group) already took full control via a $109.4 million credit-bid sale back in October 2023. The assets now belong to them.

--Part 2. APPRECIATING SKYMINT TAKE OVER. This Michigan Supreme Court appeal is just a side quest — a last-ditch push by these specific landlords against the court-appointed Receiver (Gene Kohut). It’s not trying to undo the whole takeover; it’s only trying to get more Skymint lease money owed, but settled, out of the take over. Bottom line: Small group of landlords vs. the Receiver over a few million in rent claims. Sky Mint owed $127M to Sun Beam ( SNDL ) ballooned from 70mil initial loan. Skymint debt takeover by SNDL/SunStream is long finished. This is lingering noise, not a threat to the deal. Who are the landlords? = 1. Koach Group (the main ones fighting) Koach GR II, LLC Koach Ypsilanti I, LLC (They own the big Ypsilanti cultivation facility that Skymint leased.) 2 3Fifteen Parties 3Fifteen Cannabis business (trade name of Green Skies Healing Tree, LLC and its affiliates). (They had leases/contracts with Skymint that were thrown out by the Court.)

--PART 3. APPRECIATING SKYMINT

How much is owed to them?They are mainly fighting over unpaid back rent lost future rent after the Receiver canceled their leases.

Koach was owed roughly $1 million in back rent on their properties (especially the Ypsilanti facility).

3Fifteen had similar lease/contract claims (exact amount not publicly detailed, but in the same range of hundreds of thousands to low millions).

What the landlords seek:They want the Supreme Court to overturn the lease rejections and strike the cross-default rulings. Basically, they’re asking the judge to reconsider and give them a bigger payout or better settlement terms — closer to what they originally expected under the full lease contracts.

Tech is coming to Med/Cannabis post 280E exemption. You shall see:

$SPY $GOOGL $AMZN

Cannabis Tickers of interest:

$VFF $TCNNF $MSOS $TCNNF $CURLF $MSOS $CGC $TLRY $CRON $ACB $HITI $OGI $VFF $IMCC $JAZZ $MAPS $RYM $LYFLY $GRWG $HYFM

1

2

173

$SNDL

— PART 1 = APPRECIATING WHAT HAPPENED WITH PARALLEL TAKE OVER.

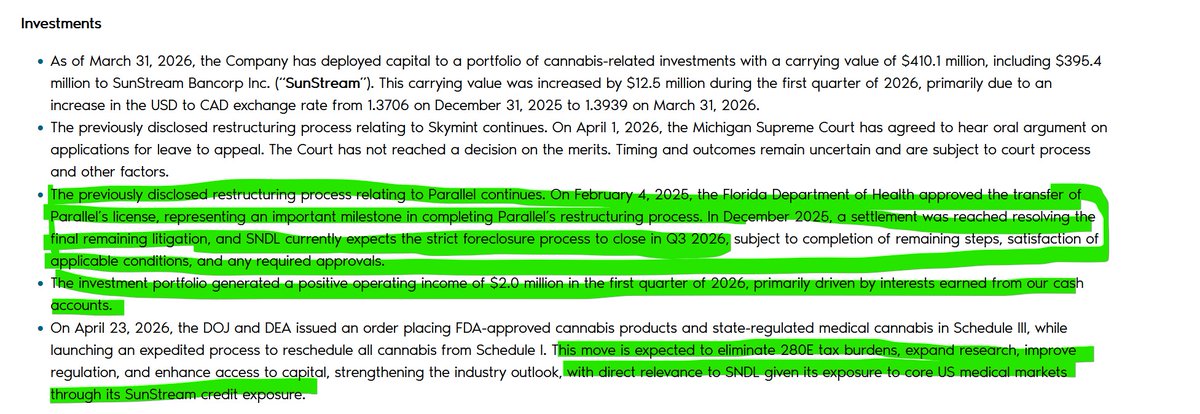

Major de-risking update from today’s Q1 2026 earnings: After Parallel (Surterra) defaulted on its debt in 2023, SunStream launched the strict foreclosure to take control of the assets. Context on the scale: SunStream’s affiliate (Talladega) originally lent ~$150 million to Parallel starting in 2021. That debt ballooned with interest and bridge loans. This triggered a long, nasty legal war from minority shareholders and junior creditors. They sued, claiming they were misled about Parallel’s finances — especially tied to the failed 2021 $1.9B SPAC deal with Scooter Braun’s Ceres Acquisition Corp. Former CEO Beau Wrigley Jr. (Wrigley chewing gum heir) and other execs were accused of securities fraud and misrepresentations that led investors to pour money in via SAFE agreements right before the SPAC collapsed.

-- PART 2 = APPRECIATING WHAT HAPPENED WITH PARALLEL TAKE OVER.

These lawsuits became a huge multi-year blocker, stalling license transfers and the entire restructuring for nearly two years.

$ Game changer: In December 2025, a settlement was reached that resolved the final remaining litigation. No more active court fights blocking SunStream’s takeover. Key milestones already cleared: February 2025: Florida DOH approved the critical license transfer SNDL now expects the strict foreclosure to fully close in Q3 2026. The bargain: SunStream is set to gain majority economic control (~2/3 ownership) of Parallel’s valuable medical cannabis assets (Florida being the crown jewel) by converting a distressed ~$150M loan into ownership of a platform that historically generated ~$208M annualized revenue (2023 run-rate on the pledged assets) and will carry only ~$100M in post-closing debt. That’s a massive debt reduction rescheduling/280E tailwinds = huge asymmetric upside for SNDL. This is a textbook distressed debt win. Source: Official SNDL Q1 2026 Earnings Release → sndl.com/news/news-details/2…

$SPY $GOOGL $AMZN $VFF $TCNNF $MSOS $TCNNF $CURLF $MSOS $CGC $TLRY $CRON $ACB $HITI $OGI $VFF $IMCC $JAZZ $MAPS $RYM $LYFLY $GRWG $HYFM

$SNDL

Valuation check using latest filings: • $623.6M in cash securities investments (no debt) Source: sndl.com/news/news-details/2… • ~$213M actual cash, rest = investments SunStream exposure Source: stocktitan.net/sec-filings/S… • Parallel (via SunStream) still in restructuring, Florida license transfer approved Source: reddit.com/r/weedstocks/comm…

👉 Simple math on liquidity: $623.6M ÷ 259M shares = $2.41 /share (headline liquidity)

Conservative haircut (~85% usable): $623.6M × 0.85 = $530M $530M ÷ 259M = $2.05 /share adjusted floor

👉 Base case (adds ops Parallel post-280E value): $2.05 $0.58 $0.87 = $3.50 /share (Where: ops ≈ $150M/259M, Parallel ≈ $225M/259M)

👉 Bull case: $2.28 (liquidity) $0.58 (ops) $1.16 (Parallel) = $4.02 /share Current price (~$1.31) implies:

➡️ significant discount to balance sheet SunStream/Parallel embedded value

Core question isn’t cash — it’s realization speed of SunStream Parallel cash flows into SNDL equity.

Tech is coming here: $SPY $GOOGL $AMZN

$VFF $TCNNF $MSOS $TCNNF $CURLF $MSOS

$CGC $TLRY $CRON $ACB $HITI $OGI $VFF $IMCC $JAZZ $MAPS $RYM $LYFLY $GRWG $HYFM

mmapplication.diversion.dea.…

1

4

2,245

$SNDL

Valuation check using latest filings: • $623.6M in cash securities investments (no debt) Source: sndl.com/news/news-details/2… • ~$213M actual cash, rest = investments SunStream exposure Source: stocktitan.net/sec-filings/S… • Parallel (via SunStream) still in restructuring, Florida license transfer approved Source: reddit.com/r/weedstocks/comm…

👉 Simple math on liquidity: $623.6M ÷ 259M shares = $2.41 /share (headline liquidity)

Conservative haircut (~85% usable): $623.6M × 0.85 = $530M $530M ÷ 259M = $2.05 /share adjusted floor

👉 Base case (adds ops Parallel post-280E value): $2.05 $0.58 $0.87 = $3.50 /share (Where: ops ≈ $150M/259M, Parallel ≈ $225M/259M)

👉 Bull case: $2.28 (liquidity) $0.58 (ops) $1.16 (Parallel) = $4.02 /share Current price (~$1.31) implies:

➡️ significant discount to balance sheet SunStream/Parallel embedded value

Core question isn’t cash — it’s realization speed of SunStream Parallel cash flows into SNDL equity.

Tech is coming here: $SPY $GOOGL $AMZN

$VFF $TCNNF $MSOS $TCNNF $CURLF $MSOS

$CGC $TLRY $CRON $ACB $HITI $OGI $VFF $IMCC $JAZZ $MAPS $RYM $LYFLY $GRWG $HYFM

mmapplication.diversion.dea.…

$SNDL = This is a no-brainer deal right now. @sndl_inc

Analyst ( ATB) pointed out that more than half the company’s value is just cash sitting in the bank.

After subtracting that cash, the whole business (Canadian stores U.S. cannabis assets) — which brings in roughly $1 Billion in yearly revenue — is only valued at about $170 million. And it has zero debt.

5 million shares bought and sold today by SOMEBODY, guess who? 13F's will soon tell us.

Volume for today for $SNDL 6,118,966 vs yesterday which was less than a MILLION AT CLOSE.

Smart money quietly buying the dip.

Can’t wait to see the big fund filings.

$MSOS $TCNNF Tech innovation coming to this sector like a beast post 280e exemption $SPY

The portal is open and ready to convert Medical Cannabis US based operators into extremely profitable overnight, and retroactive margin expansion overnight to the likes of $SNDL $TCNNF $CURLF and others.

mmapplication.diversion.dea.…

2

808

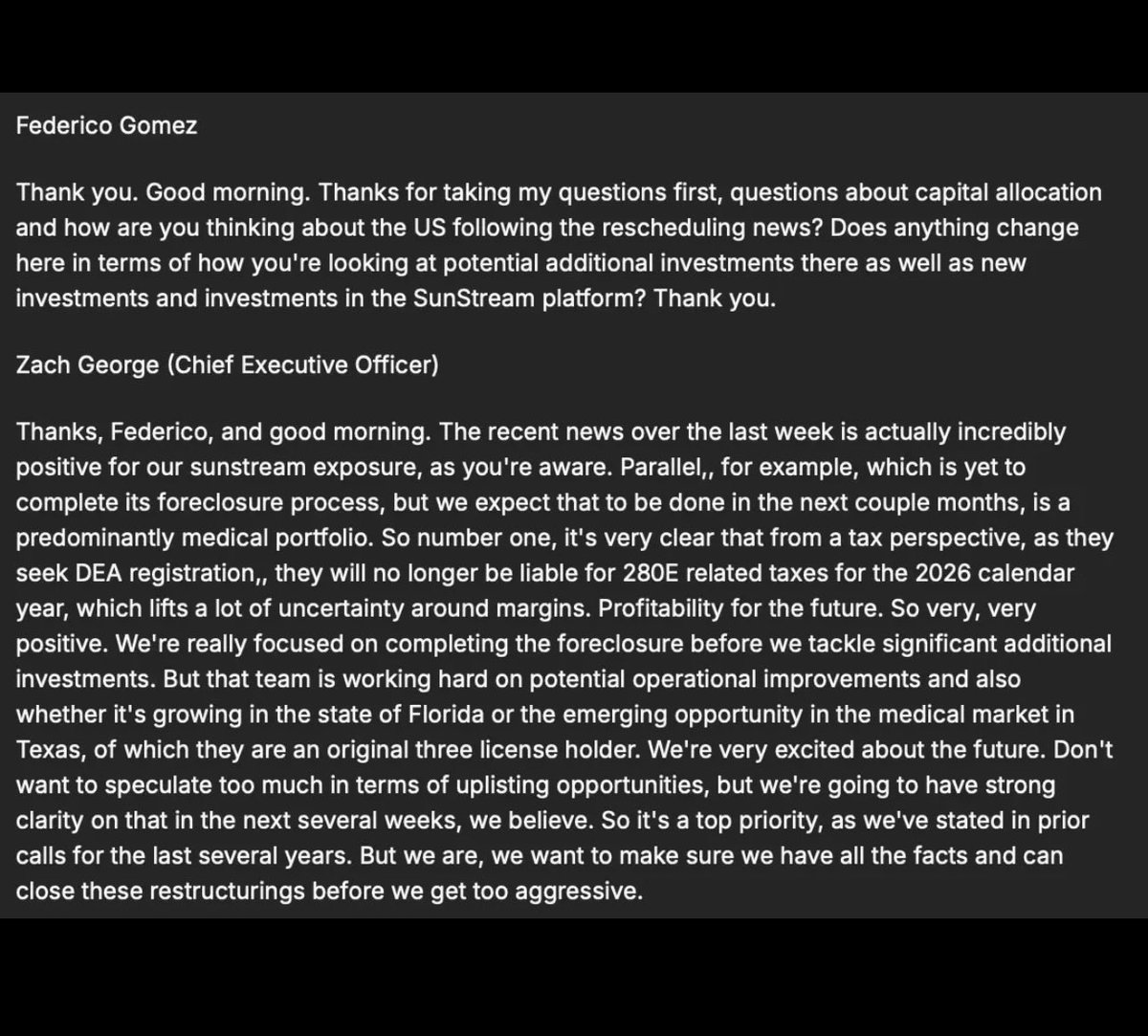

Substantiation with Conference Call Transcript =

Question directed at = CEO BY =

Federico Gomez

Thank you. Good morning. Thanks for taking my questions first, questions about capital allocation and how are you thinking about the US following the rescheduling news? Does anything change here in terms of how you're looking at potential additional investments there as well as new investments and investments in the SunStream platform? Thank you.

REPY =

Zach George (Chief Executive Officer)

Thanks, Federico, and good morning. The recent news over the last week is actually incredibly positive for our sunstream exposure, as you're aware. Parallel,, for example, which is yet to complete its foreclosure process, but we expect that to be done in the next couple months, is a predominantly medical portfolio.

So number one, it's very clear that from a tax perspective, as they seek DEA registration,, they will no longer be liable for 280E related taxes for the 2026 calendar year, which lifts a lot of uncertainty around margins. Profitability for the future. So very, very positive. We're really focused on completing the foreclosure before we tackle significant additional investments.

But that team is working hard on potential operational improvements and also whether it's growing in the state of Florida or the emerging opportunity in the medical market in Texas, of which they are an original three license holder. We're very excited about the future. Don't want to speculate too much in terms of uplisting opportunities, but we're going to have strong clarity on that in the next several weeks, we believe. So it's a top priority, as we've stated in prior calls for the last several years. But we are, we want to make sure we have all the facts and can close these restructurings before we get too aggressive.

$SNDL $MSOS $CURLF $TCNNF $CGC $GTBIF $VFF $TLRY tech innovation will pout into this sector after 280E

$SPY $AAPL $GOOGL $AMZN $INTC $META $AMD $IWM $QQQ

1

2

47

⠀ ⋆✴︎ 𝓦𝐈𝐏 .☘︎ ݁˖ KISARAGI 𝗔͟𝗢͟𝗜. 24. i̵l̵legitimate son &&. HEIR to 𝓼unstream ent. he/him. mentions of abuse, and other issues will be tagged accordingly. 𝐝𝐞𝐚𝐝 𝐝𝐨𝐯𝐞 — do not eat.

1

7

7

170

Healthy add for $SNDL at 1.35

Cost avg overall just under 1.5

No ceiling here for me…will add until the SUNSTREAM assets are on the balance sheet.

Price target $5

2

11

703

$SNDL

✅ Confirmed Link (Official SNDL Disclosure):

Here’s the direct link from SNDL’s Q1 2026 Earnings Release (published today, April 29, 2026) that confirms the Florida license transfer and current status:

➡️ sndl.com/news/news-details/2…

$SNDL —

$MSOS $SNDL $TCNNF $CGC $SPY $IWM $GTBIF

The under-the-radar 280E killer just got a massive upgrade 🔥

SNDL (via SunStream) is on track to take full control of Surterra Wellness Florida — a top-tier operator with ~45 dispensaries and a rock-solid medical cannabis footprint.

Florida DOH approved the license transfer to the SNDL/SunStream entity on Feb 4, 2025. Litigation settled in Dec 2025. Strict foreclosure now expected to close Q3 2026.

Why this matters right now:

Schedule III rescheduling (DOJ/DEA order April 23, 2026) kills 280E for state-regulated medical cannabis. That tax nightmare that used to eat 70-80% of U.S. cannabis profits? Gone.

Once this foreclosure closes, SNDL’s C$395M SunStream investment flips from a credit play into direct ownership of profitable U.S. medical cannabis assets — fully post-280E.

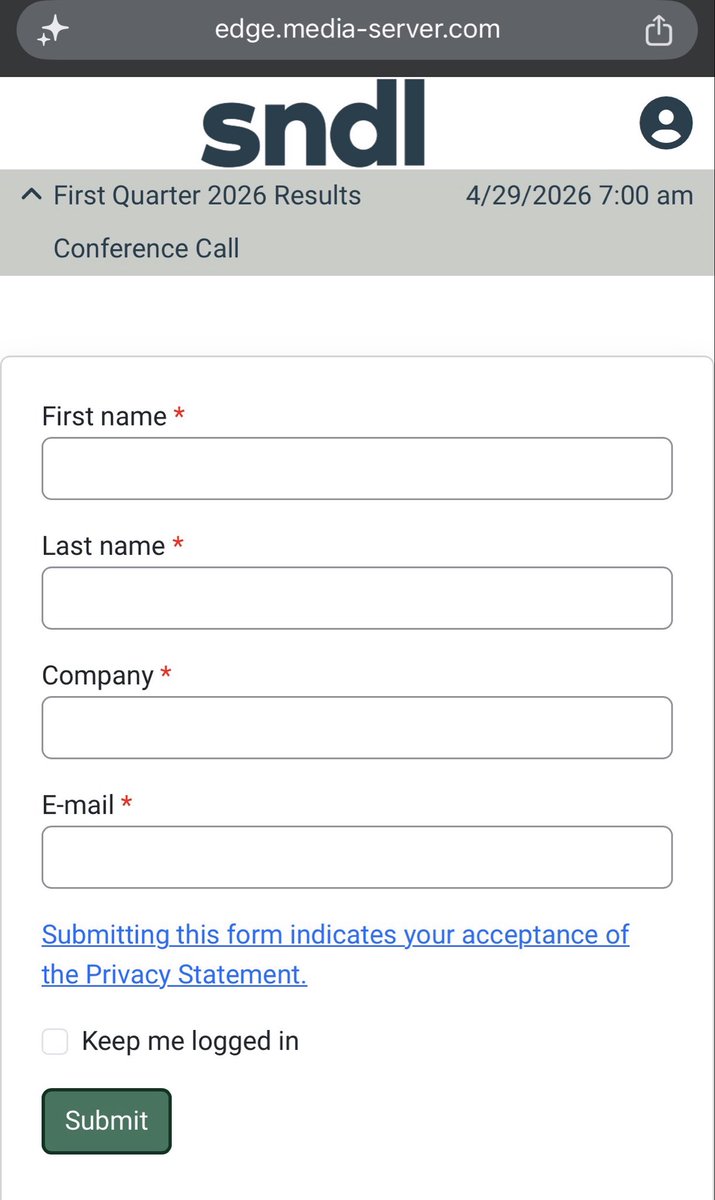

$SNDL

Conference call link = IN LESS THAN AN HOUR=

edge.media-server.com/mmc/p/…

Portal for Medical Cannabis to register 280E Free today =

mmapplication.diversion.dea.…

$MSOS $CGC $CURLF $TCNNF

$SNDL

$CURLF $MSOS $SNDL $SPY $TCNNF

same date as $SNDL earnings.... before bell

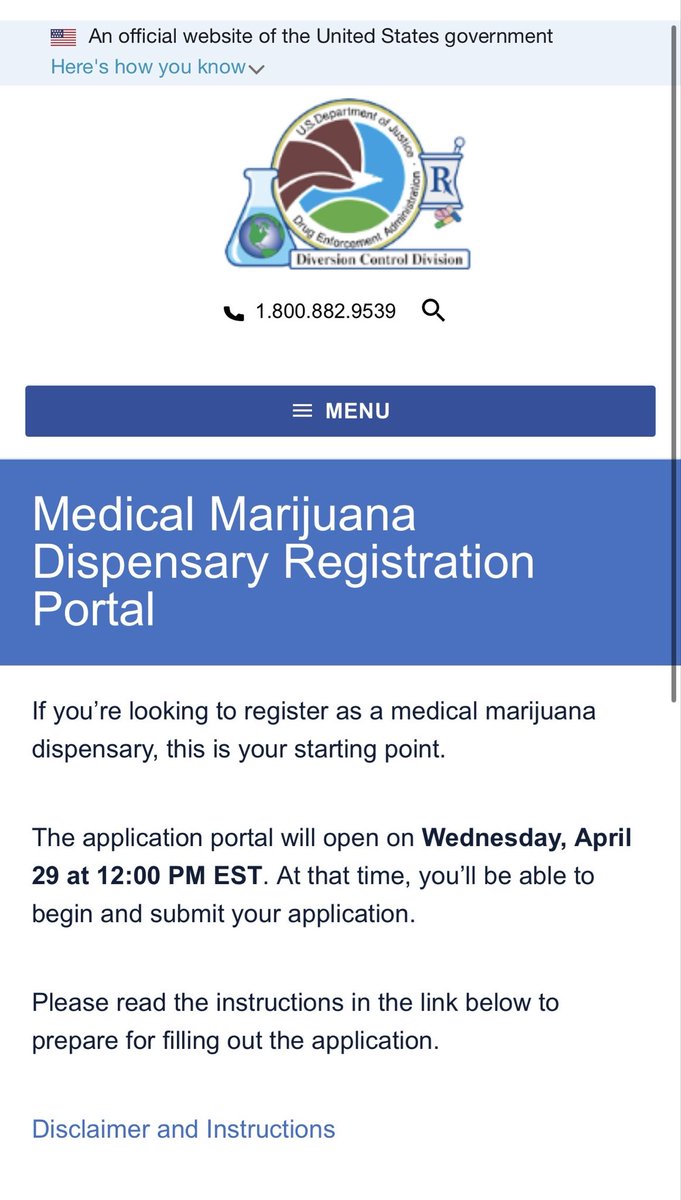

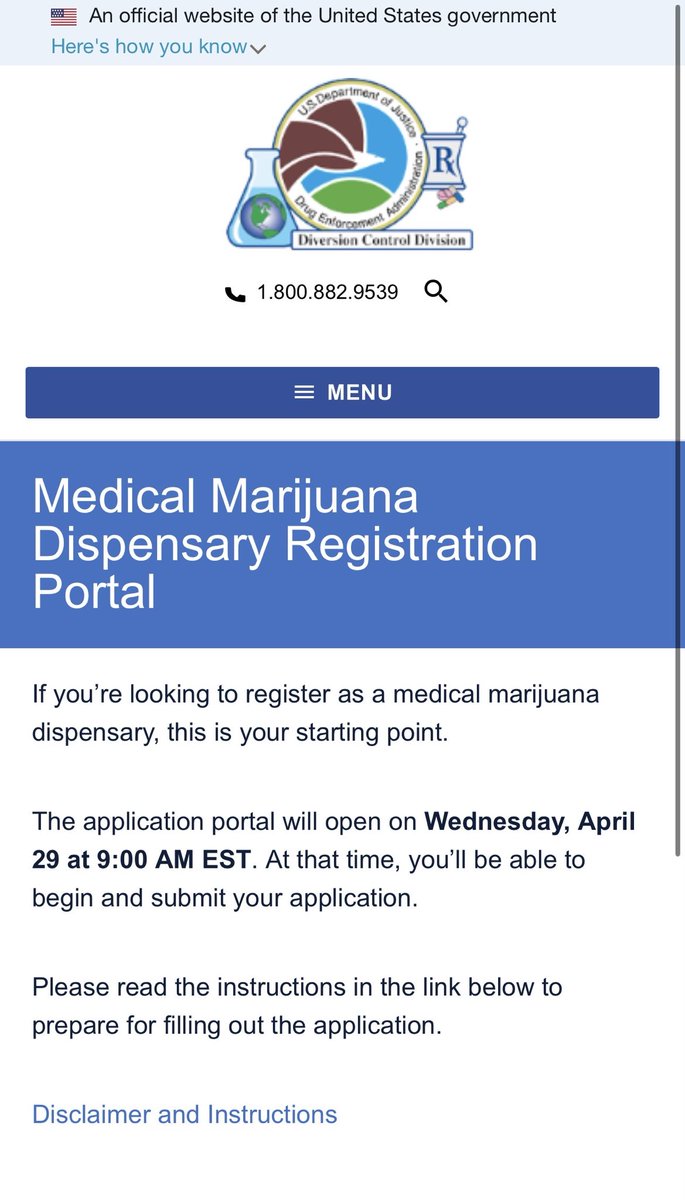

"If you’re looking to register as a medical marijuana dispensary, this is your starting point.

The application portal will open on Wednesday, April 29 at 9:00 AM EST. At that time, you’ll be able to begin and submit your application.

Please read the instructions in the link below to prepare for filling out the application."

mmapplication.diversion.dea.…

3

2

11

2,223

$200M cash on hand and $400M SUNSTREAM USA Portfolio....trading under a $400M market cap

pretty awesome US exposure for a Canadian company listed on a major exchange :) . $SNDL s201.q4cdn.com/372870431/fil…

3

2

505

Apr 29

$SNDL Earnings — Slightly Bullish 🚀

🏷️ $1.39

SNDL Reports First Quarter 2026 Financial and Operational Results

Revenue:

• Actual: $195.9 million

• YoY Change: -4.4%

EPS:

• Actual: N/A (Operating Loss of $(9.1) million reported)

• YoY Change: Operating Loss improved by 24.4% (from $(12.1) million in Q1 2025 to $(9.1) million in Q1 2026)

Key Metrics:

• Net Income/Loss: $(9.1) million (Operating Loss)

• Gross Margin: 27.0%

• Cash Position: $213.4 million (unrestricted cash)

Guidance: The Company is deploying initiatives expected to contribute approximately $20 million of incremental operating income over the remainder of the year.

Bull Case:

**Improved Operating Loss:** Operating loss significantly improved by 24.4% year-over-year, and Adjusted Operating Loss also saw a slight improvement despite market headwinds.

**Strong Balance Sheet & Liquidity:** SNDL maintains a robust financial position with $213.4 million in unrestricted cash and no outstanding debt, providing flexibility for strategic growth.

**Strategic Growth & US Rescheduling Tailwinds:** Successful launch of the Jeeter contract in Canada, ongoing profit-enhancement initiatives, and significant progress in SunStream restructuring, coinciding with the positive momentum from US cannabis rescheduling (DOJ/DEA Schedule III), which is expected to eliminate 280E tax burdens and strengthen the industry.

Bear Case:

− **Revenue Decline:** Net revenue decreased by -4.4% year-over-year, driven by persistent market headwinds and softness in both Liquor and Cannabis segments.

− **Negative Cash Flow:** The company reported negative cash flow of $(26.7) million and negative free cash flow of $(7.6) million, partly due to share repurchases and investments.

SNDL's Q1 results present a mixed picture with revenue declines and negative cash flow, but a notable improvement in operating loss and a very strong balance sheet. The proactive strategic initiatives and the major macro catalyst of US cannabis rescheduling, directly relevant to SNDL's investments, suggest significant upside potential that could overshadow current market softness and drive short-term price volatility.

#earnings #trading

Not financial advice. DYOR.

1

3

498

We’re excited to reveal the SECOND series of Arcane Vault x ElfQuest Pins — and wave 1 (of 3) brings something truly special.

Featuring:

Sunstream

Ember

Dre-Ahn

Goldruff

Pre-order here: arcanevault.com/elfquest-pin…

ALT Series 2 of the ElfQuest pin collection is available for pre-order now from the arcane vault.

2

3

15

493

$SNDL POST RESCHEDULING WE ARE NOT JUST CANADAS LARGEST PTIVATE CANNABIS AND LIQUOR OPERATOR, BUT NOW ONE OF THE TOP FIVE MSO OPERATORS STATESIDE WITH THAT LEGALIZATION OCURRENCE TRIGGERING EVENT WHICH **INCLUDES** RESCHEDULING IN THE WARRANT CLAUSE VIA SUNSTREAM THEIR LENDING ARM. THEY BOUGHT OUT VIA WARRANTS ENTIRE US SOIL INDUSTRIES FOR OWNERSHIP WARRANTS ( PROVIDED NEEDED LIQUIDITY TO THESE INDUSTRIES STATESIDE) NOW WITH RESCHEDULING THEY CONVERT TO FULL EQUITABLE SHARES BEYOND WARRANTS. SNDL CAN REPORT ON 280E TAX EXEMPT REVENUE AND MARGIN EXPANSION FROM YESTERDAY FORWARD. WE ARE NOW SURTERRA USA MEDICAL CANNABIS NOT JUST SNDL CANADA .

$MSOS $CGC $CURLF $SPY

surterra.com

$CGC $CURLF $MSOS $SNDL $SPY

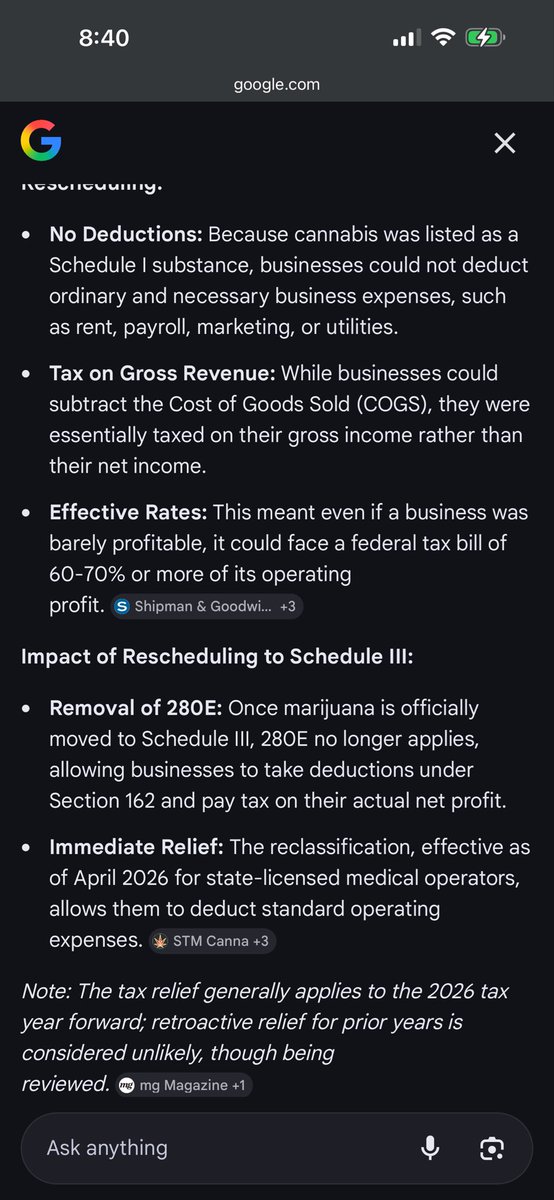

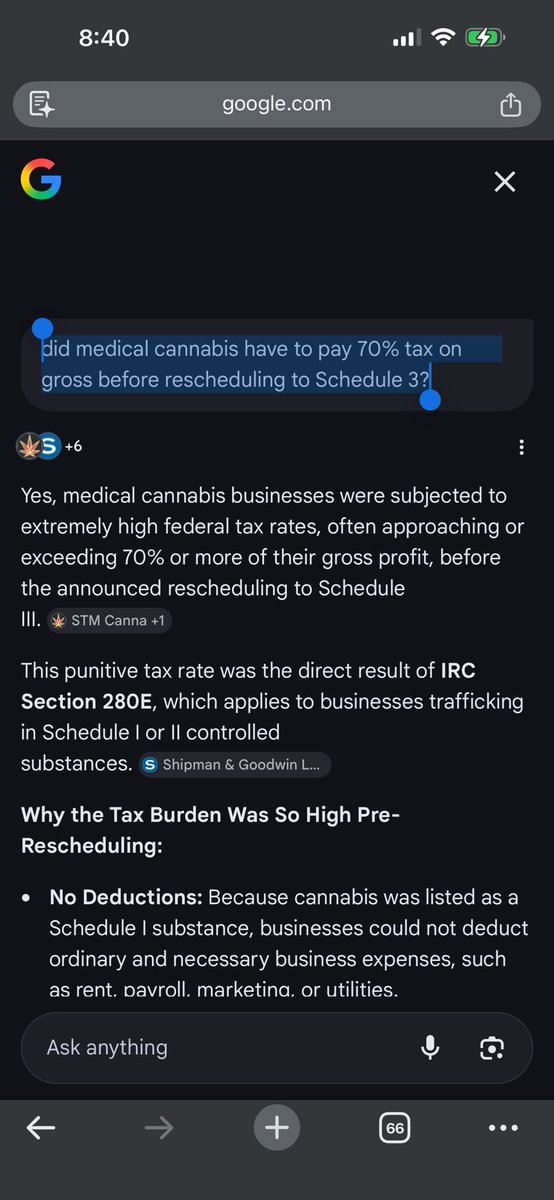

prompt= did medical cannabis have to pay 70% tax on gross before rescheduling to Schedule 3?

ANSWER=

Yes, medical cannabis businesses were subjected to extremely high federal tax rates, often approaching or exceeding 70% or more of their gross profit, before the announced rescheduling to Schedule

**Impact of Rescheduling to Schedule III**:

Removal of 280E: Once marijuana is officially moved to Schedule III, 280E no longer applies, allowing businesses to take deductions under Section 162 and pay tax on their actual net profit.

Immediate Relief: The reclassification, effective as of April 2026 for state-licensed medical operators, allows them to deduct standard operating expenses.

surterra.com/ = $SNDL

What does Today Rescheduling REALLY MEAN? = THIS IS EFFECTIVE = **TODAY** FOR MEDICAL CANNABIS The move from Schedule I to Schedule III means that state-licensed medical marijuana businesses are no longer subject to Section 280E, which previously barred them from deducting ordinary business expenses.

Tax Relief: Businesses can now deduct standard operating costs such as rent, payroll, marketing, and insurance. Lower Effective Tax Rates: Licensed operators, who previously faced effective federal tax rates as high as 70% or more, will now be taxed on net profits rather than gross income, similar to traditional businesses.

Retroactive Potential: The order specifically encourages the Treasury Secretary to consider providing retrospective relief for past tax years in which a licensee operated under a state medical marijuana license.

$SNDL Earnings is next week : April 29th before market.

$SNDL Third largest Cannabis provider after $CURLF and $TCNNF

Upon full warrant conversion, $SNDL becomes the US top five (MSO) Multi State Operator.

$CMPS $SPY $IWM $BIB $TLRY

4

1,021

$SNDL $MSOS $CGC $CURLF $GTBIF WE ARE GONNA RUN SO HARD.

THIS CHANGES EVERYTHING. **$SNDL ** ALL OUR U.S. SOIL WARRANTS (EMPIRE) JUST CONVERTED FROM SUNSTREAM!!!!! IRS TAX LAW = 280 E FOR SCHEDULE 1 !!!= IS OUT THE DOOR!!FOR US!!!!

"Under the decisive leadership of POTUS, this Department of Justice is delivering on his promise to improve American healthcare. This includes:

• Immediately rescheduling FDA-approved marijuana and state-licensed marijuana from Schedule I to Schedule IIl

• Ordering a new, expedited hearing with set deadlines, to fully reschedule marijuana

These actions will enable more targeted, rigorous research into marijuana's safety and efficacy, expanding patients' access to treatments and empowering doctors to make better-informed healthcare decisions."

x.com/dagtoddblanche/status/…

This the guy Trump singled out to execute this this last Saturday in the video below =

x.com/ravagelaserbeak/status…

$SNDL @sndl_inc 🔥= $SNDL

Complete overnight rerate and MASSIVE **U.S.** WARRANT HOLDINGS CONVERT ON U.S. CANNABIS ENTERPRISE, via Sunstream Bancorp arm, on U.S. SOIL= UPON RESCHEDULING. DEBT FREE. EXCELLENT HISTORICAL EARNINGS. ER DATE APRIL 29th NEXT WEEK. LONG. 5 a share EASILY ON SCHEDULE 3 into 10 dollars plus a share. Then easily 30 a share plus. LONG.

$MSOS $CURLF $GBTIF $TLRY $CMPS $MNMD $BIB

1

2

5

1,043