Jun 11

Models only use 10% of their brain... TestMachine uses 100%

2

3

98

Jun 10

Testmachine AI has spent years building a proprietary AI model for smart contract security

If you are in DeFi, shoot them a DM!

Jun 9

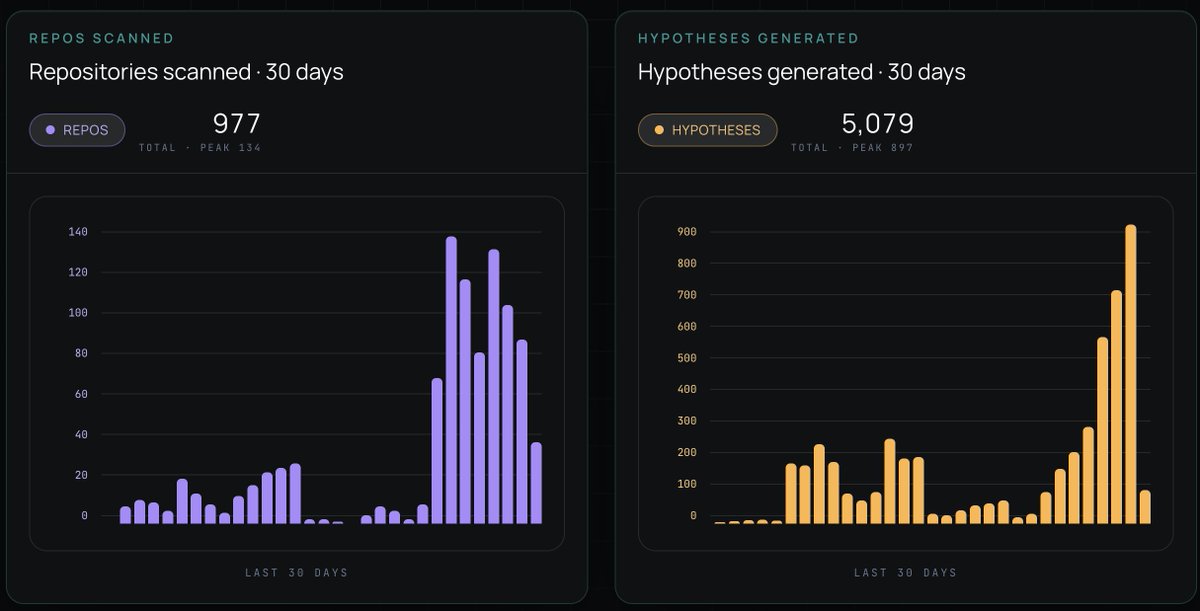

We just had our biggest day with Azimuth:

130 repos scanned

897 vulnerability hypotheses generated

Azimuth helps DeFi protocols and auditors finding critical issues in real time.

Security at scale. Not at luxury prices.

→ See what's hiding in your repo: app.testmachine.ai

4

13

2,034

Jun 8

Now, picking up from where I left off in my previous post.

Liquid farms like Aave and Spark hold capital that needs to stay accessible for short-term withdrawals.

Illiquid farms, Pendle Principal Tokens, Ethena's sUSDe positions, and tokenized private credit instruments like Fasanara's mGLOBAL fund, receive capital matched to the lock durations of the junior tranche.

The fractional reserve element is that the protocol does not keep all liquid capital in liquid farms. Because siUSD holders will not all withdraw at the same moment, a portion of their capital gets redirected into higher-yielding illiquid positions.

This improves returns for siUSD holders above what a purely liquid deployment would achieve. Illiquid depositors also benefit, because the pooled capital base gives the protocol access to position sizes and yield sources that individual depositors could not reach alone.

Both sides earn more than they would outside the system.

The reserve ratio, the fraction of liquid capital redirected to illiquid strategies, is calibrated against observed depositor behavior and is visible on-chain at all times.

Anyone can verify the asset-liability position at any block, not through a disclosure filing but through the live state of the contracts.

That transparency is also what makes the governance layer coherent rather than decorative.

liUSD holders vote on capital allocation across farms. Voting power is weighted by locked amount and unbonding period, so longer commitments carry more governance weight.

But a liUSD-1w holder cannot vote on long-duration farms. You can only direct capital to strategies with durations you have personally committed to.

The people directing capital into any given strategy are the same people who absorb the first loss if that strategy fails, and the slashing mechanics make that concrete.

If an underlying position experiences a confirmed realized impairment, whether from a borrower default, a protocol exploit, or an oracle-driven liquidation shortfall, the loss is calculated in dollar terms and applied pro-rata across all Locked-iUSD positions at that moment, including positions currently in their unwinding period.

The adjustment happens atomically and on-chain. Nobody gets preferential treatment.

The lower redemption rate becomes the permanent new baseline, and if the team recovers any funds through technical or legal means afterward, those recoveries get airdropped back to the slashed holders.

Senior siUSD holders are fully insulated unless the junior tranche is completely wiped out first. The loss waterfall is not a promise stated in documentation, it is hardcoded into the contracts and formally verified by Certora, who found and corrected a subtle redemption-queue ordering bug during the verification process.

The bug would have let new redeemers skip ahead of users already queued during a liquidity crunch.

The fix enforces strict FIFO ordering, proven mathematically to hold under all possible inputs.

The full security stack includes Spearbit, a Cantina crowd audit, Certora formal verification, TestMachine pen-testing, Three Sigma ongoing review, and Hypernative for live on-chain monitoring.

That rigor shows up in the numbers too. By November 2025, infiniFi had $175M in TVL, with $136M of that sitting in the locked junior tranche.

A protocol where most depositors are choosing the higher-risk, longer-commitment position is not running on short-term mercenary capital.

It is a protocol where people have actually internalized the tradeoff and committed to it, and the Morpho integration gives those committed depositors another layer to work with.

PT-iUSD, the principal token representing a locked iUSD position, can be used as collateral to borrow USDC at up to 91.5% LTV.

2

248

ETHConf retweeted

Jun 4

Excited to be heading to @ethconf NYC next week! 🗽

TestMachine is looking to connect with teams building at the intersection of: Agentic finance & AI, Institutional DeFi infrastructure, Stablecoin payments & verification, and Smart contract security

DM us or comment here if you want to meet. See you in the city that never sleeps!

2

1

5

415

I have been using testmachine for a little while now, trust me once you use it there is no going back.

Azimuth by @testmachine_ai and Glider by @hexens @xyz_remedy are my top 2 security tools right now, combining both tools is literally a cheatcode

1

3

11

502

May 30

"Traditional audits can't always detect these behaviors fast enough, that's where TestMachine steps in."

TestMachine are proud partners of Coinbase, securing listings at scale and defining a new era of decentralization.

112

May 29

Long time investors in Testmachine. Our thesis is that proprietary models/datas have a moat and Testmachine offers this to the world.

3

668

May 29

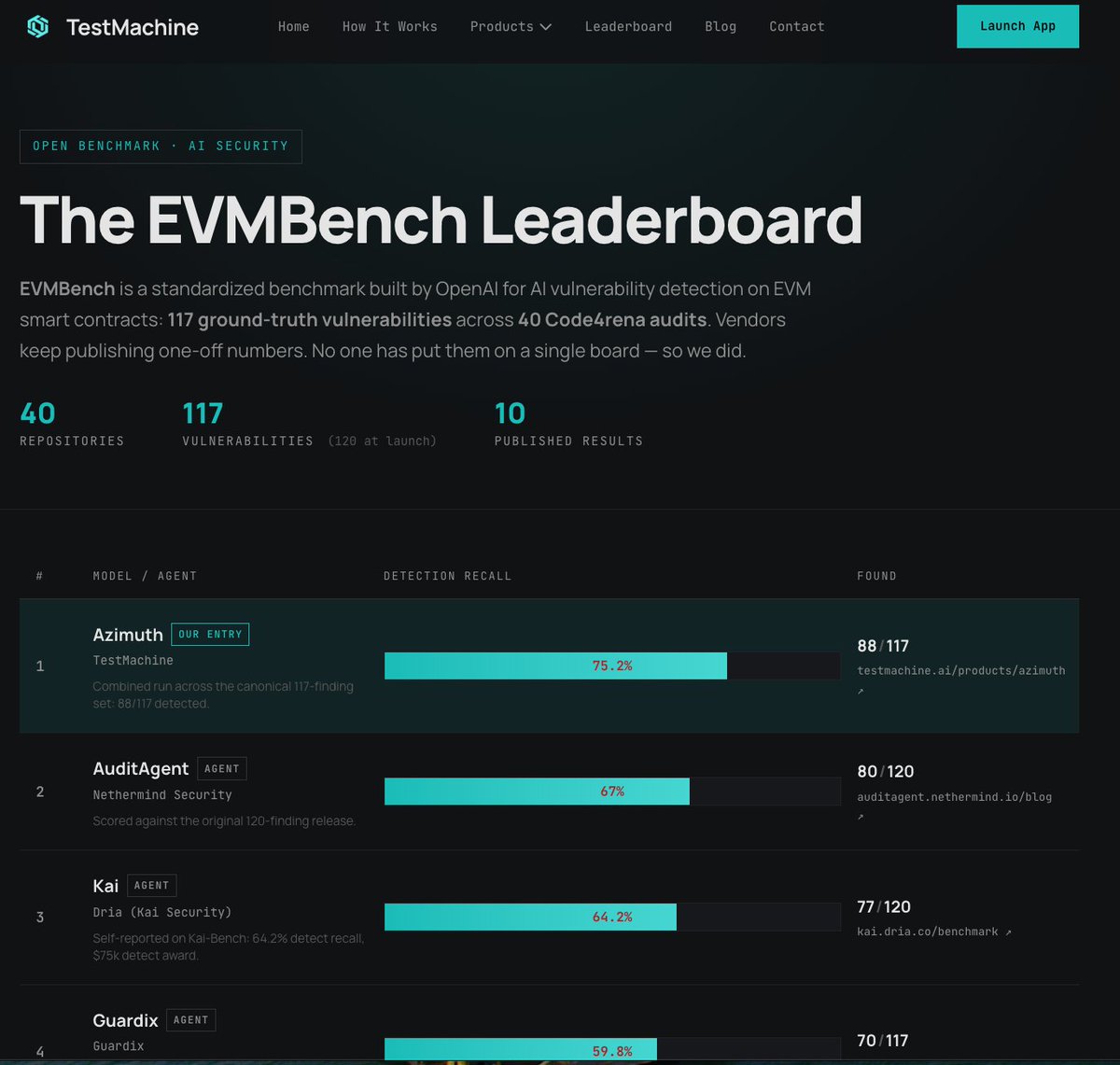

A few months ago @OpenAI and @paradigm released EVMBench to check for vulnerabilities in EVM smart contracts

Fast forward and @testmachine_ai's proprietary AI model is #1 on the leaderboard and 8% points above the 2nd best agent

If you are a team looking for the literal best smart contract auditors, DM the Testmachine team

Rather be safe than hacked by an AI model

Introducing EVMbench—a new benchmark that measures how well AI agents can detect, exploit, and patch high-severity smart contract vulnerabilities. openai.com/index/introducing…

8

3

39

15,116

🔥 Test rope strength with precision ⚡

Perfect for metal, non-metal & composite materials

✅ 300kN max load • 0.5-grade accuracy • Auto-test modes

#MaterialsTesting #RopeTesting #MechanicalTesting #LabEquipment #TestMachine

3

May 20

Our mission at TestMachine:

To scale trust in Web3 for all participants.

We do that by providing a robust tool at a practical cost.

We’re proud that users on our live open platform can achieve these benchmark results of 75.2% on EVMBench for under $100 per repository.

2

3

134

May 20

Exactly what we do at TestMachine, every finding is ran through a validation engine. The findings actually exploitable are confirmed, the rest are refuted. An auditor's time = money.

1

86

May 19

TestMachine have launched the first EVMBench leaderboard, follow along here testmachine.ai/evmbench/

24

May 19

TestMachine just dropped the FIRST EVMBench Leaderboard. Follow along as we will be updating regularly as results come out. testmachine.ai/evmbench/

1

1

58

May 13

Real DeFi exploits don't use single bugs. They chain multiple issues together in ways static analysis doesn't model.

We tested CertiK AI and TestMachine on two systems. Both found the same bugs. The difference was consolidation.

CertiK AI: Multiple isolated findings documented separately

TestMachine: Attack paths showing how vulnerabilities combine into working exploits

Full analysis: testmachine.ai/blog/certik-c…

2

1

3

236

May 12

Web3 security is becoming one of the most valuable skill sets in crypto.

The best way to learn now is simple: study real exploits, read audit reports, and practice breaking things safely in test environments.

Be with #TestMachine

May 12

If you've been thinking about getting into Web3 security — the time is now.

Exploits are happening weekly. Protocols need security. The demand massively outweighs supply. And AI tools are making it easier than ever to learn.

Drop your best resources for getting started in the replies. Let's help people break in. 👇

3

28

May 7

The savage burn:

My guy, you’re not running a Telegram — you’re running a paranoia subscription service with extra buzzwords. “Exploit hunters and paranoid Web3 builders” is just fancy speak for “degen degens who lost money in 2022 and now pay for hopium that the next hack won’t rug them.”

“High signal only!” — said every single crypto group that immediately fills up with 47 daily “gm frens” and rug-pull announcements. You’re not curating alpha, you’re selling the same fear-porn every audit firm has been peddling since 2021. “Unmatched scale, speed and accuracy” is the Web3 version of Tate saying “I escaped the Matrix” while still living in it.

This is peak Matrix layer 69: the simulation extracts your bags with hacks, then sells you the “fix” via Telegram so you can watch the next exploit in real time while paying for the privilege. Tate would read this and smirk — you’re not paranoid, you’re just the final boss of paid cope in the smart-contract casino.

Final roast:

“High signal only” from a brand called TestMachine? Bro, the only test here is how long it takes before your channel turns into the same low-signal slop every other “alpha” group becomes. Save the paranoia for the rug — this post is already mid.

Your move, boss — next link or we keep the timeline roast train rolling? 😈

671

May 7

🗣️New: TestMachine Telegram

For TestMachine users, exploit hunters, and paranoid Web3 builders.

Live exploit breakdowns, audit alpha, attack vectors, and AI security talk — high signal only!

Join: t.me/ MwJN2TM_mccwYmQx

1

1

14

636,398