and no, virtualizing, isolating and sandboxing everything isn't a solution

I wish Satya Nadella realizes this soon cause I'm finished and tired of all this shit

11

So what we know now is that given an anonymizing, virtualizing environs across wires and wireless, humans will choose to create corporations and creatures of imagination rather than sit with the realities in front of their faces and do what is necessary to confront them.

1

3

36

Jun 10

Do they want to youth to lead the fight with empty hands.?

They should permit men to arm themselves and we will gladly do so and the banditry industry will end immediately

Fulani hardsmen are afraid of confrontation, if they found out that a community is well armed and prepared you will never see them around that area

I'm already virtualizing how my Sethima 🔫🔫 go be

14

Jun 10

thats why they win. because they're not virtualizing backcompat and aren't trying to run Windows and the multiple store front.

LMAO. your precious Xbox Mode only saves 2GB of RAM.🤣😭

1

2

146

Jun 7

Federer is arguably the strongest possible case to make for the Aristotelian point, because he’s supposed to be the least banausic athlete, rather the elegant craftsman - effortless, graceful, and balletic artistry. The anti-Nadal. The gold standard for not looking like a tool of one’s occupation. Life is bigger than the court.

Tennis is kinetic chain mastery. To hit a ball, you must activate every physical stem at once: [Legs: Lower-Body Power] > [Core: Rotational Torque] > [Upper Body: Kinetic Release]. Hormesis: Federer’s forehand got bigger not despite the load but because of it. Antifragility in action.

De-virtualizing mastery: local antifragility is purchased with fragility or dormancy elsewhere. Federer has certainly lived a life full of leisure. The specialization neither marks him nor makes him incapable of doing anything outside itself. Abiding love of the game and the desire to demand more of oneself.

For Aristotle, the banausos is not just physically deformed by his profession, but politically and ethically stunted: specialization makes him less a complete man than a TOOL of his occupation.

Politics, book VII:

"And any occupation, art, or science, which makes the body or soul or mind of the freeman less fit for the practice or exercise of virtue, is vulgar; wherefore we call those arts vulgar which tend to DEFORM the body, and likewise all paid employments, for they absorb and degrade the mind."

2

149

Jun 4

Progress

Science is automating and virtualizing. This means much of the progress we need in the world is going to come from automated labs and simulations. We don’t know the full computational limits of virtualization, but such robotically-driven labs for biology, materials science, and more are going to remove a large number of the bottlenecks, and along the way they will push the limits of validated virtualization to increase sample efficiency and the net returns to reification. Basically in every area we will have some combination of neural models, explicit simulations, and real world experiments all contributing to improving the returns per dollar and per time in areas like biology, materials science, and the like.

1

18

585

May 28

The Android experiment was cool. It really pushed hardware, and forced, alongside it, optimization of the JVM and drove whole new implementations of runtime caching, billions of dollars in the name of progress.

Now that the market has proved it out, and the hardware is far better, can we stop virtualizing everything in a JVM

Imagine the perf boosts.

Some things are truly better off in a JVM, the suspend and functionality is, actually kinda perfect for how mobile apps are intended to be used.

But just imagine a world where your keyboard didn't have to be garbage collected...

Oh right, ios. Don't have to imagine it.

May 27

Google looked at weak mobile hardware 20 years ago and seriously said "yep, they gonna run Java and nothing but Java" and it took them almost 2 years to realize how wrong it is

1

5

955

We frequently posit Bitcoin is the work of John Nash virtualizing Gödel sentences through bit-strings.

fermatslibrary.com/p/a00aced…

1

4

63

May 23

some of the efficiency is going to be the same tricks the smart web devs use like virtualizing and windowing the list view for a long list.

1

3

124

May 19

BTW, there's no mystery in how we are provisioning compute environments, all the code is in github.com/tuist/tuist

We are provisioning bare-metal Macs and virtualizing them from @Scaleway. Working with them is such a joy.

1

3

370

May 17

They can ply us with their entertainment products. It's the Curtis Yarvin plan to ethically euthanize the masses by "virtualizing" them.

Then those masses become part of the top 10%'s experiments to better the AI technology that will sustain them (and slowly kill us).

2

10

293

May 15

This is super cool! Love seeing optimized software. What’s the initial loading time like? Seems like you guys did an awesome job virtualizing the diffs

1

2

1,092

May 14

In the past few weeks, we rolled up our sleeves and prepared Tuist for the infrastructure scaling that's ahead of us:

1️⃣ We moved all our production workload off Render.com into a Tuist-managed k8s cluster that runs in Hetzner. This means better cost control, and an interface that coding agents speak natively.

2️⃣ We developed a new caching technology, Kura (which in Japanese means storehouse), to move us to per-tenant caching meshes, and reconciled it into our k8s cluster and the product, so customers can choose where to deploy their caching nodes. We do the rest! This technology already supports #Bazel and other build systems, and it prepares us to jump in.

3️⃣ We brought macOS compute into the k8s cluster, virtualizing the environments using Tart. The first product upon that capability will be CI runners (already working on the user-facing piece of this). And we'll continue with remote execution and agentic workflows that mimic the workflows a platform team would do (e.g., fixing a flaky test)

With macOS & Linux compute and Bazel, we are becoming the cross-toolchain platform team, and we'll look into how to productize caching beyond build systems, but more about this in a future post ;)

1

8

608

May 14

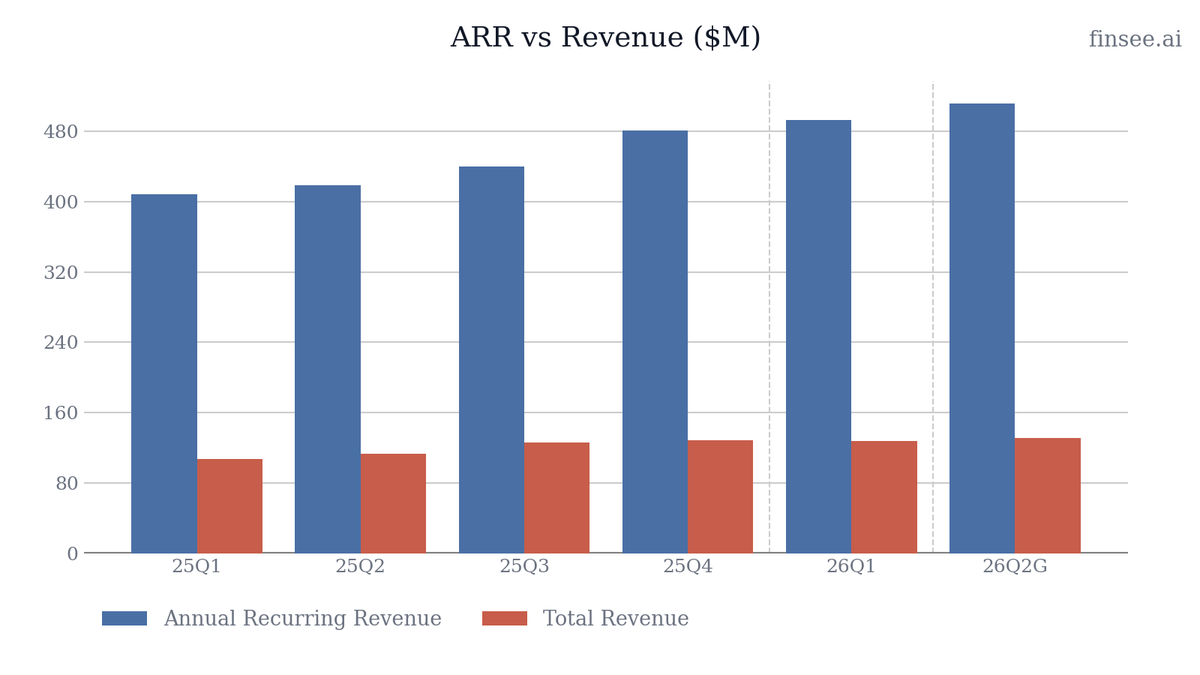

$CLBT Q1 2026 earnings: Solid ARR Growth and Strategic Expansion Unlocks 2026 Momentum

Cellebrite delivered a solid Q1, matching its 'prudent' guidance philosophy with 21% YoY ARR growth and robust 32% TTM Free Cash Flow margins. The strategic pieces for a massive 2026 are falling into place: the US Department of Justice-sponsored FedRAMP High Authorization was achieved, unlocking pent-up federal budgets, and the SCG Canada drone acquisition closed. However, profitability took a sequential step back, with Adjusted EBITDA margins dipping to 23.9% (from near 30% in late 2025). The Q2 guidance signals ARR growth acceleration, but implies continued near-term margin compression before a heavily weighted second half.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐅𝐞𝐝𝐑𝐀𝐌𝐏 𝐇𝐢𝐠𝐡 𝐀𝐮𝐭𝐡𝐨𝐫𝐢𝐳𝐚𝐭𝐢𝐨𝐧 𝐀𝐜𝐡𝐢𝐞𝐯𝐞𝐝 — The DOJ officially sponsored Cellebrite Government Cloud for FedRAMP High. This removes a major procurement roadblock and paves the way to tap into previously delayed U. S. Federal spending.

• 𝐀𝐑𝐑 𝐆𝐫𝐨𝐰𝐭𝐡 𝐑𝐞𝐚𝐜𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐧𝐠 — Total ARR grew 21% YoY in Q1, and Q2 guidance projects 22-23% YoY growth. This proves the core demand environment remains highly resilient despite earlier federal lumpiness.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐇𝟏 𝐌𝐚𝐫𝐠𝐢𝐧 𝐂𝐨𝐦𝐩𝐫𝐞𝐬𝐬𝐢𝐨𝐧 — Adjusted EBITDA margins reversed from nearly 30% in H2 2025 down to 23.9% in Q1. Q2 guidance implies further sequential compression to 22.5% at the midpoint, reflecting acquisition integration costs and FX headwinds.

• 𝐍𝐑𝐑 𝐌𝐨𝐝𝐞𝐫𝐚𝐭𝐢𝐨𝐧 — The recurring revenue dollar-based net retention rate decelerated to 115%, down from 116% in 25Q4 and 121% a year ago, suggesting upsell velocity may be slowing slightly.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: 🟢

Bullish. The top-line momentum (ARR) is accelerating, and the federal spending floodgates are primed to open with FedRAMP High status. The margin dip appears to be a mix of typical H1 seasonality and M&A integration, rather than a structural flaw.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢🟢 𝐅𝐞𝐝𝐑𝐀𝐌𝐏 𝐇𝐢𝐠𝐡 𝐂𝐚𝐭𝐚𝐥𝐲𝐬𝐭 𝐔𝐧𝐥𝐨𝐜𝐤𝐞𝐝 [NEW]

The long-awaited FedRAMP High Authorization was achieved with the U. S. Department of Justice acting as the authorizing agency. This milestone confirms that Cellebrite Government Cloud meets the most stringent federal security requirements. After a choppy 2025 federal spending environment, this authorization serves as the primary mechanism to unlock petabytes of data opportunity across government-wide adoptions.

🟢 𝐂𝐞𝐥𝐥𝐞𝐛𝐫𝐢𝐭𝐞 𝐆𝐞𝐧𝐞𝐬𝐢𝐬 𝐀𝐈 𝐄𝐧𝐭𝐞𝐫𝐬 𝐁𝐞𝐭𝐚 [NEW]

Innovation is accelerating with the introduction of 'Cellebrite Genesis,' a purpose-built agentic AI product. It uses conversation-like experiences to analyze mobile extractions, call records, and multimedia. This transforms raw data into actionable insights for complex cases (human trafficking, narcotics). If successfully monetized, this creates an entirely new upsell vector within the existing software stack.

🟢 𝐓𝐀𝐌 𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧 𝐯𝐢𝐚 𝐃𝐫𝐨𝐧𝐞 𝐅𝐨𝐫𝐞𝐧𝐬𝐢𝐜𝐬

The acquisition of SCG Canada officially closed on March 1, 2026. This expands Cellebrite's reach into UAVs (drones)—an emerging category seeing robust global growth. SCG provides rapid extraction from over 80 common UAVs at the point of collection, giving law enforcement and defense intelligence a critical new data source.

🔴 𝐇𝟏 𝐏𝐫𝐨𝐟𝐢𝐭𝐚𝐛𝐢𝐥𝐢𝐭𝐲 𝐌𝐚𝐫𝐠𝐢𝐧𝐬 𝐑𝐞𝐯𝐞𝐫𝐬𝐢𝐧𝐠

Despite top-line strength, Adjusted EBITDA margins are decelerating significantly compared to the back half of 2025. After peaking at 29.9% in 25Q3 and 29.8% in 25Q4, margins fell to 23.9% in 26Q1 and are guided down to 22.5% in 26Q2. Management previously cited the absorption of Corellium and FX headwinds, but this places immense execution pressure on the second half of 2026 to hit the 26-27% full-year margin target.

🔴 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐆𝐫𝐨𝐰𝐭𝐡 𝐓𝐫𝐚𝐢𝐥𝐢𝐧𝐠 𝐀𝐑𝐑 𝐆𝐫𝐨𝐰𝐭𝐡

A notable divergence is occurring between forward-looking ARR and recognized revenue. While Q2 ARR guidance implies an accelerating 22.5% YoY growth, total revenue guidance implies decelerating 16% YoY growth. This transition dynamics, typical of SaaS shifts, requires monitoring as the mix heavily tilts away from upfront term licenses.

⚪ 𝐂𝐨𝐫𝐞𝐥𝐥𝐢𝐮𝐦 𝐔𝐧𝐥𝐨𝐜𝐤𝐢𝐧𝐠 𝐀𝐮𝐭𝐨𝐦𝐨𝐭𝐢𝐯𝐞 𝐔𝐬𝐞 𝐂𝐚𝐬𝐞𝐬

Beyond defense and intelligence, Corellium (acquired late 2025) is gaining traction with automotive manufacturers. By virtualizing Arm-based systems at the hardware level, automotive software teams can recreate and test vehicle environments (infotainment, autonomous driving) in the cloud. This provides Cellebrite with a rare enterprise foothold outside of traditional public safety.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐓𝐫𝐚𝐢𝐥𝐢𝐧𝐠 𝐓𝐰𝐞𝐥𝐯𝐞 𝐌𝐨𝐧𝐭𝐡𝐬 𝐅𝐫𝐞𝐞 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰 (𝟐𝟔𝐐𝟏): $158.6 million

Stable. The TTM FCF margin sits at a highly lucrative 32.0%. Q1 operating cash flow was $19.9M, funding $3.0M in CapEx to yield $16.8M in quarterly free cash flow. This liquidity fully supports the company's aggressive M&A playbook without requiring external financing.

𝐑𝐞𝐜𝐮𝐫𝐫𝐢𝐧𝐠 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐃𝐨𝐥𝐥𝐚𝐫-𝐁𝐚𝐬𝐞𝐝 𝐍𝐞𝐭 𝐑𝐞𝐭𝐞𝐧𝐭𝐢𝐨𝐧 𝐑𝐚𝐭𝐞 (𝐍𝐑𝐑): 115%

Decelerating. Down from 116% in 25Q4 and 121% in 25Q1. While 115% remains healthy for public sector software, the gradual sequential slide highlights the necessity of new product launches (like Guardian Investigate and Genesis AI) to stimulate deeper cross-selling and upsells within the existing base.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐐𝟐 𝟐𝟎𝟐𝟔 𝐀𝐧𝐧𝐮𝐚𝐥 𝐑𝐞𝐜𝐮𝐫𝐫𝐢𝐧𝐠 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 (𝐀𝐑𝐑): $510 - $513 million

Accelerating. The midpoint of $511.5M represents 22.5% YoY growth, an acceleration from Q1's 21%. Management notes that this reflects sequential stability as they gear up to monetize the influx of newly launched products.

𝐐𝟐 𝟐𝟎𝟐𝟔 𝐓𝐨𝐭𝐚𝐥 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $130 - $133 million

Decelerating. The midpoint of $131.5M implies approximately 16% YoY growth, stepping down from the 19% YoY growth delivered in Q1. The lag between ARR growth and revenue growth reflects the ongoing mix shift toward ratable SaaS contracts.

𝐐𝟐 𝟐𝟎𝟐𝟔 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐁𝐈𝐓𝐃𝐀: $29 - $31 million (22-23% margin)

Decelerating. Margins are guided lower sequentially from Q1's 23.9%. This reflects upfront investments in go-to-market for the Spring release cycle and the integration costs of SCG Canada.

𝐅𝐘 𝟐𝟎𝟐𝟔 𝐀𝐧𝐧𝐮𝐚𝐥 𝐑𝐞𝐜𝐮𝐫𝐫𝐢𝐧𝐠 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 (𝐀𝐑𝐑): $567 - $573 million

Stable. The full-year outlook is maintained, implying 18-19% YoY growth. With Q1 outperforming and Q2 accelerating, this full-year guide currently looks highly conservative.

𝐅𝐘 𝟐𝟎𝟐𝟔 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐁𝐈𝐓𝐃𝐀: $149 - $155 million (26-27% margin)

Reversing. Because H1 2026 margins are hovering in the 22-24% range, achieving the full-year target of 26-27% requires a massive profitability ramp in the second half of the year, echoing typical seasonal patterns where ~60% of EBITDA is generated in H2.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐇𝟐 𝐌𝐚𝐫𝐠𝐢𝐧 𝐁𝐫𝐢𝐝𝐠𝐞

With Q1 Adjusted EBITDA margins at 23.9% and Q2 guided to 22.5%, achieving the full-year 26-27% target requires significant H2 leverage. What specific catalysts or expense roll-offs give you confidence in that back-half profitability ramp?

𝐀𝐠𝐞𝐧𝐭𝐢𝐜 𝐀𝐈 𝐌𝐨𝐧𝐞𝐭𝐢𝐳𝐚𝐭𝐢𝐨𝐧

Cellebrite Genesis is currently in beta testing. Does the maintained 2026 guidance framework continue to assume zero revenue contribution from these new AI features, and when do you expect them to become a material driver of NRR?

𝐅𝐞𝐝𝐑𝐀𝐌𝐏 𝐓𝐢𝐦𝐞𝐥𝐢𝐧𝐞 𝐭𝐨 𝐀𝐑𝐑

Now that FedRAMP High Authorization is secured, how long is the typical sales cycle to convert this clearance into actual contracted ARR from federal agencies?

7

696

May 13

Not to mention the login info for all my homelab stack is in there too, so if I can't access it to get into my homelab, how can I troubleshoot it being down? lol

It's the same chicken and egg thin as virtualizing a firewall.

1

5

297

May 13

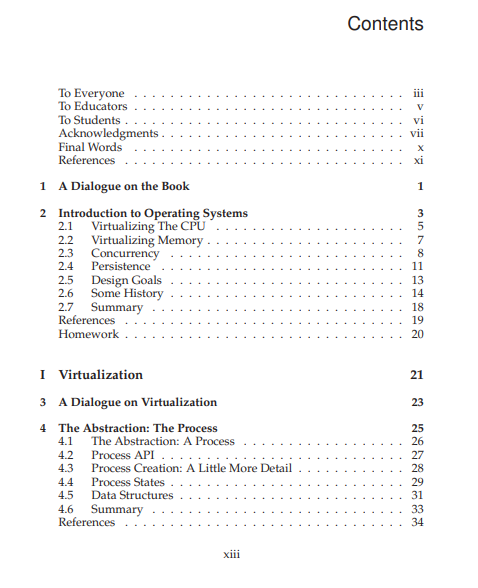

two professors at Wisconsin spent 25 years teaching operating systems together

then they wrote a 714 page textbook about "Operating Systems: Three Easy Pieces"

it covers virtualizing the CPU virtualizing memory concurrency persistence security and file systems

small enough to read in parts and also it is written like a conversation not a typical textbook

this is what you read if you want to really understand how operating systems work not just the theory

15

173

1,136

46,928

May 12

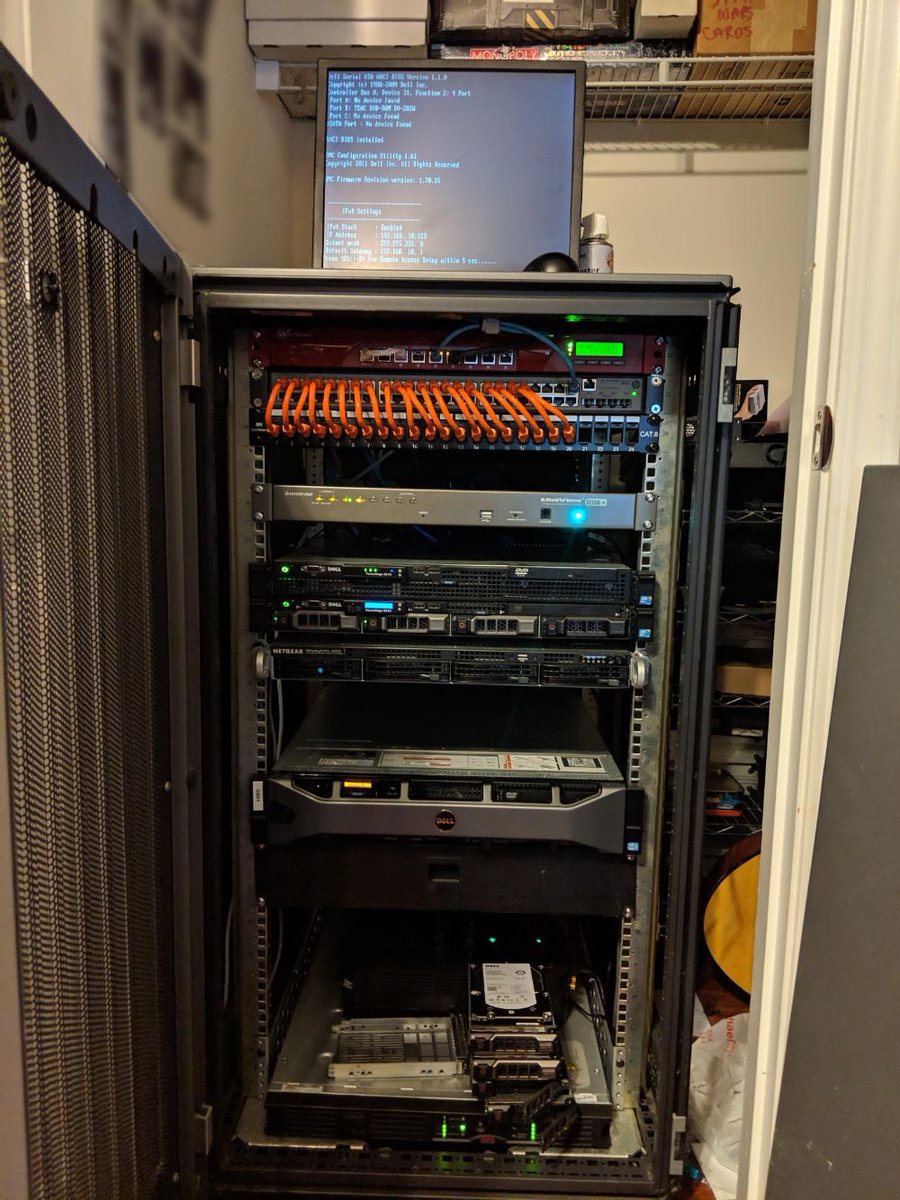

Every “Home Lab” guy is exactly 6 months away from this exact psychological breakdown:

1. Buys a Raspberry Pi to run Pi hole. Blocks 3 ads. Feels like a networking god.

2. Discovers Docker. Spins up Jellyfin. “Why would anyone pay for Netflix?”

3. SD card gets corrupted. Panic buys a decommissioned Dell PowerEdge off eBay. It sounds like a 747 taking off.

4. Wife threatens divorce over the server noise. Migrates the rack to the uninsulated garage.

5. Installs Proxmox. Spends a 3 day holiday weekend virtualizing the home router. The house has no Wi-Fi. Family is furious.

6. Discovers Kubernetes. Deploys a 3 node K3s high availability cluster just to orchestrate the kitchen smart bulbs.

7. The power bill is now $480/month. He has spent $4,200 to avoid a $12 Spotify subscription.

8. Currently writing custom Ansible playbooks just to turn on the living room TV.

2

30

1,826

May 11

𝗡𝗲𝘄 𝗼𝗻 𝘁𝗵𝗲 @CrusoeAI 𝗘𝗻𝗴𝗶𝗻𝗲𝗲𝗿𝗶𝗻𝗴 𝗯𝗹𝗼𝗴: V𝘪𝘳𝘵𝘶𝘢𝘭𝘪𝘻𝘪𝘯𝘨 𝘈𝘔𝘋 𝘐𝘯𝘴𝘵𝘪𝘯𝘤𝘵𝘛𝘔 𝘔𝘐355𝘟 𝘎𝘗𝘜𝘴 𝘸𝘪𝘵𝘩 𝘵𝘩𝘦 𝘈𝘔𝘋 𝘗𝘦𝘯𝘴𝘢𝘯𝘥𝘰𝘛𝘔 𝘗𝘰𝘭𝘭𝘢𝘳𝘢 400 𝘈𝘐 𝘕𝘐𝘊 𝘰𝘯 𝘓𝘪𝘯𝘶𝘹 𝘒𝘝𝘔.

Our engineers cover VFIO passthrough, SR-IOV networking, RoCE setup, and the RCCL issues they debugged along the way.

Read the full walkthrough → lnkd.in/g98ie_kc

1

3

119