Jun 15

🚨 نفّذت شركة ريبل برامج تجريبية مع البنك المركزي السعودي (ساما) لاختبار المدفوعات العابرة للحدود القائمة على تقنية البلوك تشين باستخدام برمجياتها المؤسسية. ويتيح هذا البرنامج التجريبي، الذي انطلق في الأصل باستخدام تقنية xCurrent من ريبل، للبنوك السعودية المشاركة معالجة وتسوية المعاملات الدولية بشكل فوري.

#XRP

2

11

94

5,239

Jun 11

Yep. Many, many people did not understand that small, yet very important nuance of xRapid vs xCurrent vs XRP

2

56

Ripple has joined the AWS Partner Network. aws.amazon.com

AWS maintains an official partner profile and case study page for Ripple, highlighting RippleNet (its decentralized global payments network) and related products like xCurrent, xRapid (which uses XRP for on-demand liquidity), and xVia. aws.amazon.com

Key Details

• Announcement/Timing: Ripple was officially listed as a verified AWS partner around November 2025. This allows financial institutions, banks, payment providers, and others already using AWS to more easily discover, deploy, and integrate Ripple’s solutions for real-time cross-border payments, settlement, and liquidity. @news

• What it means: Ripple’s technology runs on or integrates with AWS infrastructure, making it available in the AWS ecosystem (e.g., via AWS Marketplace or cloud deployments). It does not mean Amazon.com (the retail side) uses XRP for payments, nor a direct integration of AWS into the XRP Ledger itself. thecoinrepublic.com

• Additional Context: Ripple uses AWS for various internal operations (e.g., data platforms, AI experiments with Amazon Bedrock for XRPL analysis, and custody solutions with AWS CloudHSM). There have also been collaborations on public blockchain datasets for XRP Ledger analysis on AWS. coingape.com

This partnership positions Ripple’s blockchain-based payment tools more prominently within AWS’s fintech and blockchain offerings. For the latest official details, check the AWS partner page directly.

1

79

Jun 9

🗺️ ¿TIENE FUTURO REAL $XRP O ESTAMOS ANTE UN ACTIVO ZOMBI? Abro debate. 👇

Sé que la comunidad de XRP es enorme y apasionada, pero bajo mi punto de vista técnico y de estrategia macro, considero muy probable que el proyecto no logre cumplir con las enormes expectativas de precio que muchos esperan. A pesar de contar ya con total claridad regulatoria en este 2026 y de tener sus propios ETFs en el mercado, el precio sigue demostrando una debilidad estructural notable si lo comparamos con el resto del mercado.

Aquí comparto mis motivos fundamentados de por qué considero que es un proyecto con un futuro muy comprometido:

1️⃣ Utilidad de la red ≠ Captura de valor del token (El humo de las asociaciones):

Muchos confunden el éxito del software de Ripple con la revalorización de XRP. Los bancos pueden implementar sus sistemas para pagos transfronterizos sin necesidad de adquirir o mantener el token en sus balances a largo plazo. De hecho, la gran mayoría de esos "anuncios de asociaciones bancarias" históricos han sido simples proyectos piloto o pruebas de concepto usando su red de mensajería (como xCurrent), no el propio activo. Confundir marketing con adopción real en el balance de los bancos es el primer gran error.

2️⃣ La obsolescencia frente a las CBDC y el sistema Swift:

La narrativa de XRP como el "token puente" interbancario choca con la realidad actual. Los bancos centrales están desarrollando sus propias redes cerradas de CBDC (Euro/Dólar digital) utilizando tecnologías blockchain empresariales propias y de código abierto, apoyándose además en la actualización del sistema Swift (ISO 20022). Ningún gobierno ni entidad financiera global va a externalizar su liquidez transfronteriza en un activo volátil de una empresa privada pudiendo controlar y programar su propia infraestructura soberana.

3️⃣ Inflación constante por diseño (Escrows) y centralización:

A diferencia de los activos descentralizados que nacen de la competencia minera y la escasez real, XRP fue 100% pre-minado. La enorme concentración de la oferta en manos de una entidad corporativa rompe por completo la dinámica natural del mercado. Además, el sistema automatizado de liberación mensual de 1.000 millones de tokens desde sus contratos de custodia (escrows) somete al precio a una dilución constante. Mientras el minorista holdea con fe, el mercado absorbe una oferta recurrente que actúa como un ancla perpetua, convirtiendo al inversor común en la liquidez de salida de la tesorería de la empresa.

4️⃣ Un ecosistema zombi sin innovación (Coste de oportunidad):

El valor real de una red a largo plazo está en sus desarrolladores y en su actividad interna. Si miramos el TVL (Valor Total Bloqueado) y la innovación en Smart Contracts o aplicaciones descentralizadas (DApps) del XRP Ledger frente a ecosistemas como Ethereum, Solana o segundas capas, la diferencia es abismal. Es una red infrautilizada. Mientras otros activos capturan valor de forma orgánica gracias a las finanzas descentralizadas reales, holdear XRP ha significado estancar el capital y asumir un coste de oportunidad brutal durante ciclos enteros.

Las narrativas, el marketing y las comunidades grandes sostienen expectativas de forma temporal, pero a largo plazo, la economía real, la tecnología y los flujos institucionales verdaderos son los que imponen la realidad en los gráficos.

¿Cómo veis el futuro de XRP a largo plazo? ¿Creéis que logrará romper esta estructura de estancamiento o se confirmará como un activo zombi? Los leo en comentarios. ♟️💬

#XRP #Ripple #Crypto #Trading #Altcoins #AnálisisTécnico

14

3

22

4,589

Jun 9

公式ソース😘

1. AWS公式 Rippleパートナーページ

aws.amazon.com/partners/succ…

(RippleNet、xCurrent、xRapid(XRP明記)、xViaの説明が掲載)

2. SBI Remit 累計2.5兆円突破 公式発表

sbigroup.co.jp/news/2026/052…

(2026年5月29日発表 / 5月27日突破)

SBI Remit公式関連ページ

remit.co.jp/kaigaisoukin/inf…

3. SBI Remit × Ripple ODL開始 公式

ripple.com/ripple-press/ripp…

(2021年7月 日本初ODL開始)

Ripple顧客事例ページ

ripple.com/customer-case-stu…

7

183

May 27

Rippleの商標戦略とは?🤔

Rippleは昔から、

商標をかなり重視してきました。

例えば👇

✅2013年:XRP商標取得

✅2015年:Triskelionロゴ登録

✅2017年〜:xCurrent、xRapidなど保護

✅2024〜2026年:RLUSD、Ripple Custody、Ripple Primeなど拡張

つまり今回の申請は、

👉今まで積み上げてきた戦略の“集大成”

とも言える動きなんです。

1

6

140

May 20

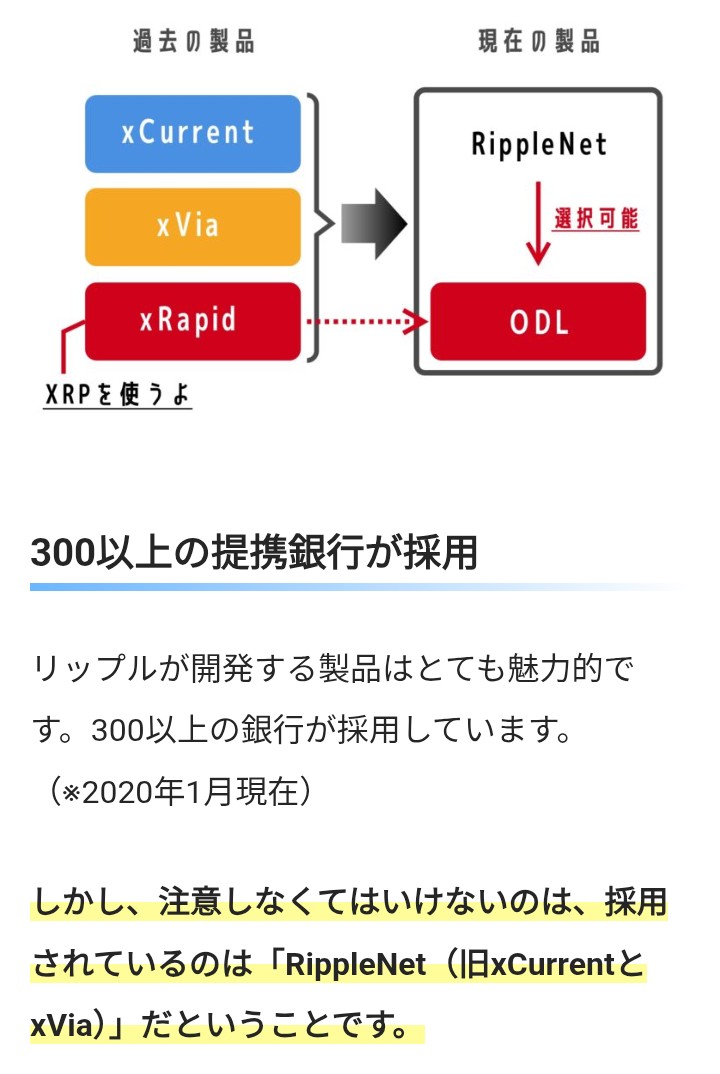

In the past, Ripple separated its enterprise offerings into three main products: xCurrent, xVia, and xRapid (which did use XRP). However, Ripple consolidated these separate platforms into a unified offering originally called RippleNet.

During the Ripple Swell conference, the network was rebranded simply as Ripple Payments. While the underlying technology of xCurrent remains operational, it has been absorbed into this broader, all-encompassing infrastructure product.

1

1

2

867

May 11

☯️ [2026년 XRP 도미넌스로 유추한 20%의 회귀와 그 가치]

현재 XRP는 전체 암호화폐 시장의 약 3.3%를 차지하고 있습니다. 만약 과거 영광의 시대였던 도미넌스 20%대로 회귀한다면 그 가격은 얼마가 될까요? 단순히 과거의 반복이 아닌, 2026년 현재 팽창된 크립토 산업 구조를 투영해 본다면 우리는 더욱 담대한 숫자를 마주하게 됩니다.

📊 [도미넌스 20% 시나리오 분석]

현재 전체 시장 파이($2.7T) 기준, 도미넌스 20% 탈환 시 XRP의 적정 가격은 약 $9.15를 가리킵니다. 하지만 제도권 자본이 본격 유입되는 2026년 하반기, 전체 시총이 $5T 규모로 팽창한다면 XRP 20%의 가치는 개당 $16~$18 수준까지 도약하는 산술적 계산이 나옵니다.

1️⃣ 과거의 복기: 2015 & 2017년의 영광

- 2015년: SBI 파트너십 등 금융권 협업의 태동과 함께 시장의 주목을 시작한 시기.

- 2017년: xCurrent 도입 기관 100곳 돌파, 기대감만으로 도미넌스 25%를 점유하며 비트코인의 유일한 대항마로 우뚝 섰던 시절.

2️⃣ 현재의 기술적 관점: 초장기 채널 지지와 돌파

10년 주기 초장기 상승 채널의 하단 생명선을 지켜낸 것은 역사적 필연입니다. 다년간의 하락 추세선을 뚫어낸 지금의 흐름은 전형적인 임펄스 3파의 서막입니다. 2파 리테스트를 마치고 이제 막 채널 상단을 향해 가속도를 붙이고 있습니다.

3️⃣ 이번엔 '실체'가 다르다: RWA & Clarity 법안

과거가 단순한 '기대감'이었다면, 이번 사이클의 엔진은 제도권 그 자체입니다.

- RWA (실물자산 토큰화): XRPL 인프라 위로 쏟아질 거대 기관 자본의 흐름.

- 클레어리티(Clarity) 법안: 규제의 안개를 걷어내고 기관 자금 유입의 고속도로를 깐 법적 명확성.

💡 차트의 기술적 경로와 매크로 호재가 완벽하게 맞물리는 역사적 변곡점입니다. 10년 주기 채널의 상단을 향한 2026년의 위대한 여정, 우리는 지금 그 출발선에 서 있습니다. 🚀

#XRP #XRP도미넌스 #Crypto2026

1

2

29

2,256

楽天ウォレットの松田様(@RW_matsuda)より、

・楽天キャッシュとは?

・なぜ楽天キャッシュなのか?

・あまり知られていないサービスの強み

・税金について

など、現状のサービスについて詳しいお話を聞くことができたと思います。

金商法(改正案)についても要チェックですね!

また、xCurrent, xRapid (ODL)といったワードが少し出て懐かしい気持ちになりました💱🏦

May 7

特別配信:楽天ウォレット|XRP上場記念! x.com/i/broadcasts/1wxWjaOPv…

3

15

1,353

Apr 10

🤣🤣🤣 10 Minuten hmm Xcurrent 4.0 ?🤫🤐 Ach nö es heißt ja SWIFT GPI aber haben noch keinen Namen für ihre Blockchain und ihren Ledger.🙈😉

Apr 10

How long do cross-border payments really take?

Today, 75% of payments on Swift reach beneficiary banks within just 10 minutes – with many arriving in seconds.

We’re building on that progress. Our payments scheme is raising the standard on today’s rails – faster, more predictable, more transparent.

At the same time, our blockchain-based shared ledger is unlocking the next phase. Enabling digital finance at global scale.

👉 Want to learn more?swift.com/payments/payment-i…

#Innovation #Payments

1

3

22

1,275

Apr 3

1. Moron, it's not "law" that XRP isn't a security, either. It's one judge's interpretation of the Howey test being applied to XRP.

The entire purpose of the Clarity Act is replace the Howey Test with it.

LINK is as much a commodity as XRP via the SEC/CFTC specifically naming it in their statement. XRP has no more of a standing than LINK.

2. An ICO isn't proof whether or not a digital asset is a security. See Ethereum.

3. Who cares if Ripple didn't have an official ICO? They relentlessly dumped on retail, while doing 100X worse things.

Let's take a trip down memory lane about what they did:

- "Large-scale unregistered public distribution of XRP and—with the goal of immense profits—simply assumed the risk that they were violating the federal securities laws."

- "In a December 2017 interview with Bloomberg Garlinghouse stated 'I’m long XRP, I’m very, very long XRP as a percentage of my personal . . . balance sheet' (though he had already sold at least 67 million XRP)"

- Garlinghouse "instructed certain Ripple employees to 'proactively' attempt to increase speculative trading value with positive XRP news", employed "supply limiting tactics", and "approved the buy back option" to increase XRP price.

- "Ripple actively sought to offer and sell XRP widely as possible.....for an imagined, future use case"

- "December 2017, Garlinghouse explained that XRP’s price had risen because Ripple was 'solving a real problem . . . a multi-trillion dollar problem around cross-border payments'"

- Through 2016 to 2019, Ripple began selling two software suites, xCurrent and xVia "neither uses XRP or blockchain technology."

- "The first potential use that Defendants touted for XRP—to serve as a 'universal digital asset' and/or for banks to transfer money—never materialized"

- "On June 21, 2018, Garlinghouse explained in a public speech that nobody was using XRP to effect cross-border transactions as of that date. Instead, he said that Ripple “expect[ed] this year for at least one bank to use XRP in their payment flows, to use xRapid"

- "Since its launch, ODL has gained very little traction, in part due to certain costs of using the platform...Much of the onboarding onto ODL was not organic or market-driven. Rather, it was subsidized by Ripple. Though Ripple touts ODL as a cheaper alternative to traditional payment rails, at least one money transmitter found it to be much more expensive and therefore not a product it wished to use without significant compensation from Ripple....Ripple had to pay the the Money Transmitter significant financial compensation—often paid in XRP—in exchange for the Money Transmitter’s agreement to help Ripple increase volume on ODL....

Specifically, from 2019 through June 2020, Ripple paid the Money Transmitter 200 million XRP, which the Money Transmitter immediately monetized by selling XRP into the public market, typically on the very days it received XRP from Ripple. The Money Transmitter publicly disclosed earning over $52 million in fees and incentives from Ripple through September 2020....

The Money Transmitter became yet another conduit for Ripple’s unregistered XRP sales into the market, with Ripple receiving the added benefit that it could tout its inorganic XRP “use” and trading volume for XRP. The Money Transmitter has served that principal purpose for Ripple in exchange for significant financial compensation"

- "Even after ODL’s launch, Ripple publicly acknowledged in July 2019 that XRP has no significant use beyond investment"

- "Ripple and Garlinghouse did not disclose to XRP investors or the public the full extent of incentives that Ripple provided to the Money Transmitter in return for its assistance in increasing XRP trading volume.....

Ripple created an information vacuum such that Ripple and the two insiders with the most control over it—Larsen and Garlinghouse—could sell XRP into a market that possessed only the information Defendants chose to share about Ripple and XRP"

1

2

146

Mar 27

PS: you’re bringing up exactly the same question that BTC Maxis were saying five and ten years ago, yet here we are, Ripple still thriving and now at a $50 billion dollar valuation!

Big banks don’t build their own full blockchain platforms to completely replace Ripple/XRP for cross-border payments mainly because it’s expensive, slow to scale, lacks network effects, and comes with massive regulatory/compliance headaches—while Ripple already offers a battle-tested, plug-and-play alternative that many institutions prefer.9

Here’s the breakdown based on how the industry actually works (as of early 2026):

•Building from scratch is costly and fragmented. Developing a private blockchain (or even a public one) that handles global liquidity, compliance (AML/KYC/OFAC sanctions), interoperability across currencies, and real-time settlement requires huge upfront investment in tech, legal, and operations. RippleNet (and the XRPL) already connects hundreds of banks/fintechs across continents with proven speed (seconds vs. days for SWIFT) and low fees (~0.15% in some cases vs. 5% traditionally). Why reinvent the wheel when you can license or partner?18

•Public vs. private ledger preferences. Many big banks (and TradFi firms) avoid fully open/public blockchains like the XRPL for core trading/risk management because everything is visible, which clashes with how they protect strategies and manage risk. That’s why some build private blockchains (e.g., JPMorgan’s Onyx) or use permissioned systems like R3 Corda. But even then, they often still use Ripple’s messaging tech (xCurrent/Ripple Payments) for the actual cross-border plumbing.9

•XRP isn’t always required—but it’s a killer feature when it is. Most Ripple partners use the network for messaging and tracking without touching XRP (fiat-to-fiat works fine). But for On-Demand Liquidity (ODL), XRP acts as a neutral bridge asset that eliminates pre-funded Nostro accounts, cuts capital tied up in transit, and enables instant settlement in corridors where liquidity is thin. Banks get the benefits without Ripple forcing the token on every deal. Ripple’s co-founder has openly noted that heavy compliance requirements make on-ledger XRP use a tough sell for some institutions right now.11

•Network effects and regulation win. Ripple has 300 banking/financial partners globally. Building your own competing network from zero would mean convincing everyone else to join your ledger—while dealing with ongoing regulatory uncertainty, sanctions screening, and capital rules. Ripple’s open-source tech XRP’s bridge role already solves the “correspondent banking” pain points that SWIFT exploits for profit. Smaller/regional banks especially love it because they can’t afford their own rails.13

Some banks are experimenting with their own or consortium solutions (and stablecoins/CBDCs are rising competitors), but Ripple continues to grow volume ($1.3T moved in Q2 2025 in some reports) precisely because it reduces friction without banks having to own the entire stack.

You specifically asked for an X post that’s “for Ripple”—here’s a recent one that directly addresses your exact question (posted March 27, 2026 by @pompxrp):

Banks avoid building their own cross-border rails because it’s costly, slow and fragmented…instead they can leverage $XRP and XRPL for faster settlement, shared liquidity and interoperability across institutions.

It captures the pro-Ripple argument perfectly: why bother building when Ripple/XRP already delivers the efficiency and liquidity edge that big banks (and smaller players) actually need. Plenty of other X chatter echoes this—Ripple’s ecosystem gives institutions speed and cost savings without the full build-out headache.

3

237

Mar 25

🚨 Ripple and China Corridors 🇨🇳

LianLian utilize Ripple's enterprise solutions, specifically "xCurrent and RippleNet" to facilitate Real-Time Cross-Border Payments into and out of CHINA 🇨🇳

Announced in 2018, LianLian have since broadened their blockchain Inititatives.

39

146

5,158

Mar 12

So it's clear BC provides a regulatory edge & is a significant member of the sector. Will we see more play out w/ Flash & Novatt? I should note they also service Airwallex and LianLian, both pre-2019 xCurrent customers, but unable to confirm if they still work with Ripple.

1

4

43

1,334

Mar 10

現在Rippleは「Ripple Payments」という名称で決済ソリューションを展開していますが、これは過去のプロダクトであるxCurrentとxRapid(後のODL)などをまとめたブランドに近いものです。これらは必ずしもすべてがXRPやXRPLを必要とする仕組みではありません。

1

2

27

How Banks Actually Use XRP

Many partners use RippleNet's messaging (xCurrent) to speed and monitor transfers, even if they don't use XRP on every transaction. Those that do leverage XRP typically use it for remittances or FX liquidity.

3

22

Mar 8

RippleNet=xCurrent

XRPの使われないシステムでしたが

バージョン4.0でODLの選択が可能に。

ですがXRPを生かすなら最初からODLのみが採用されています。

xCurrentは他の暗号資産システムと繋がると思います。

繋がると世界中の殆んどの地域を網羅します。

Mar 7

読む価値あり

イーロンX Moneyが発表された。P2P決済、デビットカード、口座振替。Xアプリ内でVenmoが利用可能で、Visaのネットワーク上で動作する。

提携銀行はCross River Bank。FDIC(連邦預金保険公社)の預金保険付きで、送金ライセンスも取得している。また、Rippleの提携銀行で、国際送金にはRippleNetを使用している。

そして、これだ。XRPScanに「~musk」というラベルのXRPウォレットが登場します。16,783,000XRPが入金されている。近日中…乞うご期待

5

27

2,767

Don't listen to him. He doesn't know what he's talking about. With Xcurrent they don't even get 5% of the benefits. They need on demand liquidity which uses XRP. They will all use XRP because Xcurrent is only for the messaging and still has to go thru to old correspondent banking system, etc.

6

358

Mar 4

LMAO at wrongfully sued. Let's take a trip down memory lane. This is why their execs drive 1 of 1 multi million dollar lambos, yet XRPL isn't a top 40 used chain (less than 1% marketshare in RWAs, less than .01% in stablecoins, 46th in developer ecosystem)

- "Large-scale unregistered public distribution of XRP and—with the goal of immense profits—simply assumed the risk that they were violating the federal securities laws."

- "In a December 2017 interview with Bloomberg Garlinghouse stated 'I’m long XRP, I’m very, very long XRP as a percentage of my personal . . . balance sheet' (though he had already sold at least 67 million XRP)"

- Garlinghouse "instructed certain Ripple employees to 'proactively' attempt to increase speculative trading value with positive XRP news", employed "supply limiting tactics", and "approved the buy back option" to increase XRP price.

- "Ripple actively sought to offer and sell XRP widely as possible.....for an imagined, future use case"

- "December 2017, Garlinghouse explained that XRP’s price had risen because Ripple was 'solving a real problem . . . a multi-trillion dollar problem around cross-border payments'"

- Through 2016 to 2019, Ripple began selling two software suites, xCurrent and xVia "neither uses XRP or blockchain technology."

- "The first potential use that Defendants touted for XRP—to serve as a 'universal digital asset' and/or for banks to transfer money—never materialized"

- "On June 21, 2018, Garlinghouse explained in a public speech that nobody was using XRP to effect cross-border transactions as of that date. Instead, he said that Ripple “expect[ed] this year for at least one bank to use XRP in their payment flows, to use xRapid"

- "Since its launch, ODL has gained very little traction, in part due to certain costs of using the platform...Much of the onboarding onto ODL was not organic or market-driven. Rather, it was subsidized by Ripple.

-Though Ripple touts ODL as a cheaper alternative to traditional payment rails, at least one money transmitter found it to be much more expensive and therefore not a product it wished to use without significant compensation from Ripple....Ripple had to pay to the Money Transmitter significant financial compensation—often paid in XRP—in exchange for the Money Transmitter’s agreement to help Ripple increase volume on ODL....

-Specifically, from 2019 through June 2020, Ripple paid the Money Transmitter 200 million XRP, which the Money Transmitter immediately monetized by selling XRP into the public market, typically on the very days it received XRP from Ripple.

The Money Transmitter publicly disclosed earning over $52 million in fees and incentives from Ripple through September 2020....The Money Transmitter became yet another conduit for Ripple’s unregistered XRP sales into the market, with Ripple receiving the added benefit that it could tout its inorganic XRP “use” and trading volume for XRP. The Money Transmitter has served that principal purpose for Ripple in exchange for significant financial compensation"

- "Even after ODL’s launch, Ripple publicly acknowledged in July 2019 that XRP has no significant use beyond investment"

- "Ripple and Garlinghouse did not disclose to XRP investors or the public the full extent of incentives that Ripple provided to the Money Transmitter in return for its assistance in increasing XRP trading volume.....

Ripple created an information vacuum such that Ripple and the two insiders with the most control over it—Larsen and Garlinghouse—could sell XRP into a market that possessed only the information Defendants chose to share about Ripple and XRP"

3

2

54

1,157