Institutional Investor. Private Markets (PE, PD, Infra, Real Estate): €1Bn invested. Primaries & direct Secondaries. Sharing insights on markets, deals & GPs

Joined April 2020

- Tweets 1,538

- Following 362

- Followers 9,755

- Likes 2,997

204 Photos and videos

Pinned Tweet

30 Jul 2023

This is the story of the most profitable private equity buyout of all time and it’s French 🇫🇷

Company : Polyplus-Transfection

Sector : Healthcare 💊

Sponsor : Archimed

Here is a thread on how Archimed achieved a 300x MOIC on its initial investment 🧵👇

3

29

126

58,579

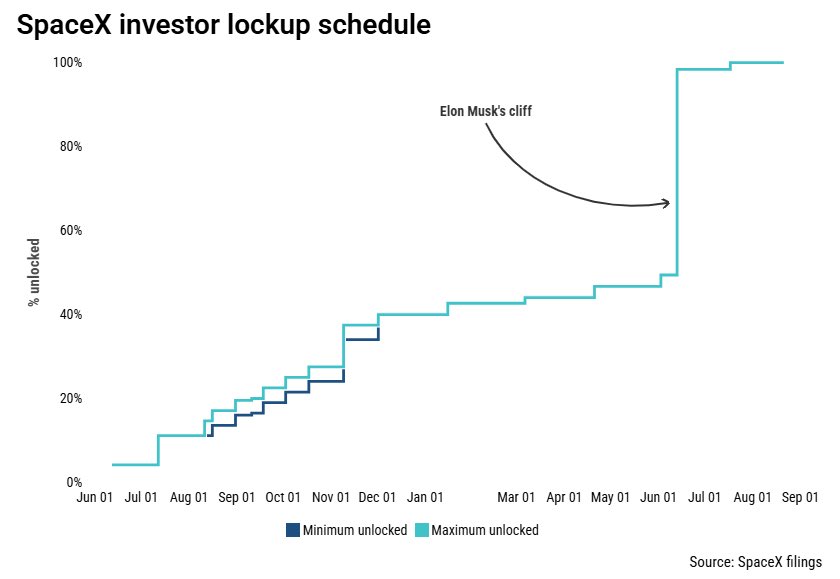

SpaceX private investors lockup schedule

4

12

214

24,768

I start listening when a guy delivers 4x net MOIC on a buyout fund.

I had a meeting with a Top 5% European lower mid-market GP today, and one of the partners shared is thought about Software Investing 👇

« Software is not 'dead' because of AI, but you now have to be much more disciplined in what you back. The market reaction has been partly justified, but the idea that all software companies will be disrupted is intellectually lazy. Instead, there is a clear split between fragile and highly defensible software businesses.

The types of software we like have common characteristics

1. Backbone systems: software that sits at the core of a client’s operations and cannot be removed without breaking the business (e.g., accounting or ERP systems).

2. Ownership of proprietary data: the software generates and controls the underlying data, rather than just layering on top of existing datasets.

3. Strong distribution moat: customer bases built over many years through direct sales and deep integration, not easily replicated by a new AI-native entrant.

4. Regulatory barriers: software operating in regulated environments (e.g., certified platforms) is far harder to replace quickly.

5. Low tolerance for error: when mistakes have financial, legal, or operational consequences, clients are reluctant to switch to less proven AI-driven tools.

6. High technical depth: complex products with large codebases are more defensible than lightweight tools that can be rebuilt easily with vibecoding.

Bottom line: we remain positive on software, especially vertical, mission-critical, and regulated solutions. The current environment as potentially attractive for investing, as valuations may be over-correcting due to generalized fears around AI. »

8

83

43,448

I had a meeting with a Top 5% European lower mid-market GP today, and one of the partners shared is thought about Software Investing 👇

« Software is not 'dead' because of AI, but you now have to be much more disciplined in what you back. The market reaction has been partly justified, but the idea that all software companies will be disrupted is intellectually lazy. Instead, there is a clear split between fragile and highly defensible software businesses.

The types of software we like have common characteristics

1. Backbone systems: software that sits at the core of a client’s operations and cannot be removed without breaking the business (e.g., accounting or ERP systems).

2. Ownership of proprietary data: the software generates and controls the underlying data, rather than just layering on top of existing datasets.

3. Strong distribution moat: customer bases built over many years through direct sales and deep integration, not easily replicated by a new AI-native entrant.

4. Regulatory barriers: software operating in regulated environments (e.g., certified platforms) is far harder to replace quickly.

5. Low tolerance for error: when mistakes have financial, legal, or operational consequences, clients are reluctant to switch to less proven AI-driven tools.

6. High technical depth: complex products with large codebases are more defensible than lightweight tools that can be rebuilt easily with vibecoding.

Bottom line: we remain positive on software, especially vertical, mission-critical, and regulated solutions. The current environment as potentially attractive for investing, as valuations may be over-correcting due to generalized fears around AI. »

2

57

46,589

I am computing some stats on our secondary track record, and I found that on a time-series basis, our weighted-average DPI after 18 months is 0.46x, which I think is quite good for buyout exposure.

This is what secondary is meant for: early cash flows

2

2

844

The market is so bad that they are organizing a private equity Mass in Paris 🤣

« Good Lord, offer us crystallized carried on unrealized gains, forgive us our 2% management fees, keep us away from adjusted EBITDA, and deliver us from add-backs. Amen.”

3

14

84

10,074

The Institutional Limited Partner retweeted

🚨As we prepare the launch of our Private Equity Secondaries fund dedicated to small deals (target Sept 2026) and given the current prolific deal flow, I’m looking for a partner able to provide ~€10 to 15m of warehousing capacity to seed initial transactions.

These deals would be transferred into the fund at launch (avoiding a blind pool for incoming investors and making it more appealing).

Economics are negotiable but ideally: pre-agreed yield and exit through inflows or option to convert into the fund with no fees and no carry.

DMs open, feel free to reach out

4

1

25

4,592

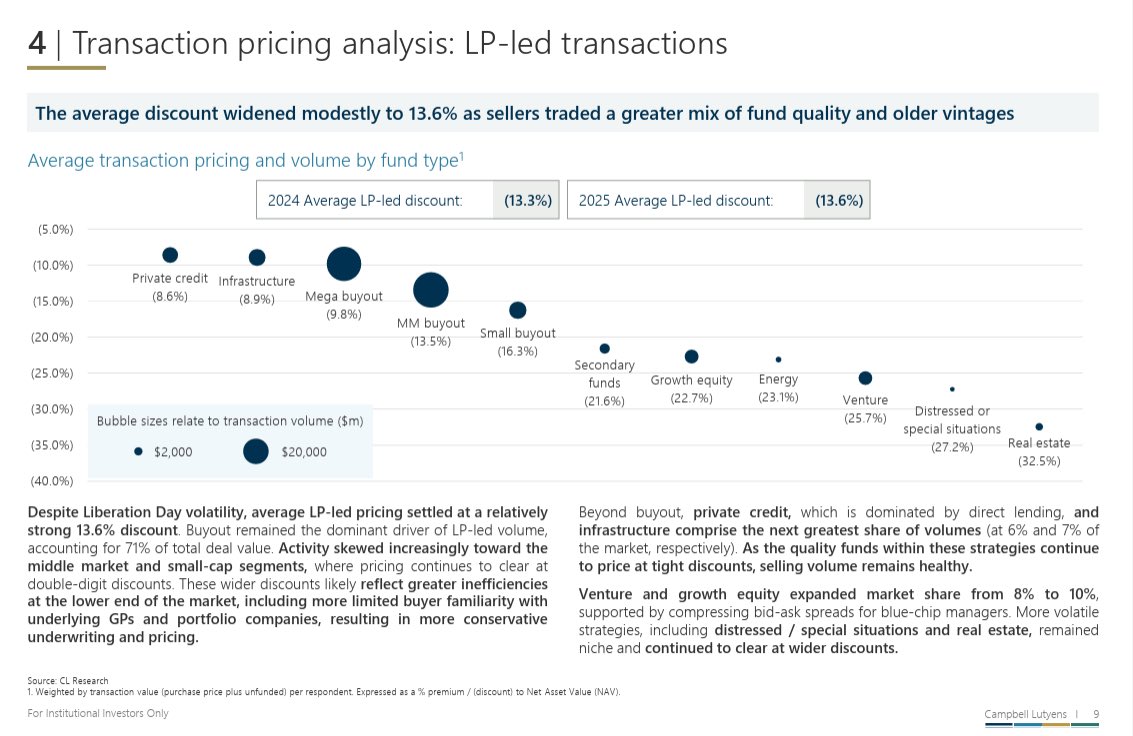

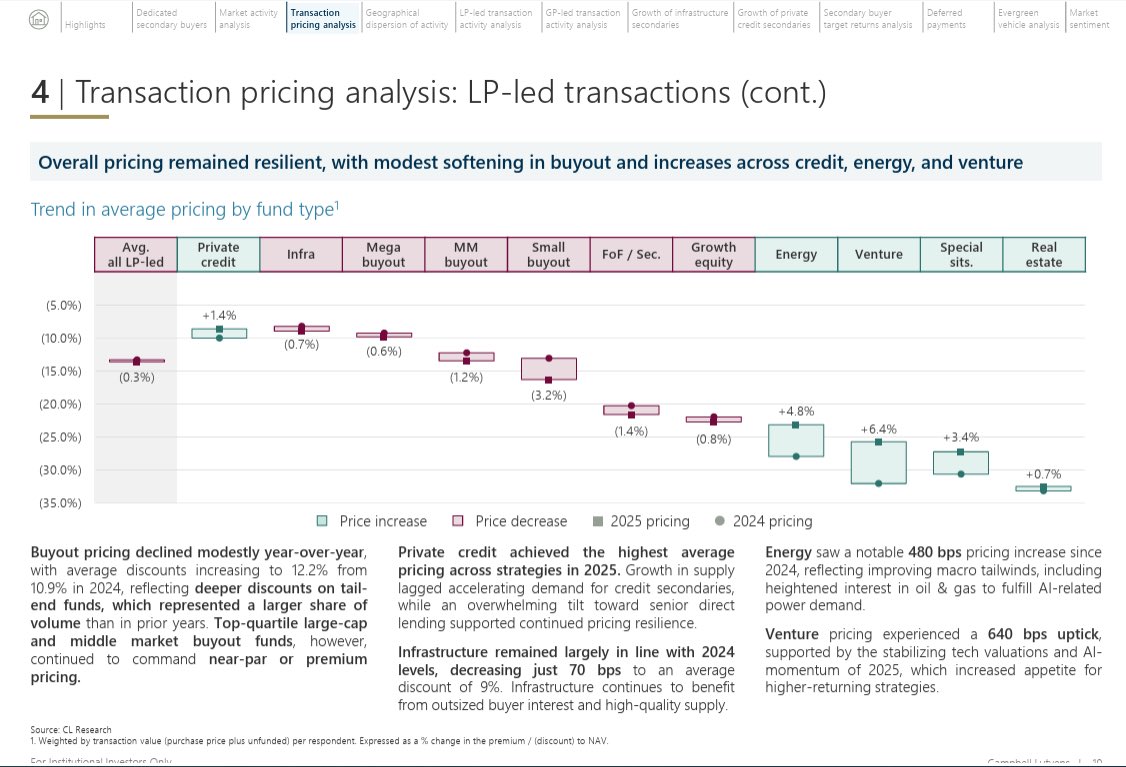

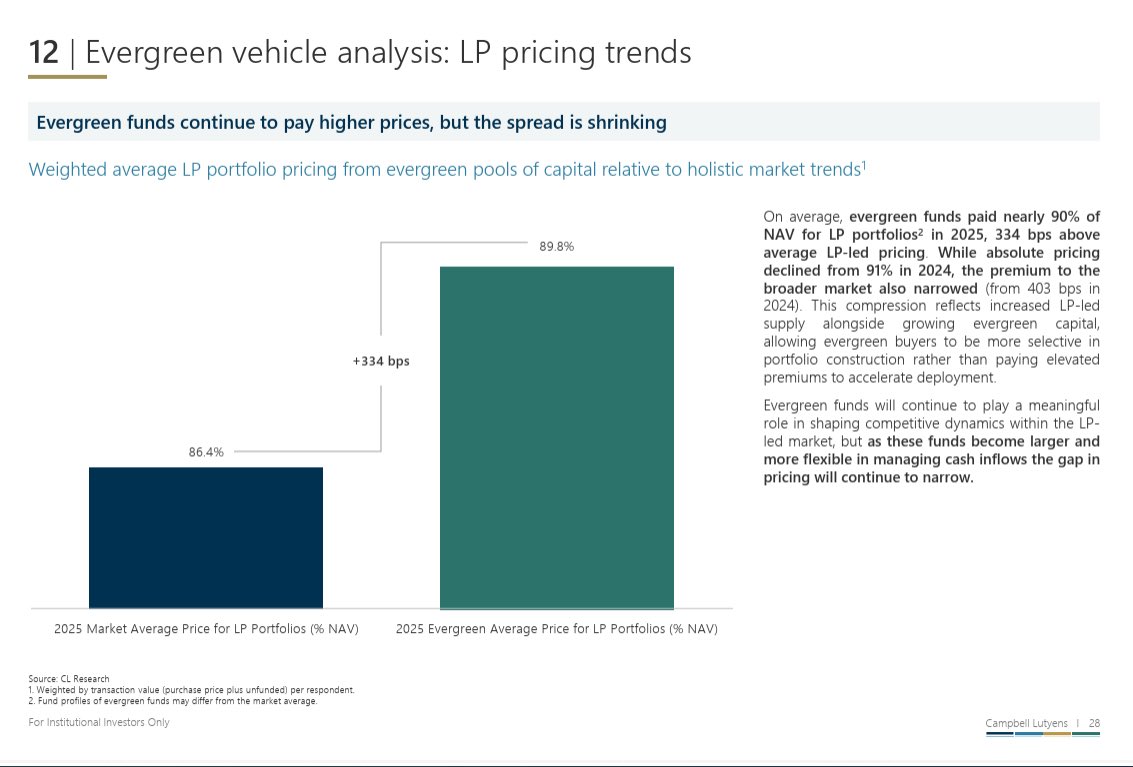

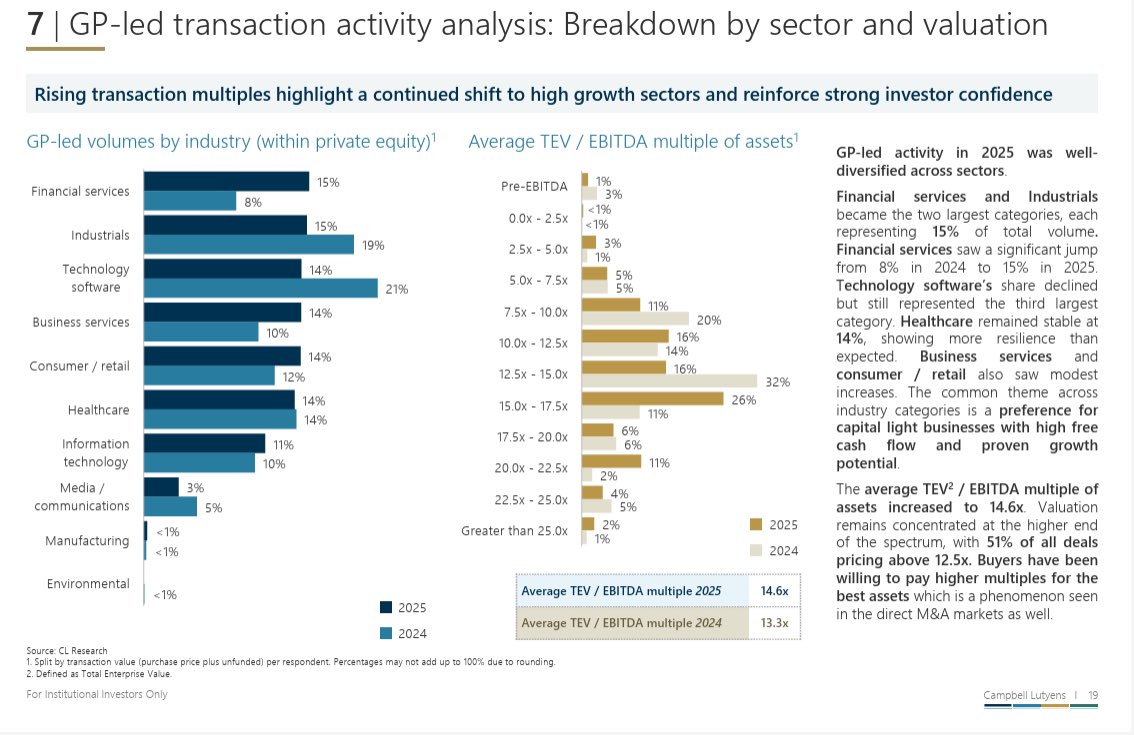

Another good report from Campbell Lutyens on secondaries. Some stats that caught my attention 👇

1. Average pricing and size by underlying strategy

2. Trend in pricing by underlying strategy

3. Evergreen still overpaying 330bps on average vs traditional closed funds

4. GP-led activity by sector and valuations

1

8

61

6,031

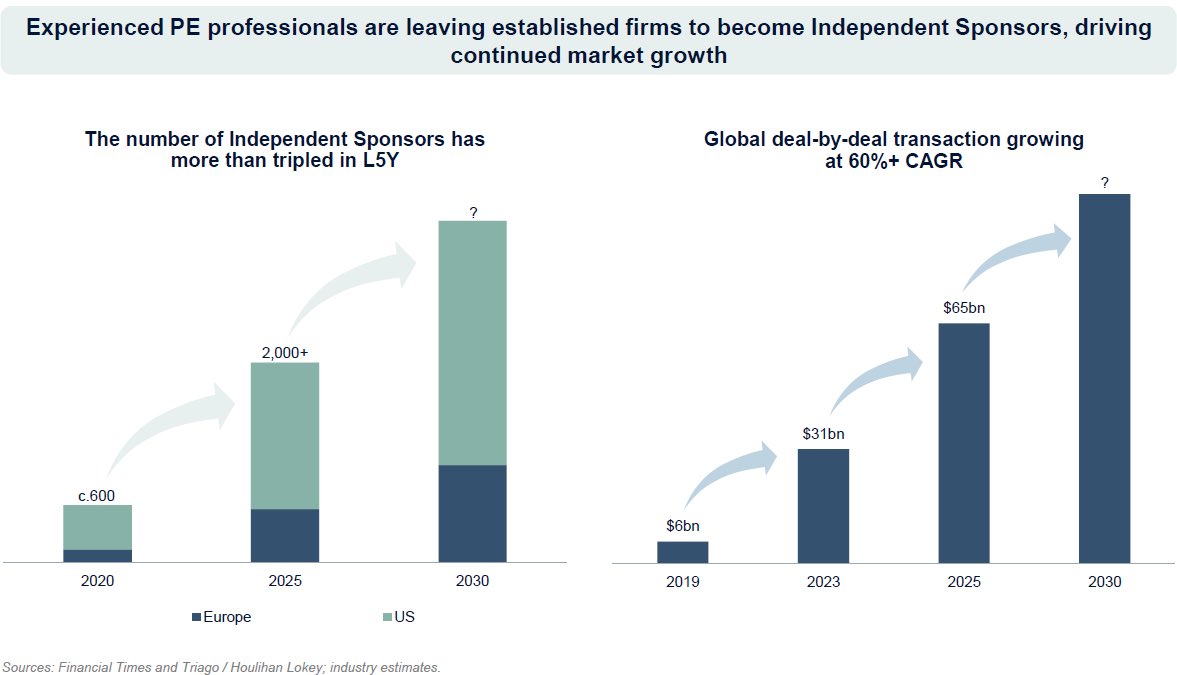

The independent sponsor model is gaining traction, with deal value increasing tenfold over the last 7 years.

The current state of the PE market is prone to the formation of this type of structure, and I believe we will see more and more going forward

3

8

82

11,168

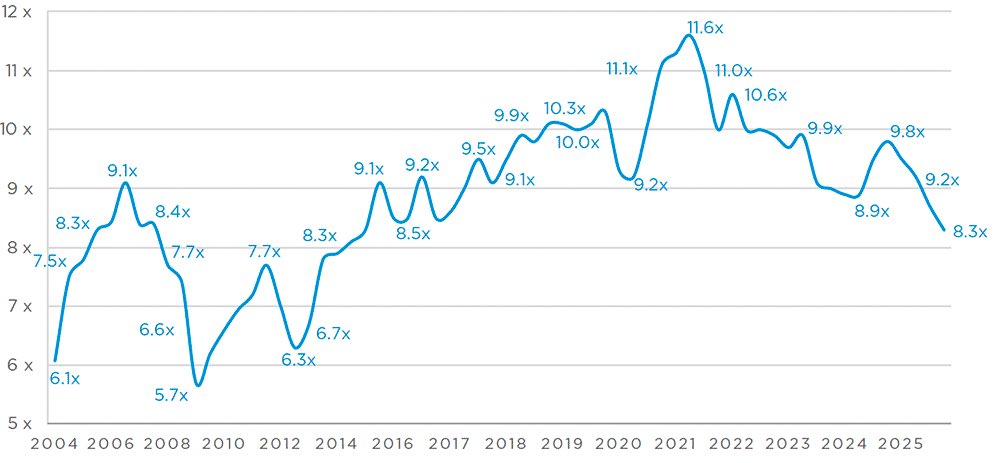

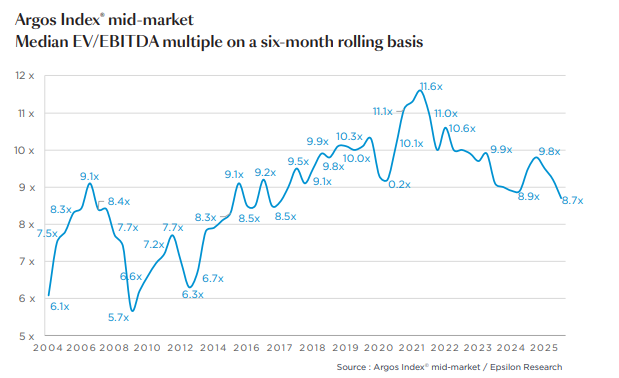

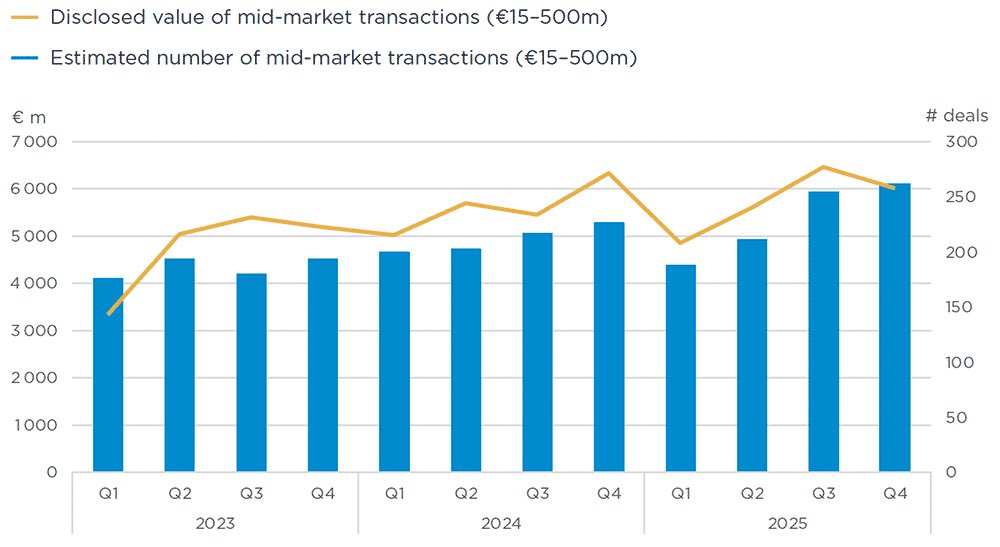

Private Equity - Valuations for European mid-market deals continue to decline, reaching levels not seen since 2015.

1. Argos Index fell to 8.3x EV/EBITDA in Q4 2025, down from 9.8x at the same time last year.

2. Only 7% of deals are now closed above 15x EBITDA, a record low

3. Mid Market M&A accelerated at year's end, supported by lower valuations and better alignment between buyers and sellers expectations

5

10

69

13,087

The Institutional Limited Partner retweeted

It's happening! In a few months, I will go on the other side of the fence after a decade as an LP.

With a bit of structuring and time to clear all the regulatory hurdles, our fund dedicated to small secondaries should be ready in Q3.

9

1

46

4,289

The Institutional Limited Partner retweeted

More investing and operational widsoms from the same sponsor 👇

Management quality sits at the center of the value creation equation. A strong CEO-GP relationship creates transparency, speed, and trust when things go wrong. And they always go wrong. Most value destruction in private equity comes from the delayed recognition of management failure.

Real value creation requires people who have actually run companies, handled crises etc... When operators are in the ownership structure, with authority and carry then execution improves. On the other hand, when “operating partners” are peripheral or advisory, their effect is limited. Value creation is not something you can outsource.

Had an interesting conversation with a very successful sponsor on how to pay low multiples at entry:

“There is no magic you have to go in places most investors deliberately avoid. The first real driver of value is how you enter. Buying something “cheap” is not about luck; it’s about accepting complexity that others can’t or won’t underwrite. That complexity can be governance deadlock, a messy carve-out, a loss-making division, a stigma around the sector, or a management transition. The discount is not upside it is a protection. That protection will become upside only if you are able to fix the reasons the asset was cheap in the first place”

1

1

7

3,012

The Institutional Limited Partner retweeted

Had an interesting conversation with a very successful sponsor on how to pay low multiples at entry:

“There is no magic you have to go in places most investors deliberately avoid. The first real driver of value is how you enter. Buying something “cheap” is not about luck; it’s about accepting complexity that others can’t or won’t underwrite. That complexity can be governance deadlock, a messy carve-out, a loss-making division, a stigma around the sector, or a management transition. The discount is not upside it is a protection. That protection will become upside only if you are able to fix the reasons the asset was cheap in the first place”

5

7

121

15,114

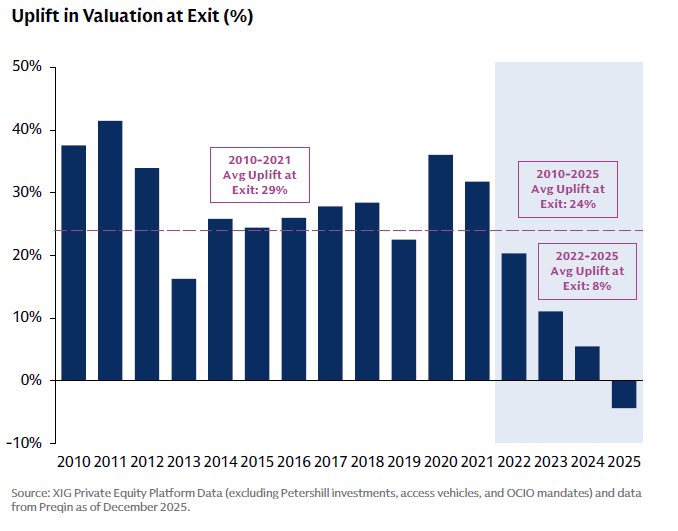

Interesting data on PE from Goldman Sachs noting an average negative valuation uplift at exit for deals in 2025 (average of 1, 3 and 5 quarter valuation prior to exit). I had somewhat more positive stats from Stepstone, but I can’t say I am surprised.

6

15

128

67,424

Received this goodie today at a private equity conference

2

14

1,474

I am in touch with the team running an electronic secondary platform that is currently integrating with iCapital and Private Bank platforms to facilitate liquidity offerings to their clients.

It appears that the retail/wealth management crowds require earlier liquidity than anticipated.

8

1

15

2,900

The Venezuela thing reminds me of a story.

In 2015, I briefly worked at the FX treasury desk of a large pharmaceutical company, which had cash trapped in Venezuela, equivalent to $200 million in local currency. The currency wasn’t exchangeable, and you couldn’t repatriate it. But the Venezuelan government offered a solution for foreign companies. You could exchange your Bolivars to buy a primary bond issuance of PDVSA, denominated in USD, at a set, rigged exchange rate, of course. PDVSA, the local oil company, was in default, and the bonds on the secondary market were trading at 25 cents on the dollar. However, by owning the bonds, you could then sell them to get US dollars back.

So the only way to get cash back was to take a 75% hit on it.

Pure organised racketeering

2

7

77

9,147