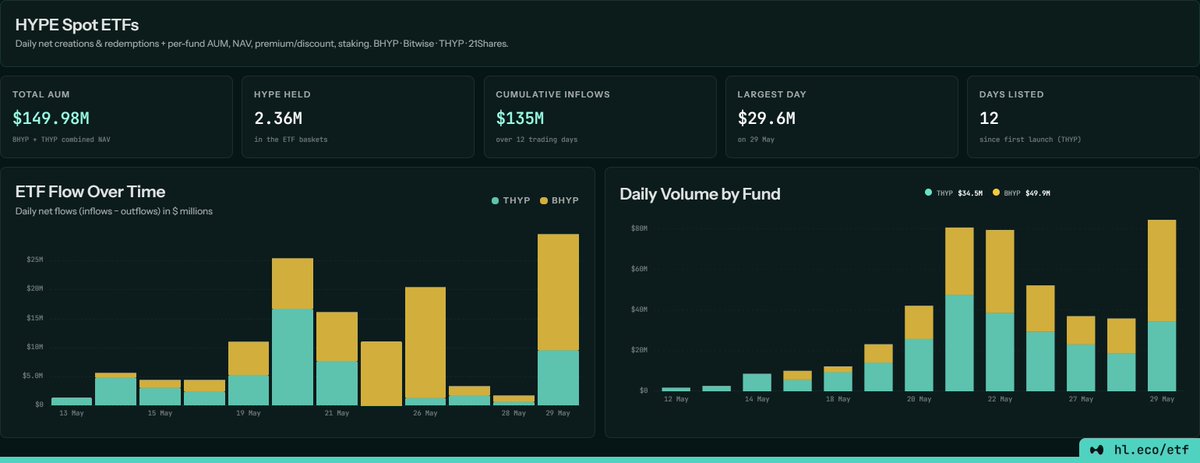

Joined August 2017

- Tweets 2,377

- Following 635

- Followers 354

- Likes 33,638

66 Photos and videos

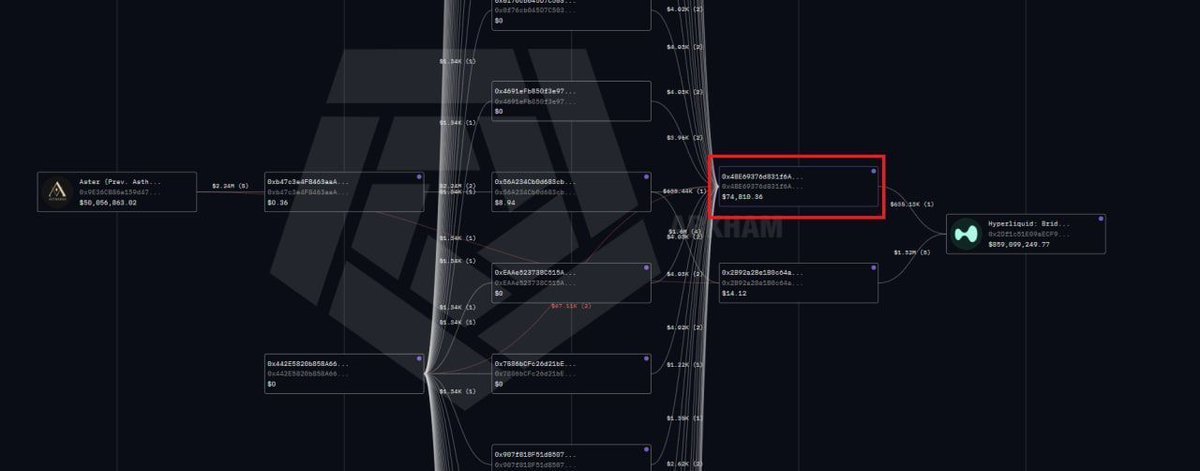

Someone tried to attack Hyperliquid's liquidity pool.

They lost $540K.

The pool they attacked? Lost $130K.

The attacker took 4× more damage than their target. 🧵

Per @MarketsAlpha on-chain analysis:

A wallet cluster — allegedly funded via Aster — deposited $635K into Hyperliquid and started longing Fartcoin.

Four hours later: 👇

→ Position grew to $7.1M notional

→ That's ~20% of entire Fartcoin OI

→ Wallet: fully liquidated, -$540K

→ HLP absorbed & closed position: ~$130K loss

The alleged 5-step playbook: 👇

→ Step 1: Grab ~20% of OI on a low-cap token

→ Step 2: Buy spot to pump price

→ Step 3: Force a backstop liquidation

→ Step 4: Make HLP inherit the position

→ Step 5: Dump spot — leave HLP bleeding

Sound familiar? It's the same structure used in previous HL attacks.

This time, it couldn't even clear Step 2. 🔁

Mainstream take: "DeFi pools are sitting ducks for manipulation."

This case: the attacker lost 4× more than the protocol they targeted.

That doesn't make HL invincible — one failed attempt isn't a stress test. But it does mean the risk runs both ways.

Open question: if attacking costs more than winning, how long before that math changes the calculus? ⚡

Jun 16

Yesterday, a wallet funded from Aster may have attempted to attack Hyperliquid. .

It belongs to a cluster that withdrew $2.3M from Aster one week ago.

20h ago, the wallet deposited $635K into Hyperliquid and started longing Fartcoin.

Address:

markets.xyz/trader/0x4be6937…

Four hours later, the position had reached $7.1M notional, which was almost 20% of the entire open interest in that market.

The setup was familiar:

Step 1: Open a huge share of OI on a low-cap token.

Step 2: Buy spot to push the price up.

Step 3: Try to force a backstop liquidation.

Step 4: Make HLP take over the position.

Step 5: Then dump the spot, leaving HLP stuck with a large long and a large loss.

That appears to have been the plan, but this time, it failed hard and couldn’t even reach the step 2.

After pushing the price up longing non-stop for 4 hours, the wallet got fully liquidated and lost $540K on the trade.

HLP took over the position, closed it and ended up taking only around $130K in losses.

The entity behind the cluster remains anonymous.

4

6

54

12,458

Jun 16

Everyone's pricing $HYPE off the wrong number.

1 billion is too high. "Circulating supply" is too low.

The real valuation base sits in between — and almost no one is using it yet. 🧵

Hyperliquid Research Collective (HRC) introduces Outstanding Token Supply (OTS) — a middle-ground metric that strips out what's truly gone or uncommitted.

Snapshot @ $65.78/HYPE · June 15, 2026 :

→ Start: 1,000,000,000 tokens

→ Less 414M: future emissions, not yet issued

→ Less 45.2M: Assistance Fund (keyless address, validator-locked)*

→ Less 63M: Foundation grants

→ Less 1.1M: literally burned via fees

📊 OTS: 475.6M tokens = $31.3B

*Not a technical burn — but economically permanent per Dec 2025 validator vote.

Mainstream take: "Just use circulating supply ($15.5B). The rest is noise."

The problem: circulating supply ignores 241.3M Core Contributor tokens that WILL vest on a known, published schedule.

That's 50.6% of OTS — still locked, but contractually committed.

Underpricing that overhang is the same mistake equity analysts make when they ignore unvested RSUs.

OTS counts them. Deliberately. 💸

One flag before you quote this everywhere:

HRC is affiliated with Hyperliquid Strategies Inc — an institutional HYPE product. Not a fully independent source. The methodology is rigorous; the conflict of interest still matters.

That said — if $31.3B (OTS) becomes the standard vs $15.5B (circulating), how does that change institutional sizing decisions?

The number you use in the denominator changes everything. ⚡

4

2

18

3,955

Jun 14

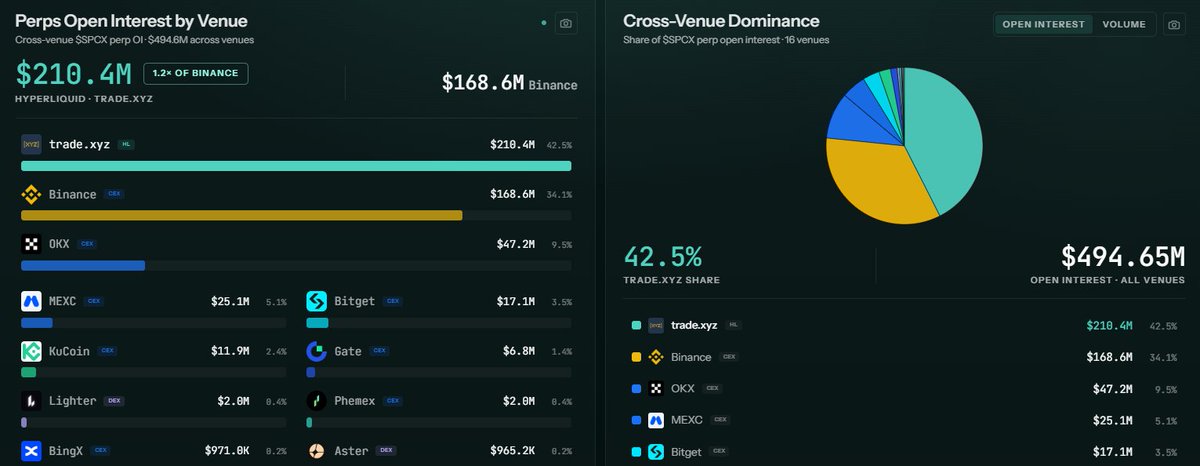

A DEX just out-OI'd Binance in the same market.

Not a meme coin. Not an airdrop farm.

A pre-IPO equity perp — across 16 venues. 🧵

$SPCX perp OI, right now: 👇

→ trade.xyz (DEX on HL): $210.4M — 42.5%

→ Binance (CEX): $168.6M — 34.1%

→ OKX: $47.2M — 9.5%

→ MEXC: $25.1M — 5.1%

→ Total across 16 venues: $494.65M

trade.xyz is sitting at 1.2× Binance in open interest.

Mainstream take: "CEXs dominate on liquidity. DEXs can't compete."

But trade.xyz isn't fighting CEXs on their turf.

It listed first. It settled on-chain. It runs 24/7 with no KYC gate.

By the time Binance showed up, trade.xyz already owned 42% of the market. 🔁

That's not competing. That's not being where the competition even knows to look.

When a DEX outruns Binance in OI — not through token incentives, but by listing a real-world asset first — what does that say about where price discovery is actually heading? ⚡

4

180

Jun 13

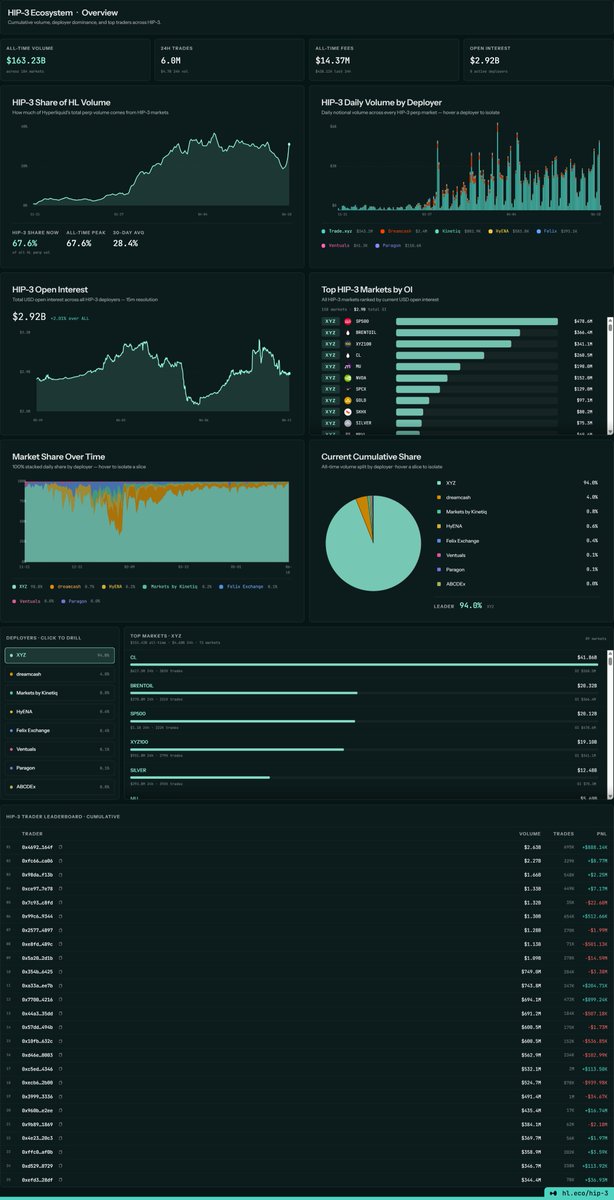

HIP-3 markets now make up 42% of ALL Hyperliquid perp volume.

And 75% of that volume isn't crypto at all.

It's commodities. 🧵

The breakdown right now: 👇

→ HIP-3 24h vol: $2.5B (41.9% of all HL vol)

→ HIP-3 open interest: $2.9B (31.7% of all HL OI)

→ Core crypto perps: $3.5B (58.1%)

→ HL total OI: $9.0B

HIP-3 asset mix:

🛢️ Commodities: 75%

📊 Indices: 15%

📈 Equities: 10%

₿ Crypto: 0%

Mainstream take: "HIP-3 diversifies Hyperliquid's market ecosystem across many builders."

The data says otherwise.

→ XYZ deployer: 97.3% of 24h volume, 96.8% of OI→ Everyone else (dreamcash, Kinetiq, HyENA, Felix, Paragon, Ventuals) splits the remaining ~3%

One deployer is effectively HIP-3 right now. 🍰

So HL's fastest-growing segment (42% of total volume) is:

Dominated by ONE deployer (97%)

Dominated by ONE asset class (commodities, 75%)

Zero crypto exposure

Is this "ecosystem growth" — or one team building a commodities exchange on top of Hyperliquid? ⚡

2

1

19

1,409

Jun 12

Hyperliquid just quietly expanded into daily betting markets for ETH, HYPE, and SOL.

Not perps. Not options.

Binary outcomes — settled every single day. 🧵

What changed :

→ BTC already had daily binary outcomes

→ Now ETH, HYPE, SOL added too

→ Auto-deployed daily

→ Settled at 06:00 UTC

→ Settlement price = HL mark price (e.g. ETH-USDC)

Fully automated. No manual listing needed. 📅

Counter: recurring daily binaries = a built-in prediction market layer running on the same infra, same price feed, same liquidity base.

This isn't a new app bolted on. It's native — and now covers 4 major assets daily. 🔁

A perp DEX that also runs daily settled binary markets on its own price feed, for free, at scale.

Open question: if this expands to more assets — does HL become the default venue for daily crypto prediction markets too? ⚡

5

95

187

1,799

Jun 11

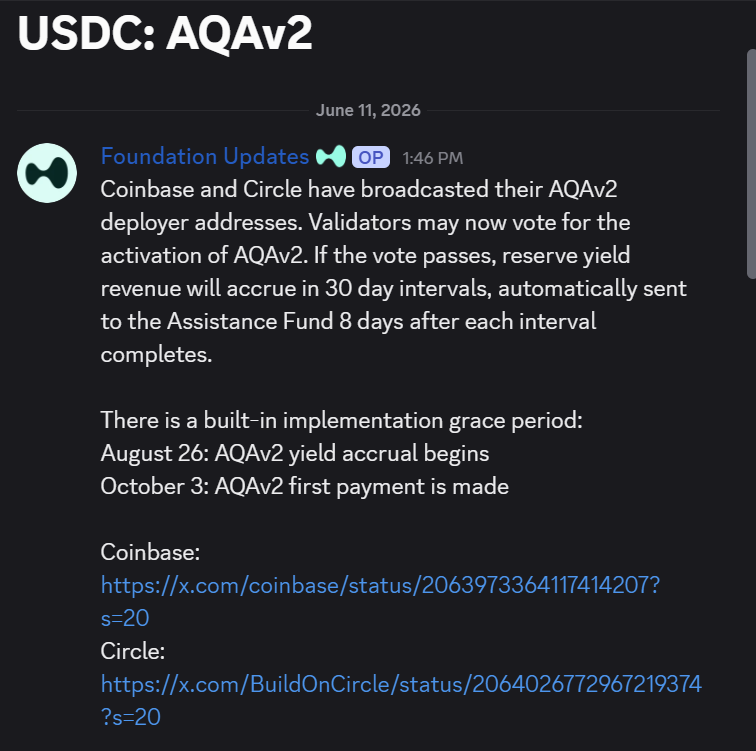

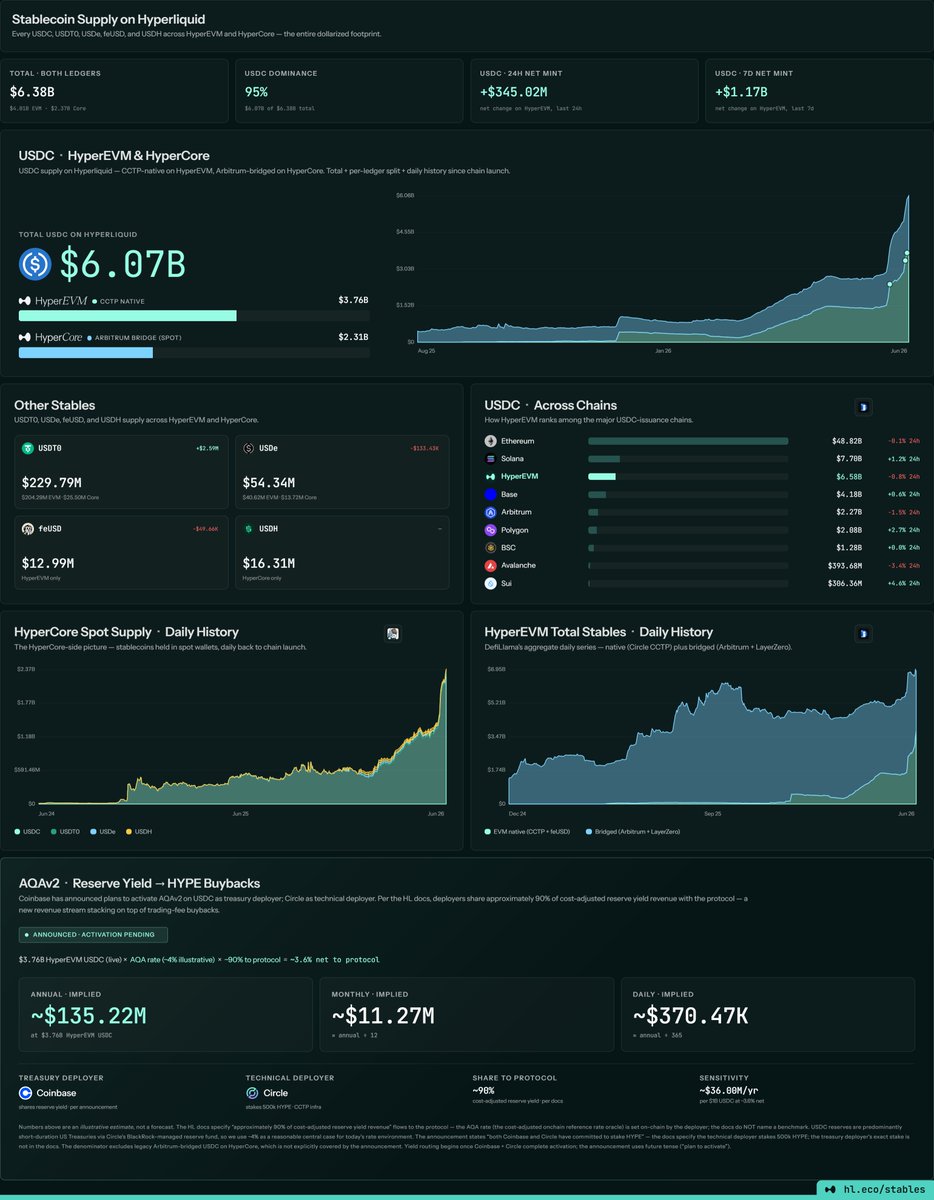

Coinbase and Circle announced AQAv2 at 1:46 PM.

By 9:40 PM — same day — at least 13 validator groups had already voted Yes.

That's 8 hours. No drama. No debate.

What's AQAv2? A mechanism routing USDC reserve yield — interest Coinbase and Circle earn on reserves — to the protocol's Assistance Fund.

If vote passes (Foundation announcement, June 11, 2026):

→ Yield accrues in 30-day intervals→ Auto-sent to Assistance Fund 8 days after each interval → Accrual starts: Aug 26→ First payment: Oct 3

(Exact yield amount not disclosed in announcement.)

Validators who've already voted Yes (Discord, June 11 — vote still ongoing):

B-Harvest · ASXN · Nansen x HypurrCo · Kinetiq x Hyperion · Imperator.co · Hyperstake · ValiDAO · Alphaticks · Flowdex · and more.

Several entries represent multiple validator entities in one vote — individual validator count likely higher.

Mainstream take: "On-chain governance is slow and contentious."

Reality: 13 validator groups coordinated a Yes vote within 8 hours of two centralized institutions agreeing to redirect real yield onto a public chain.

If this passes — what's the precedent for every other chain with billions in stablecoins sitting idle?

2

147

Jun 11

Today, two-thirds of Hyperliquid's perp volume isn't BTC or ETH.

It's S&P 500, crude oil, and NVDA stock.

Most people still think of Hyperliquid as a "crypto exchange." The data says otherwise.

HIP-3 — Hyperliquid's permissionless market creation protocol — hit 67.6% of all HL perp volume as of June 11, 2026.

That's not just high. That's the all-time peak.

The 30-day average was 28.4%.

→ All-time HIP-3 volume: $163.23B

→ Open interest: $2.92B (8 deployers)

→ Top market by OI: SP500 — $478.6M

→ One deployer (XYZ) holds 94.8% of all cumulative volume

TradFi assets are migrating onto crypto rails. Retail is getting 24/7 access to S&P 500 and crude oil futures — through infrastructure that doesn't close on weekends.

This isn't crypto copying TradFi. It's TradFi assets losing their venue monopoly.

If HIP-3 sustains above 50% of HL volume — at what point do you stop calling this a crypto exchange?

And if one deployer holds 94.8% of all HIP-3 volume, is that a dominant venue emerging — or early-stage concentration risk?

4

5

26

1,297

Jun 10

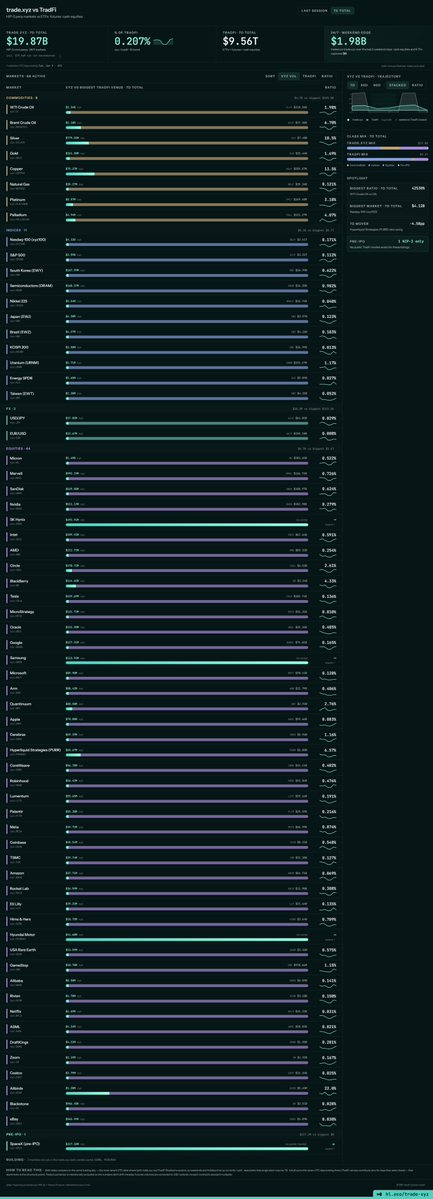

WTI Crude Oil on a crypto perps platform trades at 42,500% of its TradFi ETF equivalent volume.

Crypto isn't just eating finance.

It's eating commodities too — and most people haven't noticed.

The numbers from @tradexyz's dashboard (as of June 10, 2026 — prices shift daily):

→ Total XYZ volume: $19.87B→ TradFi equivalent: $9.56T→ Crypto perps = 0.207% of TradFi overall — still small

But zoom into the gaps:

🥈 Silver: 18.5% ratio vs TradFi ETFs

🛢️ WTI Crude: 42,500% ratio vs TradFi ETFs

📅 Weekend volume: $1.98B — traded while TradFi was closed

🚀 SpaceX pre-IPO: literally no TradFi market exists for this

(Note: TradFi comparison = ETFs/cash equities only, NOT CME futures. WTI's 42,500% is real — but reflects thin ETF oil markets, not total crude derivatives.)

Mainstream narrative: "Crypto perps are just token speculation with leverage."

The counter: The extreme ratios appear precisely where TradFi has structural gaps — illiquid commodity ETFs, closed weekends, and pre-IPO assets with no public market.

This isn't degens gambling. This is market structure filling a real void: 24/7 price discovery for assets TradFi deliberately ignores outside business hours.

The $1.98B weekend volume alone is evidence. That's price action happening on real assets — crude, silver, equities — when every traditional exchange is dark.

Crypto perps = 0.2% of TradFi by total dollar volume.

But in specific commodity niches? Already orders of magnitude larger than the ETF equivalent.

Open question: if volume leads price discovery, where does real-time commodity price formation actually happen now?

The dashboard suggests the answer is already shifting. The narrative hasn't caught up yet.

4

2

17

670

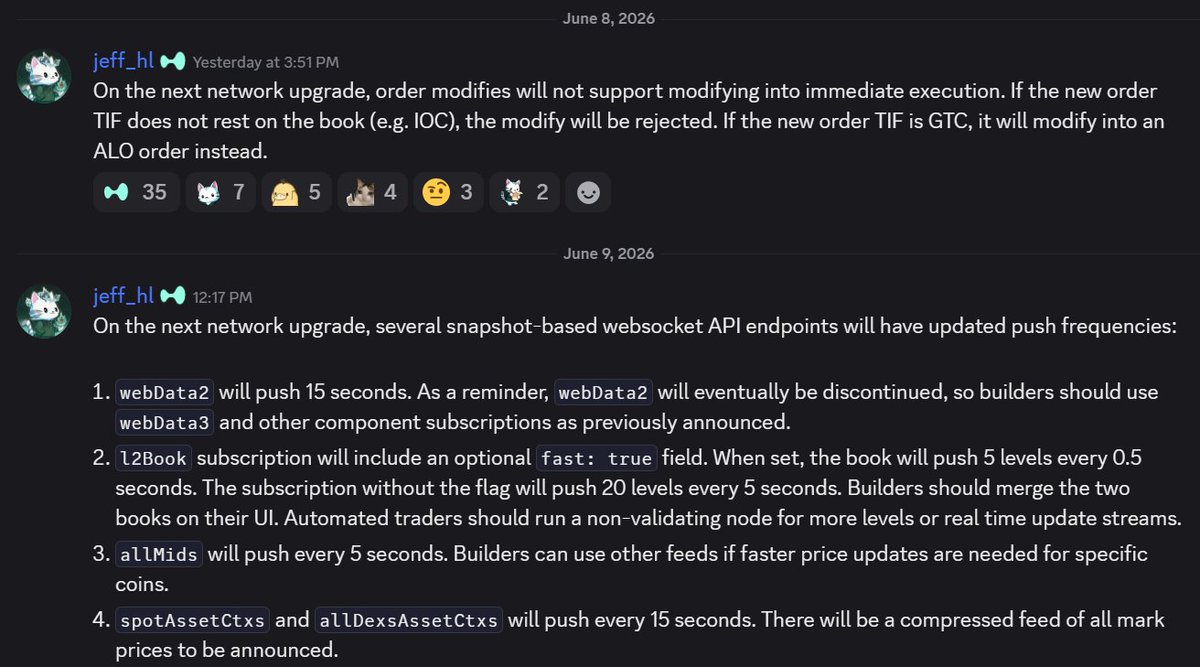

Jun 10

Most DEX teams post about token price.

@chameleon_jeff posted about API latency.

That's not boring — that's what serious infrastructure looks like. 👀

Two changes coming in the next Hyperliquid network upgrade.

Change 1 — Market integrity:

Modify-to-snipe just got closed. 🔒

If you modify an order to IOC (immediate execution) → rejected. If GTC → auto-converts to ALO (Add Liquidity Only).

Plain English: a tactic used to exploit market makers via order modification no longer works. Market makers are better protected. Orderbook quality improves.

Change 2 — Data infrastructure:

📡 l2Book fast mode: order book pushes every 0.5 seconds

📡 Normal mode: 20 levels every 5 seconds

📡 allMids price feed: every 5 seconds

📡 Compressed mark prices feed: coming soon

📡 webData2 being phased out → migrate to webData3

0.5 seconds. On a decentralized exchange. Free. Public. Available to any builder.

Mainstream take: "Just a dev update, skip."

The counterintuitive read:

Professional trading firms pay thousands of dollars per month for co-location and Level 2 order book access at traditional exchanges. Speed is a product they sell.

Opinion/interpretation: Hyperliquid is shipping sub-second order book data to any builder, for free, and actively deprecating old endpoints like a real tech company running production infra.

The cost of building institutional-grade tools on Hyperliquid just dropped. Again.

Every builder who builds on this data → more applications. More applications → more volume. More volume → more fees. 99% of fees → buy $HYPE. 🔄

The question worth asking:

When was the last time a "DEX" actively patched market microstructure exploits, upgraded data latency, AND deprecated legacy APIs — all in the same week?

The label says DEX. The operational playbook says something else entirely. 🏗️

⚠️Not financial advice. Always DYOR.

12

18

85

5,731

Jun 9

A crypto exchange that's technically outside US jurisdiction just submitted a formal legal brief to the US federal government.

Not asking for permission.

Telling regulators how to write rules that keep American innovation in America. 🤯

This filing is proof that Hyperliquid's endgame was never offshore avoidance — it's a compliant, regulated future inside the US system, on terms that preserve DeFi's core architecture.

On June 9, 2026 — today — Paradigm and Hyperliquid Policy Center submitted formal comments to FinCEN and OFAC on proposed stablecoin rules under the GENIUS Act.

This is not a press release. This is a legally filed regulatory comment with case citations, statutory analysis, and six specific policy requests. 📋

What they're actually asking for — in plain English:

1. Don't make stablecoin issuers spy on everyone:USDC issuers should only KYC their own direct customers — not monitor every wallet on earth that touches USDC. Just like a bank doesn't track what you do with cash after you withdraw it. ✅

2. Protect developers who want to help:Right now, DeFi developers who voluntarily report suspicious activity to the government get zero legal protection for doing so. The filing asks FinCEN to fix that — extend safe harbor to developers who cooperate. ✅

3. Let smart contracts be compliance:If a protocol can programmatically block sanctioned addresses in real time — that should count as regulatory compliance. Code can enforce compliance before a transaction happens, not just after. More effective. More efficient. ✅

4. The nuclear warning:

This is the most important paragraph in the entire document:

"Failing to issue this clarification would risk imposing a lawful order obligation on every Ethereum, Hyperliquid, Solana, and Layer 2 validator... The predictable result would be that U.S. validator stakes migrate offshore, U.S. block-building operations relocate, and the U.S. share of the chain validator base shrinks."

Translation: Write this rule wrong and you push America's entire blockchain infrastructure offshore. 🔴

The government's stated goal is to keep innovation in the US. This filing says: then write the rule this way, not that way.

5. The Fifth Circuit is already on their side:

The filing cites Van Loon v. Department of Treasury (2024) — where the Fifth Circuit ruled that smart contracts are neither "property" nor "services" under sanctions law.

Treasury didn't appeal to the Supreme Court.

Now OFAC is trying to regulate third-party USE of those same smart contracts — which the filing argues is directly contradicting what the court already decided. ⚖️

Mainstream narrative: "DeFi protocols want zero regulation — they're trying to stay offshore and avoid oversight."

This filing destroys that narrative.

Hyperliquid Policy Center is actively engaging FinCEN, citing specific statutes, submitting formal comments, and providing contact information for follow-up questions.

That's not the behavior of a protocol avoiding regulation.

Opinion/interpretation: That's the behavior of a protocol that believes it can WIN within a regulatory framework — IF that framework is written correctly.

The difference between "no regulation" and "smart regulation" is exactly what this filing is trying to define.

The GENIUS Act already excluded DeFi developers from "digital asset service provider" obligations. Congress drew that line deliberately.

This filing is asking FinCEN and OFAC to respect the line Congress drew — and not accidentally erase it in the implementing rules.

The question now: Will regulators listen?

The comment period is open. The precedent exists. The legal argument is made.

What happens next determines whether the world's most active on-chain exchange can eventually serve American users directly — or remains offshore indefinitely. 🎯

⚠️Not legal or financial advice. Always DYOR.

2

3

492

Jun 9

You can legally bet on the 2026 World Cup with $1 — or $1 million. No casino. No sportsbook. No bank account needed.

Just USDC and a crypto wallet. 🤯

This is Hyperliquid's HIP-4 prediction market. Live right now.

Over $2.1M in real money is already sitting in sports markets:

⚽ World Cup Champion: $1.21M OI

🏀 NBA Finals: $900K OI

France 17% · Spain 17% · England 11%.

Knicks 63% vs Spurs 37%.

These aren't odds from Vegas. They're set by real money from real people — globally, 24/7. 📊

The settlement rules are public, permanent, and on-chain.

FIFA's official result decides the winner. Hard deadline: Oct 14, 2026.

No company can change it. No casino can "adjust" the outcome after the fact. Just code. Just validators. Just facts. ⚙️

Mainstream take: "sports betting has nothing to do with DeFi."

The on-chain reality: HIP-4 lets anyone — Indonesia, India, Brazil — trade the World Cup in USDC, without a brokerage, without a bank, without asking permission.

Opinion/interpretation: This is prediction markets finding real product-market fit. Not in theory. In production. Today.

Global sports betting market: ~$200B annually.Hyperliquid sports OI today: still in the millions.

The gap is either the opportunity — or a ceiling.

Which one it becomes depends entirely on one word: regulation. 🎯

⚠️Not financial advice. Always DYOR.

3

2

19

1,835

Jun 9

Coinbase competes with Hyperliquid.

They're both exchanges. Same category. Same customers.

And yet Coinbase just became Hyperliquid's official treasury partner — and voluntarily bought more $HYPE than they were required to. 🤯

When a direct competitor becomes your infrastructure layer and buys your token on top of the minimum required — that's not a business deal. That's a structural bet on who wins the next era of finance.

Here's what actually happened, step by step 👇

The old reality:

Hyperliquid held $5.5B in USDC generating approximately $220 million per year for Circle — money that flowed entirely outside the Hyperliquid ecosystem.

The protocol generated the users. The protocol built the platform. But the yield from sitting capital went elsewhere. Entirely.

The new structure under AQAv2:

Coinbase is now the official treasury deployer, sharing the vast majority of USDC reserve yield revenue back to the Hyperliquid protocol. Circle handles the technical side — CCTP and native cross-chain infrastructure.

Both Coinbase and Circle have committed to stake HYPE tokens to activate AQAv2. Coinbase has also increased its staked HYPE position beyond what the activation requires.

That last sentence matters. The minimum was already set. They chose to go above it.

The on-chain proof:

Two wallet addresses from the official @coinbase account — publicly posted, publicly verifiable:

0x4E5319dEb1072B01439EE674db5C321d11fd96F8 0xc20699185c15D0a2fD65779BB5d69f5b0B113c00

No back-room deal. No rumor. On-chain. Permanent.

What $5B USDC means in yield math:

At ~4% annual rate: $5B × 4% × ~90% to protocol = ~$180M/year in new protocol revenue (illustrative estimate — actual AQA rate is set on-chain, subject to change)

That's on top of Hyperliquid's existing ~$800M in trading fees. 📊

Mainstream narrative: "This is just a Coinbase partnership — good for exposure, nothing structural."

The counterintuitive read:

Coinbase is the co-founder and preeminent distribution partner of USDC. This isn't a PR partnership — it's Coinbase placing its core product (USDC) inside Hyperliquid's core infrastructure, permanently.

When you embed your primary revenue asset into a competitor's ecosystem AND buy their token voluntarily, you're not managing a PR moment. You're making a directional bet that this platform's liquidity will matter at scale — and you want to be positioned inside it before that happens.

Opinion/interpretation: The "skin in the game" signal here is unusually strong for a corporate announcement. Companies don't voluntarily over-stake a competitor's token unless they genuinely believe in the platform's trajectory.

Before AQAv2: $220M/year in yield left the ecosystem.

After AQAv2: majority of that yield stays — to buy $HYPE.

As Coinbase CEO Brian Armstrong put it: "USDC is becoming the standard across crypto markets. Coinbase is deploying USDC on HyperliquidX to help grow the ecosystem and scale how capital moves."

The question worth sitting with:

If Coinbase — your direct competitor — is voluntarily deepening its financial exposure to your platform...

What do they know about where this is going? 🎯

⚠️Not financial advice. Always DYOR.

Jun 8

Coinbase is now the official deployer of @HyperliquidX's USDC treasury wallet.

We will be activating AQAv2 from the two addresses below:

0x4E5319dEb1072B01439EE674db5C321d11fd96F8

0xc20699185c15D0a2fD65779BB5d69f5b0B113c00

9

14

142

17,511

Jun 8

During the worst crypto week of 2026 — $HYPE just quietly overtook both BNB and Solana in total value locked.

While being valued at 17% of BNB's market cap. 🤯

TVL measures how much real capital people are actively trusting a platform with.

When one chain holds more capital than two giants — but is priced at a fraction of their value — the gap is either an opportunity or a warning.

The data forces you to decide which.

Numbers directly from hl.eco/tvl-vs-chains, June 8, 2026. Crosscheck via DeFiLlama.

Total Value Locked — right now:

🟢 Ethereum: ~$37.4B (#1)

🟢 Hyperliquid: $5.92B (#2) ← new

🟡 BNB: $5.17B

🔵 Solana: $4.86B

One month ago, Hyperliquid was below both BNB and Solana. Today it's above both. 📈

The MCAP/TVL valuation gap:

Chain TVL Market Cap Ratio HYPE $5.9B $14.0B 2.36x SOL $4.9B $38.2B 7.86x BNB $5.2B $80.4B 15.54x

HYPE holds more capital than both SOL and BNB. Yet the market values it at 17% of BNB and 37% of SOL.

Mainstream narrative: "HYPE is down 20% from ATH, it's losing momentum."

The TVL chart tells a different story.

While price declined and broader crypto bled, the amount of real capital being actively deposited into Hyperliquid kept growing — not falling.

Opinion/interpretation: This divergence between price and TVL is unusual. Typically in a bear market, TVL and price move in the same direction — both down. When TVL grows while price drops, it suggests users are still choosing to put their money there regardless of short-term price action.

Whether this TVL growth sustains if the bear market deepens is genuinely unknown. TVL can reverse quickly.

The uncomfortable question the data raises:

BNB has 6.5x more TVL-per-dollar of market cap pricing than HYPE.

Either the market is pricing in massive risks for HYPE that TVL alone doesn't capture — or it hasn't yet caught up to what the on-chain data is showing.

One of those two things has to be true. 🎯

⚠️Not financial advice. Always DYOR.

2

5

45

2,531

Jun 7

$1.14 billion worth of $HYPE moved on-chain yesterday.

It wasn't sold.

Every single dollar was restaked — spread across 11 validators instead. 👀

When a team redistributes $1.14B of its own stake instead of selling, that's the most credible on-chain signal of conviction — and it doubles as a direct decentralization action.

June 6 is Hyperliquid's monthly unlock date — running since January 2026.

Although $675M worth of HYPE was scheduled for the June 6 cliff, the team committed to claiming only $38M. The rest stays locked.

The 18.88M HYPE (~$1.14B) that moved on-chain wasn't distributed to the market.

On-chain data shows it was redelegated FROM the team's self-custody TO 11 separate validator nodes — including CMI, HypurrCorea, ASXN, Imperator.co, ValIDAO, and others. ⛓️

All transactions executed within a 3-minute window at 6:57–7:00 PM on June 6.

This is visible, verifiable, and permanent on Hyperliquid's L1.

The mainstream narrative on unlock days: "Team tokens unlocked = sell pressure incoming."

The on-chain reality on June 6: Zero sell pressure from this move.

Redelegation ≠ liquidation.

The tokens never left staking. They moved from a single point of control to 11 different validators — each with different operators, geographies, and communities.

Hyperliquid's consensus requires greater than two-thirds of total staked HYPE to commit rounds. Distributing team stake across more validators directly reduces single-point-of-failure risk in the consensus layer.

Opinion: Most projects talk about decentralization. This team executed $1.14B worth of it in 3 minutes — transparently, on-chain, verifiable by anyone. That's a different category of action.

The question worth asking:

If the team wanted to sell — June 6 was the perfect day. Unlock day. Market already down. Easier to hide in the noise.

They chose to restake instead. 🎯

Whether that reflects genuine long-term conviction or is simply the rational move given vesting constraints — only time and future on-chain data will tell.

But the ledger doesn't lie.

Check the hashes yourself. 🔍

⚠️Not financial advice. Always DYOR.

15 hours ago, the team unstaked 18.88M hyperliquid:native, worth approximately $1.14B, and redelegated it across 11 validators.

10

15

146

16,184

Jun 7

One of these assets crashed -38% today.

The rest just followed the market.

Only one of them had a 4-year-old hidden bug exposed. 🤯

Can you spot which one?

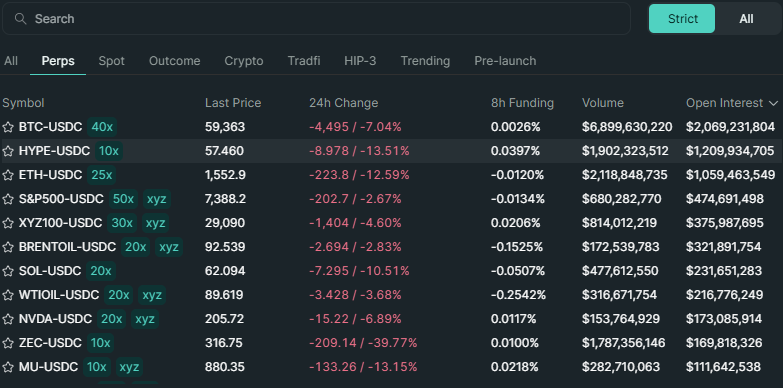

One screen. Nine assets. Two completely different stories. 👇

Story 1: The macro sell-off

This is crypto's worst week since July 2024.

The culprit: US spot Bitcoin ETFs saw net outflows of over $3 billion across 10 consecutive trading days. Combined with geopolitical tension and whale selling, BTC touched near $60,000.

Everything in that screenshot bled red because of this. 📉

BTC -6.4%. ETH -12%. SOL -8.6%. HYPE -15%.

Painful — but explainable. It's the market. 💸

Story 2: The specific catastrophe

ZEC: -38.44%. 🔴

That's not the market.

Zcash plummeted after its founder confirmed a critical 4-year-old bug in the Orchard shielded pool that could have allowed unlimited, undetectable counterfeit ZEC creation. An emergency hard fork fixed it — but the damage to trust was immediate.

On-chain data showed small liquidations relative to the size of the decline — meaning this was spot selling, not a leverage wipeout. Real holders chose to exit. Meanwhile, open interest in ZEC futures climbed to a record high as traders crowded into shorts.

One bad day in the market. One catastrophic disclosure in the project.

The chart looks similar. The reason is completely different. 🎯

Now look at the full picture of what's on this one screen:

🟠 BTC — crypto

🔷 ETH — crypto

🟢 HYPE — crypto

📈 S&P500 — US stock index (xyz)

🛢️ BRENT OIL — commodity (xyz)

🛢️ WTI OIL — commodity (xyz)

💚 NVDA — Nvidia stock (xyz)

🔵 MU — Micron stock (xyz)

🔒 ZEC — privacy coin

One trading platform. Crypto. Stocks. Oil. All in one place. 24/7.

The assets marked "xyz" are community-deployed HIP-3 permissionless markets — anyone can list anything. 🏗️

This isn't a screenshot of a CEX or a stock broker.

This is Hyperliquid. The exchange that didn't exist 3 years ago. 🌍

One final signal most people missed:

Despite HYPE falling -15.15% today — the funding rate is still 0.0366%.

Translation: traders are still net long on HYPE.

People aren't running. They're buying the dip. 💎

Compare that to ZEC — where the funding is negative and OI is at record shorts.

Same red candles. Completely different underlying conviction. 📊

⚠️Not financial advice. Always DYOR.

2

1

5

604

Jun 6

India has 119 million crypto users.

The world's #1 derivatives market.

And until now — zero access to the world's best on-chain exchange. 🤯

That gap just found its answer.

Let's talk about the biggest untapped market in global crypto 👇

India is one of the world's largest crypto markets with approximately 119 million active users — more than any country on Earth.

It's also the largest equity-derivatives market in the world by volume.

A nation of 1.4 billion people — who love to trade, understand risk, and want global access. 📊

So why can't they access Hyperliquid properly?

Three words: tax, friction, timezone.

India imposes a 30% flat tax on all crypto gains, a 1% tax deducted at source on every single trade regardless of whether it's profitable, and losses cannot be offset against gains.

The result? Capital leaves.

India's crypto market keeps growing despite high taxes and regulatory hurdles — proof that demand moves faster than policy.

Most of that demand is now being served offshore — by platforms with zero Indian registration, zero local recourse, and a long history of freezing withdrawals when things go wrong. 🔴

The timezone problem nobody talks about:

The US market opens at 7 PM Indian time.

Runs past midnight.

On a calendar designed for New York.

An Indian investor wanting to trade Apple, gold, or the S&P 500 has had to stay up late, fight currency friction, navigate FEMA RBI SEBI simultaneously, and hope their foreign brokerage doesn't freeze the account. 🌙

What BharatLiquid claims to solve:

BL Labs, an India-based team, has announced BharatLiquid — a platform that routes directly to Hyperliquid's order book, with:

📌 Rupee (INR) deposits and withdrawals

📌 FIU registration in progress

📌 Keys split between user and system — not a shared hot wallet

📌 Every fill verifiable on-chain

Their stated model: not competing with Hyperliquid — routing to it.

Every Indian order adds volume to the same global order book used by institutions worldwide. 🌍

⚠️ BharatLiquid is their own announcement — no independent third-party verification found yet. Verify before using.

Why this structural thesis matters regardless of BharatLiquid specifically:

The gap they're describing is real and validated:

Approximately 119 million Indians actively use crypto, with 72% of investors under 35, and 75% of activity coming from non-metro cities — showing deep grassroots demand far beyond major urban centres.

This population wants to trade the same global markets as everyone else — not a watered-down version of them. 📱

Hyperliquid's architecture — always on, fully on-chain, no closing bell — is structurally better suited for India than traditional finance has ever been.

A market that's open Sunday at 11 PM Bangalore time matters more to an Indian trader than it does to a New York hedge fund. 🕐

The macro signal:

Every time Hyperliquid adds a compliant on-ramp — ETFs in the US, wrappers in Europe, INR routing in India — the same thing happens:

More capital enters the same order book. More fees generated. More HYPE bought back from the market. Automatically. Every day. ♾️

The platform doesn't need to expand.

The world is building the bridges to it. 🎯

⚠️Not financial advice. Always DYOR.

1

1

7

592

Jun 5

The US government just officially legalized the product Hyperliquid built.

And now Hyperliquid might not be allowed to sell it in the US. 🤯

Here's the regulatory paradox nobody is explaining clearly 👇

On May 29, 2026, the CFTC approved Kalshi's BTCPERP — the first bitcoin perpetual futures contract ever listed on a US-regulated exchange. The same day, they cleared Coinbase to route customers to its offshore Deribit affiliate.

Translation: perps are now officially legitimate in America. ✅

The problem? Legitimacy came with a rulebook.

And Hyperliquid wasn't written into it. 📋

What "regulated perps" actually requires:

Kalshi's approval came with strict conditions — leverage limits, volatility controls, and full KYC requirements. Hyperliquid's entire value proposition — self-custody, no identity checks, high leverage, permissionless long-tail markets — is largely what a CFTC-regulated venue cannot match.

The regulator built a cage. Hyperliquid was built to live outside it. 🔓

The 5 paths forward — explained simply:

A legal analyst at @collab_currency (disclosed: HYPE holder) mapped out every option. Here's the summary:

Path 1 — Go full offshore:Stay global, block US users aggressively. Lose US institutions. Keep everything else. (Binance main exchange model) 🌍

Path 2 — Build "Hyperliquid US":Create a separate regulated wrapper for US users. Ring-fence funds, products, and HYPE value capture. Most ideal — but requires massive structural rewrite. (Binance US model) 🏛️

Path 3 — Decentralize under Clarity Act:Progressively reduce team control until HYPE qualifies as a commodity, not a security. Big upside — but would slow down the fast product decisions that MADE Hyperliquid great. ⚖️

Path 4 — Go corporate, make HYPE a security:Cleanest compliance path. Most damaging to everything HYPE stands for. Considered the weakest option strategically. 🏢

Path 5 — Lobby for a new framework:Work with regulators to create bespoke rules for crypto-native perp venues. Long-term play. Already in motion via @HyperliquidPC. 🗳️

The wrinkle that changes everything:

Hyperliquid's self-custody model, permissionless markets, and offshore structure cannot be replicated under CFTC-regulated infrastructure without fundamentally changing the product.

But here's the flip side most people miss:

USDC — Hyperliquid's primary settlement asset — is managed by Circle and Coinbase, two US-regulated entities.

That means whether Hyperliquid wants it or not:

US regulatory reach already exists at the asset layer. 🔗

This could be a constraint. Or it could be the exact leverage needed to negotiate a bespoke framework. The outcome depends entirely on how this dynamic is used.

The honest institutional read:

Whether you're bullish or bearish on Hyperliquid's US future comes down to two questions:

1️⃣ Which of the 5 paths do you think they'll actually take?

2️⃣ Can Hyperliquid remain dominant after adapting to whichever path they choose?

The product is world-class. The regulatory challenge is real.

Both things are true at the same time. 📊

⚠️Not financial advice. Always DYOR.

Jun 4

hyperliquid is a killer product

meanwhile, there are pressures that may constrain the project’s viability within US borders

including:

- hyperliquid’s product layer (via CFTC’s kalshi approval, coinbase/deribit no action, and policy statement)

- hyperliquid’s network and token layer (via clarity act)

- hyperliquid’s collateral layer (via USDC, managed by circle/coinbase, two US regulated entities)

haven’t seen a thorough discussion on these impacts, so below is a brief summary of the current paths forward, and the rationale behind each:

(1) hyperliquid can ignore US market, go offshore only

(2) hyperliquid can build a US regulated wrapper

(3) hyperliquid can decentralize under ‘clarity act’

(4) hyperliquid can centralize the project, turn $HYPE into a security

(5) hyperliquid can lobby for a change

these are the five, i'll start with the first

(1) hyperliquid can ignore US market, go offshore only

last week the CFTC approved kalshi’s BTCPERP as a futures contract on a DCM

the CFTC separately confirmed certain deribit perps may be treated as foreign futures through the coinbase FCM path

the implication is that regulated distributors for perps in the US may need a fully regulated venue, compliant customer funds path, approved product scope, surveillance, disclosures, and accountable corporate counterparties

without these in place

distributing hyperliquid liquidity, or offering hyperliquid perps, could look like routing US customers into an unapproved offshore venue

so the first option for hyperliquid is that they ignore the US market entirely

this approach would be similar to binance main exchange, which was ultimately forced to more aggressively block american customers after years of light effort

like binance, doing so would preserve hyperliquid’s product offshore, but cede US institutional access for the time being

(2) hyperliquid can build a US regulated wrapper

the second path is to find a way to build or partner with a US regulated wrapper to offer perps

under this path, offshore hyperliquid would remain a global crypto native venue, while a separate US affiliate or partner offers regulated perps through an FCM/DCM/DCO/FBOT style wrapper

you can think about this separate venue like Hyperliquid US™

in a perfect world, this is the ideal outcome for hyperliquid to target US users

however, this approach would likely require hyperliquid to ring fence (1) customer funds, (2) products, and (3) $HYPE value capture separate from the main network

the ongoing separation of Binance US™ from Binance’s main exchange is instructive here as a case study

- customer funds may be ring fenced because US regulated futures infrastructure cannot commingle US customer collateral with offshore protocol margin

- products may be ring fenced because the US venue will likely require approved, deep, liquid digital commodity perps, not the entire hyperliquid long tail universe of assets

- revenue and $HYPE value capture may be ring fenced because profits from a regulated corporate venue flowing into buybacks, burns, or assistance fund mechanics starts looking like token holders are economically participating in the profits of a corporate operating business, which could implicate US securities laws

net net, this model would likely require a significant rewrite of how the hyperliquid network works for US participation

(3) hyperliquid can decentralize under ‘clarity act’

the clarity act drafts offer a groundbreaking path for a lot of protocols to ‘progressively decentralize’ a network

i'll be writing more on this down the road

but for now

under clarity, progressive decentralization means reducing the role of the originator / related parties until the network and token are no longer under ‘coordinated control’

in exchange, a token may exist to capture *automatic* revenue flows originating out of the decentralized network, as long as the token value is primarily driven by the distributed ledger system rather than entrepreneurial or managerial efforts by a control group

in a vacuum, a token powering a decentralized network may support shifting the token’s classification from “security” to “commodity”

which is a big deal for many protocols and networks in the US

however, there are tradeoffs for projects optimizing for the ‘decentralization’ route

for hyperliquid, decentralization under clarity would likely mean the project would need to aggressively broaden validators, decentralize the listing process, decentralize oracle/risk controls, reduce controlled ownership, reduce emergency discretion decisions, make upgrades slower and more governance driven, among offloading other day to day product decisions

this would be a meaningful change, as a large part of the hyperliquid thesis has been underwriting the core team’s ability to make fast product decisions, in a manner they see best

ceding managerial control over the protocol to satisfy decentralization changes the trajectory of the project, and shouldn’t be taken lightly

this also coincides with a separate issue

the clarity act’s decentralization framework is not a DCM/DCO workaround. even if the hyperliquid network could eventually satisfy clarity’s decentralized governance framework, this would still not automatically permit hyperliquid to offer perps directly to US users

notably, both clarity and the ag committee text for clarity preserve the existing commodity exchange act (CEA) regime for futures, swaps, options, and leverage transactions

this is important for understanding clarity's intent, as the ag committee writes the CFTC/CEA side of market-structure legislation and this text signals that clarity act legislation is not a workaround for the existing CEA derivatives regime

simply put

this likely means any decentralization for hyperliquid will *not* erase the need to follow regulated derivatives market infrastructure without a regulated wrapper, which would require a significant rewrite of how hyperliquid works for US participation

(4) hyperliquid can centralize the company, turn $HYPE into a security

this is probably the weakest option game theoretically, but worth mentioning

hyperliquid could become a corporate exchange, register or restructure $HYPE into a security, build a regulated wrapper, and shift value capture away from token buybacks/burns and toward equity, licensing, or regulated-entity revenue

this is the cleanest for compliance because the entity, venue, governance, customer funds, disclosures, and revenue flows become legible to US regulators *today*

but it is the most damaging to the network value prop, which relies on the idea that protocol activity, incentives, and economics are all aligned around $HYPE as a digital commodity, not a tokenized security

(5) hyperliquid can lobby for a change

there is a fifth option, which is to lobby for a change

here, related organizations could work hard to lobby the agencies to eventually create a bespoke framework for crypto-native perp venues like hyperliquid to directly target US audiences and capital

the work being done here by @HyperliquidPC is instructive

there is some evidence this approach could work in part

the CFTC is clearly moving in a more innovative direction, and the kalshi / coinbase-deribit path may be the first conservative step before more liberal steps to include more unique design architectures

important to consider, however

even if the CFTC further opens up on perps to tailor approvals for decentralized networks

this wouldn’t solve a $HYPE securities classification under the clarity act, which is a separate issue that may require network changes before US participation

without these changes

and under a current reading of clarity

i do find it impractical to think there will be a special token exemption for one project, while other projects are required to satisfy clarity act’s decentralization / network token framework

ok

in closing

these are the five US options as i currently see it, i'd be curious if folks in the legal / policy community are seeing others

there is also one final wrinkle, which is USDC now serving as hyperliquid’s ‘aligned quote asset’, with coinbase/circle tied into the broader treasury and routing strategy

a final point on this

if hyperliquid’s core settlement asset is USDC, then the system unquestionably inherits some degree of US regulatory control at the asset layer

but it also opens up a unique opportunity for significant policy shifts to support extending USD dominance, as flagged by @blknoiz06

its an interesting dynamic worth keeping an eye on for policy reasons

i hope some of this discussion is useful for further dialog

as of today

whether you are bullish or bearish on hyperliquid’s US efforts from here probably depends on two things:

(1) what probability you assign to each of these paths; and

(2) hyperliquid’s ability to compete once they end up on one of these paths

disclosure: my fund @collab_currency currently has exposure to $HYPE and projects building in the hyperliquid ecosystem

1

2

342

Jun 5

A bug existed inside Zcash for 4 years.

Nobody knew.

And because of how privacy technology works — nobody can ever fully prove what happened during those 4 years. 🤯

This is a pure security analysis of what just happened to $ZEC. No hype. Just facts. 👇

What is Zcash, and why does security matter so much?

Zcash is a cryptocurrency built on one core promise: mathematical privacy.

Unlike Bitcoin — where every transaction is visible to anyone — Zcash uses something called zero-knowledge proofs (ZK proofs) to shield transactions completely.

You can prove you have money without revealing how much, to whom, or from where. 🔐

This makes ZK proof integrity the entire foundation of ZEC's security model.

If the math breaks — everything breaks.

What happened on May 29, 2026:

Security researcher Taylor Hornby discovered a critical soundness bug in the Orchard shielded pool's zero-knowledge proof circuit during an independent protocol audit for Shielded Labs. He responsibly disclosed it to the Zcash Open Development Lab within hours.

In zero-knowledge proof systems, "soundness" is the property that ensures only valid transactions and state transitions are accepted by the network. A soundness vulnerability means the system could be tricked into accepting something it should have rejected.

In plain English: the mathematical referee that validates every Orchard transaction could be fooled. 📋

The AI angle nobody expected:

Hornby used Anthropic's Claude Opus 4.8 model to write a working exploit — and successfully generated counterfeit ZEC in a local test environment.

The implication: AI-assisted security research can now discover vulnerabilities that human cryptographers missed for years.

This is both good news (found before attackers) and a warning — the attack surface for cryptographic protocols just expanded. 🤖

How bad was it technically?

A successful exploit could have allowed an attacker to forge transactions and double-spend funds within the Orchard pool. It could NOT, however, inflate the total ZEC supply.

This distinction matters:

❌ What it COULD do: Double-spend ZEC within the Orchard shielded pool

✅ What it COULDN'T do: Create brand-new ZEC out of thin air from nothing

Still serious — but not a supply hyperinflation event. 📊

The emergency response — how the team handled it:

Phase 1: Emergency soft fork activated June 2 at block 3,363,426 (~02:00 UTC) — completely freezing Orchard transactions to prevent any exploitation window. P

hase 2: Hard fork NU6.2 activated June 3 at block 3,364,600 with corrected circuit code. Total response time: roughly 5 days from discovery to patched network.

A hard fork was necessary because a zero-knowledge proof circuit fix requires a completely new pinned verifying key — you cannot simply patch it like regular software.

Five days. Emergency coordination. New cryptographic key. All while the vulnerability remained undisclosed to the public.

That is genuinely fast execution for a cryptographic emergency. ✅

The core unsolvable problem:

Due to Orchard's privacy-oriented nature, it is cryptographically impossible to prove whether the vulnerability had already been exploited before it was patched.

This is the fundamental paradox of privacy technology.

The same feature that makes Orchard transactions invisible to surveillance — makes them invisible to auditors too.

You cannot prove it was exploited. You cannot prove it wasn't.

The privacy is absolute — including the privacy of any potential attacker. ⚖️

How long was the risk window open?

This vulnerability existed since the Orchard pool launched in May 2022 — meaning it sat undetected for 4 years across every version of zcashd from v5.0.0 through v6.12.3, and all versions of halo2_gadgets prior to v0.5.0.

Four years. Every cryptographer who reviewed the codebase missed it.

It took an independent security researcher using an AI model to finally find it. 🔍

Is this a new pattern or a one-off?

In 2019, the team disclosed a similar counterfeiting vulnerability in the older Sprout shielded pool that had also gone undetected for years. That bug was also never known to have been exploited. The market responded with confidence rather than panic — ZEC climbed above $600 during the upgrade window.

Bitcoin developer Peter Todd also cited this incident as a warning against integrating Zcash-style privacy into Bitcoin, highlighting the high cryptographic risk inherent in ZK-proof systems.

Two critical bugs in two separate privacy pools. Both found years after deployment. Both fixed via emergency hard fork.

The question the industry is now asking: Is this a pattern intrinsic to ZK-proof complexity? 🧠

What happens next — the supply integrity challenge:

Shielded Labs proposed a network upgrade to allow public verification that ZEC supply hasn't been secretly inflated — implementing a "turnstile accounting" mechanism for all Orchard pool tokens. Detailed plans are expected to be released imminently.

This is the critical test for Zcash's credibility going forward.

If the turnstile mechanism can demonstrably prove supply integrity for the 4-year window — the trust problem becomes manageable.

If it cannot — the philosophical gap between "probably fine" and "mathematically provable" remains open forever. 📐

The institutional security verdict:

What the evidence supports:

✅ Team responded fast and transparently — 5-day emergency response

✅ No confirmed exploitation detected on-chain

✅ Patch is live and verified

✅ Historical precedent (2019) shows recovery is possible

✅ Bug found through PROPER audit, not active attack

What the evidence cannot resolve:

❌ 4-year undetected window — inherently unauditable due to privacy design

❌ ZK-proof complexity creates recurring blind spots — now twice documented

❌ Supply integrity for historical period: mathematically unprovable without new mechanism ❌ AI-assisted exploit writing lowers the barrier for future attackers discovering similar bugs first

The bottom line:

Zcash is not broken. It is not a scam.

But this event reveals something fundamental about advanced cryptographic systems: the more powerful the privacy, the harder it is to audit — and the longer bugs can hide.

The open question for Zcash is whether it can ship a supply proof convincing enough to retire the doubt that a private pool can never fully dispel.

That answer will determine whether this is a speed bump — or a structural turning point. 🎯

⚠️Not financial advice. Always DYOR.

1

2

5

557

Jun 4

77,000 users.

That's it. That's Hyperliquid's daily user count.

Solana has 2,300,000. 🤯

Yet one metric just ranked Hyperliquid 5x above Solana in growth quality.

Same data. Completely different story.

Let me show you something that changes how you think about crypto metrics 👇

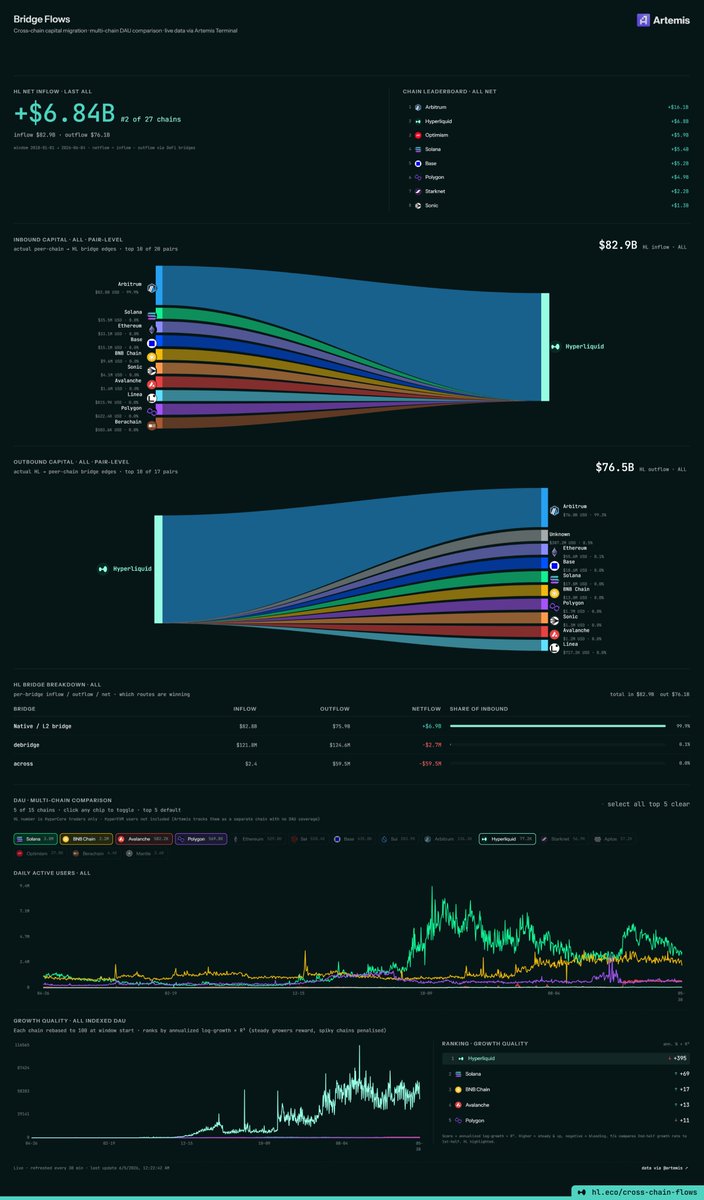

This is the Artemis Bridge Flows dashboard.

It tracks every dollar moving between blockchains from 2018 to today.

The question it answers: where is capital actually going and staying? 💰

The capital leaderboard since 2018:

All-time net capital flows across 27 chains:

🥇 Arbitrum: $16.1B

🥈 Hyperliquid: $6.84B ← born 2024, already #2 🥉 Optimism: $5.9B

4️⃣ Solana: $5.4B

5️⃣ Base: $5.2B

6️⃣ Polygon: $4.9B

Hyperliquid has existed for less than 3 years.

Every other chain on this list has been around 5-9 years.

$6.84 billion in permanent capital. Ranked #2. In under 3 years. 🚀

What does "net inflow" actually mean?

Think of it like a city's population growth.

People move in (inflow). People move out (outflow).

Net = who actually STAYED.

Hyperliquid: 📥 $82.9B came in 📤 $76.1B left 🏦

$6.84B stayed permanently

Capital that stays = capital that trusts. 📋

Now here's the part that breaks the narrative:

Hyperliquid has 77,200 daily active users.

Compare that to:

👥 BNB Chain: 2,300,000 DAU

👥 Solana: 1,700,000 DAU

👥 Polygon: 865,800 DAU

👥 Avalanche: 183,200 DAU

Hyperliquid is near the bottom in user count.

Yet it's #2 in permanent capital.

How? 👇

The answer is in the Growth Quality metric.

Artemis ranks chains by annualized log-growth R² — a formula that specifically rewards steady, consistent growth and penalizes chains whose numbers spike and crash.

The ranking:

🟢 Hyperliquid: 395

🔵 Solana: 69

🟡 BNB Chain: 17

🔴 Avalanche: 13

🟣 Polygon: 11

Hyperliquid's growth quality score is 5.7x higher than Solana.

23x higher than BNB Chain. 🤯

This isn't viral growth. It isn't bot traffic. It isn't airdrop farmers.

It's genuine, sustained, compounding adoption — the rarest thing in crypto. 📈

The user quality gap explained:

77,000 Hyperliquid users generate:

$800M annual fee revenue

$6.84B in permanent capital retained

$250B monthly trading volume

1,700,000 Solana users generate less capital retention.

Each Hyperliquid user brings ~$88,800 in net capital.

Each Solana user brings ~$3,176 in net capital.

The difference in capital per user? 27x. 💎

One important transparency note:

⚠️ The dominant Arbitrum inflow (99.9% of HL's inflows) is largely the USDC bridge route — most USDC enters Hyperliquid through the Arbitrum-bridged USDC pathway. This is a technical infrastructure fact, not "99.9% of users coming from Arbitrum." The net capital signal ($6.84B retained) remains valid regardless of which bridge route was used.

The institutional read:

When capital moves into a chain and stays — that's conviction.

When that conviction builds steadily without spikes — that's structural demand.

When 77,000 users retain more capital than chains with 30x more users?

That's capital quality over capital quantity. 🏗️

This is what institutions see when they look at Hyperliquid.

Not the user count.

The money that never left. 🎯

⚠️Not financial advice. Always DYOR.

6

7

50

2,845

Jun 4

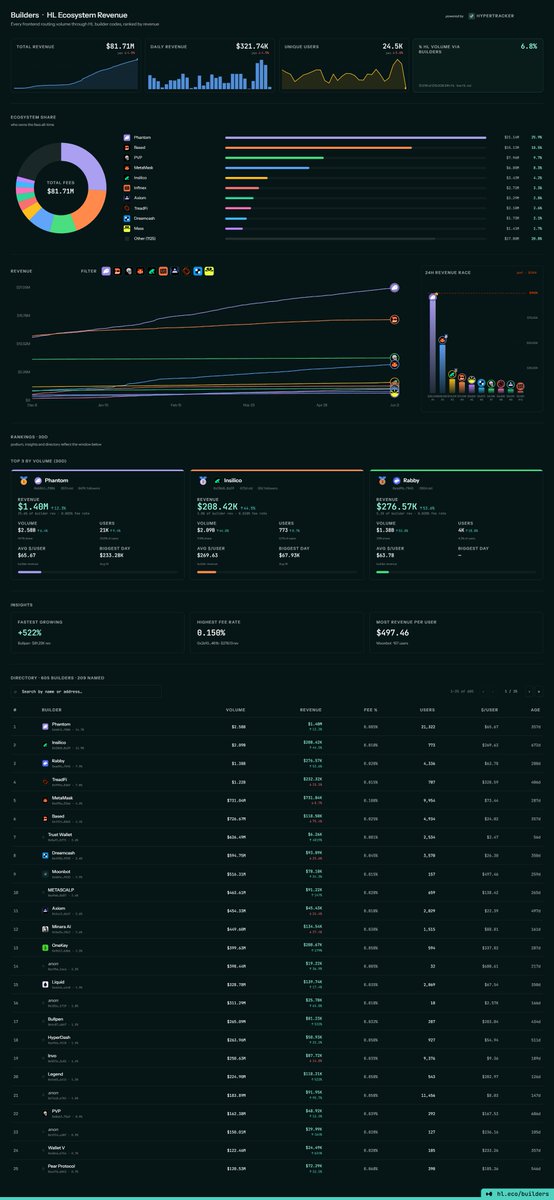

605 companies built a business on top of someone else's exchange.

Nobody gave them permission. Nobody asked them to. They just... did. And made $81 million. 🤯

Here's something that breaks the traditional business model entirely 👇

On every normal financial platform — NYSE, Binance, Coinbase — only ONE company makes money.

The platform. On Hyperliquid?

605 builders are running their OWN businesses on top of the same infrastructure.

Each one keeping their own slice of the fees. 💰

Let me show you the actual numbers.

Total Builder Ecosystem Revenue (all-time): $81.71M

Daily builder revenue right now: $321.74K/day

Unique users going through builders: 24.5K 📊

And here's the breakdown of who's winning:

🥇 Phantom — $1.40M revenue, 21,322 users

🥈 Insilico — $208.42K revenue ( 44.5% growth)

🥉 Rabby — $276.57K revenue ( 53.4% growth)

These aren't Hyperliquid employees.

They're independent teams — wallet apps, trading tools, analytics platforms — that plugged into Hyperliquid's infrastructure and started earning fees from their own users.

Now here's what most people don't understand about why this matters:

Think of it like an App Store. 📱

Apple built the phone and the operating system.

But 99% of the apps you actually USE were built by outside developers.

Those developers make money. Apple makes money. Users get better products. Everyone wins.

That's exactly what's happening on Hyperliquid — but for financial markets.

The fastest growing builder in the ecosystem just posted 522% growth. 🚀

One builder earns $497.46 per user — the highest revenue-per-user in the entire ecosystem.

And there are 605 builders total — with 396 still anonymous, building quietly in the background.

What does this signal structurally?

When builders earn real money from a platform — they have financial incentive to:

✅ Keep improving their products

✅ Bring MORE users to the ecosystem

✅ Stay on Hyperliquid instead of switching to competitors

Every new user a builder acquires → becomes a Hyperliquid user → generates protocol fees → funds $HYPE buybacks 🔄

The builders are doing Hyperliquid's marketing and distribution FOR FREE.

Because they profit from it too.

The institutional read here:

Right now, builder volume = only 6.8% of total HL volume.

Meaning 93.2% of Hyperliquid volume still comes through the native interface.

605 builders. 6.8% market penetration.

If builder penetration grows to 20%... 30%... even 50% of volume?

The builder revenue goes from $81M to $500M .

And every dollar of that activity still runs through Hyperliquid's core infrastructure — generating protocol fees, generating buybacks, generating demand for $HYPE. 🎯

The platform didn't build an exchange.

They built a financial operating system.

And 605 companies are already paying to run on it. 🏗️

⚠️Not financial advice. Always DYOR.

2

2

14

782