Working in Private Equity. Finland. SME Growth

Joined July 2013

- Tweets 282

- Following 932

- Followers 524

- Likes 32,503

29 Photos and videos

Jan 19

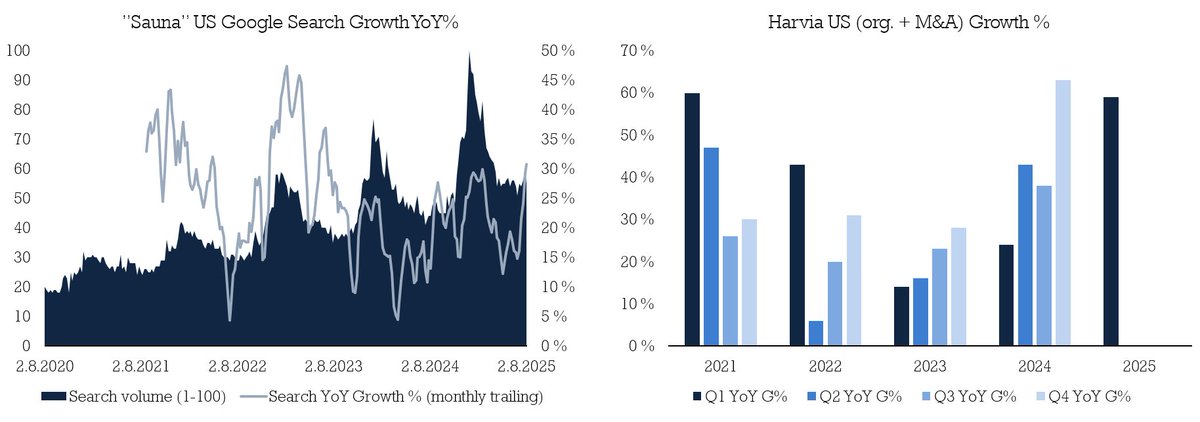

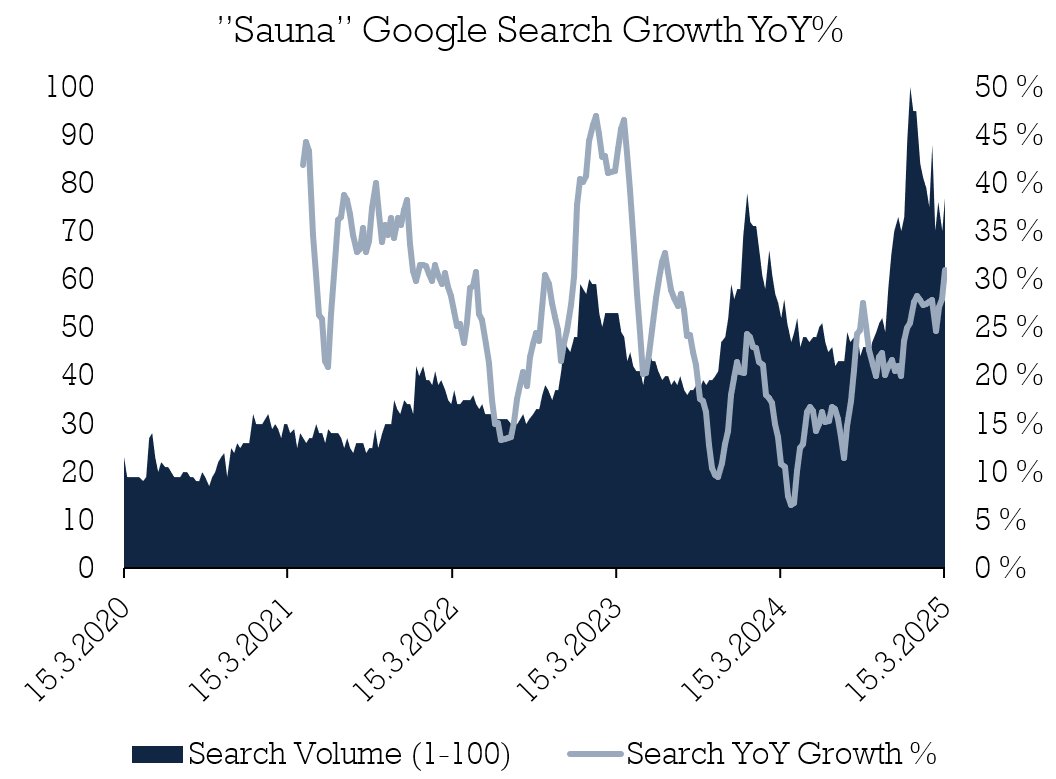

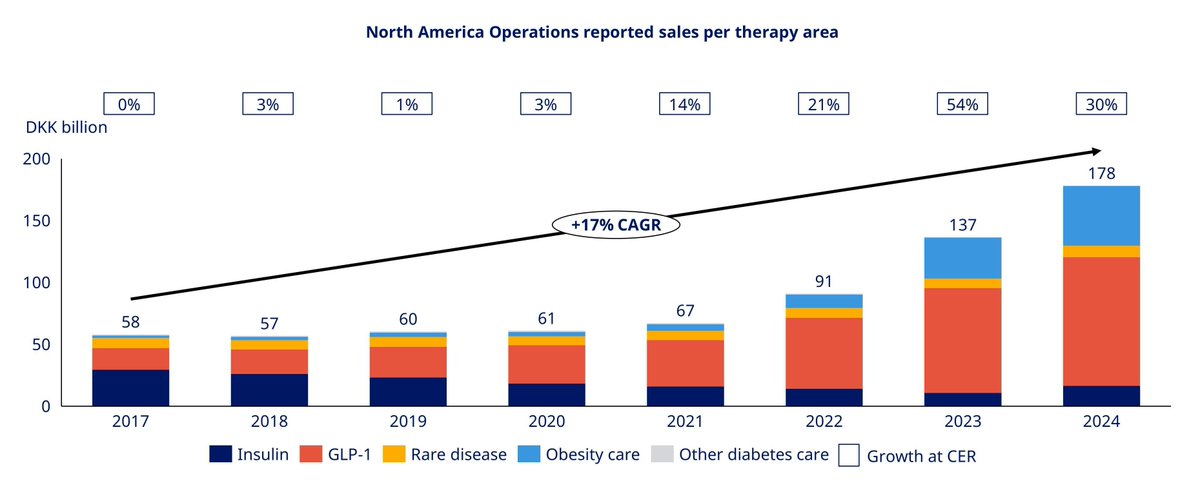

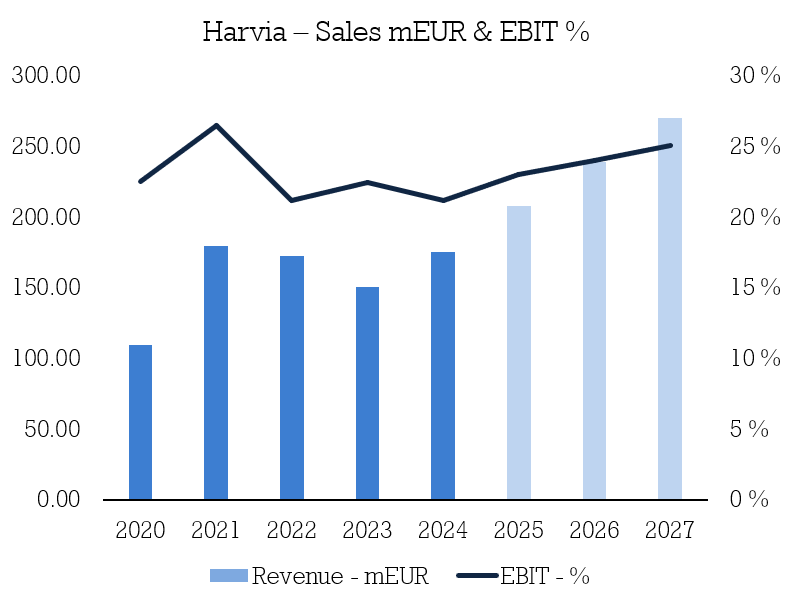

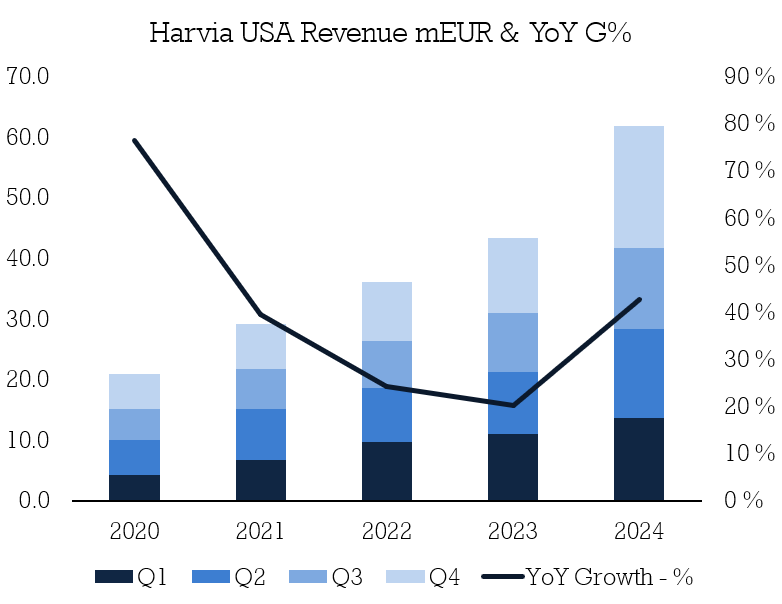

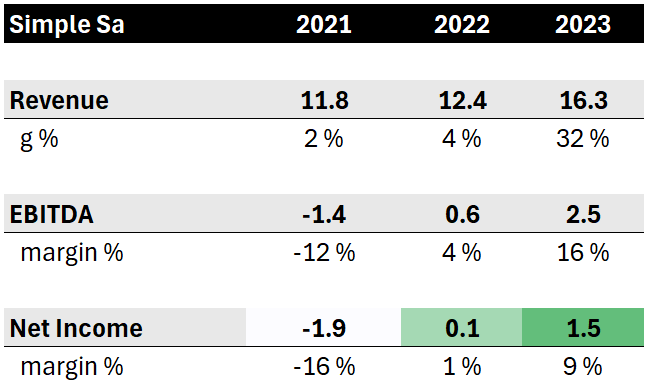

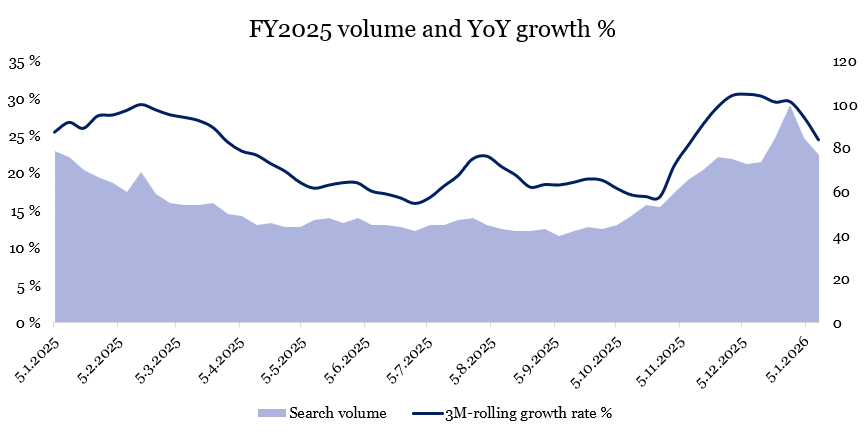

$HARVIA Based on "sauna" search data, growth was over 30% YoY on all weeks of Q4 in US. Despite tariff concerns and currency headwinds topline should be coming in strong. Japan even stronger and Europe showing return to growth.

2

7

1,200

8 Aug 2025

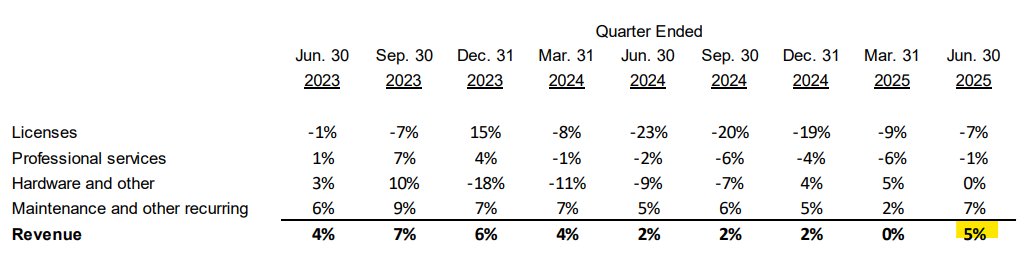

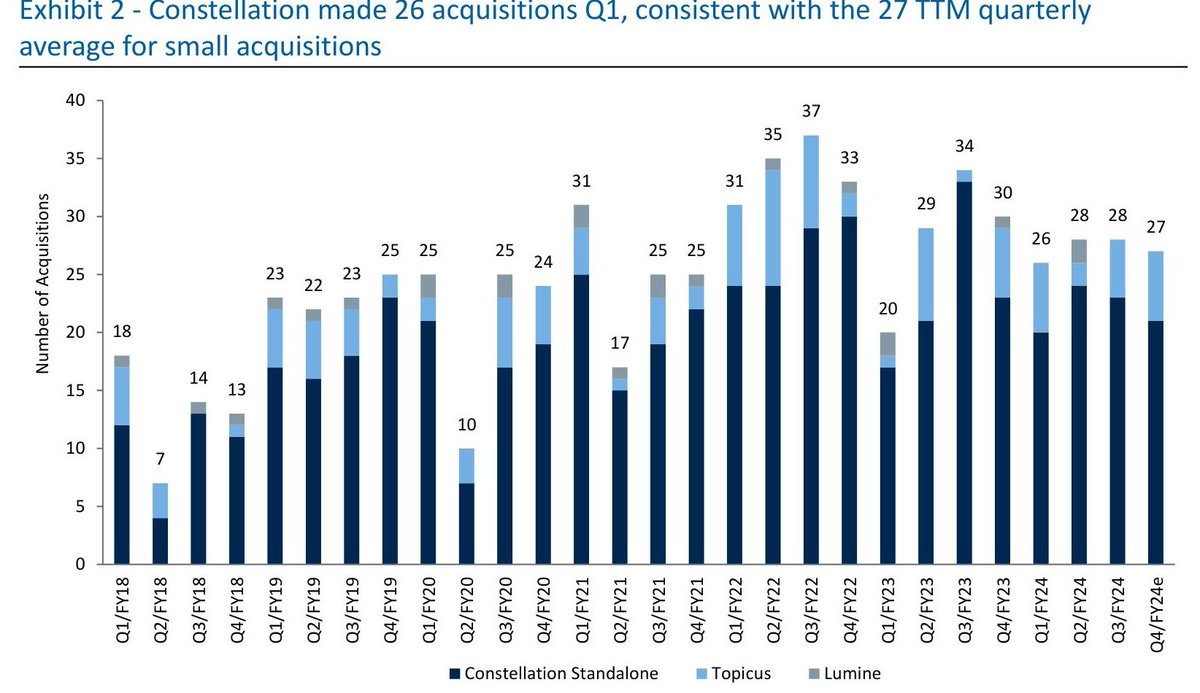

My two key observations from $CSU.TO earnings

1. Last time we saw this high org. growth (5%) was Q42023 (Where is AI disruption of legacy SaaS??)

2. The incremental margins are insane; on Q2 with revenue growing 376M expenses grew 191M those are ~50% incremental EBITDA margins

2

66

7,851

8 Aug 2025

Larger ish M&A for $CSU.TO:

Volaris acquires Useall Software, a provider of enterprise management software to the electric utility sector, manufacturing, and distributors in Brazil.

200 employees

1000 clients

50,000 users

Let's say avg. ARPU $500 this would be $25M rev

1

25

3,003

8 Aug 2025

1

424

7 Aug 2025

Extremely interesting insights from ex Head of M&A at $CSU.TO (Vencora, part of Volaris operating group)

...AI, competition, churn, organic growth, multiples paid, bonus structures, disruption risk, investment modelling and many more... 🔥🔥👀

Tune in, more below

1/x

25

12

182

58,449

7 Aug 2025

THANKS FOR READING HOPEFULLY SOMETHING NEW FOR ALL NEWER AND OLDER $csu.to $toi.v $lmn FANS

@CompTortoise @CJ0pp3l @NotMarkLeonard @bizalmanac

😃

1

14

1,939

7 Aug 2025

"The impact of AI now, at the moment, the threats seem to be toward, I would say, larger, more general horizontal businesses than the smaller niche ones"

1

9

1,404

7 Aug 2025

"Are you going to want to expend resources into developing AI without knowing if it's going to pay off? From a client's perspective, for you to decide to take AI competitor -> significant resources, training, and more importantly, also diverts attention from the business itself"

5

1,358

7 Aug 2025

"a company that provides vertical market software for a handful of golf clubs. This software will provide each golf club the ability to manage the scheduling of its tee times, the collection of membership fees, player handicap tracking, all from a single platform. That is niche"

8

1,358

7 Aug 2025

"They know already the competitors, they know the trends, and it's their responsibility to be up to speed with those. It's very rare for a CHURN to happen"

On AI disruption: 📉

6

1,393

7 Aug 2025

"What that means is that they're probably less prone to want to pay up for an AI model that's unproven at this stage."

"There are businesses at CSU that only have larger blue-chip customers, but I would say it's on average 50/50 between blue-chip and SME."

8

1,387

7 Aug 2025

On stickiness: 🔥

"if you were to rank SaaS according to their functionality, CSU average platform is Tier 3, 4, 5, whereas PE owned ones which they pay up for are Tier 1. CSU are typically legacy software for people or clients who don't want to pay up or can't afford to pay"

11

1,472

7 Aug 2025

"You're responsible for the outcome in the next few years because that's built on the investment that you created. If I put together a 10-year model and put an org. g% of, say, 6% in 10 years, that's going to get shot down by the investment committee. Typically CSU assumes 2-3%"

12

1,486

7 Aug 2025

"Everything at CSU is looked at through a microscope from a financial perspective. Every single investment model and assumption is very heavily scrutinized. Even as an M&A executive, your role there goes way beyond the acquisition when the acquisition is closed."

8

1,506

7 Aug 2025

"Through its track record, it can acquire any business and take it to around 30% profitability in the very short term just by pulling a few levers. This also because the incentive structure, where ROIC is a significant part of every employee's bonus."

14

1,713

7 Aug 2025

"The returns on year one matter significantly. If you think about an acquisition, you put together a discounted cash flow model. That's how Constellation does it. It'll be a DCF model, 10 years, has to meet the hurdle rates, which are very conservative to begin with."

7

1,794

7 Aug 2025

"historically the average multiple that Constellation has bought its businesses for, it's hovered around 1X gross revenue. If you look at it in terms of a net recurring revenue multiple, it's close to like 1.3x, 1.4x. That's very low."

12

1,878

7 Aug 2025

On M&A:

"Small SaaS companies are not educated on M&A. They're too small to sometimes even hire their own advisors. Constellation clearly has an advantage and is able to strong arm them, if you will, in terms of offering a multiple that's more attractive to Constellation itself"

7

1,977

7 Aug 2025

"CSU will acquire just about anything for the right price. It'll look at smaller businesses, restructurings, it'll look at businesses that haven't been growing or that aren't that profitable. Copycats focus on more quality growth businesses since they lack operational expertise."

15

2,423

7 Aug 2025

"If Constellation is competing, all the copycat has to offer at that moment is capital. Constellation has the knowledge, it acquires legacy businesses that have been around for a long time and whose sellers might not be interested in retiring, but they care about the legacy"

12

2,188

7 Aug 2025

"The typical playbook is raise around $20 million to form a holding company and then make a couple of acquisitions, use debt to finance further acquisitions, and then hope that you'll hit a flywheel in a few years. Constellation doesn't see it as much of a threat"

11

2,218