MSCS | MSIT | Pursuing PhD in IT, Tech expert by day, adrenaline-fueled snow trekker. Embracing AI, farming roots

Joined May 2011

- Tweets 1,252

- Following 178

- Followers 312

- Likes 1,093

147 Photos and videos

Pinned Tweet

15 Aug 2023

Just experienced @SoFi virtual assistant firsthand, and I'm blown away! 👏🏼 It's leagues ahead in maturity, efficiency, and speed compared to traditional legacy banks and E-commerce assistants. Major players should take note before it's too late. Kudos to @anthonynoto and the @SoFi team on this achievement. I'm convinced this is just the beginning of something incredible. #FintechInnovation

10

11

114

48,256

Jun 6

This is how market functions.

JP MORGAN HAS RAISED IT’S TESLA PRICE TRAGET TO $475 FROM $145

THIS IS AFTER THE BANK WAS CHOSEN BY ELON MUSK TO BE PART OF THE SPACX AND EARN 100’S OF MILLIONS IN FEES

I HOPE PEOPLE CAN SEE THRU THIS BS

$TSLA

87

May 29

Imagine what happens - if trump tweets “go out there and buy $SOFI”

24

May 27

Big moment for U.S. banking. $SOFI just launched SoFiUSD - the first stablecoin issued by a U.S. national bank, redeemable 1:1 for cash.

Integrated directly into a 15M-member banking app, running 24/7 on $ETH and $SOL.

This isn’t crypto hype this is regulated banking moving on-chain.

Say “hi” to SoFiUSD (SoFiD) 👋

The first stablecoin issued by a U.S. national bank and redeemable 1:1 for cash or cash equivalents. Rolling out now, it’s built for how money moves today: fast, flexible, 24/7.

1

148

May 15

President Trump shared a list of stocks he bought. It shows he traded over $220 million in stocks.

He bought popular tech, aerospace, and finance stocks, including:

•Palantir $PLTR

•Robinhood $HOOD

•SoFi $SOFI

•Nvidia $NVDA

Watch these lists closely because his actions and decisions makes big difference in the market.

247

May 14

Crypto market structure bill has PASSED!

ethereum:native bitcoin:native

1

75

May 13

$JPM JPMorgan files for new tokenized fund on Ethereum.

Finance giant JPMorgan has filed to launch a second money market onchain, adding to a list of major institutions pursuing tokenization of real-world assets. The new fund would be issued on Ethereum and backed by U.S. Treasuries and repurchase agreements. Last week, BlackRock also applied to launch two new tokenized money market funds, building on its established BUIDL token which holds nearly $2.4 billion worth of assets today.

Sourced from Bloomberg

66

May 13

If the "Board of Trade" becomes reality, expect a massive Super-Green. Is this the $SPY moon mission?

This is absolutely insane.

President Trump is currently flying to China with all of the following people to request "deals" with China's President Xi:

1. Elon Musk, Tesla and SpaceX CEO

2. Jensen Huang, Nvidia CEO

3. Tim Cook, Apple CEO

4. Larry Fink, BlackRock CEO

5. Stephen Schwarzman, Blackstone CEO

6. Kelly Ortberg, Boeing CEO

7. Brian Sikes, Cargill CEO

8. Jane Fraser, Citigroup CEO

9. Larry Culp, General Electric CEO

10. David Solomon, Goldman Sachs CEO

11. Sanjay Mehrotra, Micron CEO

12. Cristiano Amon, Qualcomm CEO

President Trump also says there are "many other" CEOs joining him on the trip who have not yet been disclosed.

Never in history has such a trip even remotely near this scale and caliber occurred.

This Trump-Xi meeting is far bigger than most realize.

68

Apr 21

Clarity Act experiencing intense scrutiny and significant delays it has become nothing but headline news.

75

Apr 20

1

156

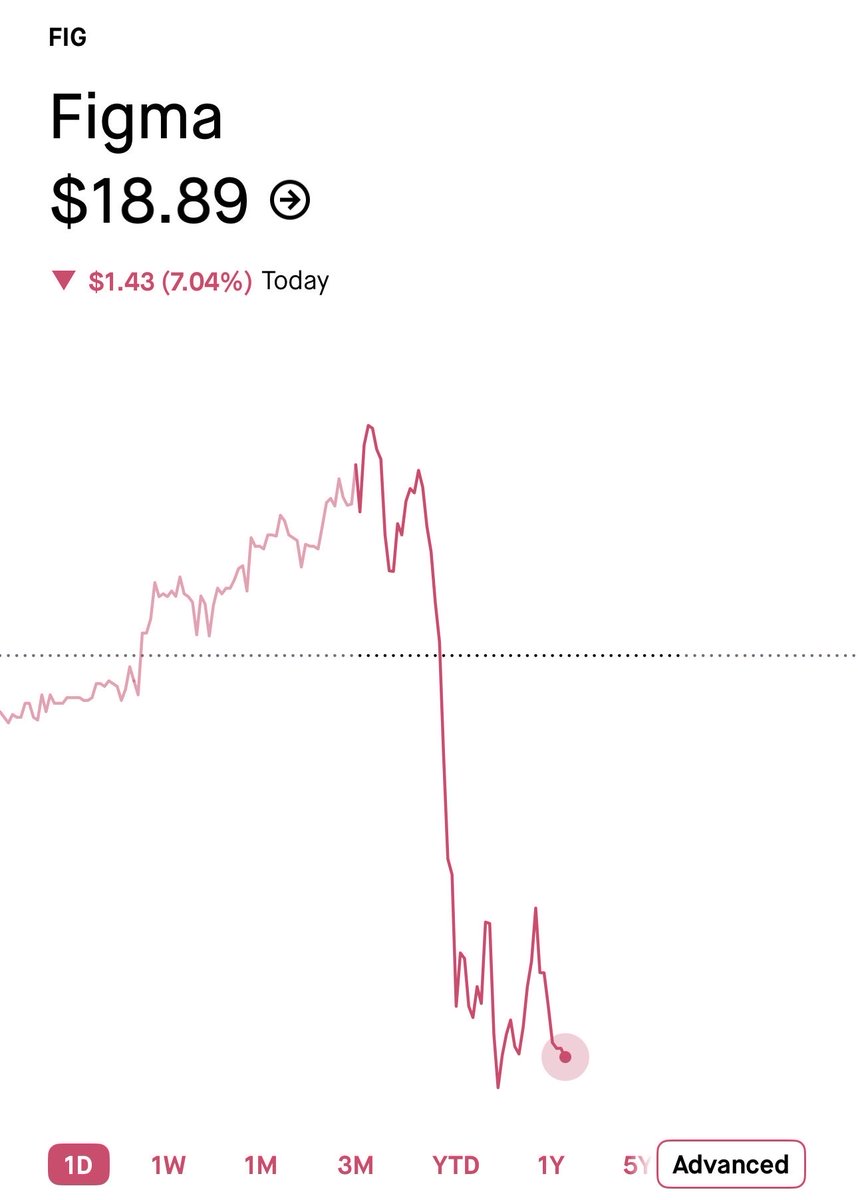

Apr 17

$FIG dropped 7.5% following Anthropic’s Claude design announcement - a clear signal of how sensitive the market is to major AI advancements.

This isn’t just about one stock reaction. It reflects a broader shift: companies that are not actively positioning themselves at the forefront of AI innovation are being repriced in real time.

We are entering a new AI cycle where capital, talent, and market value are flowing toward firms building or integrating frontier AI capabilities. In this environment, staying competitive increasingly means staying AI-native - or risk losing relevance.

Introducing Claude Design by Anthropic Labs: make prototypes, slides, and one-pagers by talking to Claude.

Powered by Claude Opus 4.7, our most capable vision model. Available in research preview on the Pro, Max, Team, and Enterprise plans, rolling out throughout the day.

214

Apr 15

Apr 15

Anthropic discusses Mythos AI model with US administration.

Anthropic's Mythos reveals 'a lot more vulnerabilities' for cyberattacks

The model, announced last week, is so dangerous that it’s not being released to the public, largely due to its alleged powerful cybersecurity capabilities.

Launching Project Glasswing - Securing critical software for the Al era. Protecting critical software systems before advanced AI models become widely available.

#Anthropic

42

Apr 15

Anthropic discusses Mythos AI model with US administration.

Anthropic's Mythos reveals 'a lot more vulnerabilities' for cyberattacks

The model, announced last week, is so dangerous that it’s not being released to the public, largely due to its alleged powerful cybersecurity capabilities.

Launching Project Glasswing - Securing critical software for the Al era. Protecting critical software systems before advanced AI models become widely available.

#Anthropic

101

Apr 14

Sitting in cash may feel safe today, but it could turn out to be the costliest decision for your future.

1

29

Apr 8

SoFi ranked No. 1 in the U.S. on @Forbes' list of World's Best Banks 2026 🏆

Thanks to our members who know we're more than just a bank—we're a one-stop shop to build your financial life and achieve your ambitions.

Check out the full article here 👇forbes.com/sites/shefalikapa…

4

186

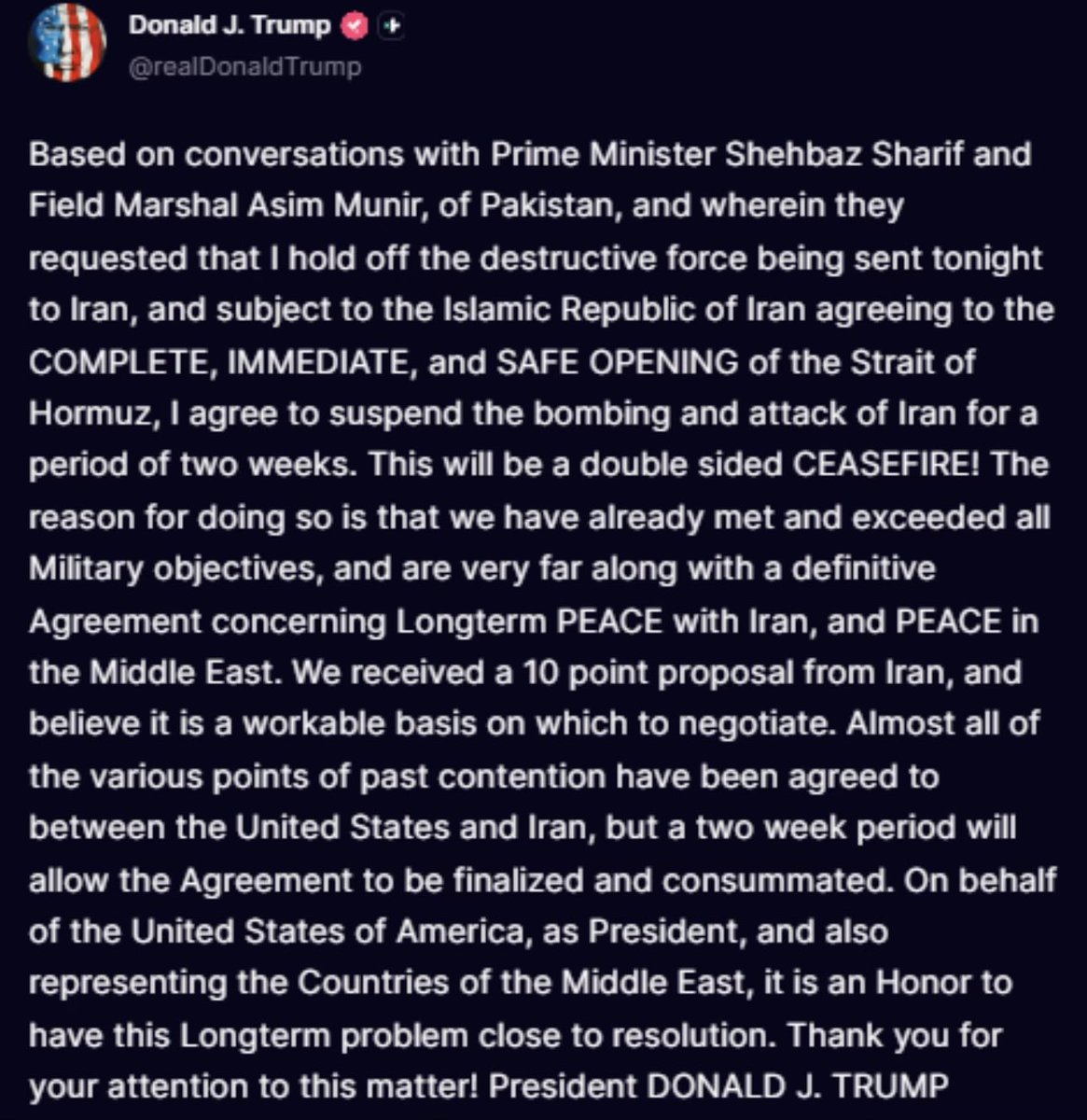

Apr 8

Iran accepted the ceasefire for two weeks. Hopefully, this is the beginning of the end of the war.

72

Apr 2

$SOFI just launched Big Business Banking - a nationally chartered bank offering 24/7/365 real-time fiat stablecoin settlement on one regulated platform.

Let that sink in. While legacy banks still operate 9–5, SoFi is enabling:

✅ Always-on global payments

✅ 24/7/365 real-time settlements via stablecoins

✅ Direct access to Fed rails through a nationally chartered bank

✅ Institutional partners: Mastercard, Galaxy, Fireblocks, Wintermute & more

✅ Built to operate at global, always-on market speed

This is not a feature update. This is infrastructure.

SoFi is building what other companies once aimed for — a seamless bridge between traditional finance and the crypto economy - but within a fully diversified platform spanning consumer banking, lending, investing, and fintech infrastructure. With a nationally chartered bank and direct Fed access, SoFi isn’t just serving the digital asset ecosystem - it’s positioning itself to lead it.

If stablecoins and tokenized settlement scale, SoFi isn’t watching from the sidelines. It’s building the rails.

Bullish.

Well done @anthonynoto and team.

Today, we announced the launch of SoFi Big Business Banking—regulated infrastructure that gives enterprises the power to hold deposits, move money across fiat and digital assets, and settle transactions 24/7 instantly.

“To be competitive businesses today must operate in a global, always-on environment 24 hours a day, 7 days a week, while legacy banks typically still operate 9 to 5, Monday to Friday. - @anthonynoto

The future of enterprise finance starts here. Learn more: investors.sofi.com/news/news…

1

6

189

Mar 28

We are winning too much! Please close the market until the war is settled.

BREAKING: The S&P 500 has now erased -$4.5 trillion in market cap since the Iran War began on February 28th.

60

Mar 26

1. Markets are down/volatile this year as geopolitical tensions and the Iran conflict have lifted risk premiums and pushed cautious positioning.

2. Oil and energy shocks remain key drivers of inflation risk , Brent crude prices are elevated vs pre-war levels, adding price pressure to the economy.

3. Inflation isn’t collapsing core inflation remains above central bank targets, slowing disinflation momentum, making the Fed cautious.

4. The Fed is holding rates steady as headline inflation remains stubborn, and risk of reigniting inflation hasn’t fully passed.

5. Markets are now pricing a non-zero chance of higher rates later this year instead of cuts, as inflation risk remains real.

6. Mortgage rates pushed higher amid geopolitical tensions and inflation expectations, showing broader financial conditions tightening.

7. Volatility is elevated (VIX and implied volatility rising), signaling uncertainty rather than calm - even if realized moves haven’t fully exploded yet.

8. Gold and traditional havens haven’t behaved as expected, reflecting nuanced risk flows and liquidity needs.

9. Growth prospects are mixed , GDP growth is modest, business investment is uneven, and geopolitical risk adds a headwind to confidence.

10. AI, data-center capex, and tech innovation remain secular themes, but they are being priced alongside macro risk, not in isolation.

Markets are continue to fall and they are digesting elevated inflation, higher energy costs, geopolitical risk, and uncertain rate policy - all driving volatility and cautious positioning $SPX $NDX $RUT $VIX

81

Mar 26

Breaking: $SOFI expands its Loan Platform Business with $3.6B in new agreements with a global bank, a top asset manager, and a financial services partner — underscoring strong demand for personal loans and confidence from institutional capital.

This is a capital-light, fee-based growth engine that complements SoFi’s core lending and financial products and strengthens its diversified fintech strategy.

SOFI continues to build scalable, modern financial infrastructure and is delivering results 📈

investors.sofi.com/news/news…

16

622

Mar 24

If your post doesn’t need expanding, don’t fake a “see more.”

Typing random filler just to trigger the expand click for engagement farming is weak - especially from accounts that claim to do serious analysis.

Standards matter.

If there’s depth, people read it.

If not, don’t manufacture suspense.

Quality > gimmicks.

32