Finance website following hedge funds and insiders. Our monthly newsletter's stock picks beat the S&P 500 by 66 percentage points in 3.5 years. See the link:

Joined September 2010

- Tweets 42,256

- Following 1,756

- Followers 21,924

- Likes 1,730

774 Photos and videos

Pinned Tweet

Apr 17

We compiled all the Q1 2026 hedge fund investor letters in one place.

What top funds are buying: $CRCL $HIMS $HOOD $MELI $APP $CRM $GOOGL $NFLX $BKNG $AVGO and dozens more.

Oakmark, ClearBridge, Jacob Funds, Lakehouse and many others. Updated regularly. See their full strategies and allocations below👇

1

2

10

4,638

Jun 10

🚨 $5.0M Insider Buy: $BORR

Director Tor Olav Trøim reported buying 1,063,000 shares of Borr Drilling on June 9 for $5.0M at $4.70, through Drew Holdings. Total position now ~27.3M shares, ~$123M.

Trøim founded Borr. He spent two decades as John Fredriksen's right-hand man, running Frontline, Seadrill, and Golar LNG, then split with Fredriksen in 2014 and started Borr in 2016 by picking up jackup rigs at roughly a quarter of construction cost in the depths of the offshore downturn. He chaired the company for most of its existence, stepped back to a board seat last September, and still chairs Golar LNG $GLNG.

The backdrop is Hormuz. The strait has been largely blocked since late February - crude transits down ~95%, LNG down ~99%. A ceasefire has held since April, but reopening the strait is the sticking point in negotiations, and the UAE's state oil company doesn't expect full flows before 2027. Energy security is suddenly worth paying for again.

Borr sits right in the middle of it. Four of its rigs work the region - Arabia II and III, Groa, Forseti - for customers in Saudi Arabia, Qatar, and the UAE. All four were down-manned when fighting started in March. All four are back. CEO Bruno Morand says customers now show "an increased sense of urgency to award existing tenders and bring forward certain drilling programs."

Trøim built this company buying offshore assets when nobody wanted them. Now he's putting in another $5M at $4.70, with a supply shock running through his core market.

Key metrics:

- Market cap ~$1.2B, trading ~$4.53 ( 12% YTD)

- Modern premium jackup fleet, expanding to 34 rigs with the new Mexico JV (5 rigs for $287M)

- 2026 contract coverage: 71% at ~$137,000 average dayrate (H1 ~78%, H2 ~65%)

- 13 new contract commitments YTD worth $274M in dayrate-equivalent backlog

- Four Middle East rigs (Saudi Arabia, Qatar, UAE) all back in operation after the March disruption

- Balance sheet: $300M convertible notes due 2033 issued, retiring most of the 2028 converts

- Trøim's stake: ~27.3M shares (~$123M), bought 1.06M more at $4.70 - above the current price

ALT Tor Olav Trøim

1

6

1,031

Jun 10

Track Borr Drilling's full insider trading activity, hedge fund ownership, and set free email alerts for new $BORR transactions:

insidermonkey.com/insider-tr…

1

701

Jun 9

$20.2M Insider Buy: $HOOD

Director Meyer "Micky" Malka reported buying 250,000 shares of Robinhood on June 5 for $20.2M at an average of $80.74 through Bullfrog Capital. This brings his total beneficial ownership across all vehicles - the fund, direct holdings, family trusts, and an LLC - to ~8.0M shares, worth approximately $670M at current.

Malka is the founder and managing partner of Ribbit Capital, the Palo Alto-based venture firm with ~$12B in AUM that is widely considered the premier fintech-dedicated VC in the world. Ribbit's portfolio reads like a roadmap of modern fintech: Robinhood, Coinbase, Nubank, Affirm, Credit Karma, Revolut, and Brex among them. Ribbit led Robinhood's $13M Series A in 2014, then led the $3.4B emergency funding round during the January 2021 GameStop crisis that effectively saved the company. Malka joined the Robinhood board in March 2022.

Born in Venezuela in 1974, Malka co-founded Heptagon Group at age 18, then launched Patagon in 1998 as Latin America's first comprehensive internet-based financial services platform - acquired by Banco Santander for $750M in 2000. He has appeared on the Forbes Midas List multiple times.

The timing is notable. Robinhood fell ~13% after Q1 2026 earnings on April 29 (revenue $1.07B missed $1.14B estimate, crypto revenue down 47% YoY), and the stock is still down ~26% YTD. But several structural catalysts have just activated: the SEC's elimination of the 25-year-old Pattern Day Trader rule officially took effect June 4 (removing the $25,000 minimum equity requirement that previously locked out ~25% of HOOD's funded accounts), Robinhood was named broker and initial trustee for Trump Accounts (the new federal savings program for ~5.5M American children), the Rothera prediction markets exchange is rolling out, and the company is opening retail access to the upcoming SpaceX IPO. Malka is buying the day after the PDT rule activated.

Key metrics:

Market cap ~$74B, trading ~$84

Stock performance: ~-26% YTD, ~-45% from October 2025 all-time high of $152.46; ~ 22% over the past year; ~ 120% since July 2021 IPO at $38

52-week range $63.52-$153.86

Q1 2026 revenue $1.07B ( 15% YoY) missed $1.14B; EPS $0.38 missed $0.42

2025 full year: record revenue $4.5B ( 52% YoY), record diluted EPS $2.05, $68B in net deposits

Crypto revenue -47% YoY in Q1; transaction-based revenue $623M

Forward P/E ~37x on post-Q1 estimates; Goldman PT $105, Cantor PT $110, Deutsche Bank $98

PDT rule eliminated June 4, 2026 - ~25% of funded accounts previously sub-threshold

Malka total beneficial position: ~8.0M shares (~$670M at current)

4

1

6

1,198

Jun 9

Track Robinhood Markets' full insider trading activity, hedge fund ownership, and set free email alerts for new $HOOD transactions:

insidermonkey.com/insider-tr…

1

1

2

574

May 27

🚨 New 13G: $2.6B AI Infrastructure Bet from Leopold Aschenbrenner's Situational Awareness LP - $NBIS

Situational Awareness LP just disclosed a 5.6% stake in Nebius Group, equal to 12,410,060 shares. At today's ~$208 close, that's a ~$2.58 billion position - and the trigger date for the 13G is May 19, 2026.

NBIS is up ~10% in after-hours trading on the news.

At ~$228, the position is now worth ~$2.83B.At this size, Nebius now stands as Situational Awareness's largest disclosed position based on the most recent filings. The previous top holding in the Q1 13F (filed for positions as of March 31) was a $2.04B notional SMH PUT, and NBIS wasn't on that filing at all - meaning the position was built entirely between April 1 and the May 19 disclosure trigger.

This is the fund run by 23-year-old Leopold Aschenbrenner, the former OpenAI Superalignment researcher whose June 2024 manifesto "Situational Awareness: The Decade Ahead" argued that AGI is coming by 2027 and the world isn't ready. He launched the fund weeks later with $225M. As of Q1 2026, disclosed U.S. equity exposure stands at ~$5.5B - a multi-hundred-percent return in roughly 12 months. The fund returned 47% in H1 2025 versus 6% for the S&P. Backers include Patrick and John Collison (Stripe), Nat Friedman (ex-GitHub CEO), and Daniel Gross. Carl Shulman is co-portfolio manager and is also listed on the 13G.

The thesis behind the Nebius position fits the broader Situational Awareness playbook. Q1 13F shows Aschenbrenner is short the semiconductor complex and long the AI picks-and-shovels: 8 of the fund's top 12 positions are PUTs - on SMH (VanEck Semiconductor ETF), $NVDA, $AMD, TSM, ASML, ORCL, AVGO, and MU. The longs are concentrated in power (Bloom Energy 6.4%), storage (SanDisk 5.3%), and neoclouds (CoreWeave 4.1%, IREN 2.9%, Core Scientific 2.8%, Applied Digital 2.3%). Now Nebius joins as a major new long - and goes straight to the top of the book.

What Nebius does: an Amsterdam-based AI infrastructure company that emerged from the restructuring of Russia's Yandex, led by Yandex co-founder Arkady Volozh. It builds GPU-dense data centers and rents capacity to hyperscalers and AI labs.

The contracted backlog is what makes this remarkable. Nebius has signed $46B in long-term AI compute contracts: $19.4B with Microsoft (September 2025), expanded to $27B with Meta (March 2026), plus a $2B equity investment from Nvidia. Q1 2026 revenue grew 684% YoY to $399M. Management is targeting $7-9B in exit ARR by end of 2026 (up from $1.25B in 2025) and planning $16-20B in 2026 capex.

Key metrics:

- Market cap ~$52B at close, trading ~$228 after-hours (up ~10% on the 13G news, ~95% YTD)

- Q1 2026 revenue $399M ( 684% YoY), adj EBITDA $129.5M

- Total contracted backlog: $46B (Microsoft $19.4B, Meta up to $27B)

- 2026 capex plan: $16-20B; targeting 2.5 GW contracted compute by year-end

- 2026 ARR target: $7-9B (vs $1.25B exit 2025)

- 15 analysts: Buy consensus, avg PT $231 (Citi raised to $287 post-Q1)

- Situational Awareness 5.6% stake: 12,410,060 shares, ~$2.58B at close / ~$2.83B at current after-hours

ALT Leopold Aschenbrenner

4

1,108

May 27

$NBIS is skyrocketing after @leopoldasch discloses a nearly $3 billion position in Nebius at 5pm. Situational Awareness didn't report any NBIS holdings as of the end of March.

2

3

1,274

May 27

$1.0M Insider Buy: $SYY

Director John Hinshaw bought 13,304 shares of Sysco on May 26 for $1.0M at $75.17, increasing his direct stake nearly 50% to 40,200 shares (~$3.0M).

Sysco announced a transformative $29.1B acquisition of Jetro Restaurant Depot on March 30. The stock fell ~12% as investors digested the $21B in new debt required to fund it, and has yet to recover to pre-deal levels. Hinshaw is buying that post-announcement dip with full board-level visibility into the deal.

Hinshaw's credentials carry weight. He was Group COO of HSBC from 2020 to 2024, running an operation of 130,000 employees with an $11B budget. Before that, EVP Technology and Operations at Hewlett Packard, Chief Customer Officer at HPE, Chief Information Officer of Boeing, and 14 years at Verizon. He has been on Sysco's board since 2018 and chairs the Corporate Governance and Nominating Committee - the committee that vets major strategic decisions like the Jetro deal. He also sits on the boards of Genpact, SingleStore, Illumio, and HSBC Innovation Banking.

What Sysco does: the largest US foodservice distributor with ~18% share of the fragmented $377B domestic market. The Jetro deal adds 166 cash-and-carry warehouses across 35 states, 725,000 independent restaurant customers, and ~$16B in revenue, making the combined company a ~$100B multi-channel distribution platform.

Key metrics:

- Market cap ~$36B, trading ~$75 (~2% YTD, ~12% below pre-deal levels around $82)

- Q3 FY2026 sales 4.7% to $20.5B, US local case growth 3.3%

- FY2026 guidance reaffirmed: adj EPS $4.50-$4.60 (tracking high end)

- Forward P/E ~16x on guidance midpoint; ~2.7% dividend yield

- Jetro deal: $29.1B EV, day-one accretive, mid-teens EPS accretive in year 2

- Combined company: ~$100B revenue ( 20%), $6.4B EBITDA ( 45%), $5.5B FCF ( 55%)

- Buyback paused for deleveraging; ~1.0x leverage reduction targeted in 24 months

3

805

May 27

$GEHC Insider Cluster Grows: Stryker's $SYK Kevin Lobo Adds $642K

Director Kevin Lobo bought 10,000 shares of GE HealthCare on May 22 for $642K at $64.18, tripling his direct stake to 14,363 shares. This makes 8 insider buyers in the last 30 days, with combined buying now exceeding $6.4M.

Lobo is the Chair and CEO of Stryker, where he has led one of the world's largest medical device companies since October 2012. Under his leadership, Stryker has completed more than 60 acquisitions and grown into a ~$130B medical technology platform. He's also Chair of Stryker's board since 2014, sits on Parker Hannifin's board, and chairs AdvaMed - the medical device industry's largest trade association.

Lobo only joined the GEHC board on March 13, 2026 - this is his first major open-market buy as a director, made about 10 weeks into his board tenure. A sitting medical-device-mega-cap CEO buying personal stock in a peer imaging and diagnostics company within his first quarter on the board is a pointed signal. He has direct visibility into both the medtech demand environment and GEHC's specific strategy from inside the boardroom.

Combined with the seven other insiders who have stepped in during the post-Q1 selloff (~$5.8M before this buy, ~$6.4M now), the cluster is broadening from financial directors into operating-executive territory. Stock is near the 52-week low and down ~22% YTD.

May 7

$5.0M Insider Buy: $GEHC

Director Larry Culp bought ~$5M of GE HealthCare on May 6, more than doubling his position to ~492K shares (~$30M ).

Culp is the architect of $GEHC's existence. He became GE's CEO in 2018 (the first outsider ever to lead GE) and led the 3-way breakup that spun GEHC public in Jan 2023. Before GE, he ran Danaher from ~$2B to a $50B industrial powerhouse, building the legendary Danaher Business System along the way. He's currently CEO of GE Aerospace and serves on the $GEHC board.

Timing: 7 trading days after Q1 earnings, when GEHC fell ~9% on a $250M inflation surprise, $90M in Q1 tariff costs, and an FY26 EPS guidance cut to $4.80-$5.00.

Stock down 25% YTD. Four other insiders also bought ~$618K in the past 30 days.

1

6

2,079

May 27

Track GE HealthCare's full insider trading activity, hedge fund ownership, and set free email alerts for new $GEHC transactions:

insidermonkey.com/insider-tr…

788

May 27

~$1M Insider Buy: $MELI

Director Nicolas Aguzin bought 600 shares of MercadoLibre on May 22 for $994K at an average of $1,655.93. This increased his direct stake to 5,355 shares (~$9.1M at current).

Aguzin's resume is the signal. He was CEO of Hong Kong Exchanges and Clearing (HKEX) from 2021 to 2024 - running one of the world's most valuable exchange operators. Before that, he spent 30 years at JPMorgan, including CEO of Asia Pacific (2012-2020, overseeing the firm's business across 17 markets), CEO of Latin America, and CEO of its International Private Bank. He's a Wharton-trained economist who has sat on MercadoLibre's board for years. A global markets and Latin America banking veteran of his caliber adding personal capital is worth noting.

The buy came into a selloff. MercadoLibre fell ~16% in the week after its Q1 print, despite delivering one of its strongest quarters ever: revenue grew 49% YoY to $8.85B, the fastest pace in nearly four years. The market punished the stock because adjusted EPS of $8.23 missed estimates by ~12% - management is deliberately compressing near-term margins by giving shipping costs back to buyers to capture share. Aguzin bought into that margin-investment-driven dip.

What MercadoLibre does: the dominant e-commerce and fintech platform across Latin America, spanning the Mercado Libre marketplace, Mercado Pago (payments and digital banking), Mercado Crédito (lending), and logistics, with leading positions in Brazil, Mexico, and Argentina.

Key metrics:

- Market cap ~$86B, trading ~$1,693 (down ~15% YTD)

- Q1 2026 revenue $8.85B ( 49% YoY, fastest in ~4 years)

- Total Payment Volume $87.2B ( 50%); GMV $19.0B ( 42%)

- Q1 income from operations $611M (6.9% margin); net income $417M

- Adj EPS $8.23 missed $9.37 (margin pressure from shipping investment)

- Trailing P/E ~44x; forward P/E ~40x on cut FY2026 EPS estimates (~$41 from ~$48 pre-Q1)

- Net income margin 4.7%

2

1

8

1,459

May 27

Quick bull/bear on $MELI alongside the Aguzin buy.

The bull case:

- Dominant market position: ~35% share in Brazil and Argentina, ~30% in Mexico. MercadoLibre's Latin American e-commerce sales exceed the combined total of its next 15 competitors.

- The flywheel is firing. Q1 2026 revenue 49% YoY (fastest in nearly 4 years), GMV 42%, Total Payment Volume 50%, fulfillment penetration over 60% in Brazil and over 75% in Mexico.

- Fintech is becoming a standalone business. Mercado Pago and Mercado Crédito now account for ~44% of revenue. The credit portfolio grew 87% in Q1, with credit cards expanding at 104%.

- Analyst fair value estimates cluster around $2,150 and sell-side PTs sit in the $2,200-$2,500 range, implying ~30% upside from Aguzin's $1,656 entry. He's buying well below where the street marks intrinsic value.

The bear case:

- Shopee is the real threat, not Amazon. Sea Limited's Shopee $SE is now Brazil's #1 e-commerce app by order volume, with low prices, gamified shopping, and a fintech arm directly attacking MELI's twin pillars.

- Amazon committed $10B to Brazil with ~25% deployed in the last 18 months and is waiving FBA fees to pull merchants into its ecosystem. Citi recently trimmed its PT to $2,500 from $2,700 citing this pressure.

- Margin compression is the price of defending share. Operating margin fell to 11.1% in Q1. Lowering Brazil's free shipping threshold to ~$3.50-$4.00 costs roughly $390M annually. If Shopee/Temu/Amazon force this to be permanent, the "invest now, harvest later" model becomes a permanent cost.

- Credit risk is rising as the loan book scales. Net charge-off rate is in the high teens. MELI doesn't collateralize loans, so a credit cycle deterioration could create real provisioning pressure - exactly what hit Q1.

- Valuation isn't cheap. Forward P/E ~40x on cut FY2026 EPS estimates (~$41 from ~$48 pre-Q1).

1

3

836

May 27

Track MercadoLibre's full insider trading activity, hedge fund ownership, and set free email alerts for new $MELI transactions:

insidermonkey.com/insider-tr…

2

545

May 27

RT @insidermonkey: @SJosephBurns @grok Grok doesn't understand the gravity of VRRM's latest earnings results. This isn't a 20% annual reven…

1

May 26

$542K Insider Buy: $INTU

Director Vasant Prabhu bought 1,750 shares of Intuit across May 22-26 for $542K at ~$309.50. This is a brand-new position - his first open-market purchase of the stock.

The timing is what makes a modest buy notable. Intuit fell 20% in a single day on May 21, its worst drop in years, and is now down ~54% YTD - extraordinary for a fintech mega-cap that traded near $814 last summer. Prabhu stepped in days after that crash.

Prabhu was Vice Chairman and CFO of Visa from 2015 to 2023, one of the most respected finance executives in the entire payments industry. Before Visa he was CFO of NBCUniversal, Vice Chairman and CFO of Starwood Hotels, and CFO of Safeway. He joined Intuit's board in 2024 and also sits on the boards of Delta Air Lines and Kenvue. A career fintech and consumer CFO buying his first shares of Intuit during a crash driven by financial-model fears is a pointed signal.

The selloff is an AI-disruption story. Intuit's fiscal Q3 (May 20) actually beat and raised: revenue $8.56B ( 10%), adjusted EPS $12.80 vs $12.28 expected, full-year guidance raised. But management lowered its TurboTax revenue outlook, said "we lost on price" among the most price-sensitive DIY filers, guided TurboTax online units down ~2%, and announced a 17% workforce cut (~3,000 jobs). The market is repricing whether AI erodes the "guided help" moat that made TurboTax and QuickBooks so valuable.

Key metrics:

- Market cap ~$85B, trading ~$304 (down ~54% YTD, ~63% off the ~$814 high)

- Q3 FY2026 revenue $8.56B ( 10% YoY), adj EPS $12.80 (beat $12.28)

- FY2026 guidance raised: revenue $21.34-$21.37B, adj EPS $23.80-$23.85

- Forward P/E ~13x on raised guidance (vs 5-year average well north of 30x)

- 17% workforce reduction; $300-340M restructuring charges

- TurboTax online units guided ~-2%; "lost on price" at the low end

ALT Vasant Prabhu

5

5

15

2,970

May 26

Track Intuit's full insider trading activity, hedge fund ownership, and set free email alerts for new $INTU transactions:

insidermonkey.com/insider-tr…

2

666

May 26

$2.5M Insider Buy: $NCLH - And This Time It's the CEO

A Form 4 filed today shows President and CEO John Chidsey bought 153,000 shares of Norwegian Cruise Line on May 22 for $2.5M at $16.37, near the 52-week low. This increased his direct stake 15.5% to 1,139,940 shares (~$19.5M).

This is the bigger signal in an expanding insider cluster. Chidsey only became CEO in February 2026 - three months ago - and this is his first major open-market buy in the role.

Chidsey is a turnaround and operations specialist. He spent 5 years as CEO of Subway (through its 2024 sale), was CEO of Burger King Holdings, and ran two divisions at Cendant (Avis, Budget, Wright Express, Jackson Hewitt). He first joined the NCLH board in 2013, served until 2022, returned in 2025, and was tapped to run the company in February. He knows this business from the boardroom and now owns the execution.

On the Q1 call, Chidsey openly called NCLH a "turnaround" and attributed the problems to "self-inflicted" missteps in marketing and revenue management. That candor matters - he's buying $2.5M of stock into a situation he's publicly framed as fixable and internal, not structural.

Q1 2026 (May 4) actually beat on profitability: revenue $2.33B ( 10% YoY), adjusted EPS $0.23 versus $0.14 expected, adjusted EBITDA $532.9M ( 18%). But management slashed full-year guidance - adjusted EPS cut ~30% to $1.45-$1.79, net yield now seen down 3-5% - citing Middle East disruption, soft Europe demand, and the booking shortfall. The stock fell ~9% to near its 52-week low.

Key metrics:

- Market cap ~$7.4B, trading ~$17 (down ~23% YTD)

- Forward P/E ~10-12x on cut FY2026 guidance (vs ~8x pre-cut)

- Q1 2026 revenue $2.33B ( 10% YoY), adj EPS $0.23 (beat $0.14)

- FY2026 guidance cut: adj EPS $1.45-$1.79 (from $2.38), adj EBITDA $2.48-$2.64B

- Net yield seen -3% to -5%; ~26% of Q2 capacity in Europe

- $125M annualized SG&A savings program underway

- Net leverage 5.3x, total debt $15.15B, liquidity $1.6B

- Multiple banks cut PTs but most maintain Buy/Neutral

May 11

$521K Insider Buy: $NCLH

Director Zillah Byng-Thorne bought 29,467 shares of Norwegian Cruise Line Holdings on May 7 for $521K, three trading days after the post-earnings selloff. Modest dollar size but worth noting given her background and the timing.

Byng-Thorne is best known for running UK media company Future plc from 2014-2023, taking it from ~£20M market cap to ~£2B through a string of acquisitions and digital transformation. She's currently CEO of Dignity plc and Chair of Trustpilot, with prior CFO roles at Sage Group and eBay.

The buy came after NCLH fell ~9% on Q1 results. Earnings actually beat ($0.23 vs $0.15 consensus, revenue 9.6%), but FY26 EPS guidance was cut from $2.38 to $1.45-$1.79 on Middle East conflict pressuring European bookings (26% of Q2 capacity), higher fuel costs, and execution missteps. Goldman, Morgan Stanley, Barclays, and Susquehanna all cut PTs.

She more than doubled her direct stake (~70K → ~100K shares). Small in dollar terms, but a director with her operating background stepping in 3 days after a yield-reset guidance cut is the relevant signal.

1

5

1,667

May 26

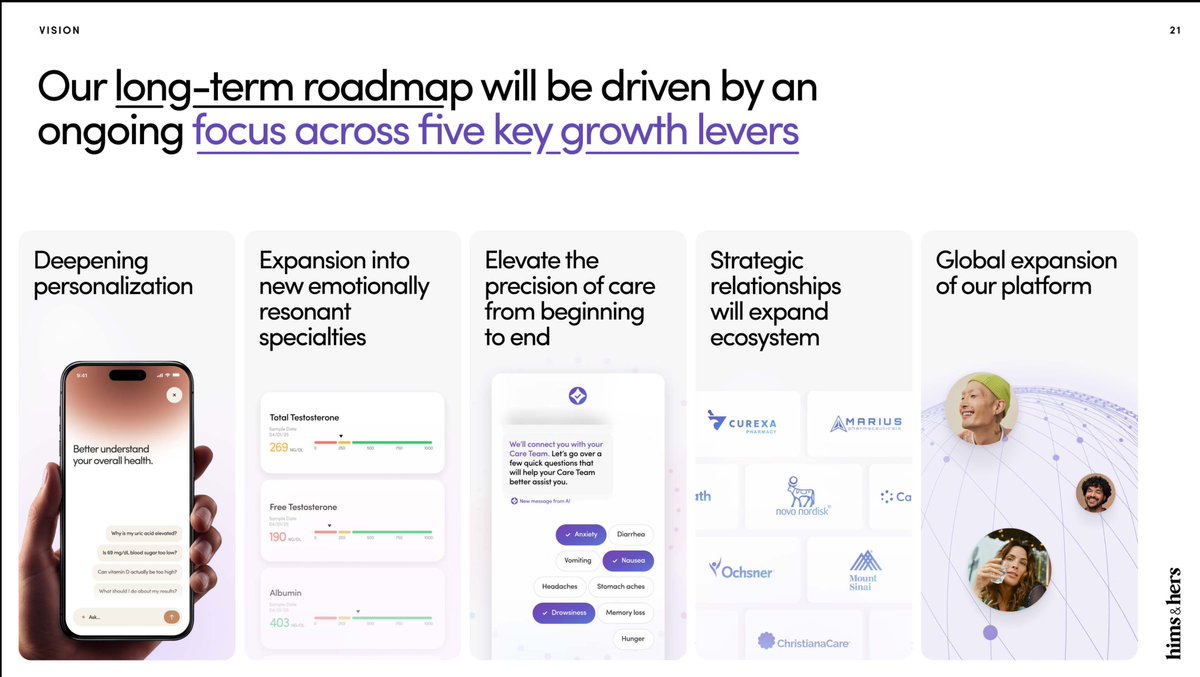

$1.2M Insider Buy: $HIMS

Lead Independent Director David Wells bought 48,400 shares of Hims & Hers on May 26 for $1.2M at $24.24. This increased his direct stake 27.5% to 224,417 shares. The buy comes two weeks after the stock fell ~15% on a Q1 print disrupted by the company's GLP-1 strategy pivot.

Wells brings serious financial credibility. He's the Audit Committee Chair at Hims & Hers and has been on the board since September 2020. He spent 8 years as CFO of Netflix (2010-2019), through its global streaming expansion. He's currently Chairman of Wise, the London-listed fintech, and was an independent director at The Trade Desk from 2016 to 2025.

A former Netflix CFO and sitting Audit Chair buying $1.2M of stock is a notable signal - he has the deepest possible visibility into the financials during a messy transition quarter.

In March, Hims & Hers pivoted its weight-loss business away from cheaper compounded GLP-1s toward branded medications, signing arrangements to carry Novo Nordisk's Wegovy and Eli Lilly products. The shift cratered near-term margins (gross margin fell to 65% from 73%, adjusted EBITDA halved) and triggered a $92.1M net loss versus a $49.5M profit a year ago. But it removes the regulatory overhang that came with compounded drugs and replaces it with FDA-approved branded supply.

What Hims & Hers does: a subscription telehealth platform spanning weight loss, men's and women's dermatology, sexual health, hormone therapies, and mental health, serving ~2.6 million subscribers.

Key metrics:

- Market cap ~$5.5B, trading ~$24 (down ~27% YTD)

- Forward P/E ~45-50x (premium growth multiple vs ~17x industry median)

- Q1 2026 revenue $608M ( 4% YoY), missed consensus

- Q1 net loss $92.1M (vs $49.5M prior year); adj EBITDA $44.3M (from $91.1M)

- Subscribers ~2.6M ( 9% YoY); international revenue surged to $78M from $7M

- FY2026 guidance raised to $2.8-$3.0B revenue ( 19-28%), adj EBITDA $275-350M

- $250M buyback authorized; Eucalyptus acquisition pending (mid-2026)

- 125,000 Wegovy shipments fulfilled in the first 6 weeks

ALT Hims & hers investor presentation

1

8

1,279

May 26

Track Hims & Hers' full insider trading activity, hedge fund ownership, and set free email alerts for new $HIMS transactions:

insidermonkey.com/insider-tr…

1

650

May 26

The thesis is playing out in real time.

$MOD just signed a $4B Long-Term Capacity Agreement for its Airedale data center cooling products, calendar 2027 through 2029, with $165M cash upfront. Stock 16.5% on pre-market today.

Modine was one of the names we highlighted on the liquid cooling theme. The multi-year order book just got a lot bigger.

May 19

Semis under pressure this week. NVDA earnings tomorrow night. Where does the AI trade rotate next?

Goldman's Shawn Tuteja walks the evolution: semis → hyperscalers → data centers → AI equipment → memory chips → fiber optics. His team's next call: liquid cooling. Theme up only 30% YTD vs optical networking 100%.

Why it matters: data centers spend nearly as much electricity on cooling as on compute. Liquid cooling cuts that by up to 10x.

Goldman flagged the theme. We did the stock work. Pure plays:

$MOD - Spinning off legacy auto biz via Reverse Morris Trust with Gentherm in Q4. Becomes a pure-play climate solutions co with data center as the growth engine. Guiding 50-70% annual DC growth over the next two years.

$NVT - Infrastructure now 55% of sales, up from 12% at spin. Liquid cooling driving 34% growth at 20% margins. NVIDIA partner.

$VRT - The scale name. Q1 EPS 83% YoY. $15B backlog. NVIDIA Vera Rubin partner. Trades in the 50s on fwd PE.

$ECL - Buying CoolIT from KKR for $4.75B at 29x EBITDA. Closes Q3. The actual pure-play target.

$ETN - Bought Boyd Thermal for $9.5B in March. Liquid cooling bolt-on to electrical portfolio.

5

1,663