Time@Mode analysis via Discord 💹| TradingView chartist | Called each cycle top and bottom in #BTC since 2015 in real time.

Joined March 2014

- Tweets 23,854

- Following 4,161

- Followers 3,060

- Likes 25,216

3,925 Photos and videos

Pinned Tweet

Apr 17

10 years of timestamped calls.

Every link verifiable.

3 BTC cycles, equities, commodities, macro.

👇

8

5

18

830

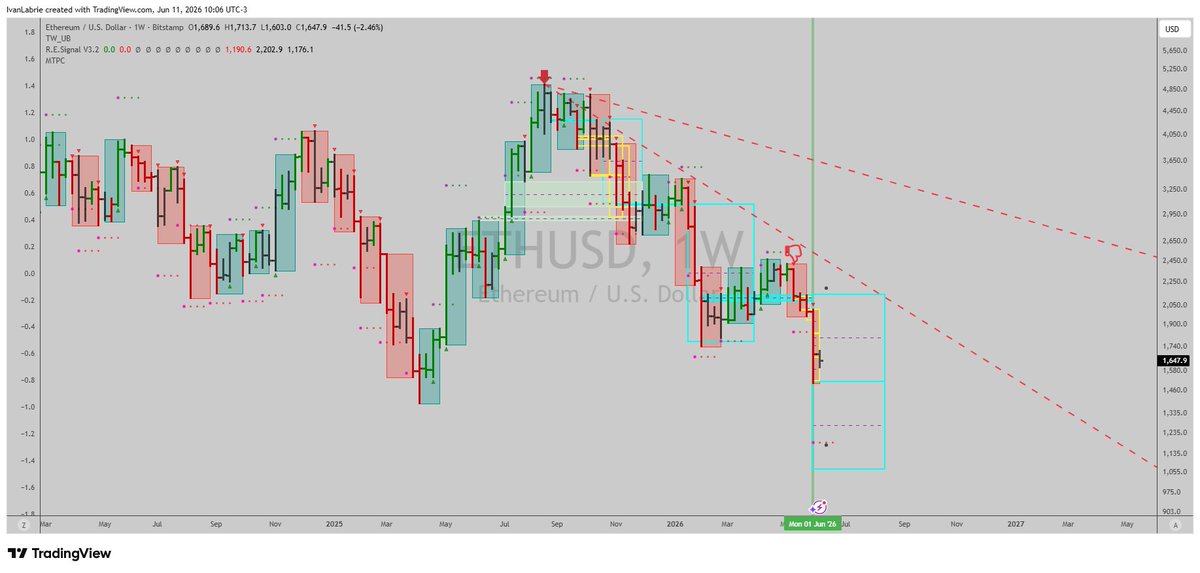

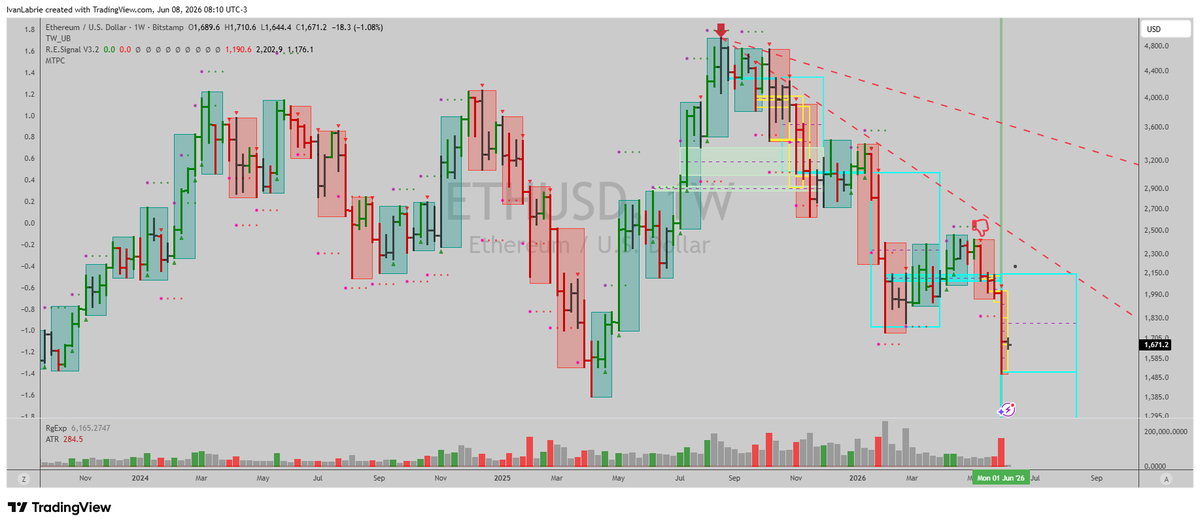

The week's pivot is the Iran-US MOU that kept almost-signing through the weekend and kept slipping.

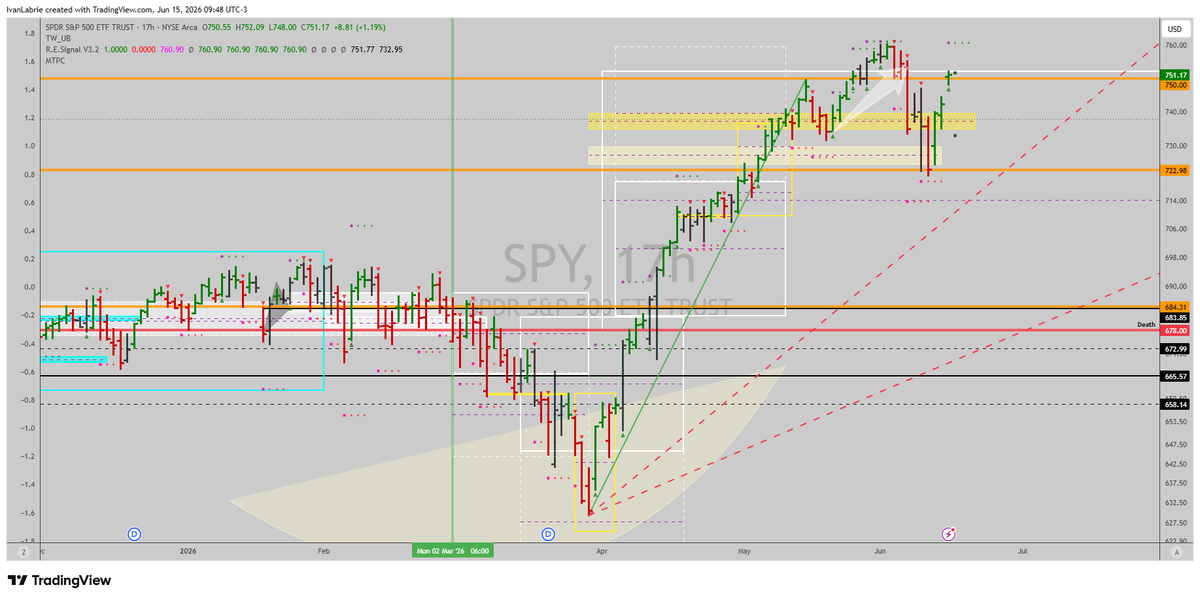

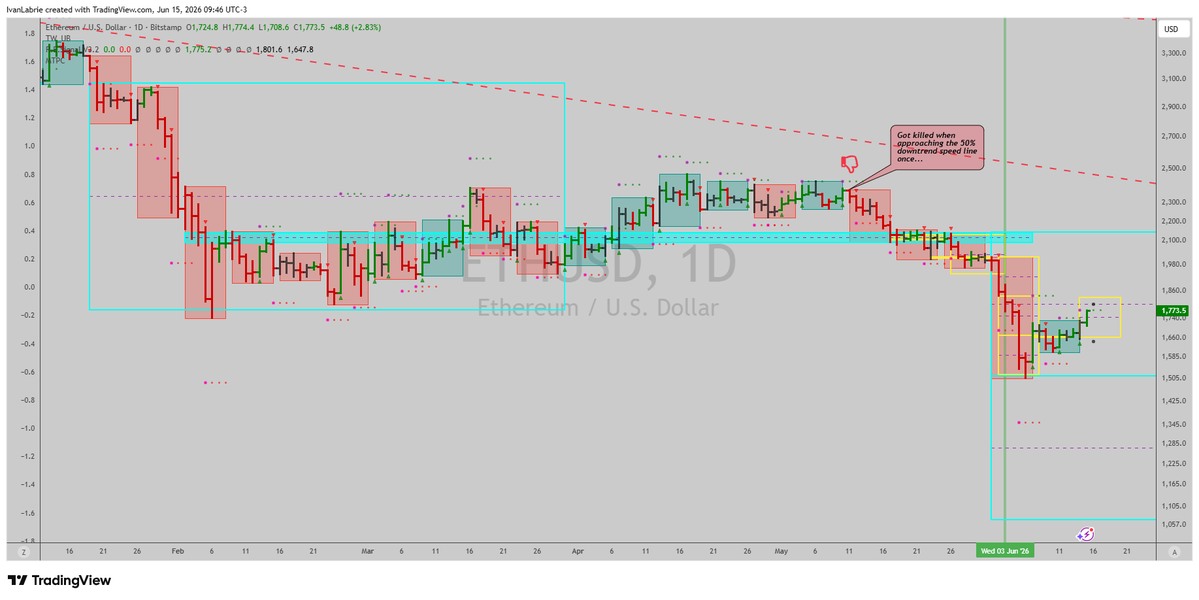

ETHUSDT daily turned up first off Extreme Fear (F&G 8). BTC lags.

Warsh's first FOMC first dot plot lands Wed 6/17 2pm ET; the BOJ meets the same window.

👇Thread.

1

45

Gold short ($4,150 entry, stop $4,775), mostly cash; crypto positioning is tactical this week. Spot almost fully cash. Active stock book flat since 6/5. LT book ~59% cash. Two-sided bot sleeve at reduced size. Juneteenth closes Fri; dot-plot reaction has Thu to settle.

1

1

32

Laboratory Notes members get the mid-week update and exact levels. $29/mo, crypto accepted; annual saves.

moonpay.hel.io/pay/69e29f1b9…

1

13

Cyclical data firmed this week and the bottom-callers got loud. But the two rows that built this bear, inflation and rates, never budged. PPI printed 6.5% YoY. That is not a thaw, it is stagflation wearing a bull jacket. I stay defensive into the dot plot.

37

Ivan Labrie retweeted

Most traders who don't trade options assume options markets are someone else's problem. Fabio Ruggeri's data suggests that's been wrong for the past five years.

Pre-2020, options volume was dominated by institutional hedging. The effect on price action was real but manageable. After 2020, retail options participation exploded. The flows got large enough that market maker hedging became a primary driver of short-term price behavior in indices like SPX and in individual large-cap stocks.

When market makers are net short gamma, they buy as price rises and sell as it falls, which amplifies moves. When they're net long gamma, they do the opposite, suppressing moves and compressing volatility.

This regime switch happens at known price levels, and the data to identify them is publicly available.

Most price-based systems were built before this dynamic was this influential. The traders ignoring options flow are operating with a model of how price behaves that the market partly left behind after 2020.

2

2

17

2,367

Jun 13

Crypto stopped trading on-chain and started trading rates. The tell is the CME line: BTC, ETH, SOL get pushed by macro hedgers regardless of fundamentals, non-CME names trade their own book. That dispersion, not "is crypto up or down", is where the long/short edge lives.

5

174

Jun 13

Sooooo tired of winning...Jan 2025 feels a decade away after all us crypto guys been through.

Jun 13

Govt taking stakes in companies, banning access to AI models to everyone that isn't Murican...yeah, land of freedom my a$$.

108

Jun 12

What a scam!

Jun 12

Ron Baron of Baron Fund did the unthinkable with his long term investors in his fund. He prioritized new, short term investors to jump to the front of the line to get free money from the SpaceX IPO.

Instead of blocking new investment into Baron Partners Fund, BPTRX and BPTIX once the SpaceX IPO was coming, he allowed new investors to get right in line and dilute our share of SpaceX to those new investors.

It’s a tough call for him, but an obviously BAD call from my perspective. Why? They diminished my position in SpaceX by giving it to them instead. Downright theivery.

Shameful

1

158

Jun 12

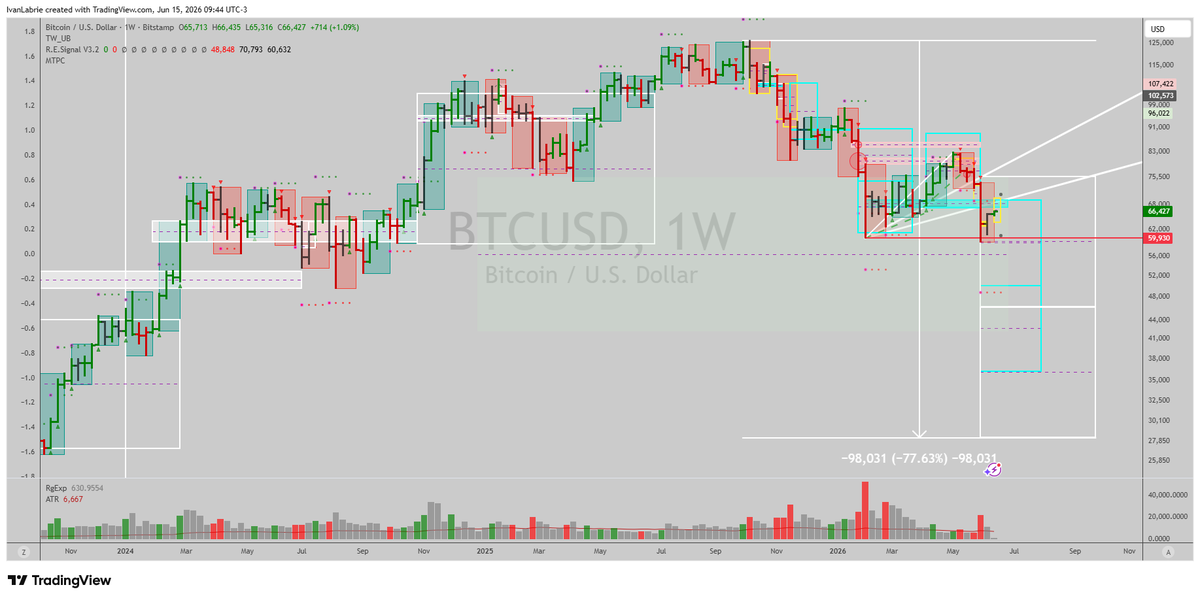

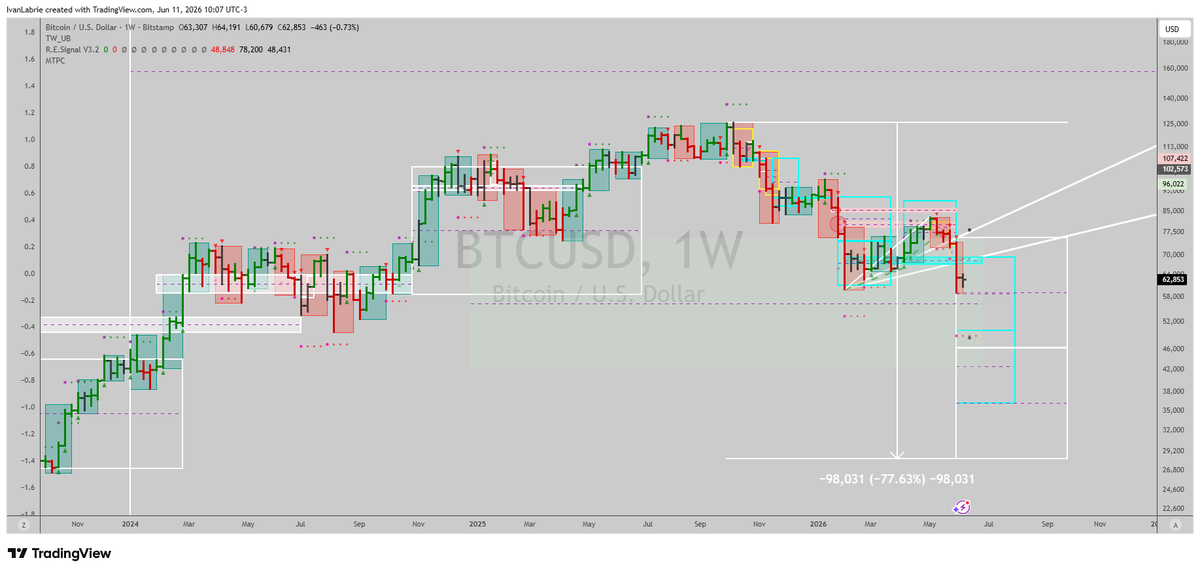

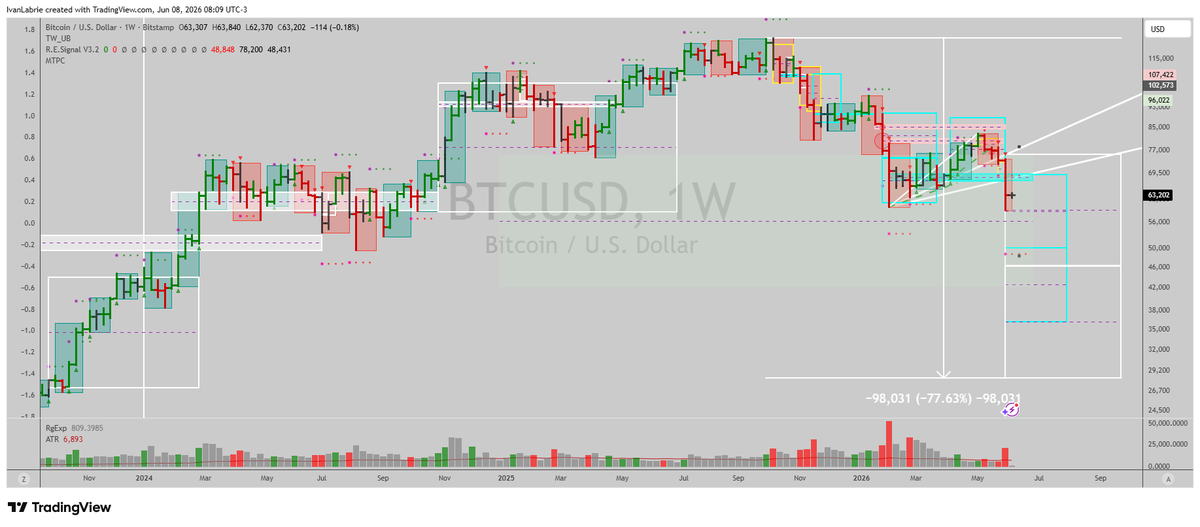

Everyone is calling $63k the macro bottom. The weekly trend turned down weeks ago and never reclaimed. I am short from ~$65.7k, stop $71,383. Every rip is a trap until that takes a weekly close. The binary is Warsh's dot plot on 6/17, not the tape into it.

71

Ivan Labrie retweeted

Jun 12

I got robbed today in broad daylight by the fund management company who let brand new investors into our fund at the last minute to get the gains we have earned by holding fund shares for years waiting for SpaceX to come public. This fund company earns over 1.5% of the assets every year for many years and then gives away the profits that are due to the shareholders in the month before the IPO. Disappointed and disgusted

1

2

4

371

Ivan Labrie retweeted

Jun 12

This matches how I run it. Covered calls on a BTC and ETH spot bag, bull put spreads sold at support, risk capped per lot before the trade goes on. The yield is durable because the demand to hedge uncertainty never switches off. You know the loss before you enter.

1

3

155

Ivan Labrie retweeted

Jun 12

Options yields are durable because their underlying demand is always there: uncertainty.

Investors want to hedge against outcomes they cannot predict. Miners want to protect revenues, funds want downside protection and treasuries want to cap risk.

Every one of these participants are willing to pay an option premium AKA yield to transfer that uncertainty to someone else.

Bull markets, bear markets, even periods of low volatility, it doesn't matter. The need to transfer risk remains, because uncertainty never goes away.

2

5

104

10,808