I am not a licensed financial advisor and as such, I do not post financial advice. All X are my thoughts and opinions, solely information and entertainment.

Joined March 2011

- Tweets 3,901

- Following 89

- Followers 12,681

- Likes 4,155

841 Photos and videos

links to easily navigate my profile:

Hudson Bay Capital—

• x.com/sboho/status/177134918…

• x.com/sboho/status/178609705…

• x.com/sboho/status/178606814…

• x.com/sboho/status/178605439…

• x.com/sboho/status/182351132…

• x.com/sboho/status/178897379…

• x.com/sboho/status/178645164…

• x.com/sboho/status/178609705…

• x.com/sboho/status/178606814…

• x.com/sboho/status/176809523…

• x.com/sboho/status/170925593…

Net Operating Losses (NOL)—

• x.com/sboho/status/176762882…

• x.com/sboho/status/175455285…

• x.com/sboho/status/173771355…

• x.com/sboho/status/172010820…

• x.com/sboho/status/172964844…

• x.com/sboho/status/172308047…

•reddit.com/r/BBBY/comments/1…

•reddit.com/r/BBBY/comments/1…

•reddit.com/r/BBBY/comments/1…

Lazard—

• x.com/sboho/status/179258137…

• x.com/sboho/status/179257384…

• x.com/sboho/status/179256614…

•reddit.com/r/BBBY/comments/1…

Ryan Cohen's 16(b)—

• x.com/sboho/status/176360317…

• x.com/sboho/status/174734172…

• x.com/sboho/status/174695470…

• x.com/sboho/status/174734172…

Ryan Cohen's Class Action—

• x.com/sboho/status/179204360…

• x.com/sboho/status/179202509…

• x.com/sboho/status/179086875…

• x.com/sboho/status/177634567…

• x.com/sboho/status/175856843…

Form 25, Form 15 and Going Dark—

• x.com/sboho/status/173211914…

• x.com/sboho/status/171178861…

• x.com/sboho/status/171176841…

• x.com/sboho/status/171176841…

• x.com/sboho/status/171139900…

•reddit.com/r/BBBY/comments/1…

$GME New Class and Blockchain Shares—

• x.com/sboho/status/184912888…

• x.com/sboho/status/184185955…

• x.com/sboho/status/183623118…

• x.com/sboho/status/179163422…

• x.com/sboho/status/179155259…

• x.com/sboho/status/179163422…

#GME Investment Policy—

• x.com/sboho/status/178541881…

• x.com/sboho/status/182444849…

• x.com/sboho/status/182444849…

• x.com/sboho/status/178541881…

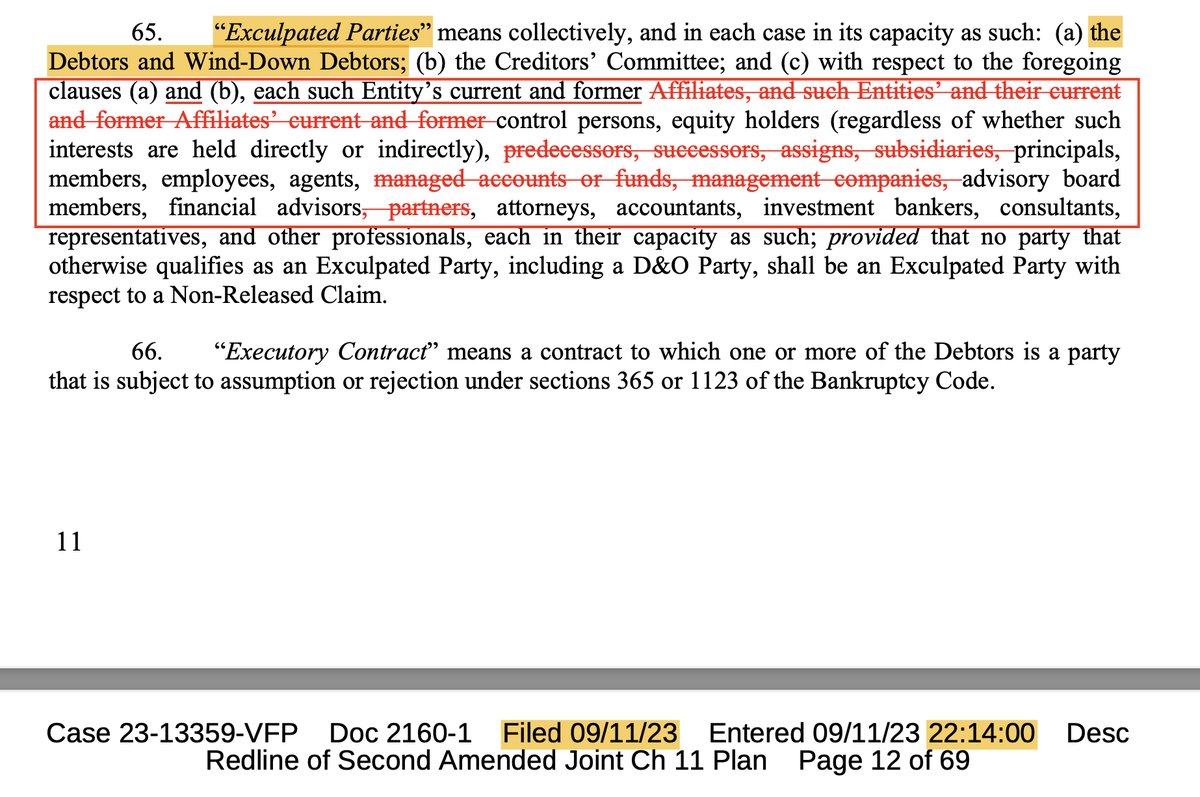

• x.com/sboho/status/173252015…

$BBBY #BBBY $BBBYQ #BBBYQ

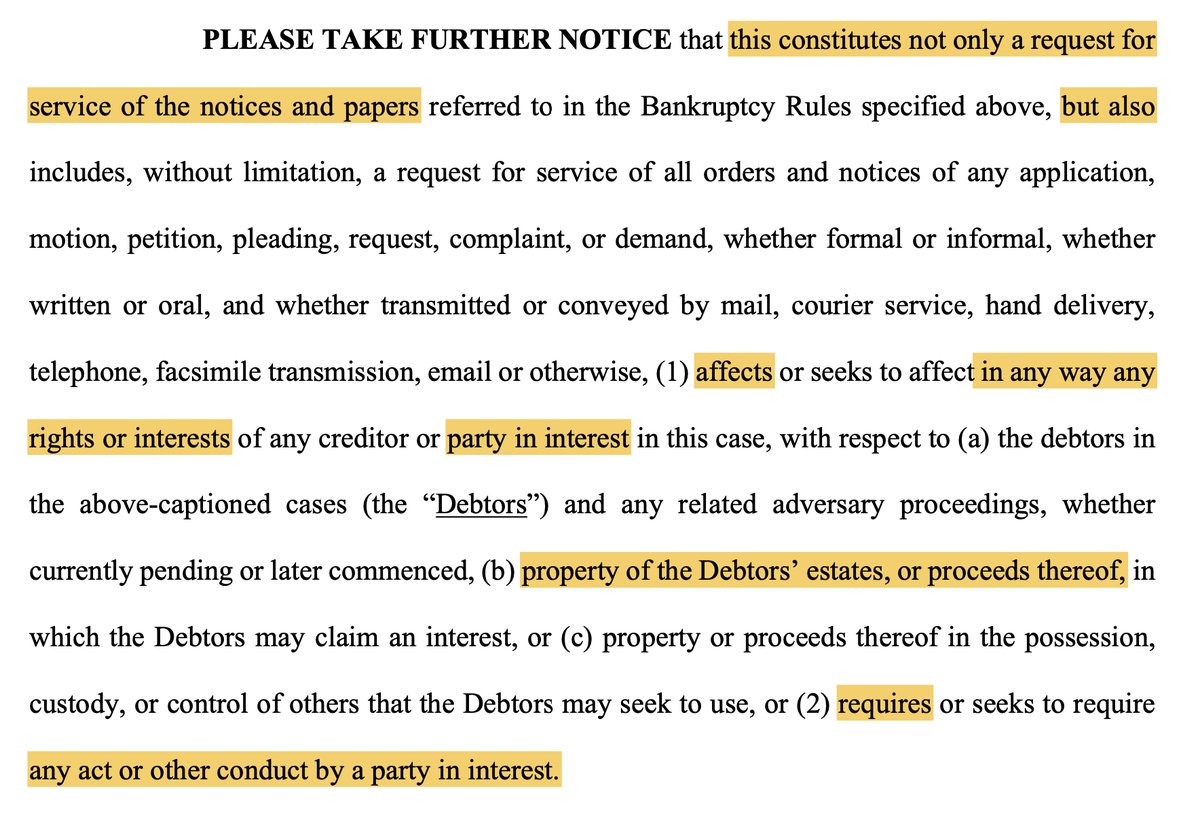

re: Hudson Bay and the great conversation that it has started.

Let's look back at the work Kirkland did, going to August 2023:

Specifically the language. It's important that they denote a potential Section 16 reporting claim.

Further down, we have a reporting issue.

I believe that these could be the result of the combination of RC and HBC's holdings. From the cooperation/standstill, RC was allowed to increase his position to 19.99%.

From the share buybacks, he was pushed from 9.8% to 11.8%.

Now, if you look at HBC at 9.99% limit and RC at his purchase which concluded at 9.8% limit, you are under 19.99% with 19.97%.

However, if you take RC's pushed 11.8%, you arrive at 21.79% ownership and are in violation of the standstill.

Could this have been the move to establish "harm" and justify a future suit? Or to assist in a suit brought forward by Mr. Goldberg? I don't know.

—

Then we also have the fun topic of the new HBC 16(b). So let me pose a question..

What if the Section 16(b) is not the result of HBC going over 9.99% (they can't), but because the window of time from RC's sell on August 18 to HBC's entry on February 8 is less than 6 months?

That is a violation, if they are related.

This only applies if RC and HBC are related—if RC is an attribution party (affiliate) through the HBC deal, this is a violation of 16(b). Their combined ownership is greater than 10% and the time between the sale and the buy is less than 6 months.

I wonder if that is why it is under seal?

I also wonder, is that why JP Morgan was in such a rush on the weekend of February 4-5 to declare the Company insolvent and push it into Chapter 7, well before the grace period to repay the bond note had expired?

fun times. 🥷

$BBBY #BBBY $BBBYQ #BBBYQ

63

142

614

362,069

Sixth Street, Class 6, the Asset Sale Transaction and the marshalling agreement—

• x.com/sboho/status/186511288…

• x.com/sboho/status/186512801…

Bratya, modifications to the Plan and the lack of Exculpation protections for RC—

• x.com/sboho/status/190421303…

• x.com/sboho/status/190454906…

RC as Bypassed Recipient, Interests—

• x.com/sboho/status/193101846…

• x.com/sboho/status/193976106…

a video presentation of my thoughts for $BBBY Class 9 recovery, how it relates to Interests, the Holder of Interests, and legal language reserving the rights for a Distribution to the aforesaid contained in the Confirmed Plan—

• x.com/sboho/status/193867376…

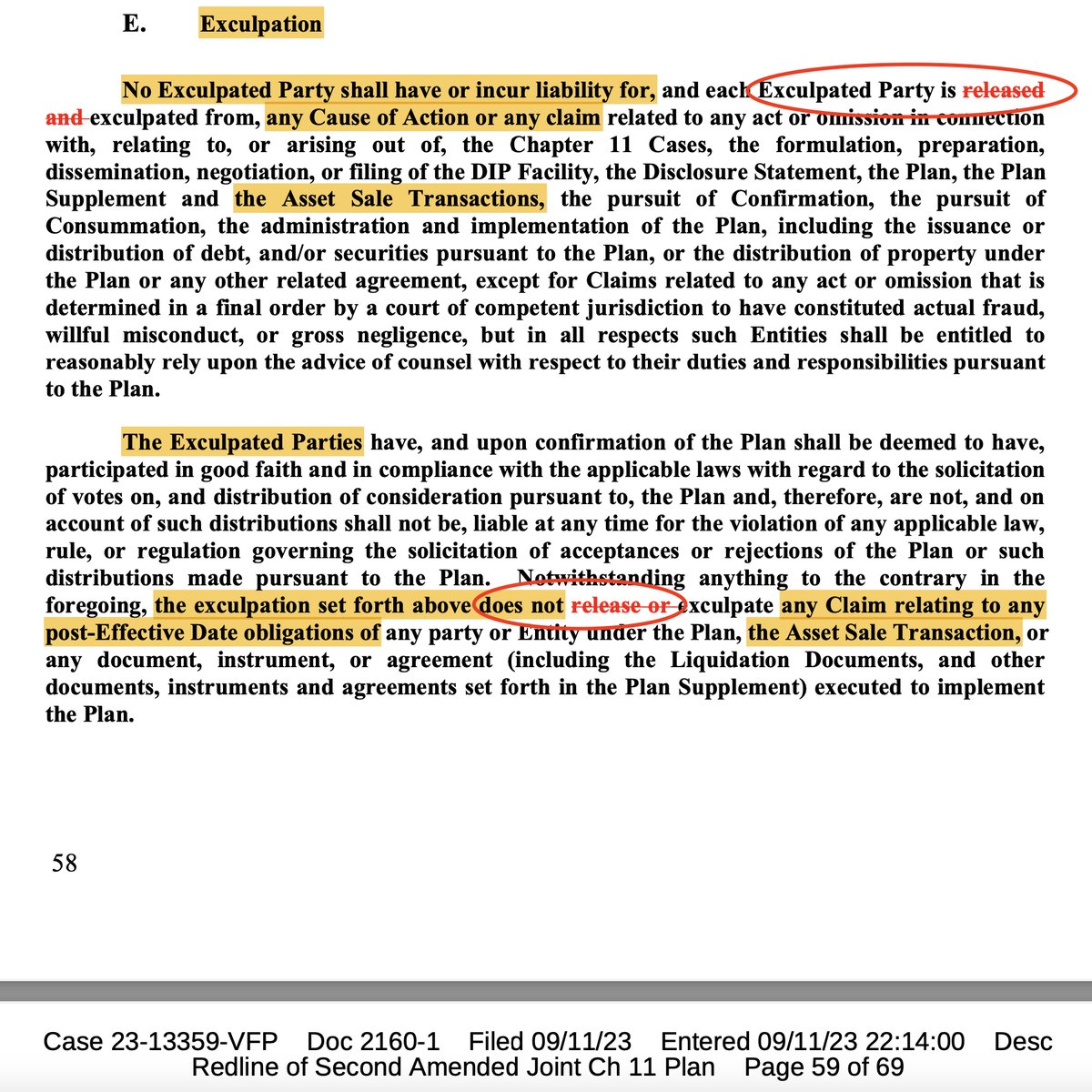

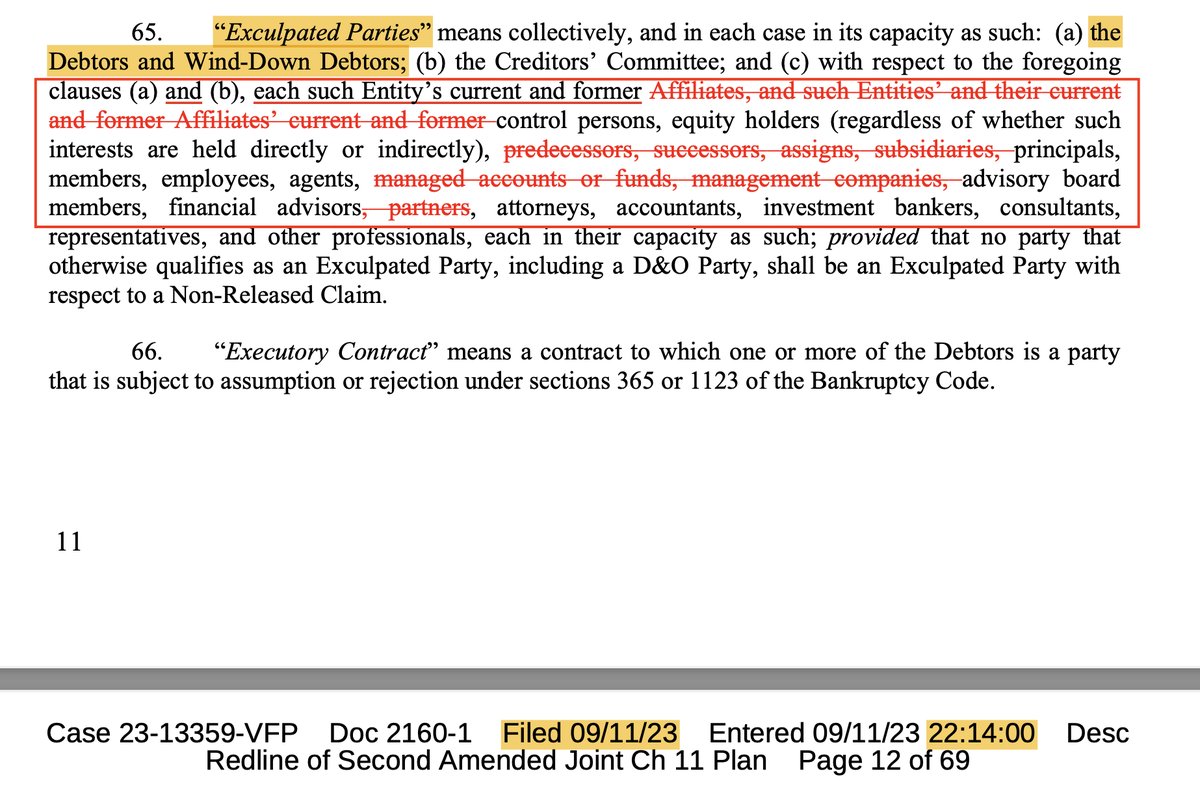

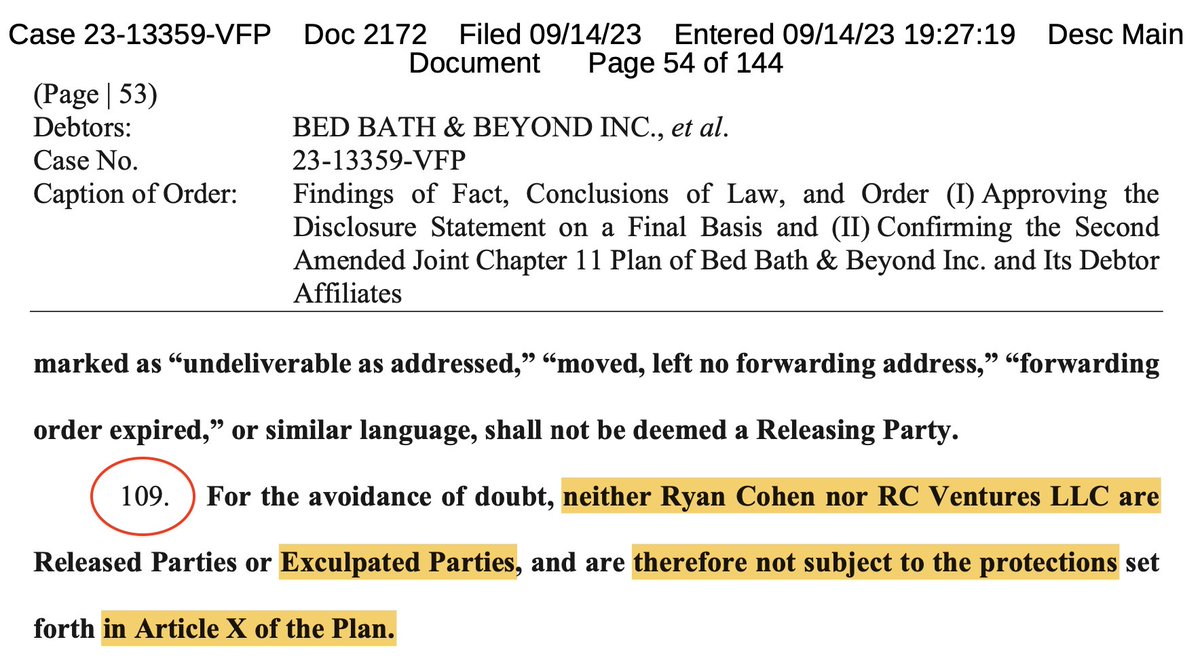

here are some more examples of the Plan language having been modified at the same time that the addition occurred of RC not being an Exculpated Party under the Plan, thereby not having the protections offered within the $BBBY Plan. I will highlight the most obvious one here:

remember, the Plan has already been voted on. these modifications to the Exculpated Party language are happening the night before the Confirmation Hearing and are uploaded at 10:14pm. these are not oopsie mistakes. at this point in the Chapter 11, the Plan is prepared to be brought before Judge Kaplan for Confirmation the next day.

and yet, at the same time that RC is now-added as not being a Released or Exculpated Party—as requested by Bratya, a non-participant in the $BBBYQ Chapter 11, but as the Plaintiff in the Class Action against RC, and threatening to object to the Confirmation of the Plan for Bed Bath—we see the Plan modified in statements involving the Exculpation and affiliates.

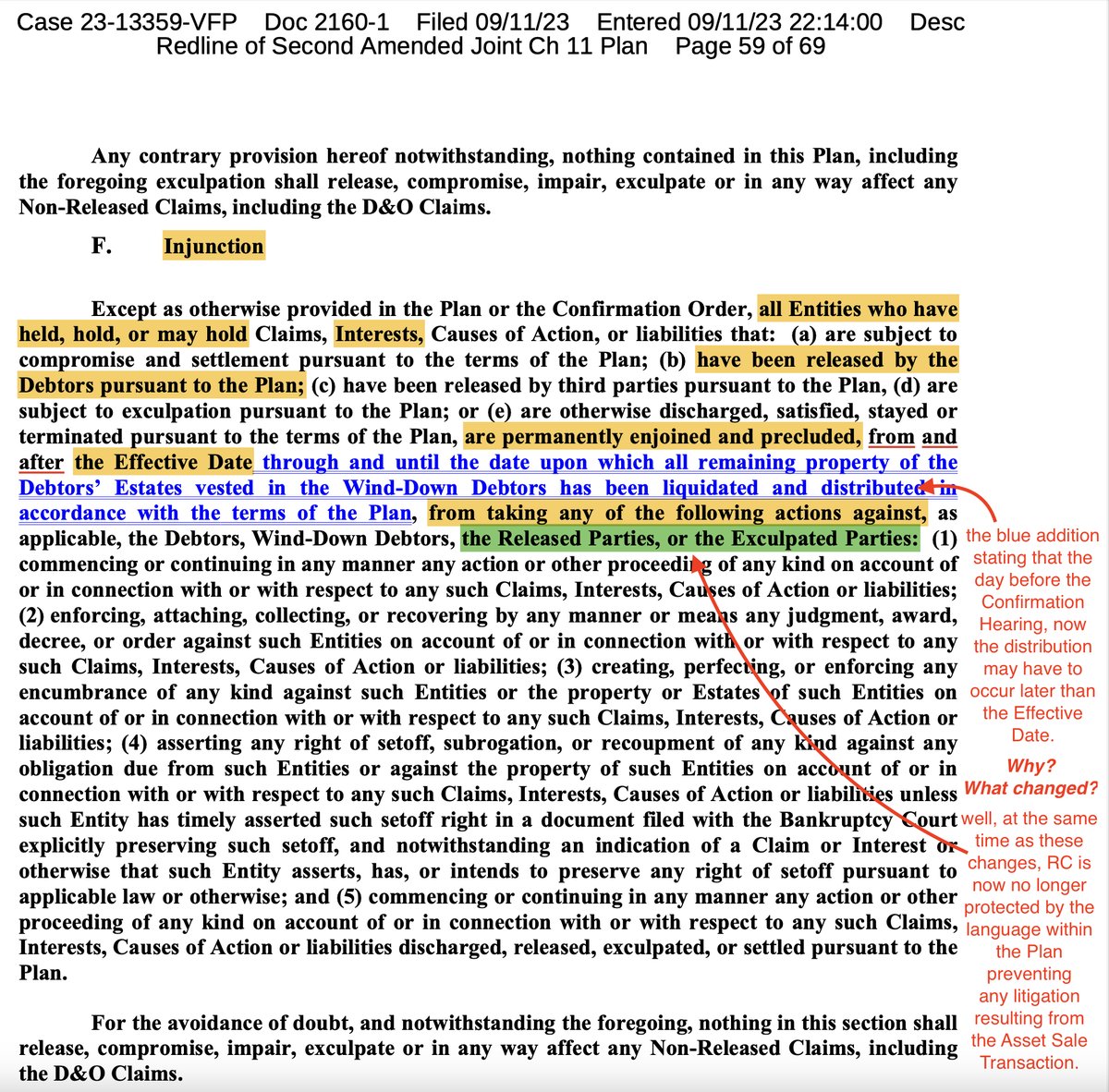

additionally, we see legal language added, that only as of now, the day before the Confirmation Hearing, everything may not be completed by the Effective Date:

"through and until the date upon which all remaining property of the Debtors' Estates vested in the Wind-Down Debtors has been liquidated and distributed in accordance with the terms of the Plan,"

what are the odds?

unless,.. RC is the Holder of Interests, who agreed to the third-party release in exchange for "substantial consideration" with multiple parties, which included the contributions to reach agreement for the Asset Sale Transaction,.. which had not been able to have been consummated because Bratya's Class Action lawsuit against RC was open until just two weeks ago.

the plan man himself acknowledges in the most-recent PCR filings in January 2025 that the rights of the Holder of Interests remain acknowledged, intact and date upon which their distribution can occur is "unknown at this time."

as noted in Part 3 of the PCR filings for the separately documented 7 subsidiaries:

"Part III: Recoveries to Holders of Claims and Interests Under Confirmed Plan:

“Total Anticipated Payments Under Plan” are unknown at this time.."

emphasis mine.

I believe that this has been the "hold up." everyone always said "push the button, RC", but no one thought to ask if doing so would expose RC to litigation en masse. in all fairness, no one considered it either. I confidently believe we have discovered the methods and mechanisms of what the future emergence and pathway to recovery will be—the Asset Sale Transaction, pursuant to the third-party release, effectuated by the Holder of Interests.

11

55

344

22,391

a deep dive into the definition of the word "Interests" in the $BBBYQ Confirmed Plan of Reorganization, its use throughout the Plan and legal language that allows for a future distribution for former shareholders.

youtu.be/s3aUVz1M_As

Part 1: Interests

in my first video I explore the definition of the word "Interests" ...

youtube.com 13

26

163

8,503

yay! I've uploaded my $BBBYQ video series to YouTube.

the channel link is: YouTube.com/@jake2b and here is a playlist link for all of the videos: youtube.com/playlist?list=PL…

I hope they are still helpful and I'll be adding more videos soon. I appreciate everyone's kind words and support plus the naysayers for the good laughs!

68

104

620

35,949

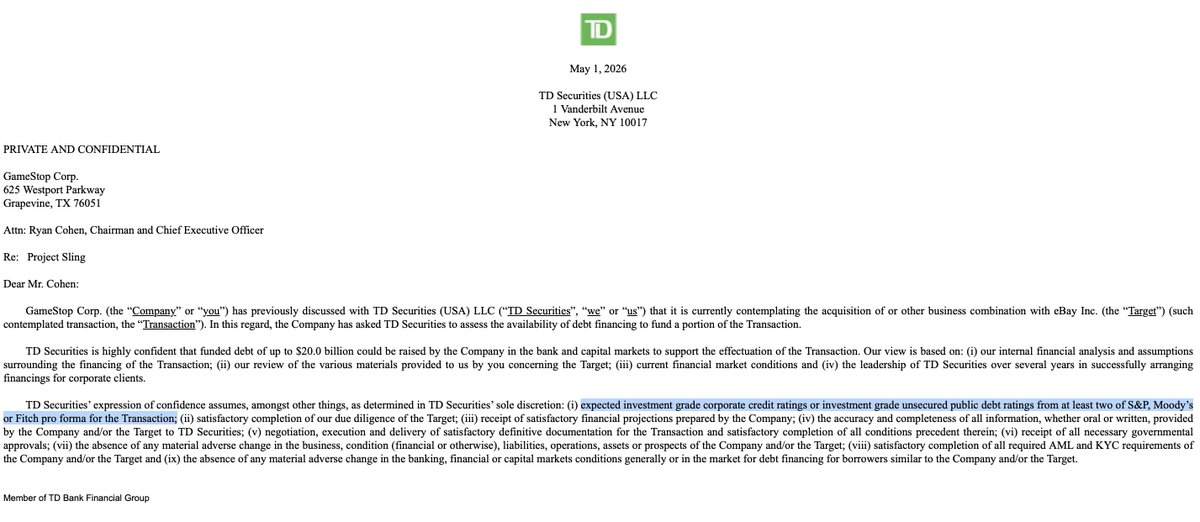

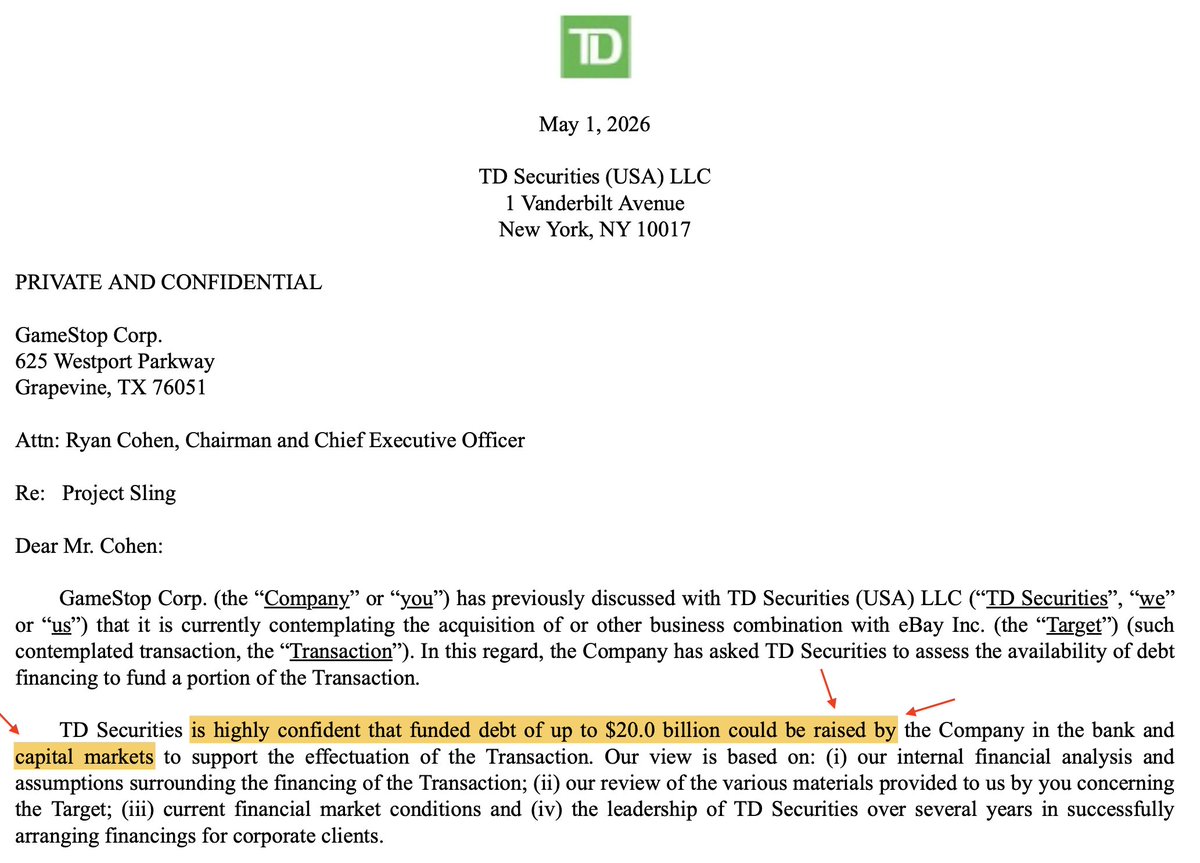

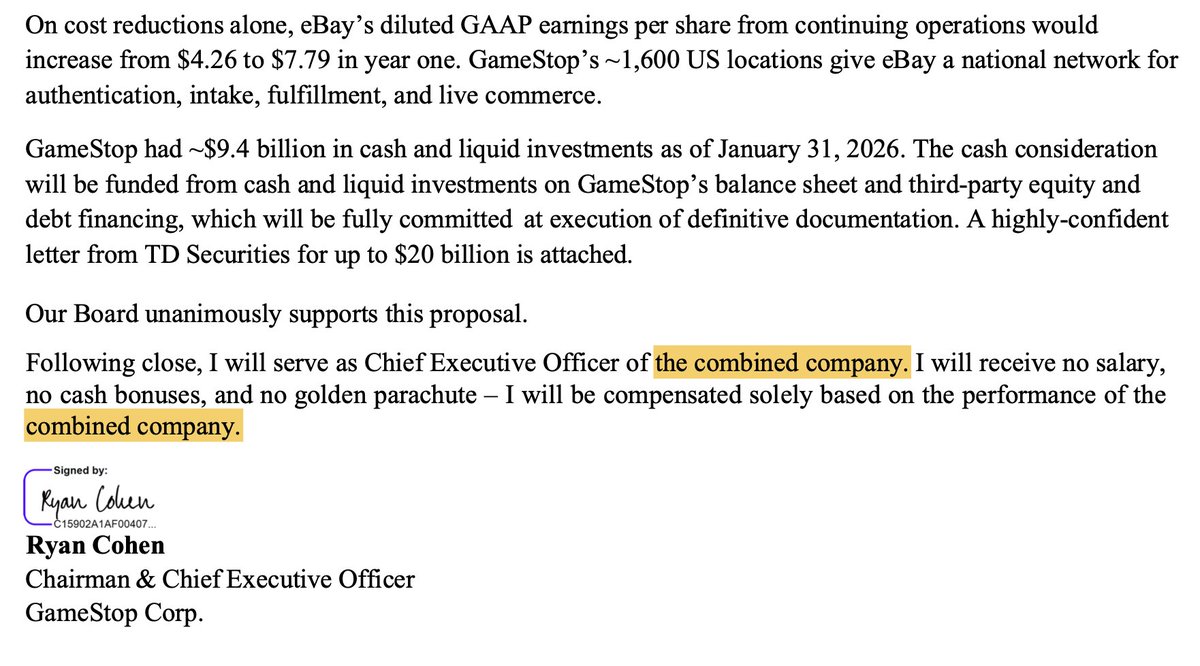

looking for clues it seems quite clear in my opinion that when $GME counters or amends their purchase offer of $EBAY there will be a rather significant change in the deal structure.

the key to the financing is TD Bank seeing an "investment grade" credit rating. if you do the math you know that this is not possible under the current terms because it would bring the combined company's leverage to somewhere around a ~9x ebitda.

I think that is pretty far out and would not meet "investment grade". this has been documented and I highlight it because I do think the credit rating will be achieved. how could the offer be amended to be <5x ebitda? I think there is one realistic pathway and it is through forming an investor group or a private equity co-investor.

what if a deal sponsor enters with a large cash infusion into $GME? in exchange they could get a large minority stake of the company in shares, be issued preferred shares or convertibles. the reason for it is in corporate credit agreements rating agencies look at private equity cash injections as equity/ownership and not debt. so lowering the leverage vs. ebitda becomes simple you have someone that sponsors the deal for x amount of dollars and the company doesn't need as much from TD Bank and the bond market.

i.e. for half cash half stock they need 28 billion in cash. PE or a friendly investor shows up with an 18 billion investment to be a part of the deal, the need from TD Bank comes down to 10 billion and voila! a debt multiple to ebitda <5.

I still believe that we will see GameStop issue bonds but it won't be the only way they raise funds. I wonder if there is anyone out there who sees value in big dog?

“with foresight, the excitement was palpable.”

bonds. by the time everyone else realizes GameStop will not have to deplete 88% of their balance sheet cash, excitement will be off the charts.

bonds are not notes.

$GME

43

74

511

58,180

I started a YouTube channel that will begin with my $BBBYQ video series uploaded if you prefer to watch or listen there. I've starting with Part 1: Interests; here is a direct link: youtu.be/s3aUVz1M_As

more soon!

Part 1: Interests

in my first video I explore the definition of the word "Interests" ...

youtube.com 76

186

874

72,433

$GME earnings were so good I think it might have slipped under everyone’s nose that it could be a prerelease ahead of a material event.

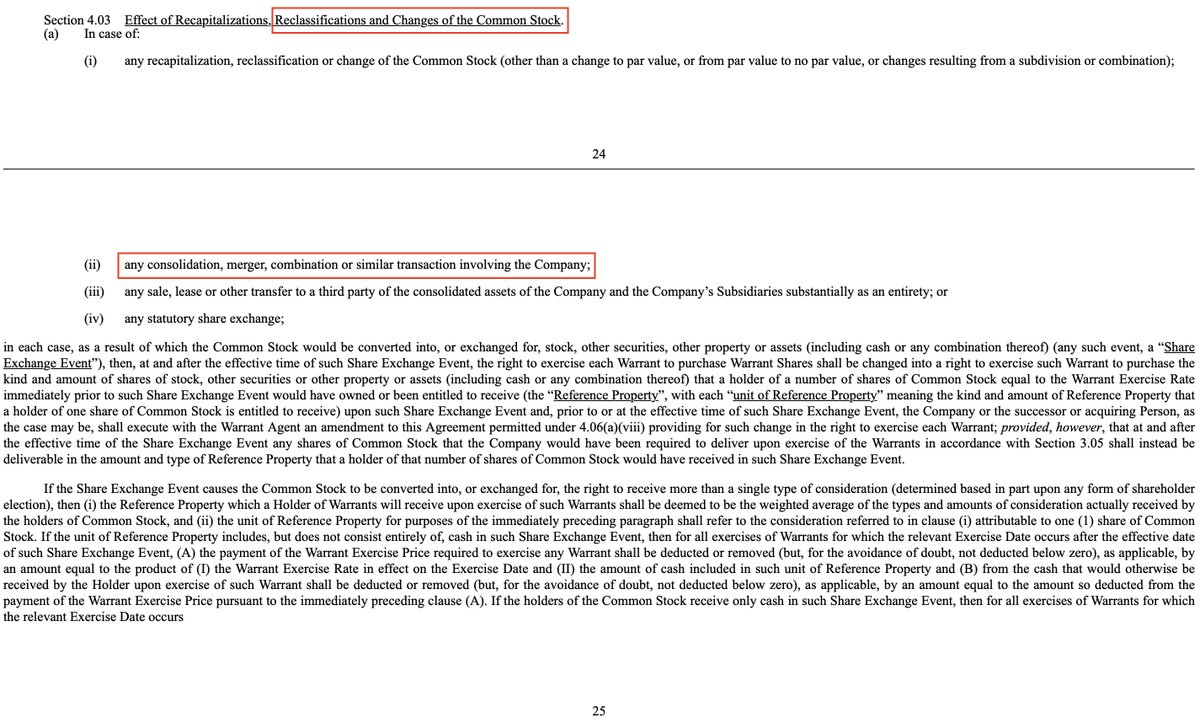

after RC's interview with the WSJ it really looks like all the pieces are starting to fit together for $GME. quoted to this post is my observation about GameStop filing a templated bond indenture back in October with the modified S-3 from the warrants.

so now we have:

• a warrant agreement that outlines a "Share Exchange Event" if there were to be a merger or acquisition, a new class of shares, etc. (section 4);

• a ready-to-go bond indenture;

• the GameStop board announcing a compensation package for RC;

• big dog himself telling the WSJ that he is looking to make a large acquisition.

who needs forward guidance when the roadmap is this clear!

the bond indenture is a finalized, execution-ready document. there is just no way that they filed this as a "just in case" and it became painfully obvious after the interview article. you don't file detailed indenture documents unless bond issuance is part of a concrete capital plan. that's when it clicked.

when the compensation package was revealed it whimsically (read: intentionally) did not have a set shareholder vote date set and just said "sometime in March or April". none of it is coincidence I believe all of it is planned around the Company's annual earnings release and they are going to issue bonds to help fund their big acquisition(s). the only question is in what order?

I thought to myself, for someone who never "telegraphs their strategy", why is RC saying that they are ready to utilize the investment policy and make an acquisition? what purpose does it serve? then it hit me. are they doing the bond roadshow right now?

here's the thing. almost half of GME's cash is from the convertible notes and if they just went and marketed a bond raise it could face significant skepticism and demand weak pricing, maybe even get a lacklustre credit rating. investors might push for a higher yield premium for their risk.

but if big dog is talking to the main M&A writer for the Wall Street Journal, well, that changes everything. bond markets like certainty and RC just gave out his plan for all of them to hear. I think he is providing a use of proceeds narrative and creating the business rationale that bond investors like to hear.

here I thought that the vote on the compensation package was going to be first but it may be the last piece. in my opinion this unfolds in one of two ways:

one:

• first will come the annual earnings to give an up-to-date financial baseline before major strategic moves. this will show credibility with institutional investors before asking them to evaluate a major acquisition;

• make an acquisition announcement in hopes of boosting the stock price and creating momentum heading into the shareholder vote on the pay package;

• issue the bonds to offset the cost, fill a funding gap or if the acquisition is announced with some lead time, get the financing in order before closing.

• shareholders can evaluate big dog's strategy and vision ahead of the vote to approve the pay package.

I think the pay package and its astronomical targets might create stock price volatility that could complicate bond pricing so I think no matter what, it happens last. (this places all other events before or inside of "March or April").

two:

• earnings first for up-to-date financials;

• everything else from the first point stays the same but the acquisition and bond issuance announcements are bundled together to signal confidence into the stock price (against the price of an acquisition);

• pay pack vote last to show the vision and get approval.

remember, the bond indenture was filed back in October 2025 so every step has been planned out for a long time. they have probably engaged with the Investment banks for months already. same goes for anchor investor(s) (maybe this is how Mr. Almadeed fits into the picture in all this).

three:

• things are happening really quickly, the bonds are about to be marketed or are right now and this is why big dog gave the interview to WSJ.

• earnings will come afterwards because "things are moving fast" for whatever reason.

the biggest signal of this option happening will be an earnings pre-release like there was in May 2024 before the first ATM offering.

I believe that the second option is the most likely. RC communicating the plan to the news was a bit of a curve ball on the timeline, but maybe it is to negotiate attractive bond pricing and have investors lined up well ahead of time, just like they did with the templated indenture.

it makes the most sense to announce the acquisition and financing together as a complete and strategic plan because it will make everyone happy. the bond investors hear about specific use of proceeds and a clear business rationale; equity investors will be happy because it avoids the uncertainty of announcing an acquisition without explaining how it will be paid for. that will absolutely insulate downward pressure on the stock if it is known the current cash pile won't be depleted. you tell the market one comprehensive story. bond buyers can see the complete transaction, (maybe even giving GME leverage to negotiate better pricing?), create some excitement and momentum from a major announcement that could drive stock price acceleration ahead of the pay pack vote.

the really exciting thing about the bond indenture is it opens the flood gates for how big the GameStop Board could be thinking.

rocket. wee. genesis. isn't it obvious?

45

110

867

54,028

I’m excited about the share buyback authorization like everyone else but in my opinion, I don’t think it will be utilized now. lowering the balance sheet cash would make it more difficult to conduct the bond roadshow, both in the ability of how much can be raised and would result in higher interest rates from fixed-income investors based on risk. you want to look strong when marketing yourself for investment.

if a genie granted me a wish the ideal series of events would be to raise a ton of corporate debt, have the market sink the stock price to middle earth on this news (“oh no, huge leverage! they’re going bankrupt!”), buy back down there, note holder arbs go super long, the stock price explodes, present the tender offer to eBay shareholders at that price with the goal of dipping into authorized shares as little as possible.

we’ll see.

8

14

225

7,669

part 7: I would like to share compelling points relating to the HBC equity raise and its use to secure the position of the Holder of Interests, which forced participation in the $BBBYQ third-party release. I hope you like it.

$BBBY

(old).

part 6: my thoughts on the January 13, 2023 LBO and its intended (and failed) use to force $BBBYQ into insolvency.

I hope you like it. $BBBY (old).

79

154

647

58,212

a handful of comments to this post presented a counter that the participants were not friendly to $BBBYQ and they wanted to exit their investment.

this argument fails logic but it was also not possible. the Company issued restricted shares which means the investors had to hold them for a minimum of 6 months, sometimes up to a year before they could transact with them.

thank you for your comment @JuicyPabl0.

Rule 506(c): sec.gov/resources-small-busi…

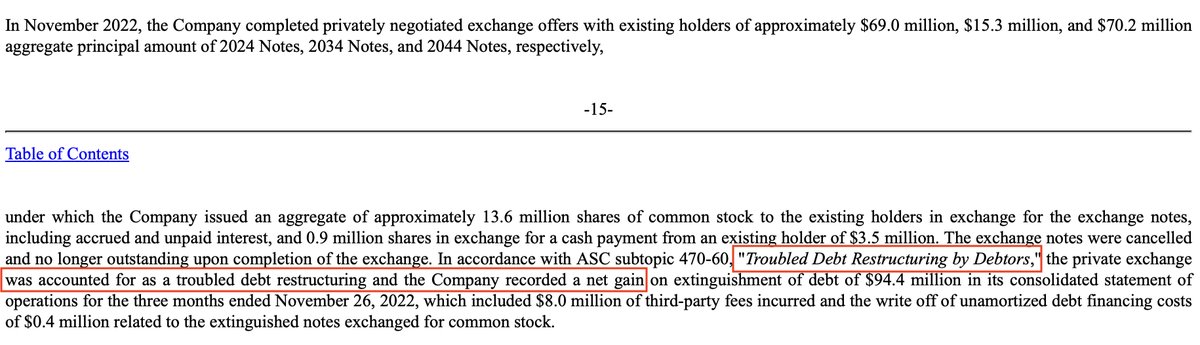

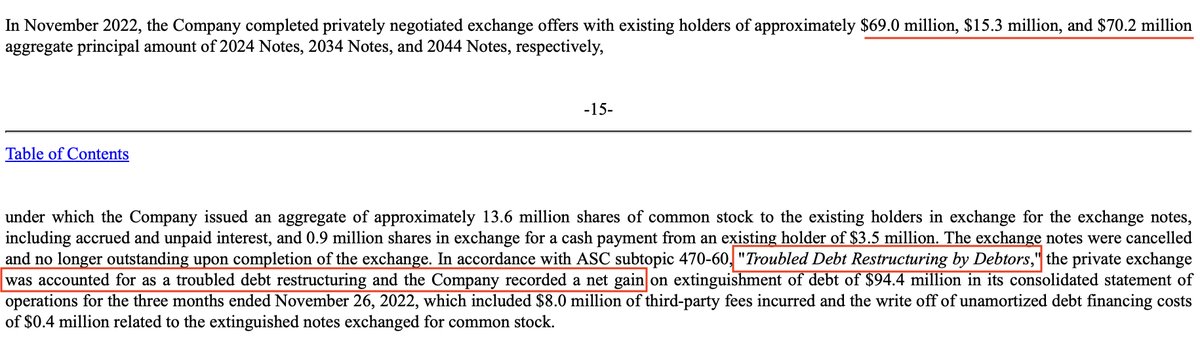

I was reading through old $BBBYQ SEC filings and came across something that really stood out. whatever the intentions of the affiliates and/or Purchaser, the assets had to have been secured at the end of 2022 in some way.

think back to the private bond exchanges; there was first a single investor, then an institutional group that followed by retiring their bonds for shares some time between November 14 and December 6, 2022. here is what I had never caught before:

[image 1]

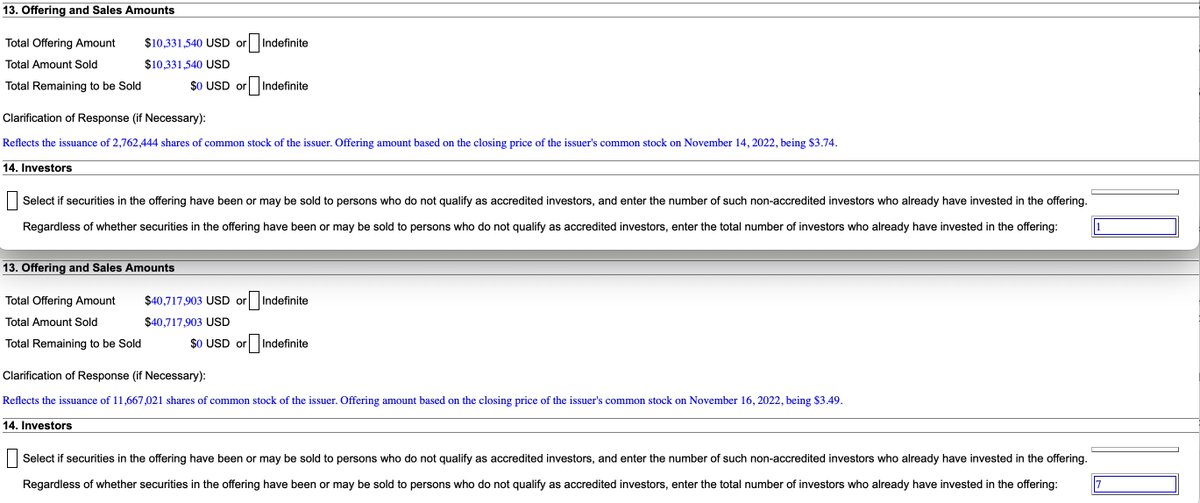

thanks to accounting requirements there is disclosure in the 10-Q that the exchange was performed under what is called a "troubled debt restructuring". that can only be used under very specific circumstances, say if a company discloses that it may not be able to continue as a going concern. if we dive into the math on the deal we will see that whoever participated in the exchange was friendly to the company. here's why:

[image 2]

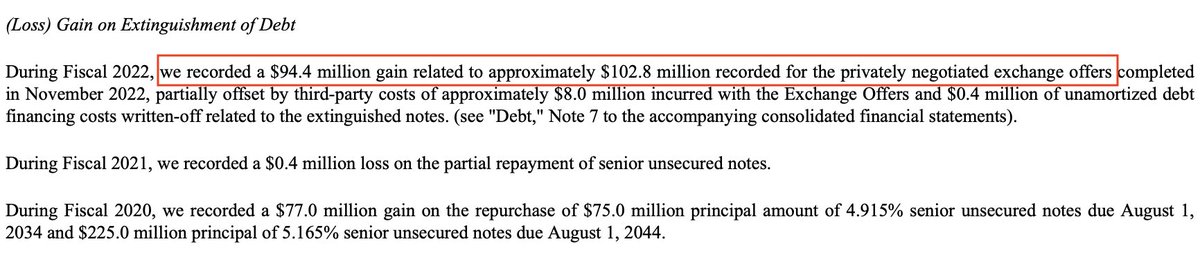

the aggregate principal amount retired through the bond exchange:

69.0 (2024) 15.3 (2034) 70.2 (2044) = 154.5 million dollars worth of bond debt.

[image 3]

but investors only received:

first Form D: 2,762,444 shares which was an offering amount of 10,331,540$;

second Form D: 11,667,021 shares which was an offering amount of 40,717,903$;

10,331,540 40,717,903 = 51,049,443$.

[image 3]

154.5 million of debt was retired in exchange for 51 million dollars’ worth of shares. the bond holders exchanged at 0.33 on the dollar when they could have just sold them on the open market at the time for a better return plus the individual investor gave the Company another 3.5 million dollars cash for 0.9 million additional shares.

the Company obviously benefitted tremendously from this deal, recording a 94.4 million dollar gain (the net difference) on their 10-Q. who would do that? the only way it makes sense is if the former bond, then equity holders received something more than just the shares in return. the only alternative explanation is preferring to lose money over open market sales to help the Company.

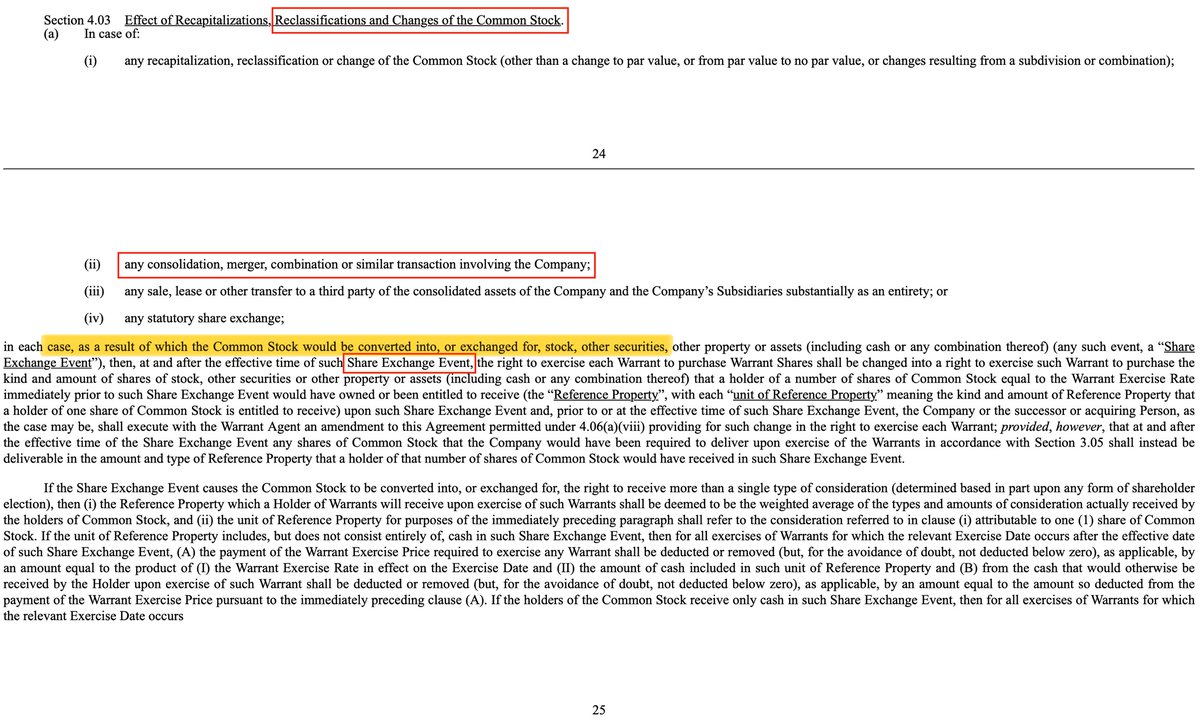

[image 4]

fun little side fact, looking at the TSO from the 10-Q (which was late!) if you look at the share amount received by the institutional group they total 9.9444% ownership, just under 10% with no way to round up to 10% and be labelled an insider. two more fun facts, the Company filed that their 10-Q was going to be late on the same day the bond exchange was finally terminated with no more extensions, and, the "troubled debt restructuring" was only revealed in the 10-Q itself, over a month later.

to summarize: no investor retires their senior, secured debt instrument for junior, unsecured equity at a loss compared to open-market price to help the Company's balance sheet, unless they got something in return. this exchange retired 25% of all 2024 bonds, an imminent insolvency risk at the time.

so.. what did they get?

33

47

362

36,473

I was reading through old $BBBYQ SEC filings and came across something that really stood out. whatever the intentions of the affiliates and/or Purchaser, the assets had to have been secured at the end of 2022 in some way.

think back to the private bond exchanges; there was first a single investor, then an institutional group that followed by retiring their bonds for shares some time between November 14 and December 6, 2022. here is what I had never caught before:

[image 1]

thanks to accounting requirements there is disclosure in the 10-Q that the exchange was performed under what is called a "troubled debt restructuring". that can only be used under very specific circumstances, say if a company discloses that it may not be able to continue as a going concern. if we dive into the math on the deal we will see that whoever participated in the exchange was friendly to the company. here's why:

[image 2]

the aggregate principal amount retired through the bond exchange:

69.0 (2024) 15.3 (2034) 70.2 (2044) = 154.5 million dollars worth of bond debt.

[image 3]

but investors only received:

first Form D: 2,762,444 shares which was an offering amount of 10,331,540$;

second Form D: 11,667,021 shares which was an offering amount of 40,717,903$;

10,331,540 40,717,903 = 51,049,443$.

[image 3]

154.5 million of debt was retired in exchange for 51 million dollars’ worth of shares. the bond holders exchanged at 0.33 on the dollar when they could have just sold them on the open market at the time for a better return plus the individual investor gave the Company another 3.5 million dollars cash for 0.9 million additional shares.

the Company obviously benefitted tremendously from this deal, recording a 94.4 million dollar gain (the net difference) on their 10-Q. who would do that? the only way it makes sense is if the former bond, then equity holders received something more than just the shares in return. the only alternative explanation is preferring to lose money over open market sales to help the Company.

[image 4]

fun little side fact, looking at the TSO from the 10-Q (which was late!) if you look at the share amount received by the institutional group they total 9.9444% ownership, just under 10% with no way to round up to 10% and be labelled an insider. two more fun facts, the Company filed that their 10-Q was going to be late on the same day the bond exchange was finally terminated with no more extensions, and, the "troubled debt restructuring" was only revealed in the 10-Q itself, over a month later.

to summarize: no investor retires their senior, secured debt instrument for junior, unsecured equity at a loss compared to open-market price to help the Company's balance sheet, unless they got something in return. this exchange retired 25% of all 2024 bonds, an imminent insolvency risk at the time.

so.. what did they get?

63

100

557

88,987

“I was totally going to buy this, spent hundreds of hours planning the venture, had a roadmap to 600 million revenue, recruited executive talent and then I didn’t because the IP sold for 3.5-23.5 million dollars less than what I was willing to pay.”

$BBBYQ

52

95

723

55,054

“with foresight, the excitement was palpable.”

bonds. by the time everyone else realizes GameStop will not have to deplete 88% of their balance sheet cash, excitement will be off the charts.

bonds are not notes.

$GME

after RC's interview with the WSJ it really looks like all the pieces are starting to fit together for $GME. quoted to this post is my observation about GameStop filing a templated bond indenture back in October with the modified S-3 from the warrants.

so now we have:

• a warrant agreement that outlines a "Share Exchange Event" if there were to be a merger or acquisition, a new class of shares, etc. (section 4);

• a ready-to-go bond indenture;

• the GameStop board announcing a compensation package for RC;

• big dog himself telling the WSJ that he is looking to make a large acquisition.

who needs forward guidance when the roadmap is this clear!

the bond indenture is a finalized, execution-ready document. there is just no way that they filed this as a "just in case" and it became painfully obvious after the interview article. you don't file detailed indenture documents unless bond issuance is part of a concrete capital plan. that's when it clicked.

when the compensation package was revealed it whimsically (read: intentionally) did not have a set shareholder vote date set and just said "sometime in March or April". none of it is coincidence I believe all of it is planned around the Company's annual earnings release and they are going to issue bonds to help fund their big acquisition(s). the only question is in what order?

I thought to myself, for someone who never "telegraphs their strategy", why is RC saying that they are ready to utilize the investment policy and make an acquisition? what purpose does it serve? then it hit me. are they doing the bond roadshow right now?

here's the thing. almost half of GME's cash is from the convertible notes and if they just went and marketed a bond raise it could face significant skepticism and demand weak pricing, maybe even get a lacklustre credit rating. investors might push for a higher yield premium for their risk.

but if big dog is talking to the main M&A writer for the Wall Street Journal, well, that changes everything. bond markets like certainty and RC just gave out his plan for all of them to hear. I think he is providing a use of proceeds narrative and creating the business rationale that bond investors like to hear.

here I thought that the vote on the compensation package was going to be first but it may be the last piece. in my opinion this unfolds in one of two ways:

one:

• first will come the annual earnings to give an up-to-date financial baseline before major strategic moves. this will show credibility with institutional investors before asking them to evaluate a major acquisition;

• make an acquisition announcement in hopes of boosting the stock price and creating momentum heading into the shareholder vote on the pay package;

• issue the bonds to offset the cost, fill a funding gap or if the acquisition is announced with some lead time, get the financing in order before closing.

• shareholders can evaluate big dog's strategy and vision ahead of the vote to approve the pay package.

I think the pay package and its astronomical targets might create stock price volatility that could complicate bond pricing so I think no matter what, it happens last. (this places all other events before or inside of "March or April").

two:

• earnings first for up-to-date financials;

• everything else from the first point stays the same but the acquisition and bond issuance announcements are bundled together to signal confidence into the stock price (against the price of an acquisition);

• pay pack vote last to show the vision and get approval.

remember, the bond indenture was filed back in October 2025 so every step has been planned out for a long time. they have probably engaged with the Investment banks for months already. same goes for anchor investor(s) (maybe this is how Mr. Almadeed fits into the picture in all this).

three:

• things are happening really quickly, the bonds are about to be marketed or are right now and this is why big dog gave the interview to WSJ.

• earnings will come afterwards because "things are moving fast" for whatever reason.

the biggest signal of this option happening will be an earnings pre-release like there was in May 2024 before the first ATM offering.

I believe that the second option is the most likely. RC communicating the plan to the news was a bit of a curve ball on the timeline, but maybe it is to negotiate attractive bond pricing and have investors lined up well ahead of time, just like they did with the templated indenture.

it makes the most sense to announce the acquisition and financing together as a complete and strategic plan because it will make everyone happy. the bond investors hear about specific use of proceeds and a clear business rationale; equity investors will be happy because it avoids the uncertainty of announcing an acquisition without explaining how it will be paid for. that will absolutely insulate downward pressure on the stock if it is known the current cash pile won't be depleted. you tell the market one comprehensive story. bond buyers can see the complete transaction, (maybe even giving GME leverage to negotiate better pricing?), create some excitement and momentum from a major announcement that could drive stock price acceleration ahead of the pay pack vote.

the really exciting thing about the bond indenture is it opens the flood gates for how big the GameStop Board could be thinking.

rocket. wee. genesis. isn't it obvious?

36

112

725

109,714

imagine the surprise after $EBAY formally declines the purchase offer, $GME counters with an “all-cash, no stock” deal. with the backing of a financier/investment group it would be quite an ace up the sleeve, nullifying the board’s reasons for declining and thereby cornering them into acceptance under fiduciary duty.

the coy responses about the how they can pull it off would sure start to make a lot of sense. now, imagine if plan b was plan a. the best ones are always many steps ahead.

66

132

956

40,136

“in hindsight, it will all seem so obvious.”

$GME

what if the ace up the sleeve for $GME is not about the actual acquisition, but what happens after the acquisition? what if it is Delaware Law Title 8, Chapter 1, Subchapter IX. Merger, Consolidation or Conversion.

specifically §251(g)?

like many I was surprised to see RC doing the media tour and for the first time, hyping how big their plans will be. I mentioned before that a likely explanation could be they are doing a roadshow for an upcoming traditional bond offering. I also couldn’t help but worry when I read some snippets:

“it's gonna be really big. Really big. Very, very, very big," Cohen said of the size of the acquisition.”

“this is something that really has never been done before within the history of the capital markets.”

“it has the "potential to make [GameStop] worth several hundreds of billions of dollars.”

..because no matter what the Board was planning, the market could make this the largest sell-the-news event in history to try and curb their momentum and sentiment around the pivot of GameStop into a holding company.

why would big dog do that? why would he not say basically anything for 5 years then suddenly risk shooting himself in the foot by making grandiose claims about their first acquisition? lets not overlook that in the CNBC article he claims this one acquisition could propel the market cap of the company to the extent his entire pay package vests..

it got me thinking about why he would be so confident. then I found §251(g):

“Delaware General Corporation Law Section 251(g) allows a corporation to reorganize into a holding company structure without requiring a stockholder vote. This statutory provision facilitates mergers with a wholly-owned subsidiary, ensuring the holding company has the same charter provisions as the original corporation, often used for corporate restructuring or, historically, for adopting anti-takeover measures.”

emphasis mine. it is mainly used to create a new, top-level holding company where the original parent corporation used to be. That old parent co becomes a subsidiary and shareholders receive identical shares in the new holding company.

“Section 251(g) facilitates a holding company reorganization merger where outstanding shares of the original corporation are automatically converted into equivalent shares of the new holding company upon the merger’s effective time, provided all statutory conditions are met (e.g., identical rights and no tax recognition). This conversion is seamless and does not require surrendering or recalling physical certificates or shares,..”

hang on.. I know exactly what I thought of when I read that. do you remember this?

this sure provides a convenient explanation. oh, I can already hear the naysayers.. upon the merger's effective time. do you now remember what happened immediately before September 2024? the Board closed their credit facility and less than one month later, a pre-negotiated, pre-settled agreement was filed by the FTC.

I wrote at the time that I believed the Company applied to the FTC for a pre-merger certificate, hence why the settlement came out when it did and that the issuance of the certificate occurred after the second, 30-day review period following the filing of RC's settlement of the FTC violation. that is why he tweeted "yolo" exactly 60 days after the application for the certificate, because he got it.

OK back on topic. guess what else?

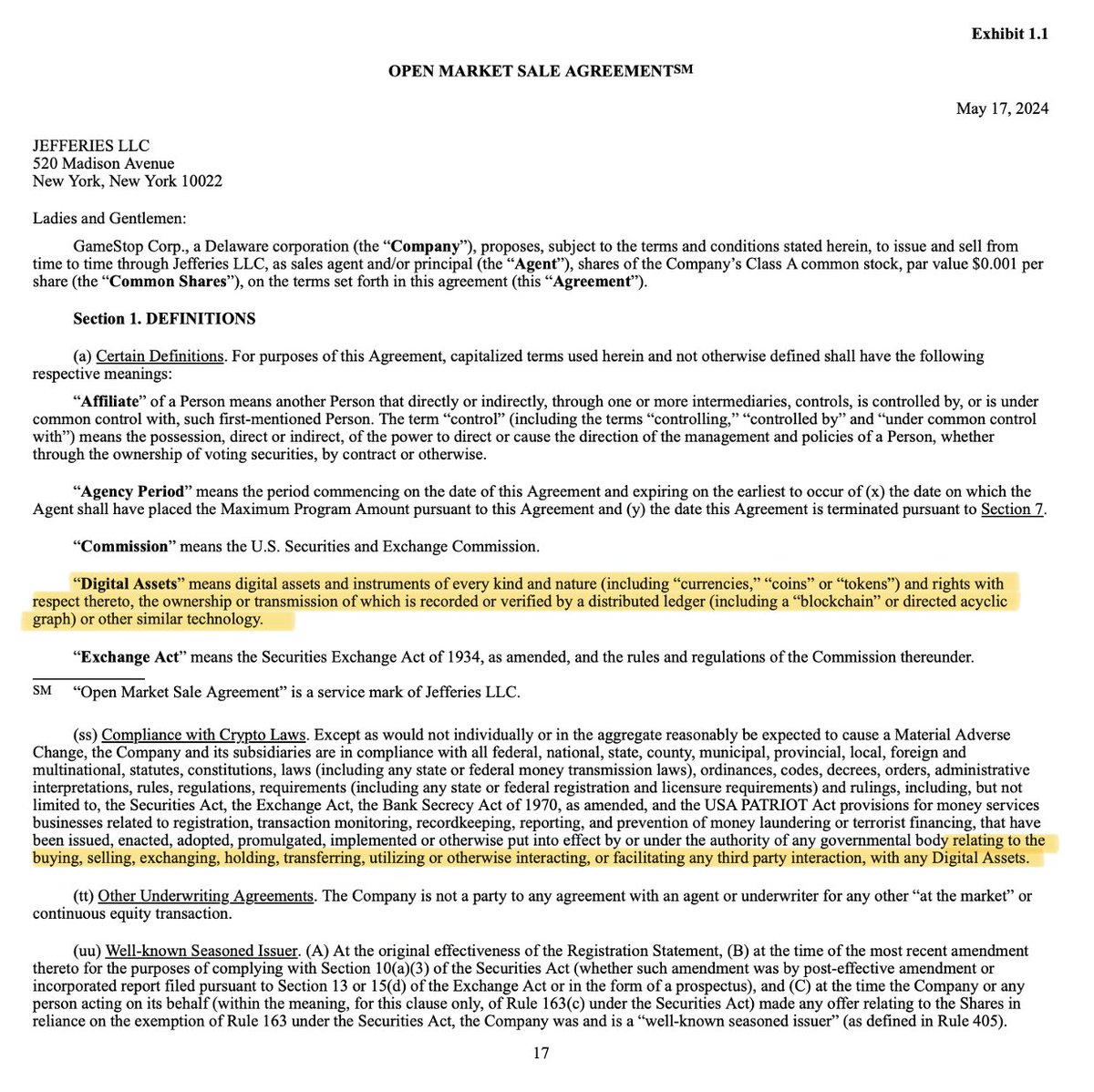

if they want to, a company can reissue shares under §251(g) as tokenized shares even if they weren’t tokenized before, as long as the tokenized shares are identical in all the important respects like rights, voting powers, etc. to the original shares. this is explained in §251(g)(2).

“Since §251(g) allows for a holding company reorganization where the new parent issues shares that mirror the originals, the holding company can adopt a blockchain-based stock ledger for its issuance process. This doesn’t violate the “identical” requirement because the form of record-keeping (traditional vs. blockchain) is administrative, not substantive—much like switching from certificated to uncertificated shares, which Delaware law expressly supports.”

hang on now.. do you remember the S-3 that was filed in May 2024, defining digital assets inside of the sale agreement contract between GME and Jefferies? for their share offering?

GameStop’s current corporate structure looks like this: GameStop Corp (parent) holding company → GameStop Inc (subsidiary) that manages retail operations. the shares are issued for ownership of the parent company. important to understand that the legacy business is managed by a subsidiary.

what if in the future GameStop wanted to maintain the brand identity for their retail business as the premier destination for how to spend your leisure time, but wanted to have a new name for their investment behemoth diversified holding company.. like Teddy?

they could:

• acquire a company that they find undervalued or owning an asset they would want;

• place it as a subsidiary of GameStop Corp;

• perform a Section 251(g) corporate reorganization;

• and name it whatever they want.

then it becomes Teddy (probably) → GameStop Corp → GameStop Inc.

you may be wondering why? ..well, tell me why shares of GME were labelled new class in 2024? kidding aside, this allows GameStop Corp to keep its current roles: strategic oversight, capital allocation, governance.. the investment policy.., and allows a new parent corporation to be formed to hold all of the acquisitions made by a dying, brick and mortar retailer-turned-investment fortress, managed by big dog and friends. and! it does not require a shareholder vote.

that could explain Section 4 of the warrant agreement, specifically why they chose to include legal definitions around a “Share Exchange Event” in the event of a reorganization:

it would explain the “new class” anomaly observed in September 2024 (or it was a private placement);

it would explain why the ATM agreement would require GME and Jefferies to have explained digital assets in a contract only to do with selling of their shares;

and lastly, it could explain why RC is so confident in his interviews with the news media.

talk about exciting times.

n.b.—this is just my personal opinion and fun speculation.

59

172

998

75,940

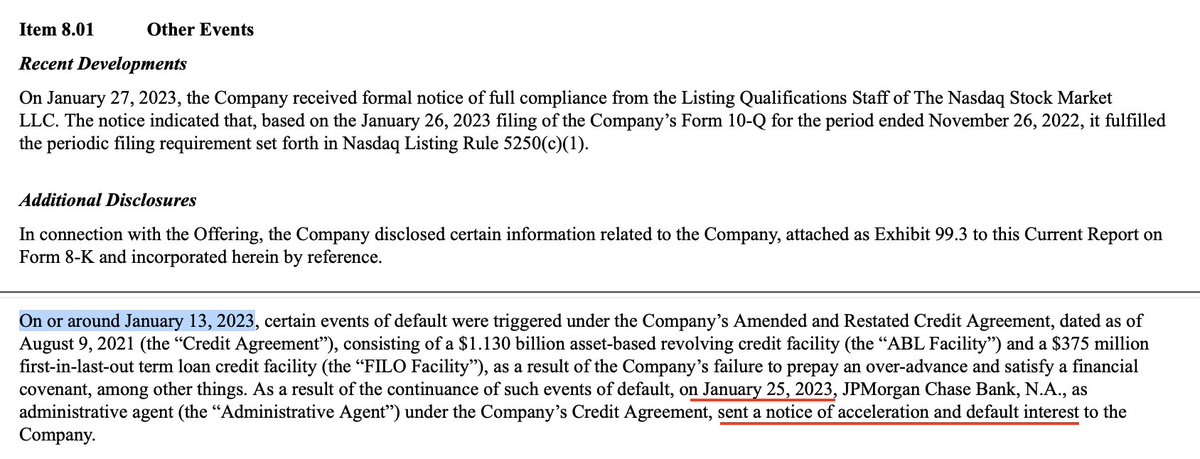

someone asked a great question in my last video post and I can't find it so I will post it here. the question was how could there have been an LBO without an 8-K or SEC filing? (paraphrasing).

in my opinion the point I want to make very clear her his that an LBO did not occur, that is what I emphasize throughout the last video. an LBO was attempted and was blocked because of contractual covenants within the credit agreements. there is an important difference.

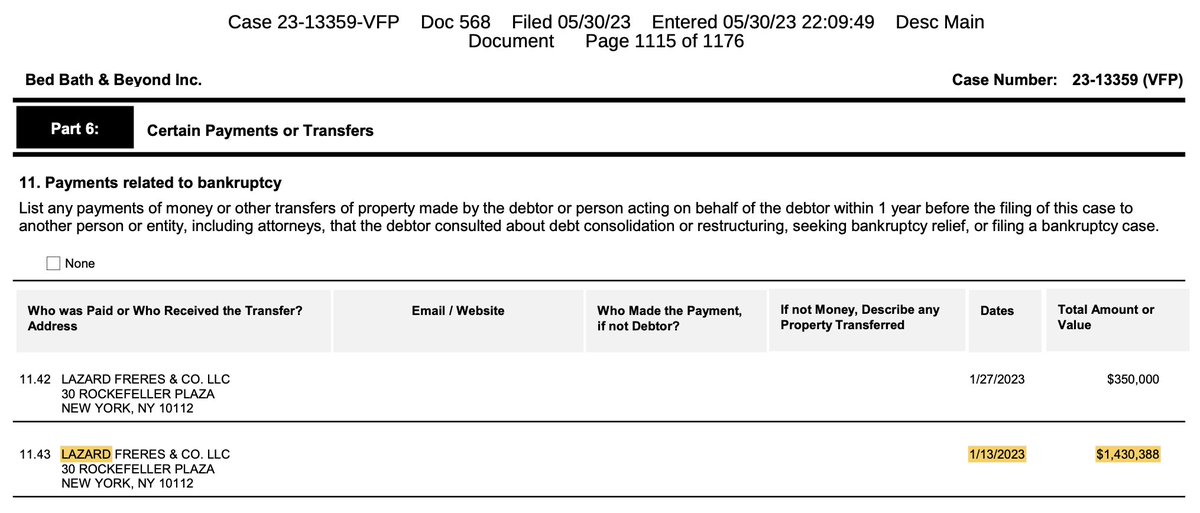

the easiest way to show how I arrived at this conclusion is to work backwards. we know that some kind of purchase offer for $BBBYQ had to have been offered on January 13. we know this because the sofa filed shows that Lazard, the financial advisor for old $BBBY was paid 1,430,388$ on this date.

when we read the Lazard engagement letter, we see that the only way to arrive at an odd-lot number like the one they were paid is if it were a percentage of a purchase offer.

we also know that there were no 8-K's filed for an activist shareholder or group to have taken a 40% position to effectuate a Change in Control of the company, therefore we know that it could not have been an attempt to buy the company through a tender offer, or other outcome through the common equity.

therefore, there are only two options. either someone attempted an LBO or a binding purchase offer was brought to the company and had to be rejected. it is very important to understand the threshold that has to be met for Lazard to have been paid their 1.4 million dollars and they are clearly outlined in their engagement letter. the company paid them their fee! this is not speculative.

we also know from the SEC filing which would later reveal that "certain events of default" happened to trigger default. two of those things were the prepayment of the ABL being in over advance (amount owed vs. collateralized inventory value) and satisfying a financial covenant, "among other things."

the SEC filing itself by the company admits that there were multiple events. since the LBO failed, it would have been inappropriate to identify it as a reason, maybe because that would have affected the market price of the company stock for example.

I then speculate in the video that I found it very odd there was a period of 12 days between when the events of default occurred, vs. when the priority loans were accelerated and cash dominion was enforced.

especially since, on that same day, Jan 13:

• Lazard received a payment resulting from an attempt to purchase the company or significant assets like BuyBuy Baby, and;

• the news ran articles that Sycamore Partners were trying to acquire BuyBuy Baby;

• the company filed multiple events of default were triggered, and;

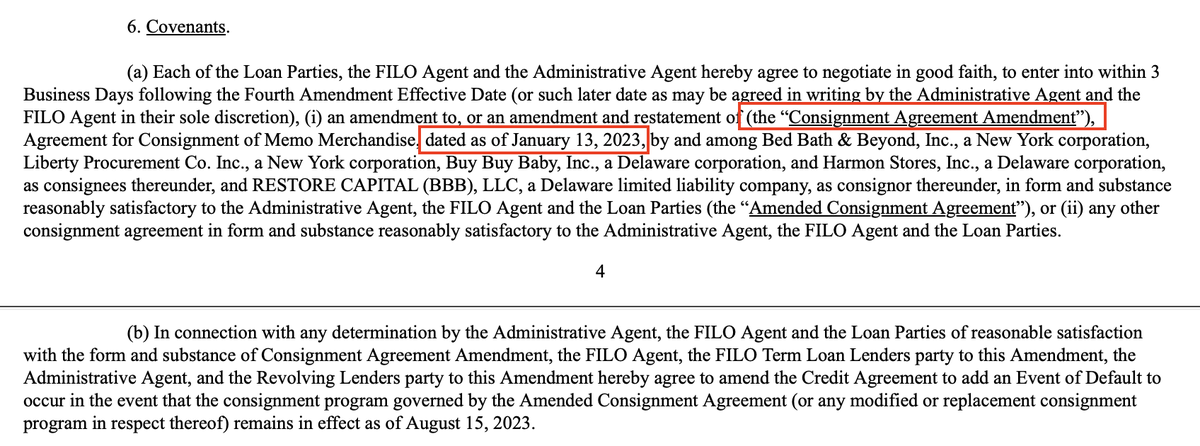

• an April credit agreement amendment will later reveal that additionally, on this same day, a consignment agreement was birthed.

because of the timing and all of these events having occurred on the same day, I speculated that an LBO was nefariously attempted as a reaction to the onboarding of a Consignment Agreement to ensure that the events of default would continue, because the consignment agreement could have corrected the imbalance on the ABL and eliminated the other events of default very quickly.

in other words, the loan contract terms were no longer strong enough to ensure an unfavourable fate for the company and it became apparent there were investors wanting to see it survive. a nefarious LBO attempt (which could not have happened, as I go over throughout the video) would have kept the events of default ongoing despite a surplus of inventory, which was then compounded by the period of cash dominion. the battle for control.

part 6: my thoughts on the January 13, 2023 LBO and its intended (and failed) use to force $BBBYQ into insolvency.

I hope you like it. $BBBY (old).

33

48

300

35,949

part 6: my thoughts on the January 13, 2023 LBO and its intended (and failed) use to force $BBBYQ into insolvency.

I hope you like it. $BBBY (old).

here is the $BBBYQ IRC § 368(a)(1)(G) Type G Reorganization with working video and slides. it will be much better to follow along with visuals.

I think we've solved the puzzle (again). remember, can only use the full NOL if the NewCo issues shares as a substantial portion (or all) payment for the acquired asset.

69

114

594

147,991

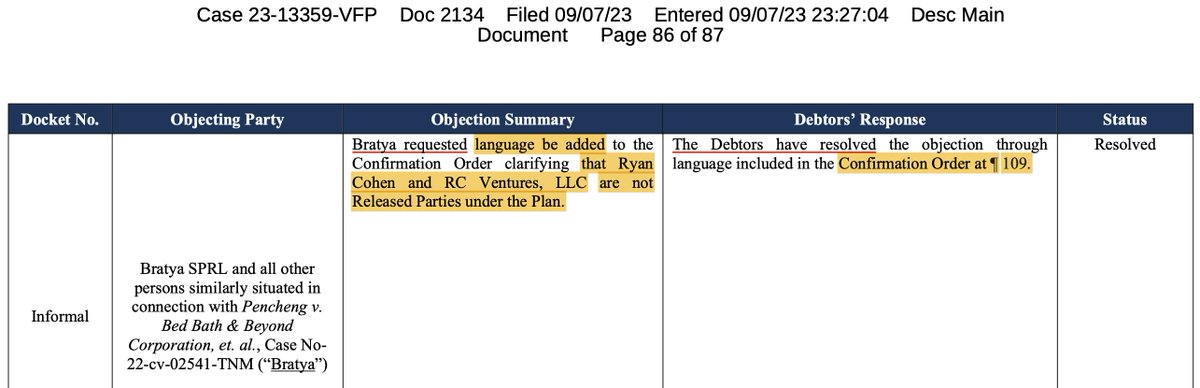

building on the SOFA financial disclosure listing RC as a co-debtor for $BBBYQ, I want to remind everyone of some other anomalies surrounding him throughout the Chapter 11.

Bratya became the lead plaintiff of his class action over the moon emoji. often forgotten is that on the same day that the voting had ended the Plan, they attempted to enter the case and made a legal request to be apprised of any and all information that could include a transaction between any party in interest.

from docket 2114:

to the attentive reader, that should seem very odd. they are in a lawsuit against one individual—who sold his shares!—and yet they want a ton of information about the inner workings of the old $BBBY involving anyone.

why? what possible reasoning could they have to justify any and all details about any transaction, if their only interest is litigating RC?

isn't that a great question! it makes no sense unless through the discovery process of their case against RC, they uncovered information that would have suggested he is involved with the Reorganization through an affiliate or proxy.

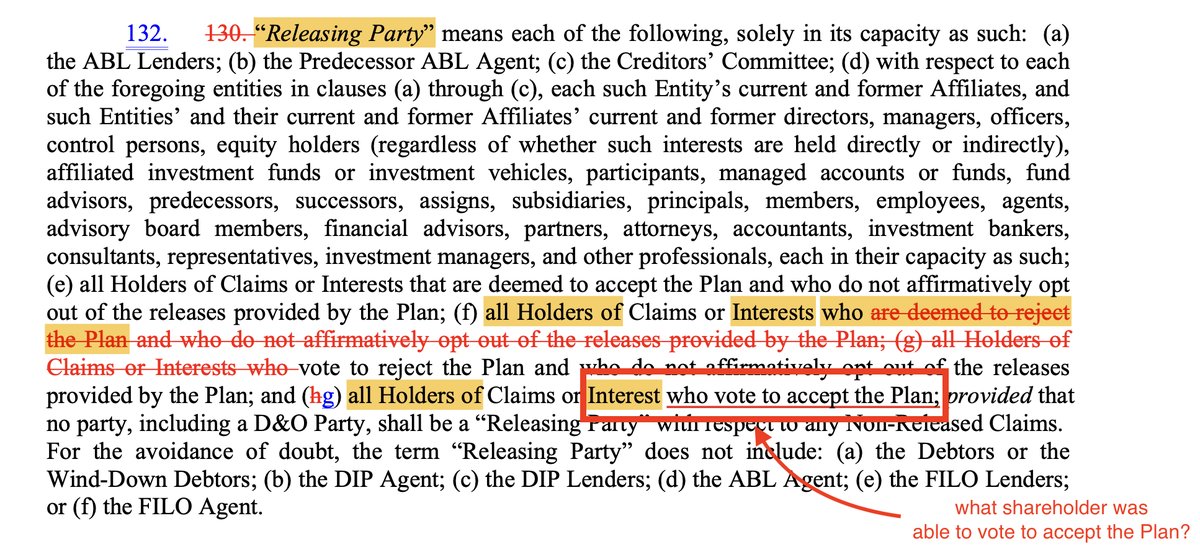

then it would make perfect sense. after some negotiations, we see that there was a compromise reached. the details of any transactions were not shared, but to prevent impairing Bratya from their class action, Ryan Cohen was explicitly identified in the Plan as not being a Released or Exculpated Party.

this would allow Bratya to continue their class action litigation and so they had no reasonable explanation for why they would need any other details, especially involving any party in interest.

—

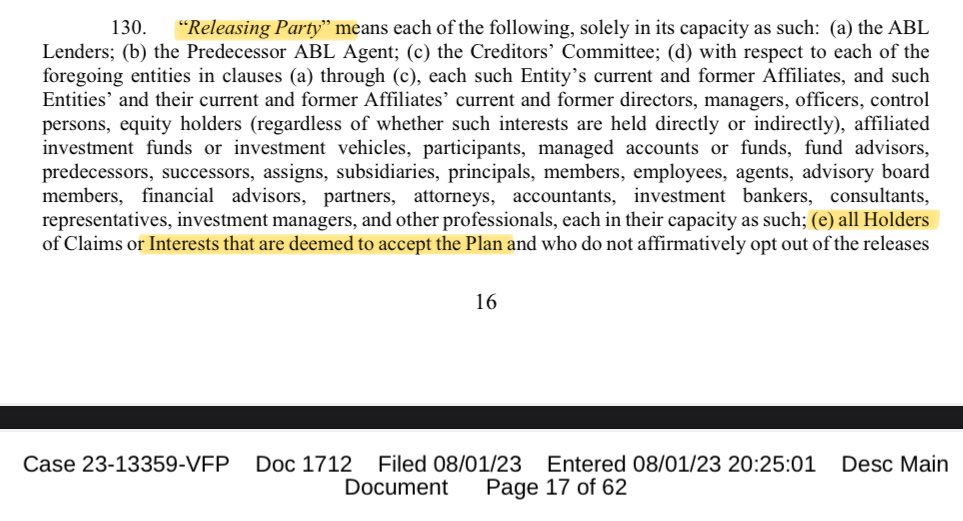

if you have been following, this is an important distinction. as the Holder of Interests within the third-party release, he is a Releasing Party. very important difference!

—

I will say it again because it is very important to understand: Ryan Cohen was explicitly identified in the Plan as not being a Released or Exculpated Party.

here is where things get really interesting. let's establish a timeline:

• on September 1, Bratya wants information involving any party in interest;

but then..

• on September 7, the Kirkland attorneys admit that the Bratya request had escalated to a potential objection to Confirmation of the Plan and as we just explained;

• this was publicly by stating that RC is not a Released or Exculpated Party.

but look what else happened before the Confirmation hearing for the Plan:

within a few days of the attorneys stating that they resolved the Bratya issue, the Plan is refiled with the court as amended and includes a plethora of edits to the definitions section, the releases, as well as the injunction and exculpation provisions.

none of these modifications existed during the voting period. all of these changes came only after satisyfing Bratya to not object to Confirmation by stating that RC will not be a Released or Exculpated Party. the significance of the timing of these changes cannot be understated.

what other reason could there be to have to amend definitions, releases and exculpations at the last minute, that had just excluded only ONE specific individual?

Bratya found through discovery exactly what $BBBYQ holders have always believed.

"in hindsight, it will all be so obvious."

if you are curious for more reading, here are a few posts I made in 2024 and early 2025 going over all of the changes in detail:

x.com/jake2b/status/19042130…

x.com/jake2b/status/19045490…

x.com/jake2b/status/18219810…

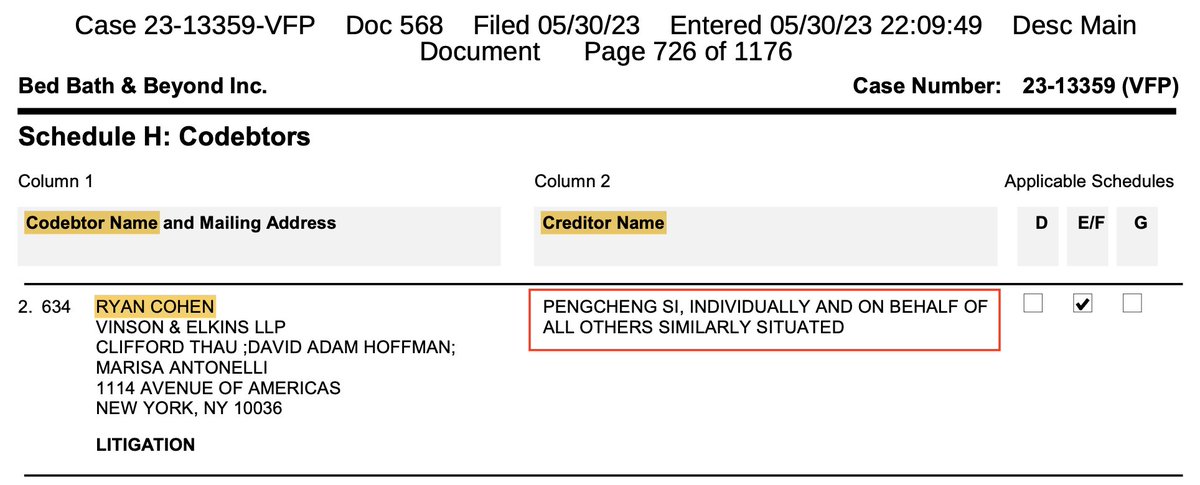

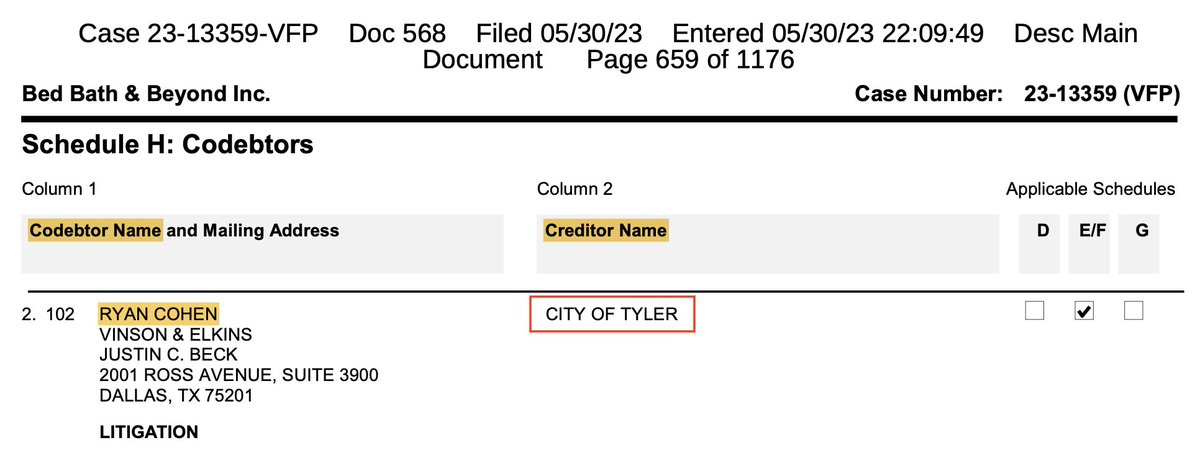

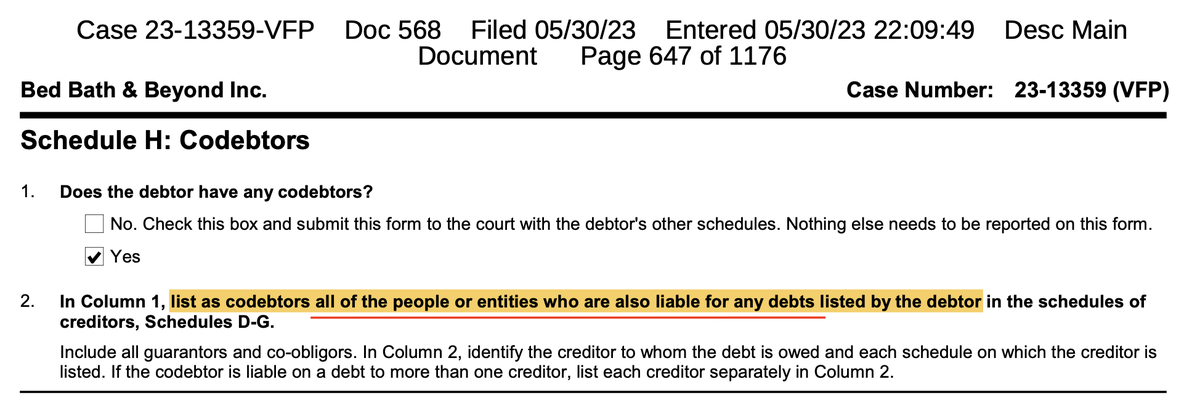

one thing I didn't get to spend much time discussing on the Space call was the $BBBYQ Statement of Financial Affairs and it disclosing RC's co-debtor status.

first I want to establish the importance and legitimacy of this disclosure. the Statement of Financial Affairs (SOFA) is a document that must be filed with a Chapter 11 and has to be accurate; it is considered perjury to lie. the point of it is to give a history of financial transactions and activities leading up to a company's bankruptcy filing:

"The Statement of Financial Affairs is designed to disclose relevant financial information to the bankruptcy court, the trustee, and your creditors. It helps establish an accurate picture of your financial affairs, including your income, expenses, assets, liabilities, and recent financial transactions. The form assists in assessing your eligibility for bankruptcy relief and aids in determining the best course of action for your case."

jdsupra.com/legalnews/unders…

I am trying to emphasize this point because you cannot dismiss the significance of seeing RC listed here and it is not a mistake. do you really think his lawyers would allow for that when he had two ongoing litigations involving the company? that is ridiculous. it is also not "because he is being sued", that argument is either repeated because someone was too lazy to look, they don't understand what they are reading or they are intentionally being misleading. it is laughable.

I'll explain how we know:

here we see RC listed opposite the plaintiff of his class action suit before the lead was changed to Bratya. it is listed.

here is why you cannot dismiss finding RC in the sofa:

because here we see RC listed again, separate of the class action and 16(b) lawsuits. unless you believe that a municipality where there used to be a $BBBY and Baby store location is involved in the litigations against RC, this is what is referred to as a "slam-dunk find."

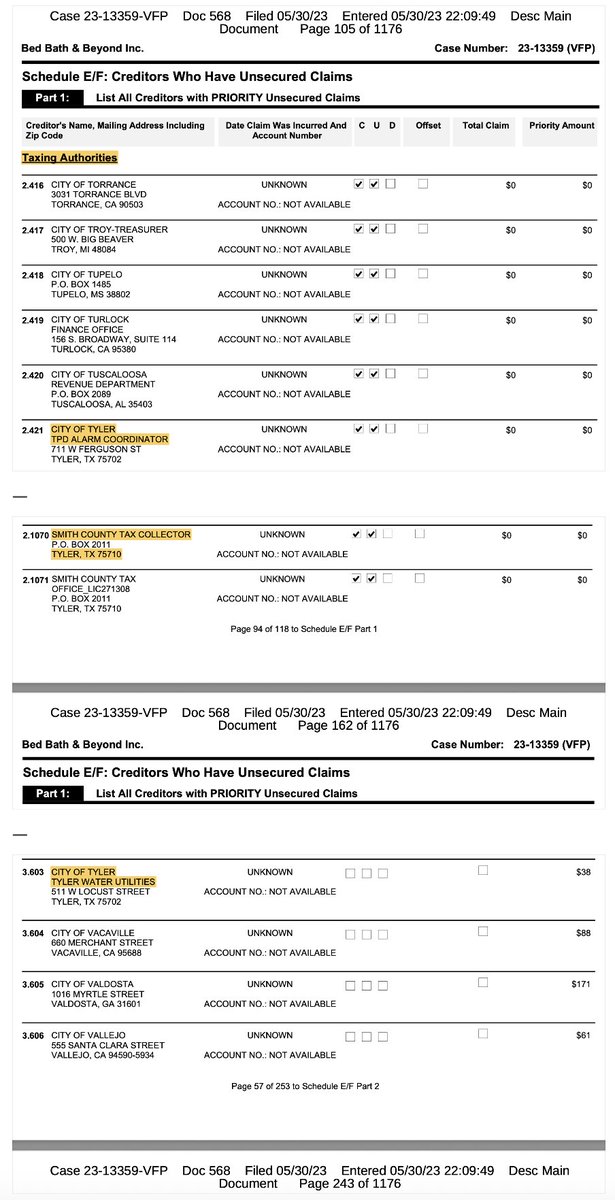

the previous comment was obviously a joke but in case you really did believe (or someone has claimed) that Tyler, TX and several other municipalities are involved in the lawsuits, further in the sofa we will see the city of Tyler disclose to the court exactly why they are in the creditor list:

to no one's surprise, they are a taxing authority. do you remember the Texas Taxes and the Comptroller, for who the Plan reserved the right to pursue a third-party for taxes owed by the OldCo? who would agree to that? only an acquirer.

RC is listed in the full financial disclosure presented to the US Court that he is a co-debtor of the Old $BBBY company, opposite of a municipality claiming they are owed for county taxes and water utility bills.

do you really think that RC's attorneys would allow a "mistake" of this magnitude to exist, when he is being litigated relating to the same business? do you think the signatory for the Statement of Financial Affairs, would make the "mistake" of falsely attributing company debts to a third party, under penalty of perjury? of course not. that would be laughable.

make no mistake, that is exactly what this says. RC is a co-debtor for the OldCo and a co-debtor is a person other than who is filing for bankruptcy, who is also legally responsible for paying the debts. there is no alternative interpretation. and you don't have to believe me, it is written at the top of the sofa itself:

liable for debt nearly a year after he sold his shares. RC had a chip on his shoulder seeing how the former board treated him and his ideas for transforming the company. he could not turn away from the destruction of shareholder value resulting from the "October 2020 plan" and he held everyone to account as the Holder of Interests through the third-party release.

look at the information filed with the US Court and decide for yourself. the facts are right there in front of you and they do not care how difficult it is for anyone "to get there" with their own opinion to believe them.

33

83

485

71,107

anyone who thought they “dunked” on $BBBYQ or $BBBY because of this post should do themselves a favour and take a literacy test.

yet at the same time it was a marvellous display of true colours. so much emotional bias was revealed by so many, over something they have no vested interest in; they just wish to see others lose. a pathetic and shameful display of poor character and lack of class.

reminds me of RC’s television interview where he described his distaste for vitriol towards being invested in GameStop for no reason.

92

77

739

70,876

I love this discussion about $GME. blows my mind that this pro-level discourse is happening on X, for free, for anyone who is curious to see. incredible.

@michaeljburry I was happy to read that you made the connection between operational shorting and the use of creation and redemption privileges within ETF units.

I completely understand your explanation about shares sold short, short volume and market maker liquidity creation and I hope that I can ask a question to further pick your brain: what are your thoughts that this is merely the surface layer of a deeper problem? while I understand your explanation of a “phantom share” and the short-term nature of this dynamic as you describe it, what do you think about the repetitive and ongoing misuse of Reg SHO exemptions that allow the creation of persistent fail to delivers, *particularly* among ETF assets?

publicly-released data often shows outlier quantity of ETF fails on the *exact day* that an underlying equity would face forced delivery pursuant to Reg SHO Rule 204. do you find that curious?

of particular interest, with the popularization of single-equity leveraged ETFs marketed as leveraged exposure, there have been countless examples of outlier failure to deliver on the first trading day of these instruments, or again at deadlines to meet obligations on fails of the underlying common equity. worse yet, you can follow the data to daisy-chain and connect juggling of these obligations from one ETF to another, on the exact day of forced buy-in. some ETF products compound this situation by offering unlimited creation rights to their authorized participants, allowing for near-limitless access to an underlying security without raising the cost-to-borrow and reducing real demand on the open market. could you share your thoughts on this?

I and many others have observed this across many equities and I am not suggesting that this is an isolated issue targeted at $GME, having seen large FTD spikes on ETF vehicles for $MSTR, $TSLA, $NVDA, $CRWV, etc. it is as you say across many stocks and I wonder if you would agree that this is endemic within ETF products?

further, combined with the nature of continuous net settlement, I and many believe that this allows for the even-further deferral of delivery obligations which naturally, in a fair and efficient market, fundamentally impacts supply and demand and therefore price discovery.

I find it fascinating that many of the recent short squeezes like $SMCI, $CVNA, $MSTR will begin during pre-market hours, which happens to overlap with the CNS position report before the day cycle (T 1) begins, after the previous eve’s night cycle has batched orders. I can’t help but be intrigued if this is not attributable to lack of liquidity in premarket, nor dismissed as a coincidence?

I further question if this creates the potential for an environment with alignment of interests between authorized participants and issuers of these ETFs that would be in contrast with price discovery.

please accept my gratitude for sharing your professional, qualified perspective for everyone’s benefit and the time you take to provide explanations on market making and operational shorting specifically. I think this discussion is very valuable but went off-track when the subject of “legality” was brought up. at this point any serious retail investor should understand that the system exists by design with many shortfalls in the law such as “like-kind” and “reasonable expectations, prior to the entry of a short sale order, that sufficient securities will be available..” to ensure there is enough grey area to prevent “blatantly illegal” practices, at least most of the time.

I hope you can find the time to share your thoughts.

28

68

486

31,300

one thing I didn't get to spend much time discussing on the Space call was the $BBBYQ Statement of Financial Affairs and it disclosing RC's co-debtor status.

first I want to establish the importance and legitimacy of this disclosure. the Statement of Financial Affairs (SOFA) is a document that must be filed with a Chapter 11 and has to be accurate; it is considered perjury to lie. the point of it is to give a history of financial transactions and activities leading up to a company's bankruptcy filing:

"The Statement of Financial Affairs is designed to disclose relevant financial information to the bankruptcy court, the trustee, and your creditors. It helps establish an accurate picture of your financial affairs, including your income, expenses, assets, liabilities, and recent financial transactions. The form assists in assessing your eligibility for bankruptcy relief and aids in determining the best course of action for your case."

jdsupra.com/legalnews/unders…

I am trying to emphasize this point because you cannot dismiss the significance of seeing RC listed here and it is not a mistake. do you really think his lawyers would allow for that when he had two ongoing litigations involving the company? that is ridiculous. it is also not "because he is being sued", that argument is either repeated because someone was too lazy to look, they don't understand what they are reading or they are intentionally being misleading. it is laughable.

I'll explain how we know:

here we see RC listed opposite the plaintiff of his class action suit before the lead was changed to Bratya. it is listed.

here is why you cannot dismiss finding RC in the sofa:

because here we see RC listed again, separate of the class action and 16(b) lawsuits. unless you believe that a municipality where there used to be a $BBBY and Baby store location is involved in the litigations against RC, this is what is referred to as a "slam-dunk find."

the previous comment was obviously a joke but in case you really did believe (or someone has claimed) that Tyler, TX and several other municipalities are involved in the lawsuits, further in the sofa we will see the city of Tyler disclose to the court exactly why they are in the creditor list:

to no one's surprise, they are a taxing authority. do you remember the Texas Taxes and the Comptroller, for who the Plan reserved the right to pursue a third-party for taxes owed by the OldCo? who would agree to that? only an acquirer.

RC is listed in the full financial disclosure presented to the US Court that he is a co-debtor of the Old $BBBY company, opposite of a municipality claiming they are owed for county taxes and water utility bills.

do you really think that RC's attorneys would allow a "mistake" of this magnitude to exist, when he is being litigated relating to the same business? do you think the signatory for the Statement of Financial Affairs, would make the "mistake" of falsely attributing company debts to a third party, under penalty of perjury? of course not. that would be laughable.

make no mistake, that is exactly what this says. RC is a co-debtor for the OldCo and a co-debtor is a person other than who is filing for bankruptcy, who is also legally responsible for paying the debts. there is no alternative interpretation. and you don't have to believe me, it is written at the top of the sofa itself:

liable for debt nearly a year after he sold his shares. RC had a chip on his shoulder seeing how the former board treated him and his ideas for transforming the company. he could not turn away from the destruction of shareholder value resulting from the "October 2020 plan" and he held everyone to account as the Holder of Interests through the third-party release.

look at the information filed with the US Court and decide for yourself. the facts are right there in front of you and they do not care how difficult it is for anyone "to get there" with their own opinion to believe them.

63

94

590

94,244

I want to say that I enjoyed the discourse with @AustinTobitt last night. if I am being completely honest, I enjoyed the intellectual challenge that he brought to the table and appreciated that he took the time to prepare. personally, I really liked that he pushed back on certain points and challenged my thesis where he did. I wish he did it more.

I have always been very clear that if you have a good argument, it should be able to withstand being challenged. there can only be a net benefit that comes from exploring weaknesses of a thesis: you either become aware of perspective you may have missed, which allows you to expand or evolve your thinking, or naturally through conversation you discover additional ways to strengthen your thesis.

there is no way I will ever be able to catch up with all of the notifications I see today but let me be clear: it would have served no benefit to any listener if ATO had simply been acquiescent during the conversation. there is no benefit to an echo chamber.

over the last few days I have noticed a question that keeps popping up: “why would you waste your time explaining this to someone coming in at the 11th hour?” and I think while I understand where that question is rooted, I personally welcome discussing what I believe in at any time, as long as the person wanting to discuss does not want to be deceptive or otherwise manipulative. if I can learn something, I don’t care when it comes up; I want to know!

another thing I want to highlight from the quote of the last paragraph is the protective nature within the $BBBYQ investor community. I realized something very powerful from a conversation I had with @IanCarrollShow a long time ago: one of the best, if not the best thing about the $BBBYQ and $GME retail investor communities is the immune system that develops over time. I believe what he meant by that is because of how negatively the retail investor is perceived by the media, by the regulators and institutional investors at large, there is a sense of protection over the common interest. I absolutely loved that and I will never forget him saying it.

to a large extent, I think this showed its head in what I will call “whispergate”. I think it was funny but I also don't think it should have been any more than a laugh. I don't know what @AustinTobitt intentions were but I also don't think it needs to matter. I have always been consistent that I don't care for much more than the accuracy of the information I am sharing. I always invite feedback to my thoughts that are positive *and* negative, as long as they are in good faith and quality; I don't need to care much for who delivers the information as long as it helps evolve or solidify the thesis. I think that's a fair middle ground.

I believe the ridicule directed at @AustinTobitt has gone too far. I respect that he wanted to have the discussion and I think that there was a net benefit that came out of it. if there was someone whispering into his microphone, let’s have a laugh and move on. there is no need to ridicule him to the extent that he has endured.

@AustinTobitt, let me give you some perspective. I know that you have faced a lot of backlash and hostility. if someone whispered into your microphone I love that, that would be really “bullish!” and I really hope you can see the humour in that from a listener’s perspective. I also know that you said there wasn't anyone whispering into your microphone. I personally don't think it added or took away anything from the merit of the argument surrounding the $BBBY thesis so after a chuckle, I really don't care. I am not trying to be rude, I am trying to emphasize that it does not matter. if there was no one in the room with you like you say, let me offer a sincere apology for the behaviour and amount of negativity that has come your way.

with that said, please understand that while this behaviour went too far, the $BBBYQ investor community has endured this type of hostility from $GME “elitists” from the day that Ryan sold his shares in 2022 and is very hyper-protective of the common interest. this is a community that has endured incredible hostility. let me be clear that I am not excusing anyone’s behaviour but I think this was a response of the immune system. there are a lot of kind, good-hearted people in this community but they are battle-worn. imagine the level of ridicule that $GME investors have faced, but then add retail $GME investors too. the most ironic plot twist is that a lot (most?) are $GME investors too. I am sorry for the animosity that has come to you, regardless if your intentions were good or bad. yes, even if your intentions were negative.. that's a real apology.

I participated in the space in good faith because I always enjoy an intellectual challenge, I am always looking for faults in the thesis and I felt that it would be a valuable catch-up for listeners. I appreciated your tenacity as a refreshing discussion. I was intentional in dumping a lot of information for a lot of reasons. of course there is no way that you could have absorbed all of it in real time, let alone rebutted. in good faith and in the spirit of always wanting the highest quality information to survive, I would like to leave an open invitation to continue the conversation with you when you've had a chance to digest what was discussed, if you would ever like to; just you and I. I hope you will take me up on it.

let me end this with a difficult truth: if we $BBBYQ investors are correct about the end result, there could be a surge of media attention and spotlight that will follow like you cannot begin to imagine. let's not give the news media reasons to make us look like terrible people to easily blame and further disparage the retail investor. let’s show the power of collaboration and upstanding conduct so that no one can deny the news media and regulators got us wrong.

power to the people.

74

59

592

38,584