Joined August 2008

- Tweets 245

- Following 53

- Followers 325

- Likes 52

2 Photos and videos

The Custodia Bank case against the Federal Reserve may be heading to the highest court in the country.

Justice Neil Gorsuch has granted additional time for Custodia to file a certiorari petition, due July 11.

The core question: does the Fed have unlimited discretion to deny a state-chartered bank a master account?

Custodia, a Wyoming-chartered bank focused on digital assets, applied in 2020. The Fed denied it. A divided 10th Circuit ruled in the Fed's favor. Custodia is now asking the Supreme Court to weigh in.

If the Court takes the case, it could set precedent on whether the Federal Reserve can effectively veto which banks are allowed to participate in the US financial system.

h/t @EleanorTerrett

10

23

156

13,664

Kate Fraher retweeted

May 27

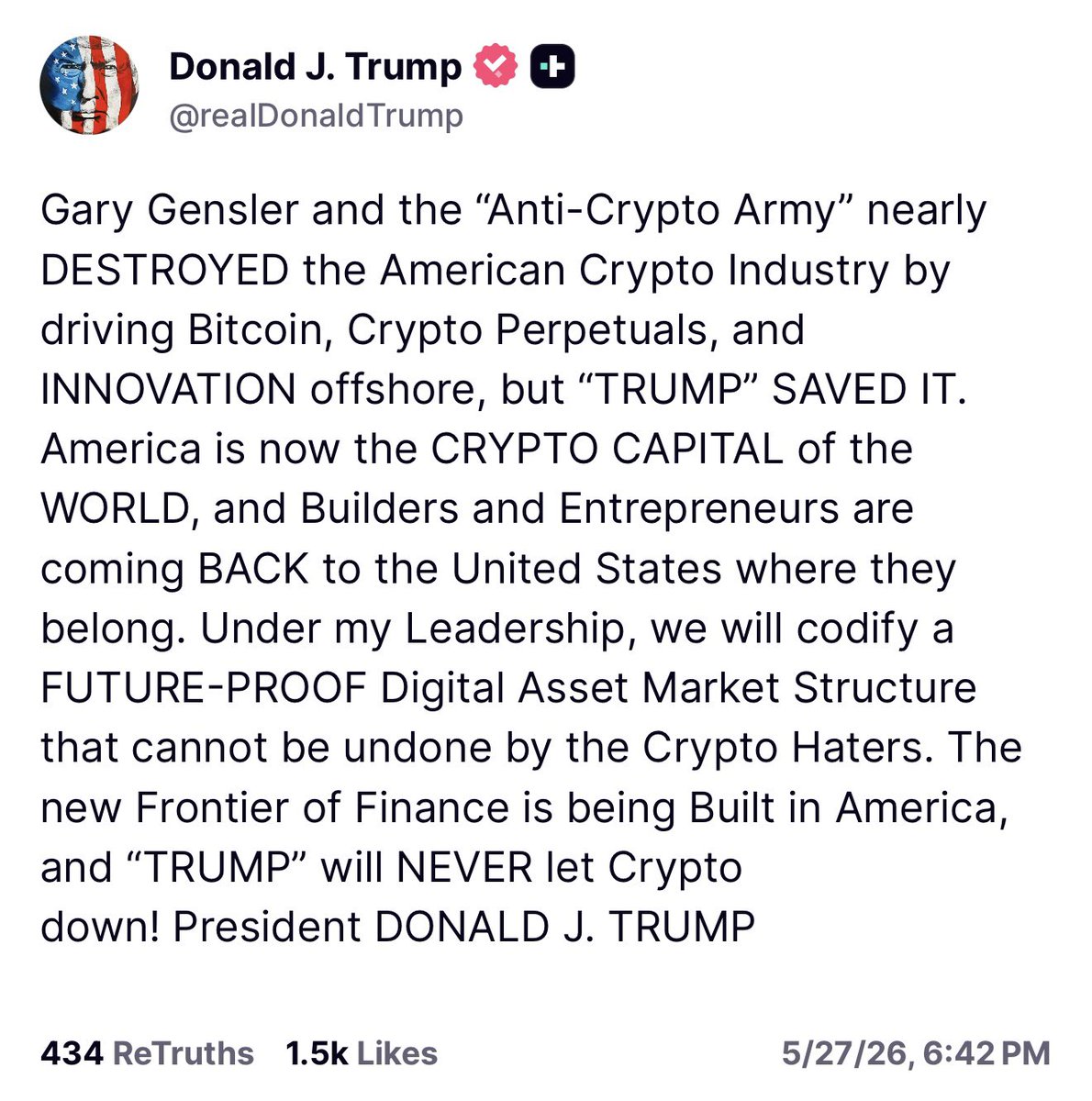

🚨NEW: President Trump says his administration is building a “future-proof” digital asset market structure that can’t be undone by “crypto haters.”

This marks the first time the president has publicly weighed in on crypto market structure since March.

268

886

4,378

682,246

May 27

1/5

My last post was about what the SEC gag rule cost individuals.

This one is about a broader structural question those costs point to:

When a sustained campaign against a financial institution destroys shareholder value without proving a single underlying crime, who is the system actually protecting, and who is it holding accountable?

🧵

3

10

29

10,078

May 27

4/5

Here is the legal asymmetry.

A licensed analyst who sent those same memos to a senator’s office while holding a short position would face mandatory disclosure of that position, compliance review, and a cooling-off period before covering under FINRA Rule 2241 and Reg AC.

An activist short seller operating outside that perimeter faces none of it. No disclosure. No supervisory review. No restriction on timing.

Ironically, Cohodes himself co-authored a 2020 FT op-ed advocating for exactly this kind of reform, a 10-day holding period after distributing market-moving research. He did not apply that standard to Silvergate.

The shareholders who bore the legal costs of the proceedings that followed had no way of knowing that a sustained public campaign against their company, one that ran in parallel throughout, operated under no disclosure obligations whatsoever.

That information asymmetry is not incidental. It is structural.

1

1

10

405

May 27

5/5

No regulator proved that money was laundered through Silvergate. No regulator proved that fraud occurred. No regulator proved that our AML controls failed.

The SEC case was a disclosure theory. Our CFO contested it and did not settle.

Our CAO’s sworn bankruptcy testimony states plainly: Silvergate had stabilized by early 2023, met capital requirements, and could have continued operating. It was two joint statements from the Federal Reserve, FDIC, and OCC that Silvergate’s own CAO cited in sworn bankruptcy testimony as the regulatory signals that made the bank’s business model untenable.

We were a victim of FTX’s fraud. Not a participant in it.

The structural questions this raises go beyond Silvergate. When activist short sellers can lobby regulators privately, without disclosure, while profiting publicly from the response, and shareholders absorb the cost of proceedings that prove nothing, that is a market structure problem worth talking about seriously.

#Banking #FinancialRegulation #ShortSelling #Silvergate #OperationChokepoint #MarketStructure #InvestorProtection

1

14

311

Kate Fraher retweeted

May 25

first American pope drops a banger encyclical on AI on Memorial Day

fitting reminder that “study” and “leisure” are linked, and that both are made possible by sacrifice

🇺🇸 🇺🇸 🇺🇸

1

3

8

306

Kate Fraher retweeted

May 25

The digital asset industry operating in America without a real rulebook isn’t a free market, it’s a liability. America needs the Clarity Act now to ensure America writes the rules

259

575

4,264

122,581

May 21

1/5

**The Freedom to Speak: Reflecting on Risk Management, Regulatory Overreach, and Yesterday's SEC Decision**

Yesterday, the SEC made a historic announcement: it officially rescinded its 50-year-old “gag rule” (Rule 202.5(e)), ending the policy that prohibited settling defendants from publicly denying or criticizing the agency's allegations. As Chairman Paul Atkins noted, “Speech critical of the government is an important part of the American tradition.”

3

15

65

8,297

May 21

4/5

At no point has any regulatory agency proven that our AML controls failed or that wrongdoing went undetected. Instead, a geopolitical narrative took precedence over objective facts.

When the federal government levels its full weight against an individual, the playing field is entirely asymmetric. They possess unlimited resources. For individuals caught in these crosshairs, the choices are severely restricted:

1. Go completely broke trying to fight a multi-year battle in court.

2. "Turn" on individuals or a company you know to be profoundly ethical—even if you have absolutely no dishonest or harmful evidence to give.

3. Settle on a "neither admit nor deny" basis, which historically meant signing away your First Amendment right to defend your reputation.

1

1

26

1,706

May 21

5/5

Faced with these options, and advised by wise counsel that a pound of flesh would be taken regardless, I chose to settle so I could move forward.

But the process itself is designed to apply maximum pressure, and the human costs are real. I was personally de-banked and had credit lines summarily closed—an aggressive tactic used to disrupt daily life and force compliance.

Furthermore, while the SEC will no longer enforce the silence, I still live with the structural consequences of this enforcement action. I bear the burden of a significant financial penalty paid as part of the settlement, alongside ongoing, very real limitations to my professional trajectory and executive options.

The allegations leveled against me were a side story to a larger political agenda. I am incredibly proud of the resilience, integrity, and operational execution our team demonstrated during a true banking crisis. I am glad the right to speak the truth has finally been restored, but we must continue to talk about the long-term professional and personal toll exacted on individuals by regulation through enforcement.

#Banking #RiskManagement #CorporateGovernance #SEC #FirstAmendment #FinTech #Debanking

8

1

40

1,091

May 21

2/5

For the first time since my own settlement, I am free to share my story. While I sincerely applaud the SEC for finally ending this unconstitutional policy, a change in rules doesn't erase the lasting damage of the process.

When FTX collapsed in late 2022, Silvergate Bank experienced a historic deposit run of ~70%. Our risk management and internal controls faced the ultimate stress test—and they held. We successfully navigated that unprecedented crisis, ensuring that no depositor lost a single dollar and no loss was borne by the insurance fund. That execution was a first in modern banking history.

1

10

439

May 21

3/5

The risk of a deposit run is a feature—not a bug—of a fractionalized banking system. Surviving one is proof of robust risk management. In fact, by the beginning of Q1 2023, we had successfully restructured the business with appropriate capital levels and a right-sized workforce to safely operate a smaller, more focused institution.

We did not wind down because of the run or the market volatility. We ultimately chose a responsible, voluntary wind-down because the broader administrative and regulatory pressure levied against the digital asset industry made operating a viable business impossible.

7

352

May 21

4/5

At no point has any regulatory agency proven that our AML controls failed or that wrongdoing went undetected. Instead, a geopolitical narrative took precedence over objective facts.

When the federal government levels its full weight against an individual, the playing field is entirely asymmetric. They possess unlimited resources. For individuals caught in these crosshairs, the choices are severely restricted:

1. Go completely broke trying to fight a multi-year battle in court.

2. "Turn" on individuals or a company you know to be profoundly ethical—even if you have absolutely no dishonest or harmful evidence to give.

3. Settle on a "neither admit nor deny" basis, which historically meant signing away your First Amendment right to defend your reputation.

1

12

523

Kate Fraher retweeted

May 19

CAN’T WAIT for what’s going to start getting revealed as a result of this.

Is @nic_carter gonna have yet more salacious scoops about federal agency wrongdoing, esp during the Gensler/Operation Choke Point 2.0 era??? 🤞🙏🤔

BREAKING: The SEC scrapped a decades-old enforcement policy that prohibited settling parties from denying the agency's allegations against them, saying the policy made it appear as if the SEC was trying to "shield itself from criticism." law360.com/articles/2479123

4

6

53

9,953

Kate Fraher retweeted

May 6

After 17 years, bitcoin is still widely misunderstood.

We partnered with @atlanticrethink to make a short film for the curious ft. @natbrunell, @NSmolenski, and our CEO @josephkelly. Not the crypto story. The bitcoin story.

The New Rules of Bitcoin, out today cc @TheAtlantic.

50

189

654

127,726

Kate Fraher retweeted

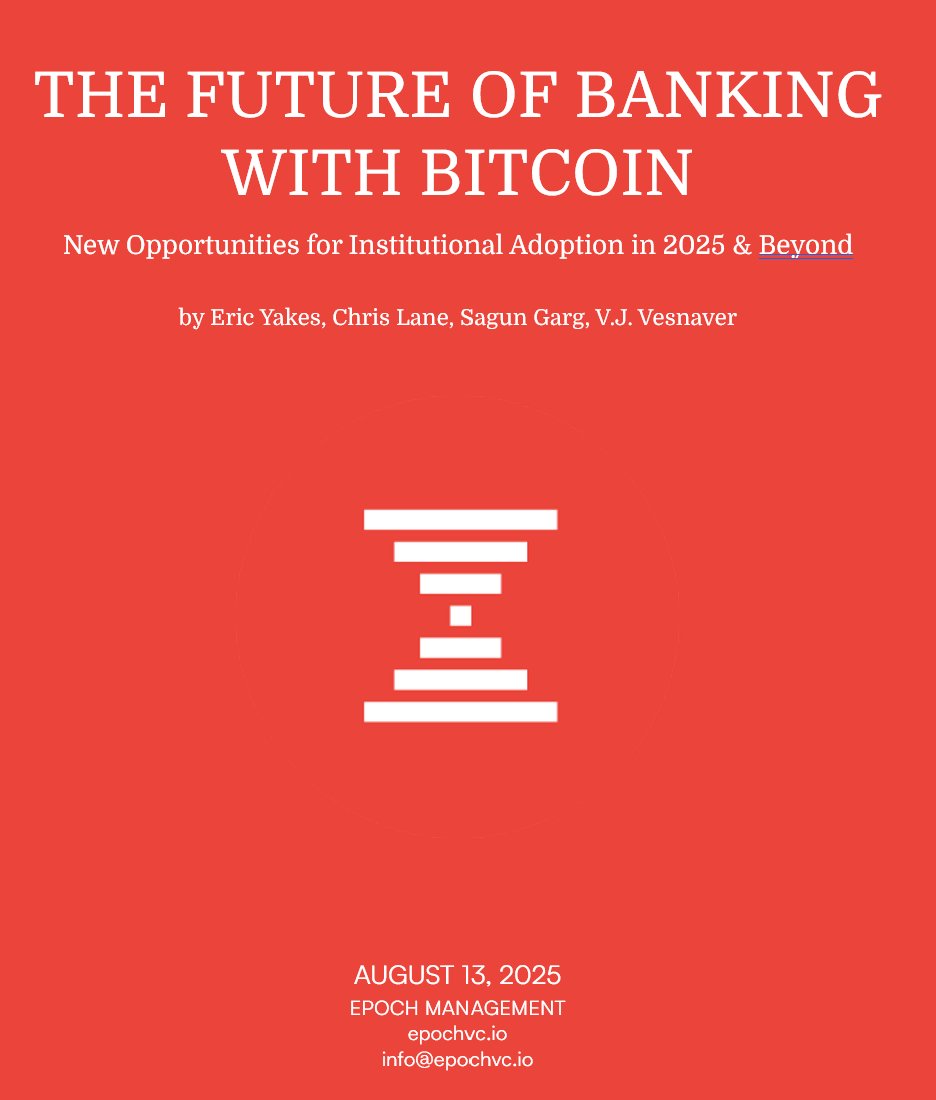

13 Aug 2025

This year everything changed for banks and #bitcoin in the US

@epochvc_ wrote a 100 page report on bitcoin adoption by banks with the former CTO of Silvergate @D_CentralBanker

It is the first comprehensive and technical resource on the topic

Summary and link in comments:

19

98

362

55,373