Fintech and stuff. General Counsel at Hometap. No legal advice here, just idle chit chat based on lots of years in the biz.

Joined February 2011

- Tweets 2,120

- Following 945

- Followers 614

- Likes 8,279

20 Photos and videos

Mar 12

When I worked at the CT DOB, one of the oddities of CT law is that the DOB also has jurisdiction over rental security deposits.

There weren’t many cases, but 100% of those cases that did exist involved small, not at all “corporate” landlords. Small owners were worse.

1

4

909

30 Dec 2025

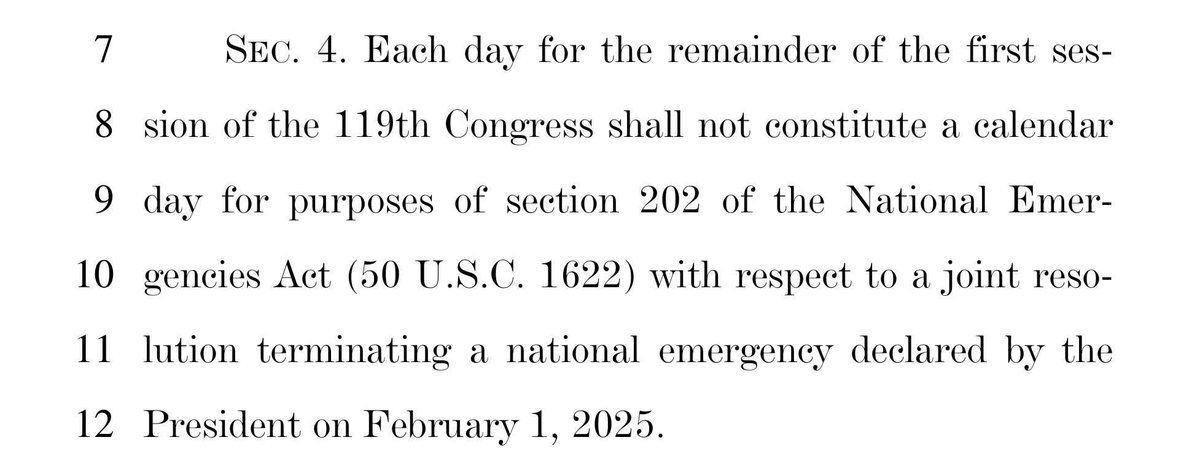

Another chapter in the unions case against the CFPB has been written

District Court ruled that the CFPB’s interpretation (based on the DOJ’s analysis) of the funding mechanism was inaccurate and the CFPB must request funding from the Fed to remain operating

(Decision follows)

2

8

3,361

22 Dec 2025

CFPB issues new advisory opinion on EWA

What a wild ride the regulatory world of EWA has been. Following the issuance of guidance in 2020, a rescission of that guidance in 2025 and then a rescission of the rescission, the CFPB today has re-issued new guidance (in next tweet)

4

7

2,574

22 Dec 2025

The opinion (rather obviously) notes that this is very fact specific and does not preempt state law, nor does it excuse deceptive and unfair practices (what about abusive practices?)

2

125

22 Dec 2025

On first pass, EWA programs that allow employees to access wages that they’ve already earned, and that:

1) are non-recourse;

2) repaid through payroll deduction; and

3) do not charge interest or fees;

Do not constitute “credit”

1

1

146

22 Dec 2025

One of the big demarcation lines seems to be with respect to fees. If the fees are voluntary or optional (like expedited funding fees), then it appears to be EWA. If the fees are mandatory, then it appears to be more like credit.

1

109

19 Dec 2025

Another interesting study from the NY Fed (in next tweet) on the impacts of state usury caps.

And the TLDR is that they’re bad for the poor (available credit contracts without improving delinquencies) and good for the rich (availability of credit expands)

1

4

939

18 Dec 2025

Interesting article on the potential expansion of deposit insurance limits from two very … different … perspectives which, nevertheless, share the same concerns

18 Dec 2025

Why do a progressive academic and conservative banker both think raising deposit insurance limits to $10M is a bad idea? Read what @JillCastilla and I wrote in @barronsonline

barrons.com/articles/higher-…

4

134

17 Dec 2025

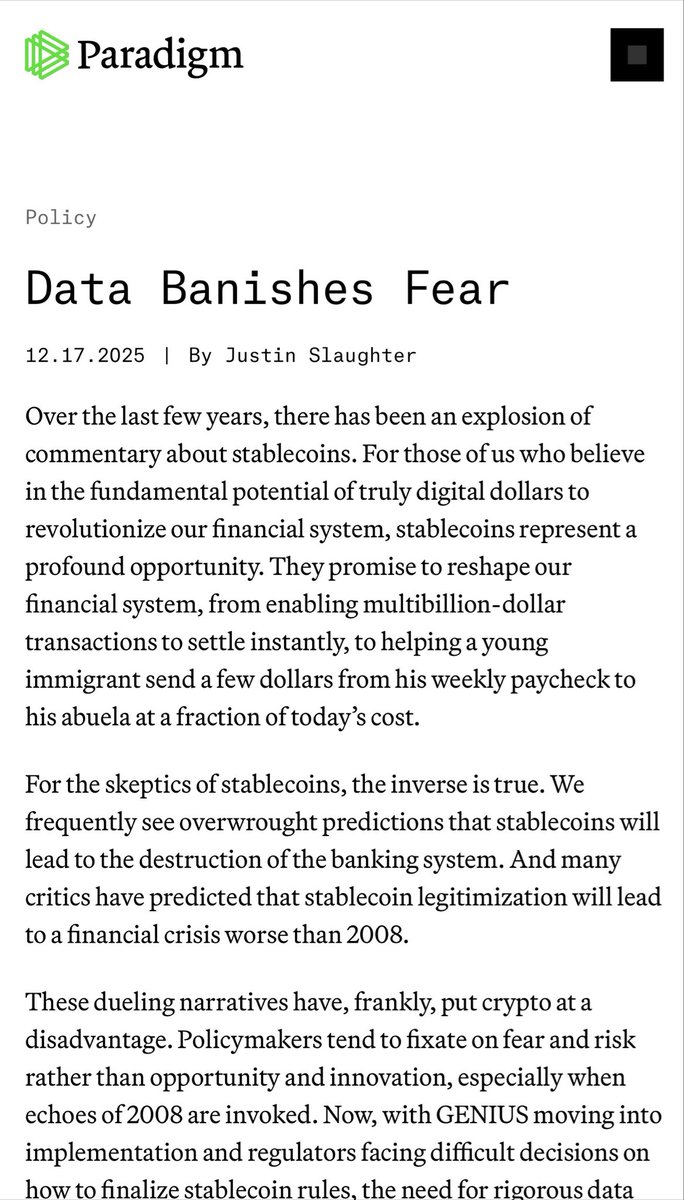

Very interesting look at impact on banks of Stablecoins. Worth a read (or at least this summary)

17 Dec 2025

Merry Christmas, we have a present for all of you: a new paper by Dr. Lin William Cong that models stablecoins’ impact on the banking system.

But to save you a click, here’s the takeaway: stablecoin adoption should be neutral or help credit creation and bank deposits.

1

6

414

Jesse Silverman retweeted

12 Dec 2025

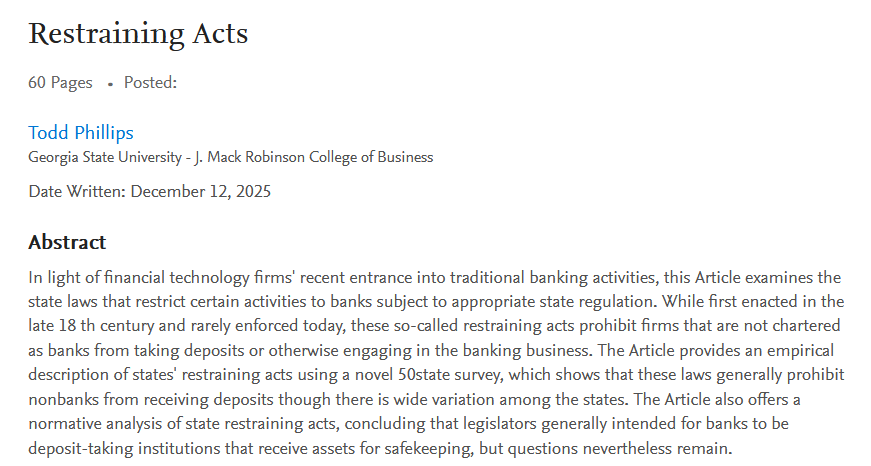

Only read a few sections so far, but this is EXCEPTIONALLY useful to practitioners in the space. And I can’t think of how rarely I’ve said that about a law professor’s paper

Kudos @tphillips

12 Dec 2025

I've uploaded a new article, "Restraining Acts." I examine the laws restricting banking in all 50 states. These laws generally prohibit nonbanks from receiving deposits and show a legislative preference that banks offer safekeeping of customer funds. 1/

1

4

13

3,023

1 Dec 2025

Some of the best insight into public fintechs and more

30 Nov 2025

I have removed the paywall from my newsletter: popularfintech.com/

All write-ups are now available for free.

This year, I have written about: Visa $V, PayPal $PYPL, Klarna $KLAR, Capital One $COF, American Express $AXP, Robinhood $HOOD, Coinbase $COIN, Block $XYZ, Affirm $AFRM, Wise $WISE.L, Adyen $ADYEN, Nubank $NU, Toast $TOST, Marqeta $MQ, Shift4 $FOUR, Fiserv $FI, Shopify $SHOP, Mercado Libre $MELI, Sea $SE, Coupang $CPNG, Circle $CRCL, and Chime $CHYM

p.s. Huge thank you to everyone who subscribed to the premium plan🙏🏻

1

9

3,992

27 Nov 2025

Happy Thanksgiving to all, especially these guys, flaunting their freedom on Thanksgiving morning

6

145

26 Nov 2025

Looks like the CFPB is back in the game …

26 Nov 2025

🚨We are so back!🚨 "Here is something to be thankful for this Thanksgiving: The Federal Reserve System has 𝙧𝙚𝙩𝙪𝙧𝙣𝙚𝙙 𝙩𝙤 𝙥𝙧𝙤𝙛𝙞𝙩𝙖𝙗𝙞𝙡𝙞𝙩𝙮. It appears to be on track for the combined profits [of] over $2 billion in the current quarter." tinyurl.com/2h5em63u @billnelson2x2

2

12

1,775

22 Nov 2025

Fresh off Fintech NerdCon, I’m struck by how many conversations I had about the Colorado DIDMCA decision and its impact on fintech and bank partnerships

The biggest takeaway is that we still don’t know the extent of the impact to those partnerships, but it’s not zero

3

2

16

4,063

22 Nov 2025

On a small policy note, it is fascinating to watch this play out. In many states, consumer credit and banking are under the Department. So this is an internal battle between consumer credit, which wants DIDMCA, and the banking division which doesn’t want to devalue state charters

2

264

22 Nov 2025

Finally, given that the Feds are much more open to granting charters, one has to wonder how many state chartered banks will flip their charters or new, federally chartered, and purpose built fintech partner banks will arise.

2

1

257