Joined September 2025

- Tweets 382

- Following 79

- Followers 230

- Likes 627

32 Photos and videos

Pinned Tweet

May 21

I just started a Substack! You can subscribe to it here tropicalpenguin.substack.com…

4

546

Tropical Penguin retweeted

The Week Ahead will be live tonight at 9:30 EST

cc: @ElBandidokz @owensinvestment

x.com/i/spaces/1OGwbbgepadKB

2

3

352

New substack post (free) on Solaris Energy (SEI) (link follows).

I traded SEI back in Feb when it was in the high 40s and it rallied all the way to the high 70s. I am now jumping back in as I like the chart, management execution, ties to SpaceX xAI (and Anthropic indirectly), Meta, and the company overall evolution from a mere oil & gas company to a power solutions provider.

I believe SEI is still below fair value when you compare management's 2029 projection versus companies in the same space. Perhaps not as cheap as February but still a worthwhile trade in my opnion. Do your own research, not financial advice.

1

5

166

Jun 13

(link follows) New substack post is out (free!). I am continuing my Edge AI trade series. This time, I focused on $AKAM (Akamai Technologies, Inc).

Once thought as a cybersecurity and content delivery network company, Akamai is making a big bet in Edge AI inference compute.

With a distributed compute platform spanning 4,300 edge locations, AKAM is positioning itself to play a prominent role in edge AI inference.

1

4

292

Jun 13

tropicalpenguin.substack.com…

Consider supporting me on substack.

Please do your own due diligence.

120

Jun 12

My broker @Questrade has been down today. I suspect due to increased traffic due to SPCX IPO. I cant place orders on any stock. Thats over 45 min and counting unable to buy or sell stocks. You will be sued.

8

698

Jun 12

I've been long $SEI since March. Sold at the top and entered the trade again last week. Solaris provides behind-the-meter gas turbines power generation for both xAI's Colossus I and II. Keep this in mind with SPCX IPO tomorrow.

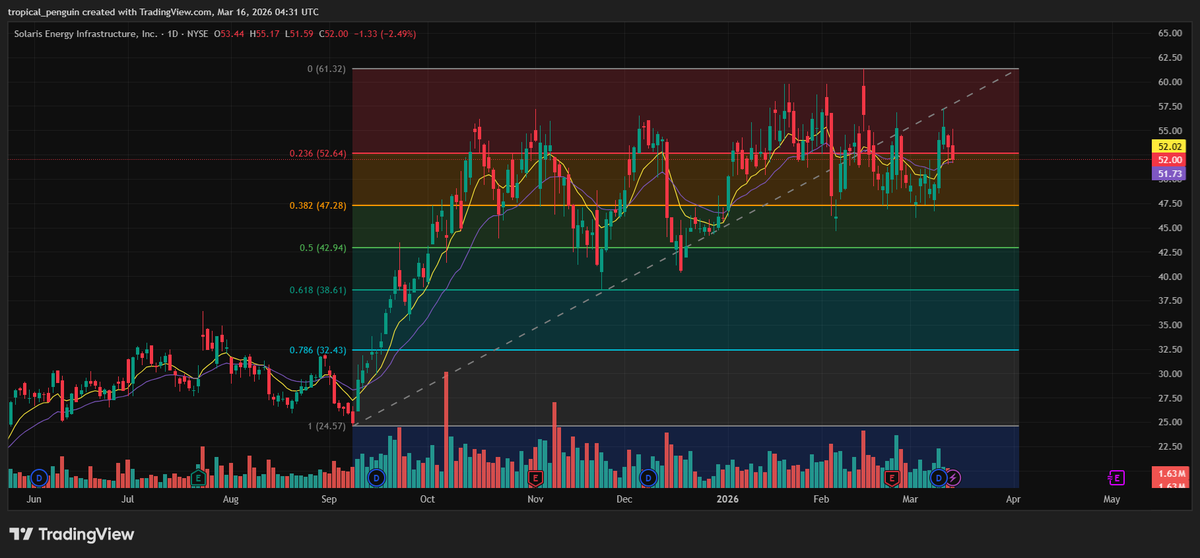

Mar 16

Solaris Energy $SEI has acted extremely well in this chop. This oil & gas company based on Texas is quickly turning into a power-as-a-service (PaaS) company in response to insatiable power demand in the US. When you think of Solaris, think about Uber, but for electricity.

From an operational standpoint, what differentiates Solaris in this space is their HVMVLV acquisition. Solaris is more than a raw source of power, they also have electrical control/distribution expertise. They are able to support complex 1 GW loads with their modular turbines, reciprocating engines, BESS, and redundancy. They have a real competitive edge in rapid deployment and AI load matching versus alternatives.

Management's execution has been flawless, and the acquistion of HVMVLV opens up their TAM to other areas other than DCs. Current fleet at 760MW with a clear plan to deploy 2.2GW by 2028.

In their last quarter, Solaris has met and exceeded expectations. Full-year 2025 revenue rose to $622 million from $313 million in 2024 while adjusted EBITDA increased to $244 million from $103 million. Management also guided to $72–77 million of adjusted EBITDA for Q1 2026 and $76–84 million for Q2 2026, which suggests the growth trend is continuing. On a GAAP basis, the company was also profitable for full-year 2025, with $58.4 million of net income versus $28.9 million in 2024. The only thing that looks ugly at first glance is Q4 GAAP net income, which was negative $3.5 million, but that was distorted by a $41.5 million loss on extinguishment of debt tied to refinancing after the convertible issuance, not by an operating collapse.

There is a lot more to say about Solaris. I really enjoyed their last earnings and their mantra "from molecule to electron". They are transitioning fast from an Oil & Gas equipment company to a power solutions provider in perhaps the hottest theme in 2026. Companies are scrambling to contract power for hyperscalers, SEI is primed to be a huge beneficiary with their PaaS business and strong know-how and execution for quick power deployment.

I own shares, please do your own research.

1

5

748

Jun 10

I want to reiterate how cheap FTAI is right now. PEG of 0.38, fwd P/E of 20. The best part? None of those multiples are factoring in their FTAI Power segment which should kick into full gear as early as Q1 2027. People keep complaining that stocks are overextended. There are still opportunities out there. FTAI is undoubtedly one of them. Stock is up 18.7% YTD. CEO bought shares at $155 in November (~50% since then). FTAI has largely not participated in the most recent rally. Probably due to higher oil prices. Guess what? Higher oil prices is a net benefit for FTAI as airlines look to cut costs by outsourcing the servicing and maintenance of their jet engines to FTAI.

1

1

210

Jun 10

Management said that prototyping and testing is ahead schedule for their first power turbine (Mod-1) . Management estimates that they will wrap things up by Q3, with commercial launch in Q4. This segment alone should add between 40-50% in EBITDA by 2027. They also revealed that their 2027 stock (100 units) are nearly sold out, with a meaningful portion of the 2028 stocks already spoken for.

1

89

Jun 10

The organic EBITDA growth from their power division will sit on top of a very strong growth foundation. Last quarter, FTAI sales was 64% vs Q1 2025. Margins took a hit, but that's because management has decided to pursue market share.

They have a profitable, growing main business and then FTAI Power should add tremendous upside moving forward. This is a real, profitable business, with strong execution. Perhaps not the sexiest name, or the next 4x, but the R/R is pretty strong IMO. Especially in this environment.

Here is my FTAI article, free on substack: tropicalpenguin.substack.com…

Please consider subscribing to my substack and support my work.

106

Jun 8

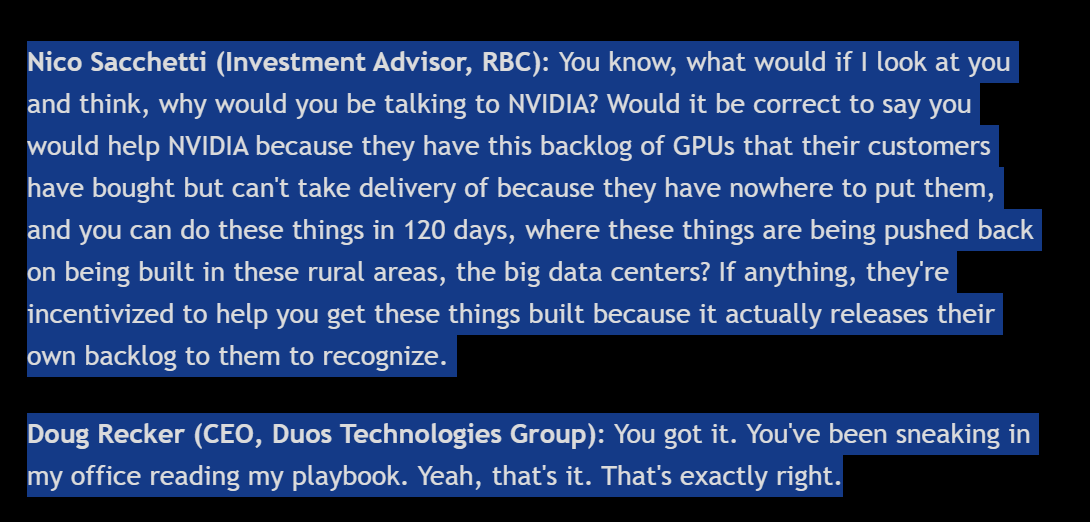

PS. This is my first post of my "Edge AI Trade Series." I will write a detailed post about companies that I believe are poised to benefit materially as Edge AI gets traction over the years. Hope you enjoy!

Jun 8

*NEW* Substack Post is OUT. Open to everyone.

My article is about a stock that I've been following since mid May. The company is Duos Technolgies ($DUOT). I believe this company has what it takes to execute in their vision of bringing Edge Data Centres (EDC) to regional and underserved locations.

I hope you enjoy. Support my work via substack, it helps me to keep going with more research on a regular basis.

Link follows...

3

560

Jun 8

*NEW* Substack Post is OUT. Open to everyone.

My article is about a stock that I've been following since mid May. The company is Duos Technolgies ($DUOT). I believe this company has what it takes to execute in their vision of bringing Edge Data Centres (EDC) to regional and underserved locations.

I hope you enjoy. Support my work via substack, it helps me to keep going with more research on a regular basis.

Link follows...

1

4

1,254

Jun 4

I was very surprised with the price action of IPO $AADX yesterday. Stock closed below pricing on its first day. This is real, tangible company, with a lot of good stuff going for them in the space and defense themes. Last time I checked, it was up almost 22% in the overnight. Expecting a big day tomorrow for AADX. We'll see.

3

604

Jun 4

New substack post just dropped. I wasn't planning in writing one today but I just found this company so compelling that I had to put out there for my subscribers. Link follows...

1

2

433

Jun 3

This is a good stock. Moat, clean balance sheet, CEO is bullish, no dillution in sight, and it is growing. IDN is in a hot thematic (idendity fraud). Can't believe IDN did not participate in this run so far.

$IDN seems too cheap. Here's the pitch:

Intellicheck, Inc (IDN) is an identity verification company. They sell into banks, credit card issuers, fintechs, retailers, government agencies, etc across North America. Their use cases are primarily KYC, AML, fraud, and age verification, with retail and financial services being their biggest markets.

Their core product is barcode validation: you scan the back of a driver's license or state ID, and IDN runs a proprietary analysis of its non-public security features and returns a fraud decision in under a second. They bundle this with OCR, facial recognition, phone verification, and criminal background checks.

IDN's edge here is in their proprietary database of issuing non-public documentation for decades. The company has served as the testing lab for AAMVA's DL/ID Card Verification Program for more than 25 years, a relationship that gives them a deep entrenchment in each state's system.

The company has an extremely clean balance sheet for its size, with zero debt and ~$10M sitting in cash. The company trades at a FWD P/E ratio of 22x with Gross Margins of 91% and net margins of 11%. I see this as a very high-quality business that will not be displaced from here, and this is a financial structure that is very impressive for a sub $100M MC company.

1

5

913

Jun 2

It's interestng to see $CSPH popping off their hermetic package solution for space application. In my opinion, CSPH more interesting angle lies in the 800V systems buildout. Their proprietary MMC can go in HVDC systems which are rapidly becoming a critical element in the AI buildout story. CPS already said that they make baseplates and heat spreaders for power semiconductors such as IGBT modules. IGBT modules as heavy-duty, very fast electrical on/off switches used to control large amounts of electricity inside these HVDC systems.

Apr 26

$CPSH (CPS technologies) is a really interesting micro-cap.

CPS core business is this metal matrix composite material, which combines metals and ceramics, most notably aluminum silicon carbide to make AlSiC. You can say AlSiC is a “better engineered metal” built for situations where ordinary aluminum or copper would struggle. Amongst the many interesting applications, the one that I find more interesting is the use of MMC in HVDC systems which are rapidly becoming a critical element in the AI buildout story. CPS already said that they make baseplates and heat spreaders for power semiconductors such as IGBT modules. IGBT modules as heavy-duty, very fast electrical on/off switches used to control large amounts of electricity inside these HVDC systems. AlSiC is also used in other interesting applications such as fiber-optic internet equipment, routers, switches, and other high-power electronic systems.

CPS also has another interesting segment in hermetic packages which functions as a sealed protective housing for sensitive electronics. These packages are used in things like avionics, satellites, GPS systems, undersea systems, telecommunications equipment, and advanced electronics.

This company is sitting in so many interesting intersections, the optionality is plenty.

5

951

Jun 2

🤨

Jun 2

This article is now FREE on my substack.

I believe there is a strong possibility that Constellium SE ($CSTM) is supplying low density Al-Li sheet and plate to SpaceX.

Constellium A&T segment (space related) is the growing engine of this business, with gross margins at 17% while other segments are in the single digits. CSTM already disclosed that they ship this highly specialized aluminum alloy to Blue Origin, Nasa, Boeing and Lockheed Martin.

The evidence that SpaceX is also a customer is quite strong. Constellium has been mentioned by name in articles about SpaceX's Falcon back in 2010 (then Alcan) and 2019. In a recebt SpaceX’s Falcon Payload User’s Guide, dated May 9, 2025, the description of the material used in Falcon's propellant tank walls is essentially a description of Constellium aluminum-lithium alloy Airware.

The best part? CSTM is not commanding a premium in the market as of now. They still trade at lower multiples than competitors like KALU, ATI, HWM, CRS. In part because of CSTM more cyclical business. However, CSTM is deeply involved in the space-economy aluminum-lithium (Al-Li) alloys used in rocket tank walls, domes, barrel panels, intertanks, thrust structures, crew modules, and others. As far as I know, there are only a handful of credible Western suppliers, with only two visible industrial-scale names that I found.

2

303

Jun 2

This article is now FREE on my substack.

I believe there is a strong possibility that Constellium SE ($CSTM) is supplying low density Al-Li sheet and plate to SpaceX.

Constellium A&T segment (space related) is the growing engine of this business, with gross margins at 17% while other segments are in the single digits. CSTM already disclosed that they ship this highly specialized aluminum alloy to Blue Origin, Nasa, Boeing and Lockheed Martin.

The evidence that SpaceX is also a customer is quite strong. Constellium has been mentioned by name in articles about SpaceX's Falcon back in 2010 (then Alcan) and 2019. In a recebt SpaceX’s Falcon Payload User’s Guide, dated May 9, 2025, the description of the material used in Falcon's propellant tank walls is essentially a description of Constellium aluminum-lithium alloy Airware.

The best part? CSTM is not commanding a premium in the market as of now. They still trade at lower multiples than competitors like KALU, ATI, HWM, CRS. In part because of CSTM more cyclical business. However, CSTM is deeply involved in the space-economy aluminum-lithium (Al-Li) alloys used in rocket tank walls, domes, barrel panels, intertanks, thrust structures, crew modules, and others. As far as I know, there are only a handful of credible Western suppliers, with only two visible industrial-scale names that I found.

1

1

582