AI is infrastructure, not software. Writing about power, chips, and the physical systems that decide the outcome. SVP Autonomy and Energy at Scania. Ex-Google

Joined April 2009

- Tweets 787

- Following 338

- Followers 302

- Likes 22

37 Photos and videos

US utilities asked for 9.4 billion dollars in rate hikes in just Q1. The AI buildout has walked out of the data center and onto your power bill. And the industry is funding studies to tell you it wasn't them. The physical economy always sends the invoice.

14

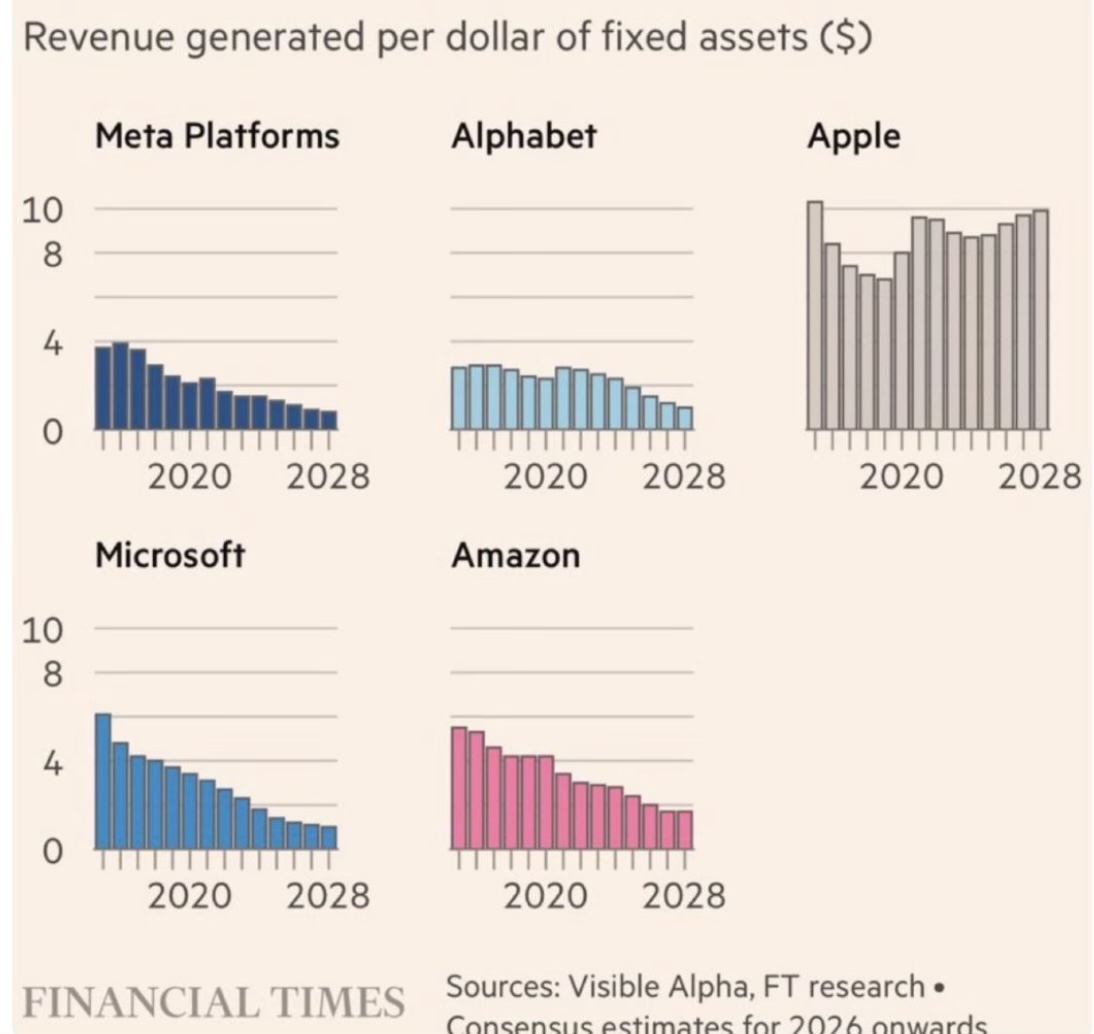

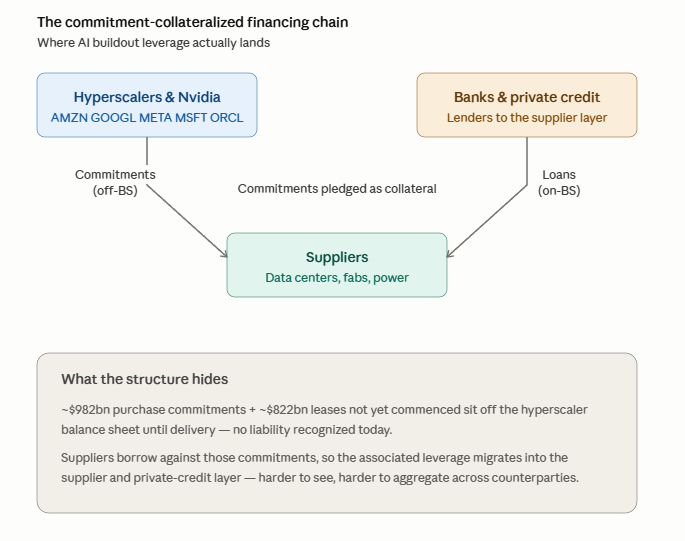

Everyone reads $1.8TN as financial leverage. It is not. Purchase and lease commitments are contracted power, land and buildings, and you cannot unsign a PPA or a 15 year lease when demand softens. The concrete is poured before the revenue shows up.

Jun 13

Where the hidden AI liabilities are:

$1.8TN in off balance sheet operating leverage ($1TN in purchase commitments and $0.8TN in lease commitments): obligations hidden in space

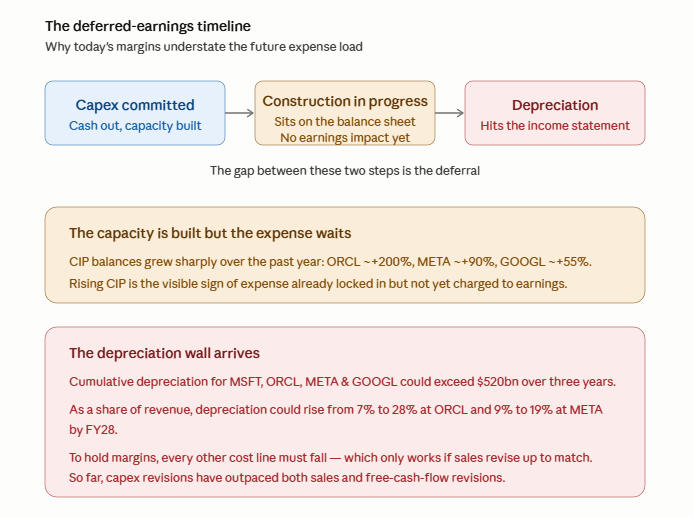

$520BN in deferred earnings masking earnings hit from spending happening now: costs hidden in time

1

15

Jun 13

There is 2,060 GW of power waiting to connect to the US grid right now. That is about twice the entire installed US fleet. The AI power problem was never about building generation. It is about the queue to plug it in.

2

1

40

Jun 13

Here is the part nobody posts. Solar in the queue fell 12%. Storage fell 13%. Wind fell 26%. The only category growing is natural gas, up 72% to 136 GW. When firm power is the real constraint, the market quietly votes gas.

1

35

Jun 13

Everyone is announcing gigawatts. Almost nobody can connect them this decade. The scarce asset is not a turbine or a chip. It is an interconnection slot. Watch who already holds one.

22

Jun 13

Everyone hears "AI will redefine automation" and pictures smarter robots, but intelligence was never the bottleneck. A plant floor runs on PLCs and safety logic certified over years, and you cannot ship a model into steel that doesn't take software updates.

30

Jonas Hernlund retweeted

Jun 11

Honeywell's $HON CEO just said:

“The power of AI is going to redefine automation”

13

17

192

21,294

Jun 12

Order a heavy gas turbine today, it arrives in 2030. Three companies build 75% of them and all three are sold out. GE Vernova's slot reservations jumped 43 to 56 GW in one quarter. The AI power crunch was never chips. It's the thing that spins.

23

Jun 12

Goldman now models AI capex at 7.6 trillion dollars through 2031, across compute, data centers and power.

The part worth sitting with is that the power line item is growing faster than the chip line item. This stopped being a software story a while ago. It is a physical buildout, and buildouts are won by whoever controls the scarce input, which right now is electrons and the steel to move them.

32

Jun 12

The Marshall Plan cleared fast because capital was the bottleneck. This buildout isn't capital-constrained at all, and you cannot wire $650B into transformer lead times or interconnection queues that already run years. The number is the easy part.

Tech companies will spend $650B on AI data centers in 2026 alone. For context: the entire Marshall Plan — which rebuilt postwar Europe across multiple nations and years — cost roughly $160B in today's dollars. We are funding civilization-level infrastructure at 4x Marshall Plan scale. Not over decades. Per year.

24

Jun 11

Everyone sizes the AI buildout in GPUs, but a cluster is dead silicon without the optics linking the racks, and those transceivers run on a compound China gates at the export desk. You can scale compute with money, you cannot buy your way past an export license.

Jun 11

U.S. officials are reportedly pressing China over delays in indium phosphide export approvals, as the material becomes a bottleneck for AI data center buildouts.

Reuters says Coherent CEO Jim Anderson raised the issue during a U.S. business delegation trip to China in May, and it was also discussed in U.S.-China trade talks in Seoul.

FWIW: InP is critical for photonic chips used in high-speed AI infrastructure.

AXT $AXTI says InP export permits are its biggest current challenge.

Coherent $COHR warned of an InP shortage in May.

Lumentum $LITE is reportedly sold out through 2028 despite quadrupling output.

6-inch InP wafer prices are up 250% to around $5,000.

82

Jun 11

Unitree shipped 5,500 humanoid robots in 2025. Tesla Figure Agility shipped 150 each, ~450 combined.

One Chinese company outshipped the entire US trio 12x.

70% of Unitree went to universities. Volume still builds the cost curve.

51

Jun 11

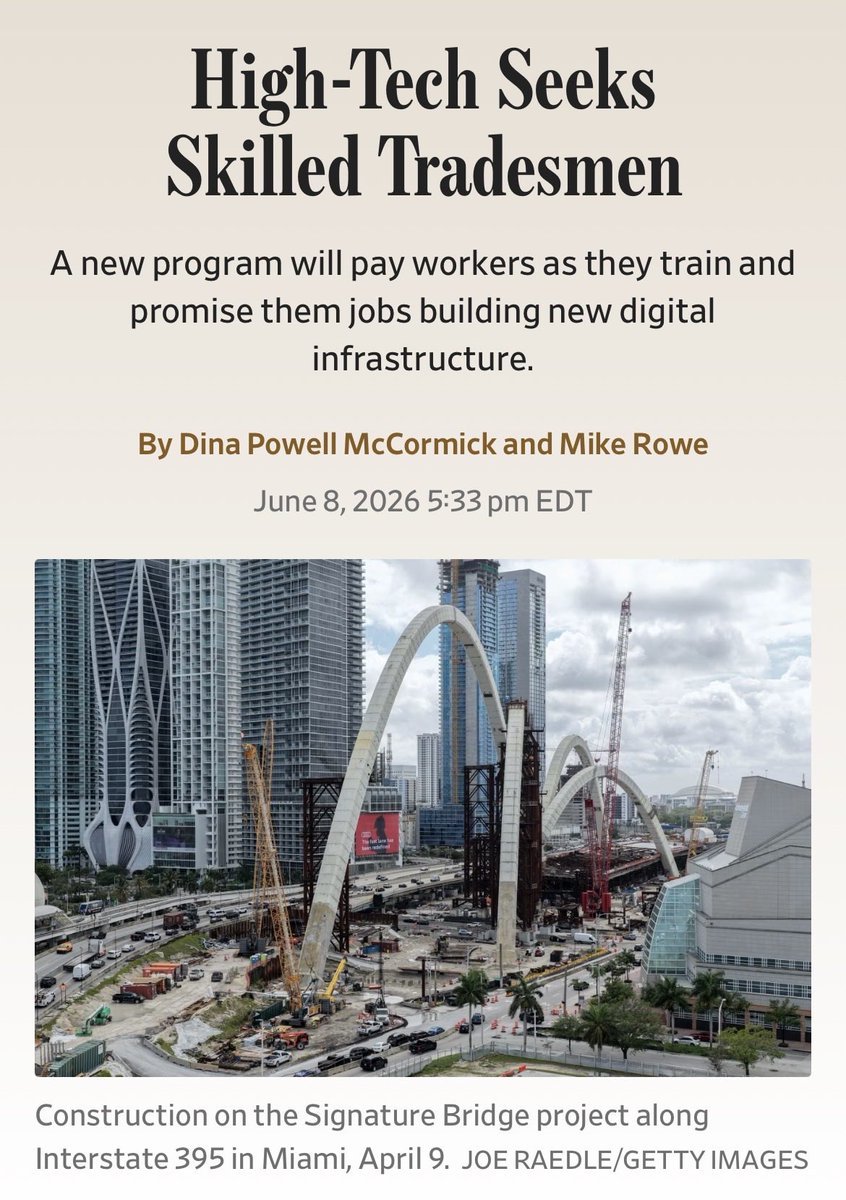

Meta is putting $115M into running a trade school. Paid training, guaranteed job, Mike Rowe fronting it. The graduates will build data centers.

The AI bottleneck has moved again.

1

45

Jun 11

BLS: ~81,000 unfilled electrician openings per year through 2034. ~30% of union electricians near retirement. An apprenticeship takes 4-5 years, the same lead time as a large power transformer.

You cannot expedite a journeyman electrician.

1

29

Jun 11

Hyperscalers signed 20-year power deals to integrate into energy, locked transformer slots to integrate into equipment, now they are integrating into labor.

A trade school run by a software company is not philanthropy, it is procurement. The constraint settles on the slowest clock.

18

Jun 10

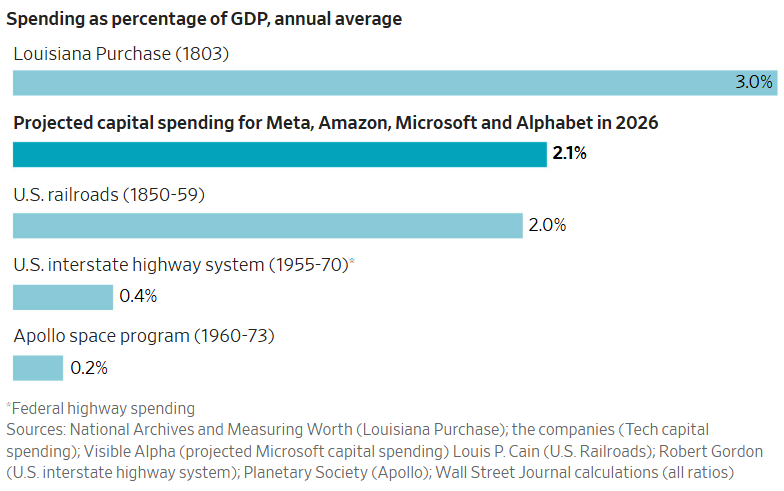

Everyone anchors on the $670B but the railroad comparison buries the real constraint, steel and land could be bought on demand while grid interconnection now runs 3 years and transformers longer, so capital was never what slows this down. x.com/charliebilello/status/…

Spending on data centers and other AI infrastructure by Google, Amazon, Microsoft and Meta is expected to hit $670 billion this year.

At 2.1% of GDP, that would represent a higher share of the economy than the investment in the US railroad expansion during the 1850s.

1

46

Jun 10

Meta signed for 6.6 GW of nuclear. Amazon locked 1,920 MW to 2042. Google bought SMRs.

2,500 GW is stuck in US grid queues. So Big Tech stopped waiting and started buying reactors.

When your biggest customers build their own power, you're just backup.

24

Jun 9

Microsoft is sitting on an 80 billion dollar backlog of Azure orders it cannot fulfill.

Not because it lacks chips. Because it lacks power.

That single number is the whole AI infrastructure story right now. Demand is not the constraint and silicon is not the constraint. The constraint is how many megawatts you can physically get to a building, and you solve that with transformers and interconnection queues, not with a better model.

38