Full-time Forex trader | Meantime, decoding startups.

Joined April 2021

- Tweets 254

- Following 132

- Followers 123

- Likes 701

114 Photos and videos

Pinned Tweet

11 Nov 2025

In India, AI tools like Perplexity Pro, ChatGPT Go, and Gemini Pro are all free.

It’s not generosity - it’s strategy.

Step 1: Offer free access = gain market share.

Step 2: Build user dependency = create network effects.

Step 3: Monetize once switching costs are high.

The new gold isn’t data. It’s attention lock-in.

2

345

Jun 12

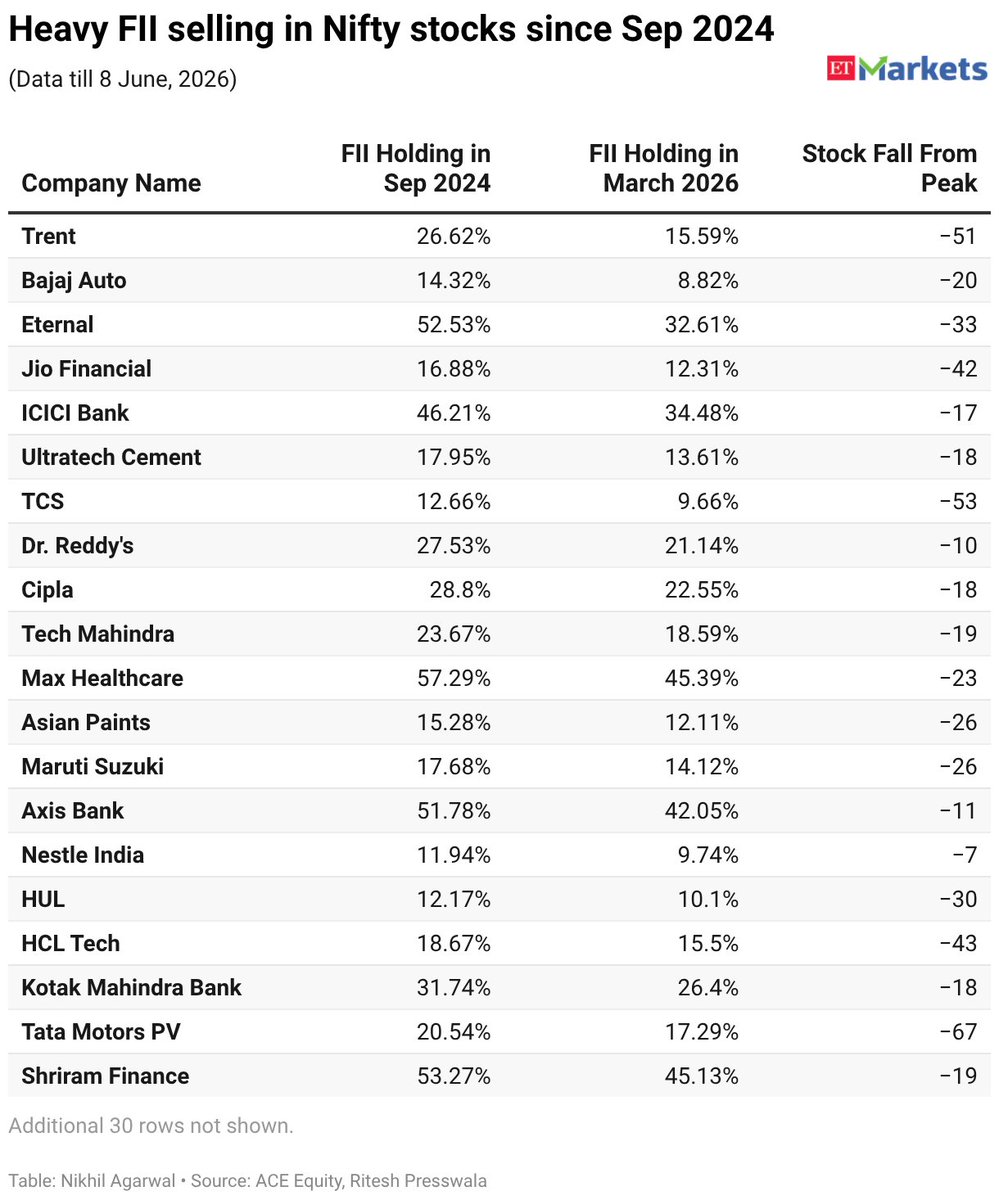

Foreign investors have significantly reduced holdings in many #Nifty companies since September 2024. This has impacted top blue-chip stocks, causing market returns to stagnate.

136

Jun 12

Tata Motors Passenger Vehicles, will raise prices of its cars and SUVs, including electric vehicles, by up to 1.5% from July 1, the carmaker said on Friday, its second price hike in four months as cost pressures from the Middle East conflict bite. #tata

95

Jun 12

ADIA's Platinum Jasmine Trust exits 2.3% of Lenskart for ₹1,960 Cr in block deals - just days after SoftBank's ₹2,873 Cr partial exit.

Yet buyers lined up: Kotak MF alone dropped ₹691 Cr.

Lenskart at ₹87,284 Cr mcap, 46% revenue growth in Q4 FY26.

The smart money is rotating - not running.

(source - entrackr)

51

Jun 12

Mamaearth parent stock hits 52-week high on strong FY31 growth outlook

27

Jun 12

Zepto P&L - line by line.

Revenue 2x'd YoY. Great. Now look at where the money actually went 👇

FY26 P&L (₹ million) 👇

Revenue from ops - ₹2,26,236

Purchase of goods - ₹1,84,850 (81.7% of rev)

Delivery & handling - ₹30,463

Employee costs - ₹17,847

Other expenses - ₹48,383

Total expenses - ₹2,90,267

Net loss - ₹59,052

So for every ₹100 Zepto earns, it spends ₹128.

BUT - FY24 ratio was ₹127. FY25 was ₹146. It's improving. Slowly.

The delivery handling line at ₹30,463 Cr is the one to watch. That's the dark store cost. As density increases, this number per order must keep falling.

Also - zero income tax in FY26. Massive accumulated losses = no tax liability for years. That's actually a hidden tailwind once profitability hits.

The P&L is ugly today. The trajectory is the investment thesis.

#ZeptoIPO

102

Jun 12

Zepto filed its DRHP. ₹80,100 Cr IPO incoming.

I read the whole filing so you don't have to.

Here's an honest take - should you invest, or is this hype dressed in purple?

1- The business in one line:

47.97M annual users. 1,139 dark stores. 2.33M orders/day. Revenue 2x'd YoY to ₹2,262 Cr.

Quick commerce grew from ₹133B to ₹963B GMV in 3 years. Zepto's order CAGR FY24-26: 119.5%. They're not just riding the wave - they're outrunning it.

2- The ugly number you can't ignore:

Zepto has NEVER made a profit. Not one year. Not one quarter.

FY24 loss: ₹1,215 Cr

FY25 loss: ₹4,700 Cr

FY26 loss: ₹5,905 Cr up 25% YoY

Net cash from ops: -₹3,462 Cr in FY26. Losses are growing faster than revenue. That's not a growth story -that's a burning building with a neon sign.

3- The unit economics are improving.

Adjusted EBITDA per order:

Q2 FY25: -₹171/order

Q4 FY26: -₹59/order

That's a 65% improvement in 18 months. The densification flywheel is working - more stores = shorter delivery radius = lower cost per drop.

If this trend holds, contribution-positive is closer than the P&L suggests.

4- The ad revenue angle nobody's talking about:

Ad revenue went from ₹8.93 Cr (Q3 FY24) to ₹542 Cr (Q4 FY26). Now at 7.88% of NRV.

This is Zepto becoming an ad platform. Brands WILL pay to be visible at the moment of purchase intent. Think Google Shopping, but inside a 10-min delivery window.

High-margin. Scales without capex. This is the hidden profit engine.

5- The IPO use of proceeds - smart or suspicious?

₹1,629 Cr - new dark stores

₹1,735 Cr - existing store lease rentals

₹1,325 Cr - tech & cloud infra

₹520 Cr - brand marketing

upto 35% for "general corporate purposes & unidentified acquisitions"

public money funds operating costs. The business isn't self-sustaining yet. That's a red flag for a value investor. Blue flag for a growth punter.

128

Jun 11

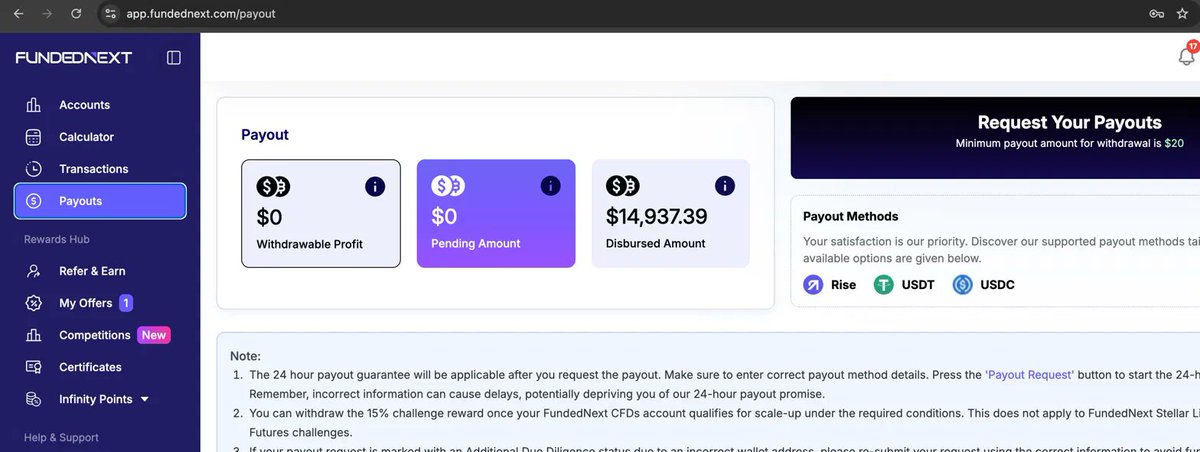

One year with @FundedNext - and what a journey it's been!

When I started my prop trading journey, I had one goal: find a firm that actually keeps its promises. After 12 months, I can say with full confidence - FundedNext delivers.

Here's my one-year recap:

1. $14,937.39 paid out (that's over INR 12.4 Lakhs!)

2. 0 payout rejections — not a single one

3. Every payout processed within 24 hours, exactly as promised

4. Customer support that actually shows up when you need them (especially #fundednext community manager @Flynnn_FN )

7

42

8,530

Jun 11

Gold surges $106 ( 2.61%) as Trump cancels Iran strikes, signaling a US-Iran deal approved by all parties.

#gold #xauusd #donaldtrump

2

114

Feb 13

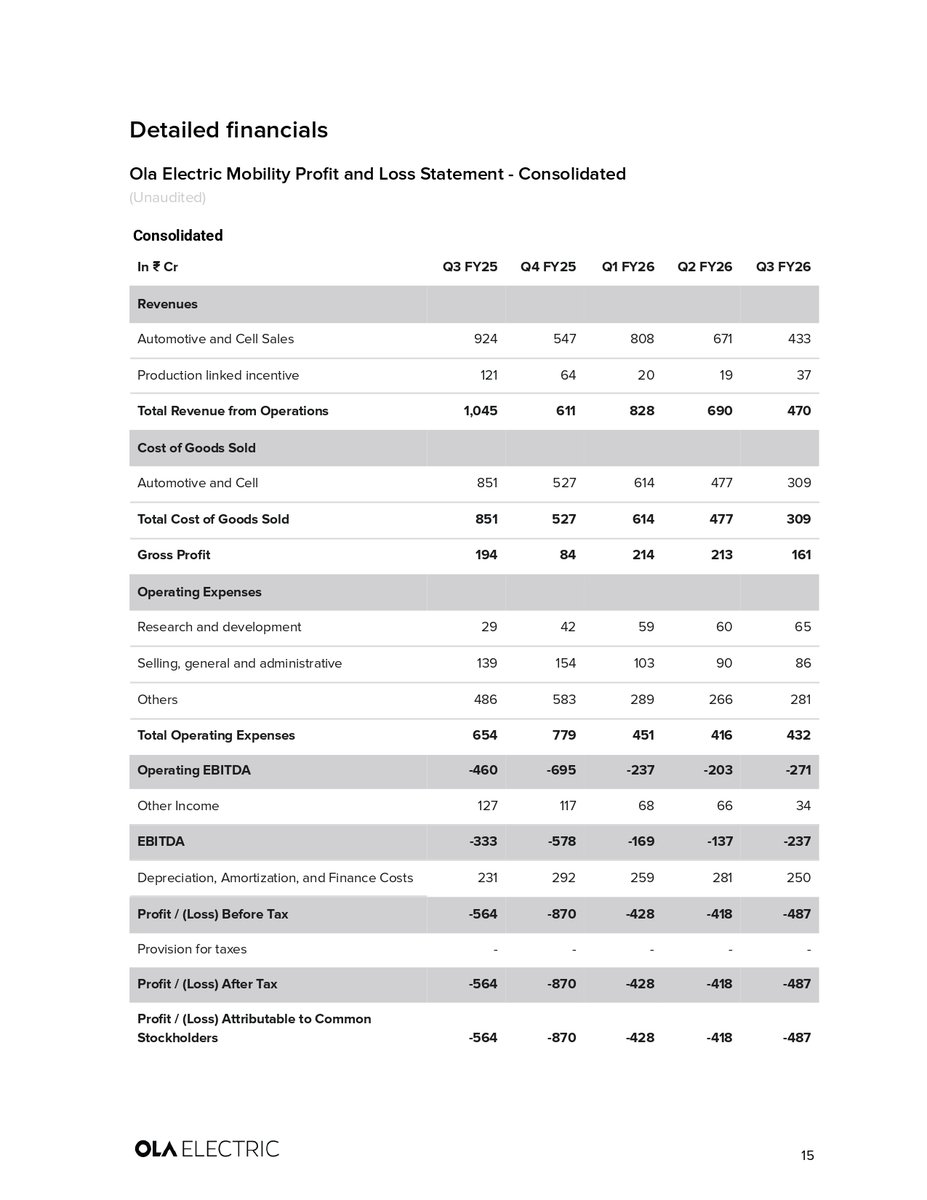

Ola Electric Q3 FY26 snapshot:

• Loss ↓ to ₹487 Cr

• Revenue ↓ 55% to ₹470 Cr

• Deliveries crash: 84k → 32.6k

• Gross margin hits record 34.3%

#OlaElectric

1

2

407

Jan 4

India × Venezuela

Who’s Actually Exposed?

With Venezuela back in global headlines, here’s a reality check on Indian companies with exposure and what it actually means for markets.

Oil & Gas: Strategic but constrained

ONGC Videsh (OVL): Equity stakes in Venezuelan heavy-oil projects (Carabobo).

Asset value exists, but cash flows remain blocked due to sanctions and payment constraints.

Indian Oil (IOC) & Oil India: Minority participation through joint ventures.

Exposure is long-term optionality, not a near-term earnings driver.

Reliance Industries, Nayara Energy, MRPL:

Exposure is through crude imports, not asset ownership. These links revive meaningfully only if sanctions ease.

Venezuelan crude is heavy oil and requires complex refining. India has the technical capability, but utilisation is driven by geopolitics, not oil prices.

105

Jan 3

Everyone’s talking about the claim that the US just gained $17 trillion worth of oil from Venezuela.

Let’s break it down simply.

Yes, Venezuela has the largest oil reserves in the world (~303 bn barrels).

And yes, oil is around $57 per barrel.

But reserves ≠ money.

Most of Venezuela’s oil is heavy crude.

It’s expensive to extract, needs special refineries, and takes years of investment to bring to market.

The US has not legally “taken ownership” of Venezuela’s oil.

Political statements do not mean instant control or the ability to sell oil.

Also important:

#Venezuela’s oil production is already very low due to sanctions and broken infrastructure.

So global oil supply hasn’t suddenly changed.

That’s why oil prices didn’t explode.

This is a geopolitical event, not a $17 trillion windfall.

Markets react to real supply, not viral math.

83

Jan 3

KFC & Pizza Hut operators in India are consolidating.

Devyani International will merge with Sapphire Foods, bringing together two major Yum Brands franchise partners to create one of the largest QSR platforms in the country.

The merger is a share-swap: 177 Devyani shares for every 100 Sapphire shares. Management expects annual synergies of ₹210–225 crore from the second full year, with regulatory approvals likely to take 12–15 months.

The combined entity will operate 3,000 outlets across India and overseas, securing pan-India franchise rights for KFC and Pizza Hut, while adding Sri Lanka to its international footprint—boosting procurement leverage and store-level efficiencies.

Post-merger, the platform competes more directly with Westlife Foodworld (McDonald’s India) and Jubilant FoodWorks (Domino’s), potentially strengthening bargaining power with suppliers and landlords.

183

Jan 2

Tobacco Stocks under pressure as India hikes cigarette excise duty effective Feb 1.

1

87

Jan 2

Ather vs Ola: Why markets are rewarding one & punishing the other

1. Both are loss-making EV players.

Only one is improving fundamentals.

2. Ather sales CAGR (3Y): ~77%

Ola sales declined in FY25.

3. Ather OPM improved from −523% → −20% (TTM).

Ola OPM worsened to −50%.

4. Ather losses are narrowing.

Ola losses are widening despite scale.

5. Balance sheet check:

Ather = controlled leverage

Ola = capital intensive dilution risk

69

15 Nov 2025

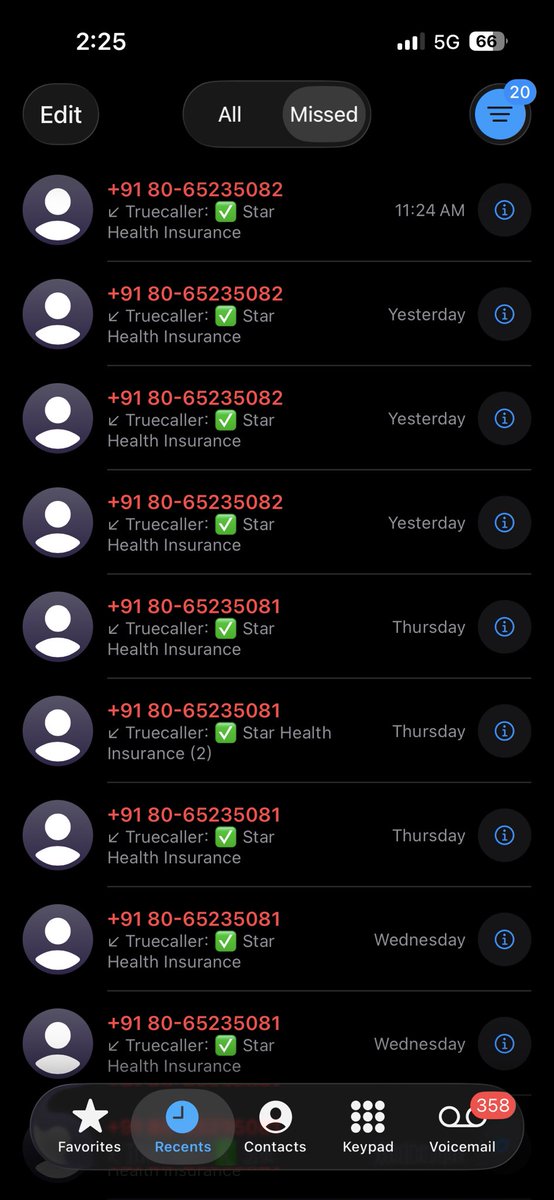

At this point, I think Star Health company misses me more than my ex ever did.

Fun fact: I never bought any insurance from them. Also added my number to DND, but still.

@StarHealthIns

1

73