Helping 3,500 investors build wealth in Digital Assets with the ABN System | Ex-Investment Banker → Co-Founder @ Decentralized Masters 👇

Joined January 2013

- Tweets 10,700

- Following 1,657

- Followers 2,476

- Likes 1,973

660 Photos and videos

Pinned Tweet

Apr 9

Two weeks ago we held Market Intelligence Live in Miami. Three days at the Fontainebleau with hundreds of our members.

3 days packed with real strategy sessions on positioning capital for 2026 to 2030.

The conversations that happened in that room, at dinner, in smaller breakout sessions, were the most valuable of my career.

Building a community online is one thing.

Meeting them in person changes everything.

1

5

888

In 2017, I gave back everything I had made in digital assets.

Four behavioral biases shaped the decisions that made me give back those gains. Once I built rules to counter them, I handled the next cycle differently.

1. Overconfidence bias: When everything you touch goes up, you stop asking whether it is you or the tide.

I was sure I was a genius. I was a passenger in a bull market, mistaking the ride for skill.

2. Recency bias: The brain treats the last few months as the permanent state of the world. Up feels like it will stay up forever, so taking profit feels insane, right up until the day it is obvious you should have.

3. Anchoring: Your mind locks onto the highest number it has ever seen and treats every price below it as theft. I refused to sell under my old high, holding out for a level that was never coming back.

4. Loss aversion: Selling a position in the red means admitting the loss is real, and the mind will avoid that admission all the way to zero. Mine did exactly that.

Every one of these is an emotional reflex. They only fire when your capital is live and your pulse is up.

So I learned their names and wrote a rule against each one in the dead market between cycles, when there was nothing open and nothing to feel.

When the next cycle came, the market did everything it had done before.

This time I kept what I made, because I had already decided what I would do back when I had nothing to lose by deciding clearly.

(This is commentary from my own experience, not investment advice. Always consult a qualified advisor for your situation.)

18

27

808

Jun 15

The first month our payroll crossed $1 million, I learned a discipline most investors never build: know what is coming in, what is going out, and exactly how long your cash can carry you.

Years in investment banking taught me to run portfolios by the numbers. A fixed seven-figure deadline made that discipline impossible to avoid as a founder.

Payroll arrives on a fixed date every month. It does not care what the market is doing, how confident I feel, or whether revenue came in as planned.

It is simply due.

A deadline like that forces a specific kind of thinking.

What is coming in against what is going out, and how many months the gap buys you.

Your portfolio has no payroll. Nothing lands on a fixed date and forces you to know your numbers.

So most investors never run them. Nothing forces them to. They wait until the market sets the deadline instead, and by then the decisions are emotional.

A $1 million payroll forced me to plan before the pressure arrived.

Your portfolio makes that same discipline optional. That part is on you.

Run your numbers now, while you can still think clearly, not when the market forces the issue.

(This is general commentary on behavioural patterns. Not personalised investment advice. Every position requires consideration of your situation, risk tolerance, and goals.)

8

16

512

Jun 13

I watched my parents get taxed 24% on every dollar they sent home.

Western Union called it a fee. I called it a system working exactly as designed.

When I got my CFA, I worked on a trading floor and sat inside M&A deals.

Somewhere in all of that, the fees stopped looking like an inconvenience and started looking like architecture.

Western Union charges 15% to 20% on remittances because the people sending money home have no alternative and no leverage to negotiate. The fee exists because the captivity exists.

PayPal buries a 3% to 4% currency spread inside the exchange rate on international transfers. Most users never notice because the math is hidden inside a number that looks like a simple conversion.

Stripe, when we launched our company, blocked $30,000 of our initial sales. Customers emailed them directly saying they wanted the charges to go through, they were happy with the service. Stripe refused. Then kept the money instead of issuing the refunds.

The system was built by institutions for institutions, optimized around participants who had the volume and leverage to negotiate favorable terms at every layer.

The banks and clearing houses who were already inside when it was built got the best terms.

Everyone else got what was left.

The reason Wall Street consistently wins has nothing to do with hiring smarter people.

They have better rails, faster settlement, lower fees, and access negotiated at a scale most individual investors will never get close to.

And for the first time in 50 years, those rails are being rebuilt by people who looked at what the current system charges and couldn't rationalize staying inside it.

3

14

28

2,231

Jun 12

Nobody had ever seen a CFA charterholder teaching crypto. Until Now.

The trust problem in this space has nothing to do with content. There is more content in crypto than anyone could consume in a lifetime.

The problem is none of it is verifiable.

Anyone can post a chart, get a call right, and have 100,000 followers by next month with zero auditable standing.

While the CFA is held by fewer than 200,000 people globally.

Three levels, pass rates hovering around 40 to 50% per level, permanent revocation if the code of ethics is violated.

I passed all three back to back by age 23.

When serious investors found my profile, they went to a public database, searched a name, found something real, and made a decision in 30 seconds.

In a space where everyone claims expertise and nobody can prove it, that's the whole game.

2

9

15

329

Jun 11

On July 4th, 2022, I posted something that made people think I had lost it.

Bitcoin had crashed from $69,000 to under $20,000. Celsius collapsed, Three Arrows was gone, and the entire space was being called dead by everyone with a platform.

And I posted publicly that I was increasing my spot exposure from 20% to 60-70% over the next six months.

The people paying attention came out well on the other side.

Every market runs two trends simultaneously. A secular trend and a cyclical trend.

The secular trend is the long-term directional move driven by adoption. Decades, not months. A 40% drawdown does nothing to that line.

The cyclical trend is the noise living inside that secular move. Retail watches it, builds permanent conclusions from it, sells, and waits for certainty that never arrives. By the time it does, the recovery has already happened without them.

Institutions treat cyclical swings as scheduled entry points.

On July 4th, 2022, adoption was still happening. Infrastructure was still being built quietly while retail was panicking loudly.

So I bought.

The question retail never thinks to ask during a drawdown is whether the secular thesis has actually changed.

If it hasn't, the drawdown is the market offering you a discount on something you already decided you wanted at a higher price.

(This is commentary, not investment advice. Always consult a qualified advisor for your specific situation.)

1

15

30

1,463

Jun 10

There was a night on the trading floor I think about more than almost any other moment from my Wall Street years.

A VP pulled me aside earlier that day. Merger in the works. Big deal. He told me to keep it quiet because our bank was also the market maker on that stock. The trading desk couldn't know. That's what the Chinese walls are for.

That same night I was having drinks with people from both sides of that wall having the same conversation.

Nobody said anything explicit. Nobody had to.

Information asymmetry at that level doesn't require anyone to break a rule. It just requires proximity. The right people in the same room reading the same signals.

Most retail investors are making decisions against this reality without knowing it exists.

The information game in traditional markets isn't rigged the way people think

It is not a conspiracy. Nobody is sitting in a dark room deciding to hurt retail.

The people with the earliest access to material information are simply the people physically closest to where it's created. By the time it reaches a retail investor reading about it on their phone, it's already been priced in.

That's not illegal in most of its forms. It's just how the system works when the infrastructure was built around institutional participants.

I spent years inside that system. I understood how it worked from the inside.

The question I kept coming back to was whether a market existed where that gap was narrower.

- Where large capital movements left a public footprint anyone could read

- Where transaction history was permanent and on-chain

- Where sophisticated money couldn't hide its activity the way it can in traditional markets

That question led me to crypto.

That's the game worth playing.

15

26

1,501

Jun 9

Most crypto investors lose in cycles they should have profited from.

1

14

23

1,267

Jun 8

In 2017 I made seven figures in crypto.

I thought I was the smartest guy in the room.

I had a thesis, conviction behind it, and enough chart time to feel dangerous.

I was moving capital around like I knew exactly what I was doing.

Then I lost it all.

Gambling and investing both involve risk. That's where the similarity ends.

A gambler accepts risk. An investor manages it.

The first question I ask before entering any position is what's the maximum I'm willing to lose, in percentage terms, before I exit. That number exists before I touch the keyboard.

I also keep a fixed limit on positions. If something new is worth entering, I cut something else first.

If the new opportunity has a better risk-reward profile than what's already in the portfolio, the weaker position goes.

That's allocation. A living, breathing framework with rules.

In 2017 I had 40 open positions and no exit plan on any of them.

This time, I had a structure in place.

Smart people with no framework just lose money faster than average.

I’ve seen it in my experience, that the best investors are the most disciplined ones.

2

17

664

Jun 5

The $25K minimum was never what stood between you and day trading profits.

Investing has three parts: planning, execution, and behaviour. This change hands you execution. Planning and behaviour were always yours to build.

For 25 years a rule supplied the discipline. The investors who learn to supply their own just gained the most.

Jun 4

Robinhood has lifted PDT restrictions.

No more $25K minimum, no more flags. Happy trading.

8

23

2,139

Jun 3

Owning more assets doesn't make you a better investor, but knowing which assets fit your investment strategy will.

A poor investor focuses on too many opportunities. It doesn't matter if the asset aligns with their risk tolerance, time horizon, or portfolio strategy. None of their positions will build wealth systematically.

A great investor is the opposite. Their investments fit a deliberate investment plan. If they define risk tolerance before position sizing, their portfolio survives downturns.

Being a poor investor with no plan is worse than not investing at all. Your portfolio will be whatever trainwreck you conjure up while scanning opportunities with no filter.

Let's say you go to the grocery store without a shopping list. You waste time scanning aisles and end up with more items in your cart than you should have. This same logic applies to picking the basket of assets that form your portfolio. The only difference is that your wealth will be affected by several orders of magnitude because of poor investment discipline.

At the end of the cycle, a poor investor will end up with dozens of trades, trading fees stacking up, and significant underperformance.

If you want to grow your wealth, your primary battle is planning first. You versus the temptation to skip straight to execution. Fighting every day to define your strategy before you deploy capital.

The order isn't optional if you want to be a great investor: planning, execution, and then behavioural discipline.

Your wealth depends on it.

13

435

Jun 2

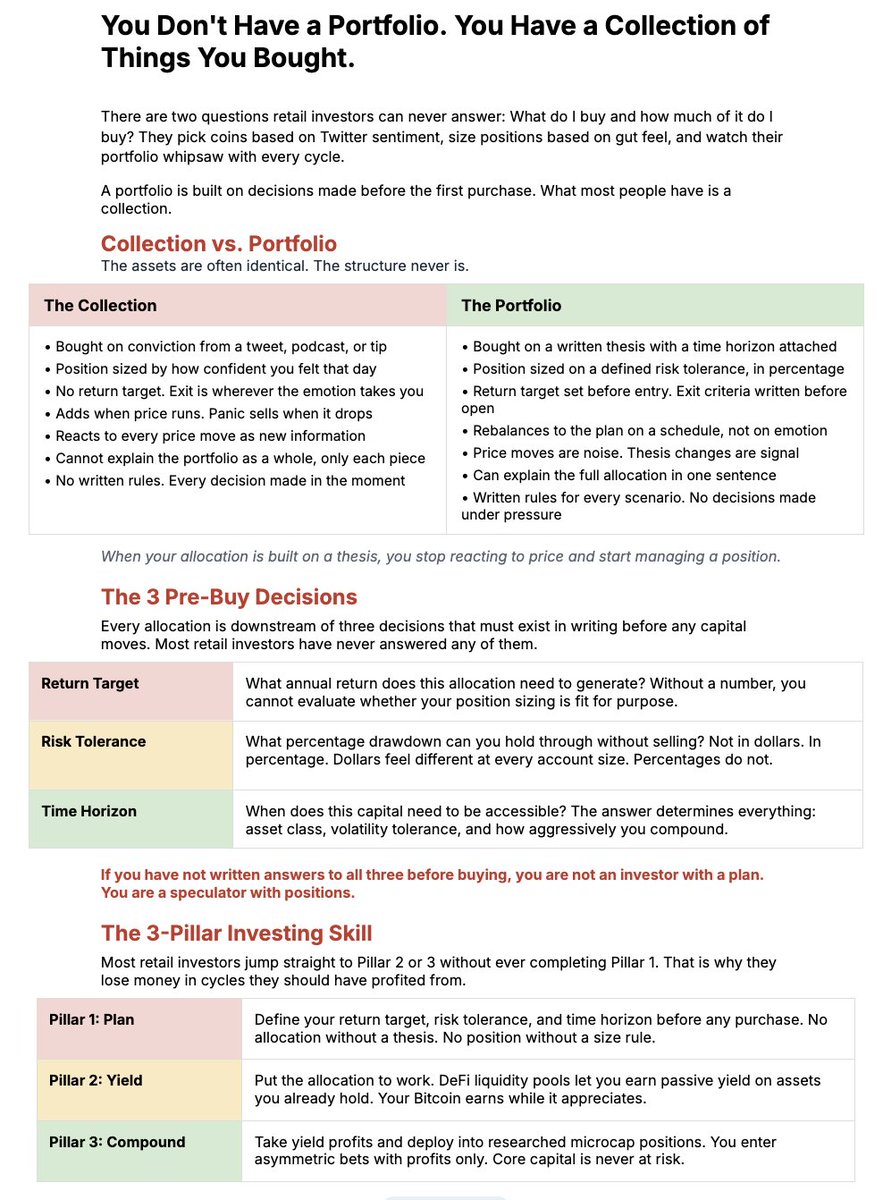

Retail investors often don't have a portfolio. They just have a collection of individual bets with nothing connecting them to an actual investment strategy.

They evaluate opportunities one by one. If something looks good, they buy it. And if something else looks good, they buy that too. But without a clear strategy, retail investors have no filter for how their collection of assets should fit together.

This approach misses the forest for the trees.

Every investment needs to be assessed based on whether it belongs in your portfolio, instead of each asset looking promising in isolation.

The investors who build real wealth start with the forest by mapping out their overall strategy first. Then they create filters to define what assets do and don’t belong. Then every opportunity gets assessed against those filters.

There's no reason to rely on luck when a strategy exists. You need an investment strategy built around your goals. Start analysing your portfolio by mapping out what you own, why you own it, and whether it belongs.

8

23

3,869

Jun 1

I've never told anyone this.

I didn't score as well on my CFA Level 3 exam as I did on Level 1 and Level 2.

I blamed it on working 24/7 as an investment banker and studying after midnight.

Level 3 is more than testing your knowledge of complex math formulas. It's about behavioural finance and the art of managing your emotions and understanding that markets are just the sum of every player's psychology, biases, and blind spots.

I understood the behavioural finance concepts. I just didn't believe they mattered at the time.

2017 proved me wrong. I made my first real money in crypto and then lost all of it.

I didn't take profit when I should have. At the time I thought I was a genius, but in hindsight, it was just luck.

The CFA Level 3 exam was trying to teach me the exact thing that later cost me everything I'd made that cycle. I just wasn't ready to hear it.

In 2021, I caught the cycle again. This time I kept what I made.

The only difference between losing it all and keeping it was my understanding of human psychology.

(This is commentary from my own experience, not investment advice. Always consult a qualified advisor for your situation.)

1

13

419

May 30

In this market, your wealth is no more stable than a melting ice cube.

With dollar devaluation currently running at 5% per year with no supply cap, fiat currencies are designed to devalue. By many estimates, real inflation runs higher than the official number, adding another few percent per year on top.

You need your investments to earn close to 10% per year just to maintain your wealth.

Sticking your money in your savings account won't help you. Neither do bonds or high-yield accounts that pay 4-5%.

Retail investors often skip this calculation entirely and put money somewhere that feels safe and call it a strategy.

However, some investors have started looking at stablecoin liquidity pools as one way to target higher yields. Unlike savings accounts and bonds, many of these pools have at times paid out more.

They don't carry the same directional market risk as equities, but they carry their own risks instead: smart contract risk, depeg risk, and liquidity risk.

That doesn't make stablecoin liquidity pools safe. But it's worth understanding they exist before assuming your only options are the ones your bank is offering you.

(This is commentary, not investment advice. Stablecoin liquidity pools carry significant risks including smart contract and depeg risk. Do your own research and consult a qualified advisor.)

1

7

15

623

May 29

ANCHORING BIAS COSTS RETAIL INVESTORS MORE MONEY THAN ANY OTHER BEHAVIOURAL FAILURE.

It makes you hold winners to zero, refuse to buy back in, and confuse memory with reality.

5 ways retail investors fall into this trap without realising it:

1. "The all-time high is X, I'd be making so little profit if I sold now."

1

15

24

1,452

May 29

5. “This industry/narrative is going to be the next big thing.”

As the old saying goes, "The market can stay irrational longer than you can stay liquid."

You may be right. You may even be ahead of your time. But that's just as harmful as being wrong. When you invest, you have to be right at the right time.

Anchoring can affect anyone. When it comes to investing, we typically look backwards to make investment decisions, but looking forward is the only direction that matters when you invest.

1

1

54

May 29

Never hold an asset for sentimental value. Over a full cycle, fundamental value tends to win out.

1

50