Joined June 2023

- Tweets 81

- Following 404

- Followers 56

- Likes 144

19 Photos and videos

May 16

what do you do after your AI video is done?

open TikTok Studio. copy link. open YouTube. fill caption. open Instagram...

I hated that workflow. so I just built Publish straight into KengStudio.

kengstudio.xyz 👇

21

Kiem Tran 🇻🇳 retweeted

Apr 14

Most people still see @solana as charts and noise.

But when you actually get close, you see something else:

-> real builders

-> real products

-> real users

-> real momentum

Packed rooms, live demos, serious conversations, teams shipping

That’s why Solana stands out. It doesn’t feel like an ecosystem waiting for a future. It feels like one already happening.

If doubt it, then watch this video.

Shoutout to @goatfishxyz for turning real Solana energy into something we can actually see and feel.

18

12

43

666

Kiem Tran 🇻🇳 retweeted

19 Dec 2025

Excited to share I've wrapped up my second internship at Flashbots (9th overall 😁), and I'm off to finish my last semester at UWaterloo! 🎓

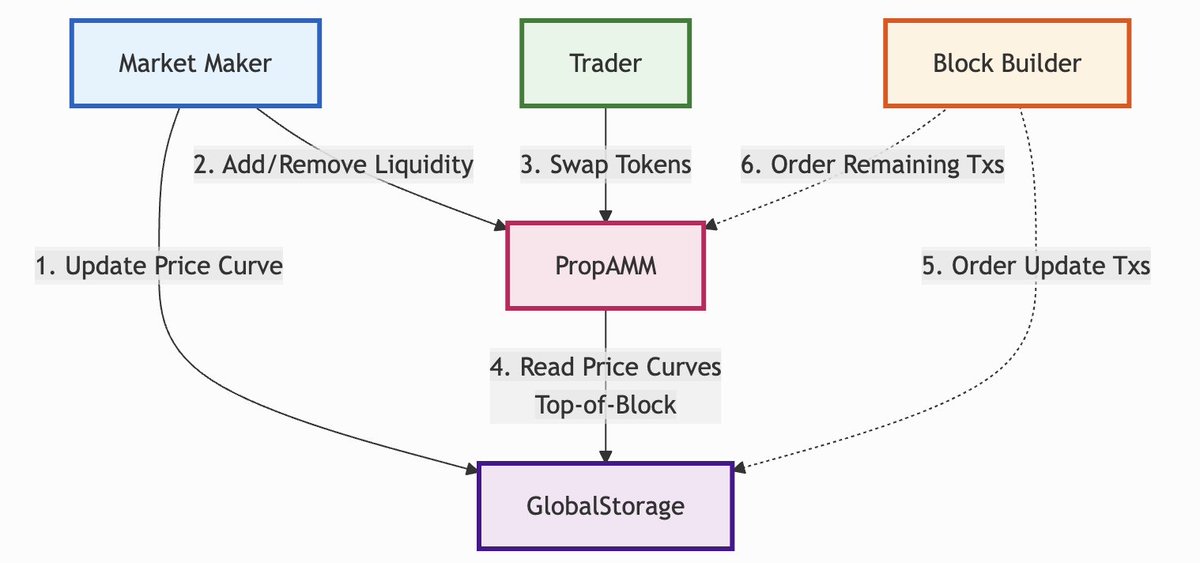

During my internship, I focused on the R&D question: "Can we bring Prop AMMs to EVM?", and the answer is YES with a working proof of concept!

Alongside my exploratory writeups, I've built a proof of concept Prop AMM that leverages a Top-of-Block priority lane for price updates (via a global storage contract custom builder logic) to ensure updates execute before swaps and with a local fee market.

Huge thanks to @DistributedMarz for enabling me to work on this problem, and @defin00b & @niftyiz for supporting me with their domain expertise! 🙌

45

27

480

33,702

Kiem Tran 🇻🇳 retweeted

9 Jul 2025

🚨 NOW LIVE: Suilend sSUI Loop Strategy

@ArmoredEnso’s latest strategy on @suilendprotocol helps you loop sSUI to earn up to 15% APY - without any manual steps.

• Loop 3x in one click: deposit sSUI → borrow SUI → swap for more sSUI

• Auto-loop. Auto-compound. Zero clicks, max gains on @SuiNetwork

New loop, new loot - join the giveaway now 👇

115

1,097

1,109

42,112

23 Jun 2025

Just picked up an Azuki Elemental. ⚡️

This isn’t about flexing => it’s alignment.

As someone who lives and breathes anime, I truly believe in what Azuki’s building.

Anime is the future. I’m all in.

#Azuki

1

14

287

Kiem Tran 🇻🇳 retweeted

24 Apr 2025

We’ve been building in public. The team is having a journey to @colosseum to learn and build🫡

Vertex is building a more convenient way to index Solana data — no infra, no headaches, just your data, your way.

Tell us what are u building and join the odyssey 🚀

2

3

9

519

Solana is great because it has a built in tornado cash since no one can read the explorer

204

149

3,509

418,749

Kiem Tran 🇻🇳 retweeted

20 Feb 2025

61

19

103

58,924

Kiem Tran 🇻🇳 retweeted

14 Feb 2025

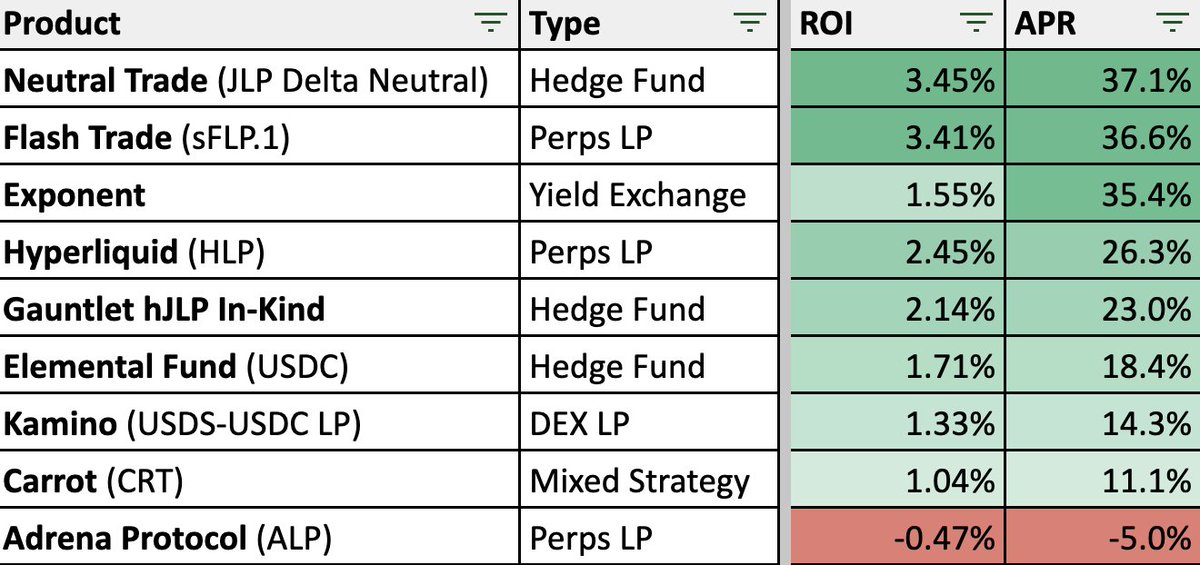

Stable(ish) Yield Update

I’m on a quest to find the best risk-adjusted yields. This update is part of a series of posts where I test different stable yield opportunities and share results of actual yield accrued over time. I hope this helps anyone who is on their own quest for quality yield on stables.

Disclaimers

🔸 None of this is financial advice. Please do your own research before making any major financial decisions.

🔸 This analysis has many different variables at play: products have different amounts invested, employ different strategies to earn yield, have different risk/volatility profiles, some auto-compound yield. I’ve calculated APR for each position to ensure some ability to compare, but don’t look at this list as a definitive ranking on which product is best to park stable assets; that decision will depend on your goals and risk appetite.

Results

The performance of each product over the time period of January 11 to February 14 is listed below. Exponent is the only position I opened later, so for that product, the time period is from January 29 to February 14. I’ve sorted the list by APR to offer the best comparison given the two different timeframes. Some observations below:

Neutral Trade continues to deliver

I have three hedge fund positions: @TradeNeutral Delta Neutral, @gauntlet_xyz hJLP In-Kind, and @elementaldefi USDC vault. Neutral continues to outperform significantly, and seems to offer additional upside via a points program (token?) and Drift FUEL points since their vaults utilize the Drift platform. I’m also in a reduced fee VIP Vault via @project_super_ which sweetens the deal further.

The hard part is deciding if it’s worth staying diversified and holding Gauntlet and Elemental or if it’s better to put the eggs in one basket and enjoy higher yield. I’ve leaned on diversification up to this point to ensure I avoid worst-case scenario issues that can always happen in the crypto space, and that will probably continue (though I may lower exposure to the others in favor of more Neutral).

Exponent is awesome, but timing matters

I covered @ExponentFinance in the last update, but for those who aren’t aware, it’s a yield trading platform that splits yield-bearing assets into income tokens (which offer fixed yield at a predetermined maturity date) and liquid yield tokens (which represent the yield portion of the yield-bearing asset). People who want fixed yields can lock their yield-bearing assets until maturity. People who want to speculate on yield volatility can trade liquid yield tokens with leverage. People who want exposure to fixed yields and trading fees can supply liquidity at a variable yield rate.

The yield has been phenomenal so far at > 35% APR! But this is not possible to achieve if you’re jumping in now. I was fortunate enough to be among the first depositors into the new USD* yield market which offered >30% APY fixed rate and >45% APY variable rate. You can see from the screenshots below that the variable yield is currently at 9.21% and fixed is at 13.39%, far below what I was able to lock in. I expect the 35% to drop as the current variable rate continues to pull the position down, but it’s still performing amazingly well for a lower risk position.

The major lesson here is to be aggressive when these new markets open up and pounce on lucrative fixed yields if they exist.

Some Perps LPs are more stable than others

I’ve shared six different stable updates, and @AdrenaProtocol was the top dog in three of them, including my last update two weeks ago. But the market is down since then, and Adrena is the least stable of my Perps LP positions thanks to its 85% exposure to SOL/BTC/BONK. So it’s on the losing end today.

By contrast, @flashtrade FLP and @HyperliquidX HLP have proven to be more resilient and have never registered a negative APY in the six check-ins I have done, so you could argue they are more in line with a stable yield option, at least since December. If I held JLP, it would be the top performing option on this list, and I remain confused on why it performed so poorly in December only to roar back to form in Jan/Feb.

The truly stable options are coming down to earth

After a wild stretch in November/December of 15–20% yields at places like @DeFiCarrot and Lulo, yields have come back down to earth. I can’t be upset with 11–14% APR on my most stable positions, though, and they still represent the two largest portions of my portfolio. I’m also looking forward to some of the new features that Carrot is building out via Greenhouse, which will enable higher yields via staking, lending, and looping CRT, and a Carrot Debit Card.

I’m not currently in @uselulo, but I am intrigued by their new Lulo Protect offering that gives users the option to earn lower yield (around 4.7%) that is backed by an insurance fund or higher yield that is the insurance fund (around 8.8%). One of the biggest problems with on-chain yield is the lack of insurance, so I think this is a cool step forward (though, importantly, it’s not on par with FDIC protection you will get in TradFi since you are still vulnerable to smart contract risks, de-pegging, and wallet drains).

Big Picture

One of the toughest tasks is deciding how to allocate across these different platforms. It’s not just about maximizing returns. It’s about maximizing risk-adjusted returns. The chart below offers some insight into how I am thinking about this right now and shows how much I am allocating to each option as well as a color-coding that indicates my opinion on the level of volatility, from lower (green) to higher (red). Some quick thoughts here:

🟢 Lower Volatility (Green): I consider Kamino liquidity pools to be the lowest option on the volatility curve. The platform is resilient, 3x audited, and yield derives from incentives. The only risk here is smart contract risk and depegging risk, both of which I consider to be low (and risks that are present on every DeFi platform). Carrot is also low volatility due to 2x audits and 80 % of it’s yield coming from audited lending platforms. Exponent is a newer platform, but is 2x audited and offers fixed yields as long as you hold until maturity.

🟡 Moderate Volatility (Yellow): The hedge fund strategies fit in this bucket because the yield depends on proper implementation of delta neutral hedging strategies, and it’s possible for the positions to have negative ROI. HLP has shown the lowest level of volatility among the Perps LPs and has been pretty much up only since I supplied liquidity in December.

🔴 Higher Volatility (Red): FLP, ALP, and JLP fit into this category, since all three have between 55–85% exposure to some combination of BTC/SOL/ETH/BONK. Platform fees help offset downturns, but there’s still risk here that these positions will fail to deliver positive ROI if we enter into a bear market downtrend. ALP is the most vulnerable in this scenario given its 85% volatile crypto asset exposure.

This is more art than science, but my thinking is to have at least 50% in lower volatility options, ~30% in moderate volatility options, and ~20% in higher volatility options. If I was more bullish on the market outlook, I would go more heavily into moderate/higher volatility options. If I were more bearish, I’d remove the higher volatility options.

Conclusion

That’s it for this week. I hope this insight is helpful. Let me know if you see things differently!

24

23

181

22,936

24 Jan 2025

Focking mad! @MadLads, ready for the MAD DROP?

Airdrop E.D.A.S for Lads holders from @ensodefai is shipping! Ticker: $EDAS

x.com/ensodefai/status/18825…

#EDAS #DEFAI @ensofi_xyz #CommunityAirdrop

65

20 Jan 2025

Impermanent loss doesn't exist 🙂

We aren't holding SOL or USDC, instead, we're holding a third coin that represents the average of the two. The benefit is generates trading fee and experiences only half the decline in value because it is the average of the two other coins

1

1

76

20 Jan 2025

of course, collect trading fee along the way, so in some ways it is more like selling cash-secured puts or covered calls with options trading

70

This is not just a function call. The agent will keep monitoring and repositioning your LP positions, while the chat terminal stays open for further interactions.

And there will be more interactions available.

Try it out yourself by checking out the PR

github.com/elizaOS/eliza/pul…

7

2

48

5,378

Kiem Tran 🇻🇳 retweeted

15 Jan 2025

AI DeFi = E.D.A.S 💪 Agents for Optimal Returns

Check It: defai.ensofi.xyz/

9

12

46

24,315

Kiem Tran 🇻🇳 retweeted

10 Jan 2025

Liquidity is LIVE on EnsoFi V2! 🚀

Deposit your assets and watch your earnings skyrocket with the new Liquidity feature! 📈

Start earning today: app.ensofi.xyz

Available now on @solana, with more chains coming soon!

10 Jan 2025

Liquidity is LIVE on EnsoFi V2! 🚀

The wait is over, EnsoFam! Deposit your assets and watch your earnings skyrocket with the new Liquidity feature! 📈

Start earning today: app.ensofi.xyz

Explore token pairs like SOL/USDC and USDC/USDT, and check out their APRs. We'll handle the rest, putting your assets to work in top liquidity pools on @RaydiumProtocol.

Easily track your positions, monitor rewards, and watch your earnings grow.

Available now on @solana, with more chains coming soon!

2

8

907