you optimize for the process not the result

Joined October 2022

- Tweets 1,200

- Following 614

- Followers 82

- Likes 7,326

36 Photos and videos

Krishsh.h retweeted

Jun 4

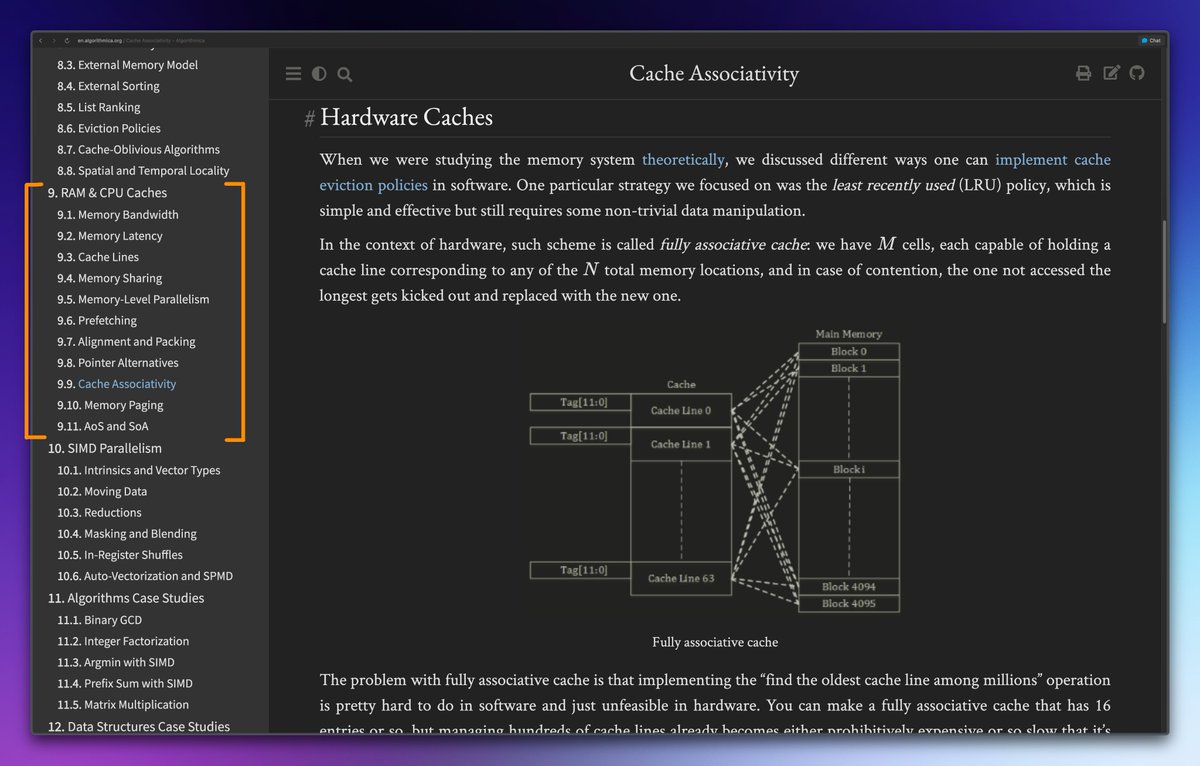

Memory organization with Algorithmica is one resource that keeps shining.

en.algorithmica.org/hpc/cpu-…

3

69

500

33,925

Krishsh.h retweeted

std::move doesn't move anything, it just casts to an rvalue reference.

9

2

88

18,943

Krishsh.h retweeted

Lock-free data structures do not eliminate contention, they only avoid blocking via locks.

9

3

53

8,025

Krishsh.h retweeted

Jun 3

In this CppCon 2022 presentation, Jan Bielak discusses strategies for writing efficient C programs - a good talk.

youtu.be/qCjEN5XRzHc

8

63

2,687

Krishsh.h retweeted

Jun 3

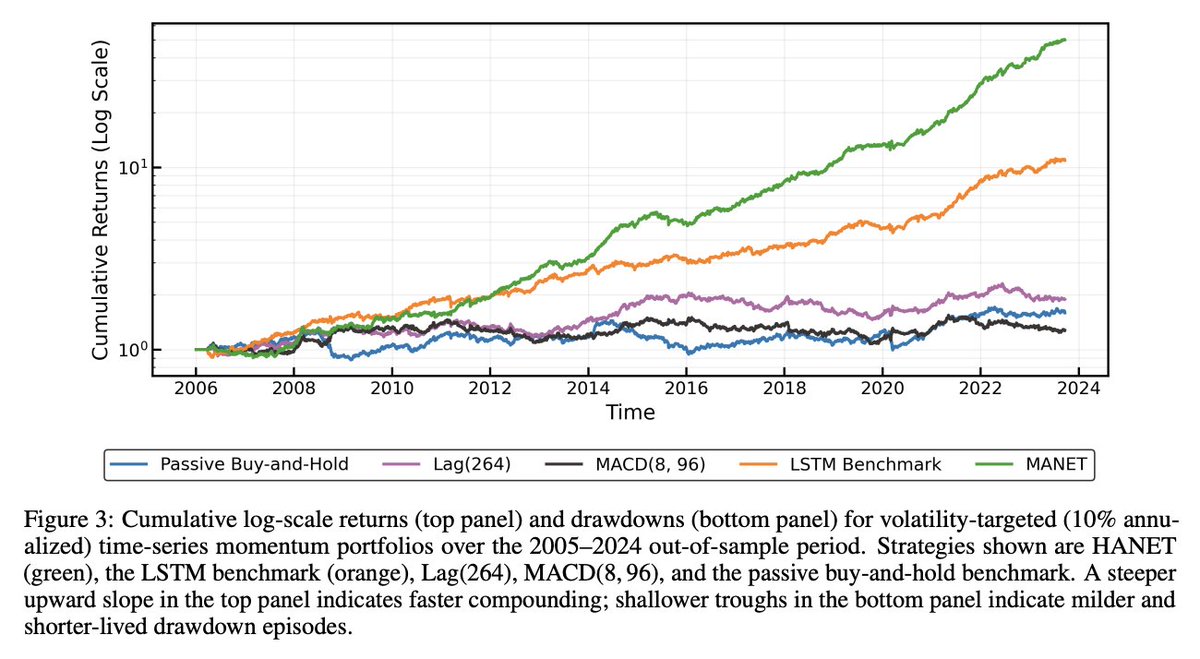

There is related research such as "Optimal Mean Reversion Trading with Transaction Costs and Stop-Loss Exit" (2014) by Leung and Li arxiv.org/abs/1411.5062 and a book worldscientific.com/worldsci… .

I did have an idea that did not work. Take a continuous indicator of regime change a use it a $vol or gmv modulator over time. Say, something that says “if the value is above one, run at full volatility. Below zero go to cash.” A large class is made by indicators of the form a*drawdown(t) b*t. This includes stop-loss, cusum, and approximate others. It took me two full days (and a lot of claude code) to determine that the only case that “works” is b=0. I.e., stop-loss. “Works” means that a solution exists and is nontrivial. So there is something special about stop-loss. My tentative recommendation is *not to use statistics used for tests of hypothesis outside of the intended application.* Obvious, maybe.

And another surprise. Stop-loss reduces sharpe, but only up to a theoretical max reduction of 50%. I feel that extensions to quadratic costs are within reach. I am writing this down and sending to my colleagues (esp. the sys PMs).

Notes: 1. The model is in continuous time. The math generated by claude seems correct but is a bit above me. 2. I thought of this problem last Sunday. This took two days of math and code-assisted simulations. I could ask questions between meetings, and at night. On my own, I don’t know if I could have gotten an answer ever. 3. There are still five days this week. Gotta hurry up. I wonder what we’ll find out.

There is no time like the present, people.

9

77

13,330

Krishsh.h retweeted

Jun 3

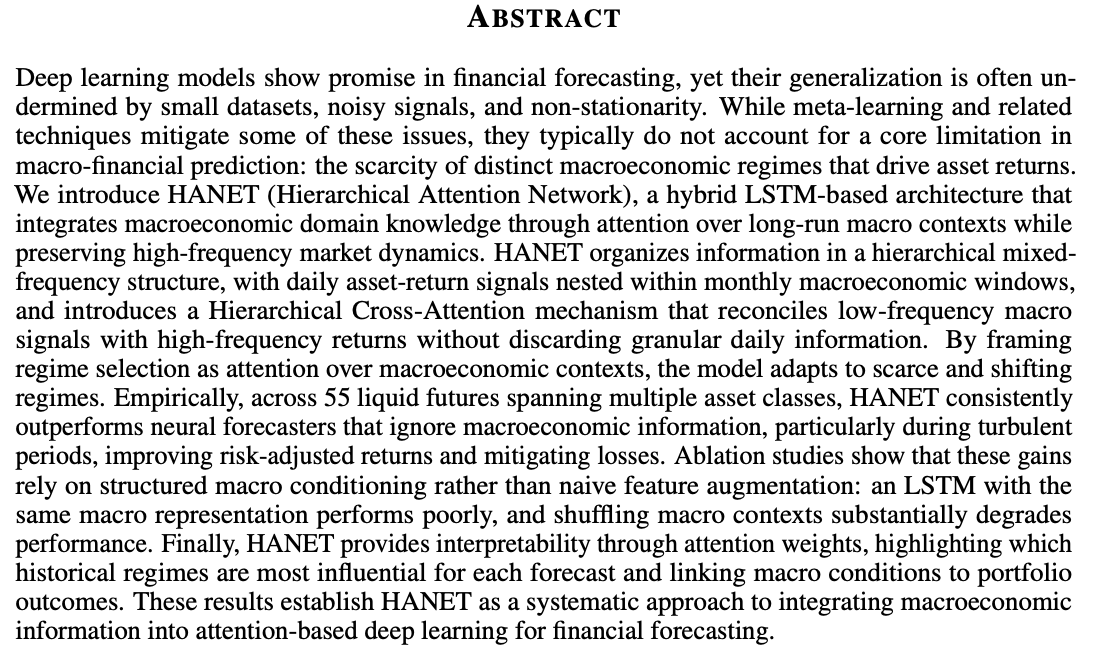

"Macro-aware time series forecasting via hierarchical mixed-frequency attention models", arxiv.org/pdf/2606.00624

2

7

112

5,608

Krishsh.h retweeted

Apr 4

A Concurrency Cost Hierarchy by Travis Downs

travisdowns.github.io/blog/2…

24

194

34,221

Krishsh.h retweeted

May 30

People complain the smartest engineers work at companies like JS.

While we probably lost many more of them to MOBA games.

1

25

1,546

Krishsh.h retweeted

May 20

Link to Godbolt for this short example

godbolt.org/z/rYfEP99Tx

2

21

3,858

Freak

May 17

The smartest man ever

John von Neumann made groundbreaking contributions across fields. He was one of the key mind behind the atomic bomb, early computers, game theory, and quantum mechanics. He even theorized self-replication before DNA was discovered.

47

Krishsh.h retweeted

May 14

And then this: quantitative-research.de/ (Hans Buehler's, co-ceo of XTX, blog). Just a small example:

- Lecture Notes Learning to Trade I: Statistical Hedging

- Lecture Notes Learning to Trade II: Deep Hedging

papers.ssrn.com/sol3/papers.…, papers.ssrn.com/sol3/papers.…

2

19

216

25,576

Krishsh.h retweeted

25 Jun 2025

Socialism is like polio, it comes back when people forget about the horrible damage it did last time.

3,101

18,679

103,444

12,639,642

Krishsh.h retweeted

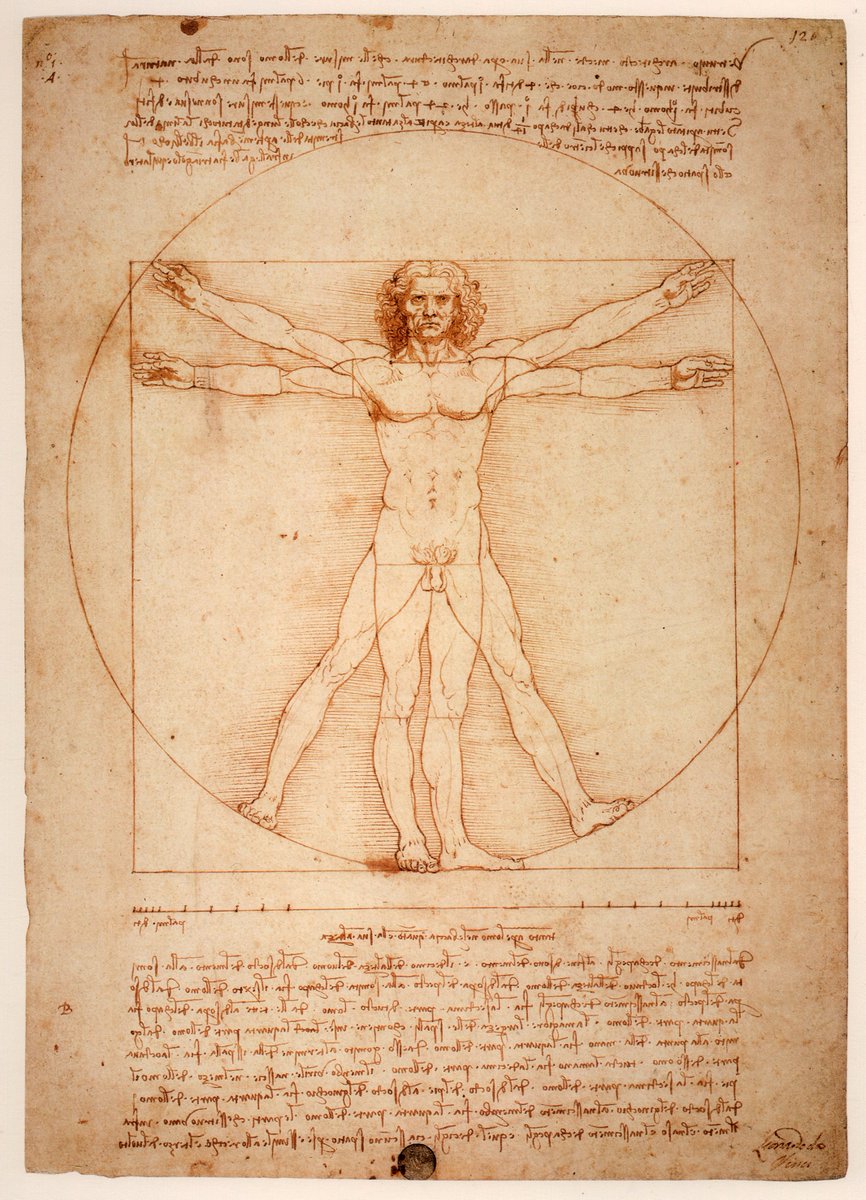

May 9

One of Leonardo's drawings, the Vitruvian Man, is a study of the proportions of the human body, linking art and science in a single work that has come to represent the concept of macrocosm and microcosm in Renaissance humanism.

2

8

72

2,484

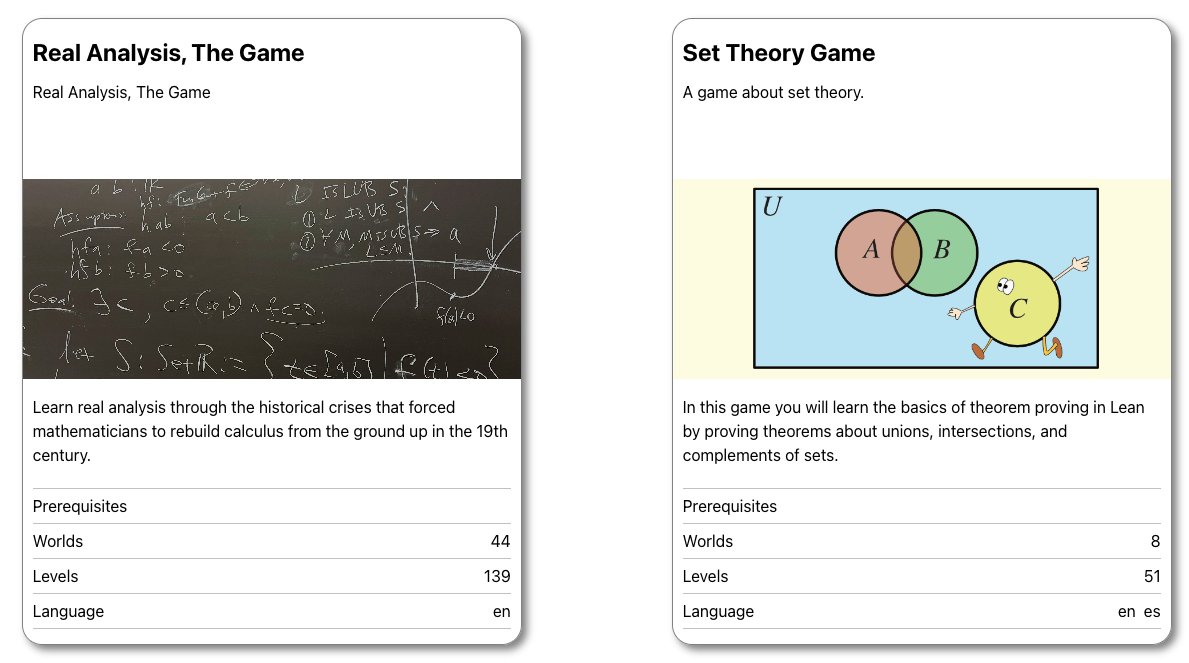

Lean 4 Game

github.com/leanprover-commun…

通过游戏化学习数学证明的方法

May 6

Many #LeanLang users were first introduced to Lean via the Natural Number Game, a gamified approach to learning mathematical proofs developed by Kevin Buzzard.

The Lean Game Server now hosts 8 games, including real analysis, linear algebra, and introduction to proofs. Open source, so educators can build their own too.

Explore: adam.math.hhu.de/

#FormalMathematics #MathEducation #OpenSource

1

37

325

22,844