Artificial Intelligence | Stock Investor| LLM Consultant

Joined November 2024

- Tweets 645

- Following 473

- Followers 75

- Likes 1,194

102 Photos and videos

Jun 12

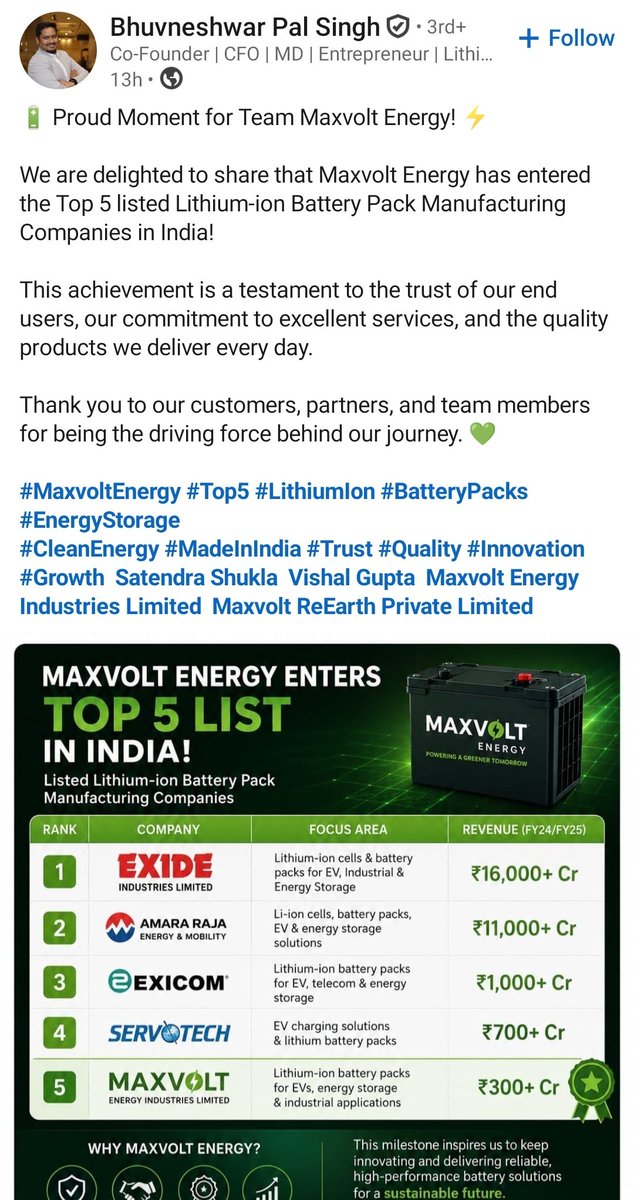

Maxvolt Energy

-----------------

Small steps....

Source - Linkedin

1

88

Jun 10

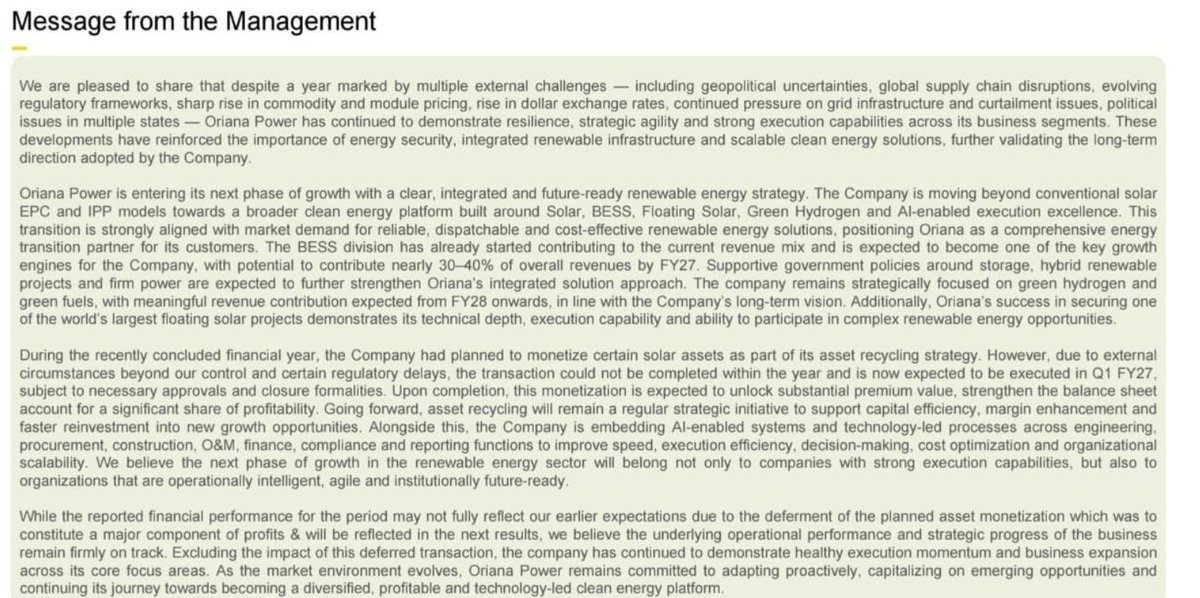

Oriana Power – Key Takeaways from FY26 concall

1. Asset monetization planned for FY26 was delayed due to regulatory and external factors.Transaction now expected to close in FY27.

2. Management indicated that the deferred monetization was expected to contribute a significant portion of FY26 profits and should reflect in upcoming results if completed.

3. Core business operations remain strong, with management emphasizing that the earnings miss was largely due to timing rather than operational weakness.

4. BESS (Battery Energy Storage Systems) is emerging as a major growth driver and is expected to contribute 30–40% of revenues by FY27.

5. Company is transitioning from a pure Solar EPC player to an integrated clean-energy platform covering:

Solar EPC

IPP

BESS

Floating Solar

Green Hydrogen

6. Strong project pipeline and execution visibility continue across solar and storage segments.

7. Asset recycling will be a recurring strategy: develop assets → monetize at premium valuations → reinvest capital into new projects.

8. Green Hydrogen remains a strategic focus area, with meaningful revenue contribution expected from FY28 onwards.

9. AI-driven systems are being deployed across engineering, procurement, construction, O&M, finance, and compliance to improve efficiency and scalability.

10. Management remains confident about long-term growth despite challenges such as module price volatility, currency fluctuations, grid constraints, and regulatory changes.

4

1,169

Jun 10

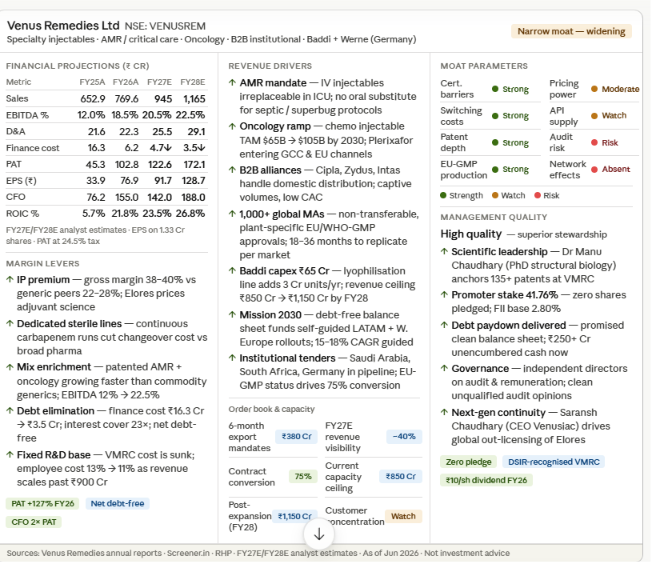

Venus Remedies.

Jun 10

#venusremedies

Is Venus Remedies a boring 15–20% compounder quietly doing hospital supply rounds — or a deeply misunderstood asymmetric bet hiding behind a pharma label nobody bothers to read? 🧵

The business

Venus Remedies is not your typical pharma company grinding out generic tablets for retail chemists. It operates in a niche that most investors walk past: sterile injectable formulations for hospital ICUs — antibiotics that fight drug-resistant superbugs, chemotherapy injectables, and critical care drugs that can only be delivered intravenously in a controlled clinical setting.

For nearly a decade the company struggled — good science, poor commercialisation, heavy debt. Then management made two pivots that changed everything: they stopped selling complex molecules directly, instead signing manufacturing alliances with Cipla, Zydus, and Intas who already owned hospital relationships. And they cleared every rupee of debt from operating cash flow. Today Venus runs a debt-free balance sheet with ₹250 Cr in unencumbered cash — while its sterile lines run at near-full capacity.

The moat — especially the IP layer

Two-layer moat.

The outer wall: 1,000 global Marketing Authorisations(license to sell medicines) tied to specific plants, non-transferable, each taking 18–36 months to secure. Any competitor replicating Venus's export footprint needs a decade and hundreds of crores just for paperwork.

The inner wall — the one the market keeps mispricing — lives inside the Venus Medicine Research Centre (VMRC). A DSIR-recognised in-house lab generating 135 global patents across the US, EU, and India. The core breakthrough: proprietary Antibiotic Adjuvant Entities — molecules that don't just treat infections, they disarm the bacterial resistance mechanism itself. The flagship Elores shields antibiotics from the beta-lactamase and carbapenemase enzymes bacteria use to neutralise them.

Management — why trust them

Two reasons: tested under pressure, and kept their word.

Dr Manu Chaudhary (Joint MD, PhD structural biology) personally anchors the 135 patent portfolio — a promoter-scientist who built the core moat. Pawan Chaudhary (MD) architected the commercial pivot. Saransh Chaudhary (next-gen, CEO Venusiac) now drives global out-licensing of Elores.

Promoters hold 41.76% equity with zero shares pledged. When debt was heavy and commercialisation was stalling, management did not dilute equity, did not diversify — they paid down every rupee from operations. FY26 net profit: ₹102.78 Cr, up 127% YoY. Under-promise, over-deliver.

Current numbers and EPS trajectory

FY26 actuals: Sales ₹769.6 Cr · EBITDA margin 18.5% · PAT ₹102.8 Cr · EPS ₹76.9 · ROIC 21.8% · CFO ₹155 Cr — cash conversion 1.5× reported profit.

Base-case model at 15–18% guided revenue growth: FY27E EPS ₹91.7 · FY28E EPS ₹128.7. At CMP ₹1,610, that is 12.5× forward P/E on FY28E — priced as if it is still the debt-heavy generic manufacturer of five years ago.

The asymmetric bet — four levers and why now

Most estimates only capture revenue growth. The real asymmetry is what happens when product mix shifts toward high-margin, IP-protected molecules.

1. Mix shift: generic → proprietary IP drugs — the highest-probability lever and the most direct EPS driver. Venus sells a blend of commodity generics (gross margin ~28–30%) and proprietary patented formulations like Elores (gross margin ~45–50% ). As Elores scales deeper into hospital formularies, every 5% revenue mix shift adds ~150–200 bps EBITDA margin. On just 1.33 Cr shares, each 100 bps margin expansion = ~₹5–6 EPS uplift. If EBITDA exits at 26–28% instead of 22.5%, FY28E EPS reaches ₹155–170 — not ₹128.

2. Global Elores out-licensing milestones — Venus already received a ₹11 Cr milestone payment from one AMR licensing deal. Each EU or US agreement adds upfront fees plus multi-year royalties — zero incremental capex. Two or three deals could add ₹15–25 Cr PAT annually, translating to ₹11–19 EPS purely from licensing income.

3. AMR becomes a global policy emergency — WHO, G7, and EU have flagged antimicrobial resistance as a tier-1 crisis. Fast-track procurement frameworks for proven AMR therapies are being legislated now. Venus is one of the very few companies globally with commercially validated, patented, adjuvant-based AMR solutions already in 60 countries — a potential strategic acquisition target for Big Pharma missing this platform entirely.

4. Plerixafor oncology inflection — entry into the $65B → $105B chemo injectable market via GCC and EU hospital formularies. EU-GMP manufacturing and regulatory filings are already in place. Adoption is a matter of when, not whether.

⚡ Why now — five reasons the window is open today

→ Balance sheet inflection just happened. The debt paydown that unlocks all future optionality was completed in FY26. You are evaluating this in the first year of a clean, self-funding capital structure

→ Capacity expansion is being commissioned now. The ₹65 Cr Baddi lyophilisation line — which raises the revenue ceiling from ₹850 Cr to ₹1,150 Cr — goes live in Q2 FY27. The earnings impact will show up in the next 2–3 quarters.

→ Mix shift is at its earliest visible stage. EBITDA expanded from 12% to 18.5% in a single year as patented molecules grew faster than generics. The inflection has started . At 22–28% EBITDA, this is a completely different earnings machine.

→ Global AMR policy is accelerating. The EU's AMR Action Plan and the US PASTEUR Act are moving from discussion to legislation in 2025–26. Governments are creating guaranteed procurement frameworks for validated AMR drugs — and Elores is one of the very few that qualifies today.

→ Valuation has not caught up (or has it ??). At 12.5× FY28E on a debt-free, 21% ROIC, IP-protected business with an expanding moat — the stock is priced for a generic compounder's destiny, not a specialty pharma platform's (it may be totally wrong to interpret this way).

Venus Remedies is an IP-protected, debt-free, founder-scientist-run specialty pharma company at 12.5× FY28E earnings. The base case already works. The mix-shift toward proprietary molecules is already happening and unpriced. The licensing optionality, AMR tailwind, and oncology expansion sit on top as free options. The window is open because the balance sheet cleared last year and the capacity expansion fires next quarter.

Is the market still seeing a debt-laden generic injectable manufacturer from five years ago — or has it simply not looked closely enough at what is quietly being built inside?

[Not investment advice, DYOR]

317

RT @shiladitya4u: Sakar Healthcare

There are quite a few companies in the small & microcap pharma space which I like and Sakar healthcare…

28

Jun 2

Maxvolt Energy Industries Ltd: Powering India’s Unregistered EV & Aggressive Shift into Circular Battery Economies open.substack.com/pub/suren2…

150

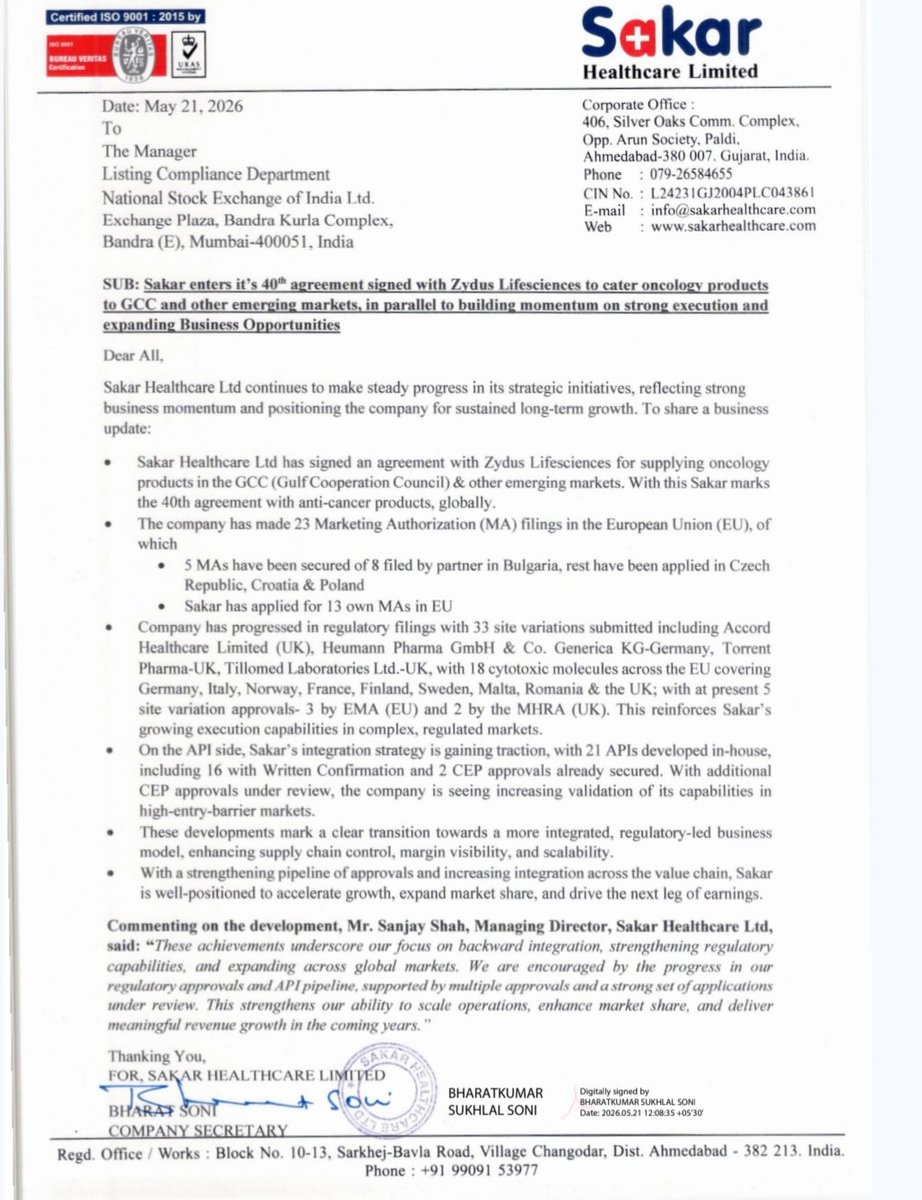

Sakar and Zydus has an agreement to supply Oncology products in the GCC and other markets.

#sakar

89

May 29

Result season is almost going to over. Some of the companies provided good guidance for FY 27.

Disc: No buy/sale recommendation. This is for educational purpose only

1

2

45

May 29

Excellent information.

May 22

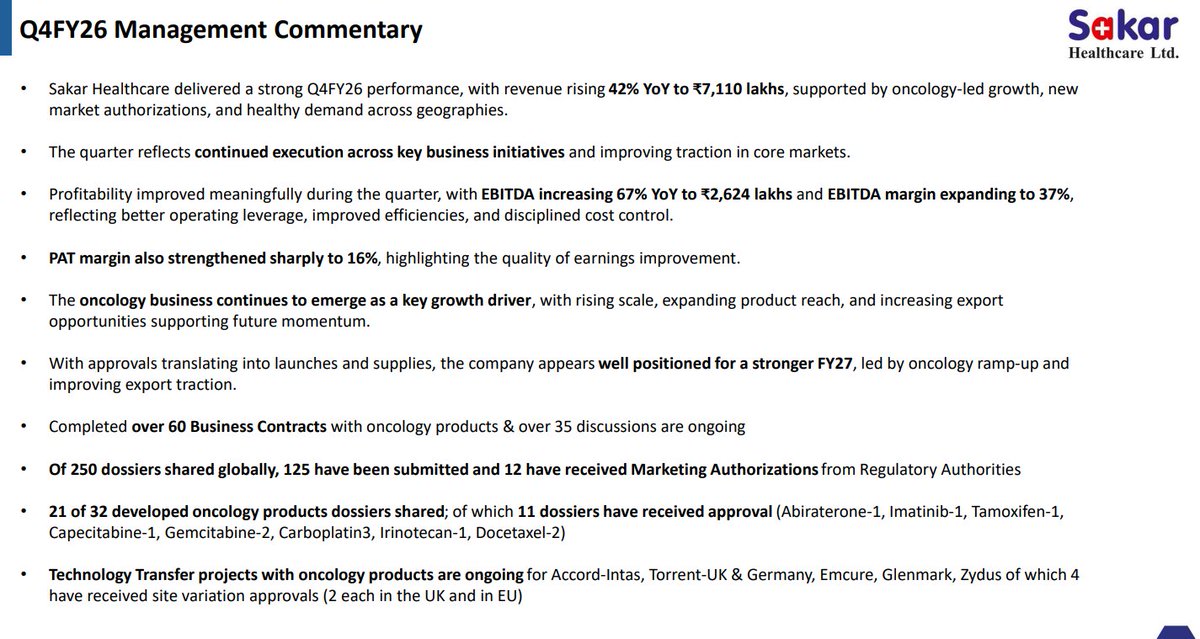

Sakar Healthcare Ltd - Q4FY26 | Concall Insights

Financial Highlights

•Q4FY26 revenue from operations grew 42% YoY to ₹71.1 crore

•FY26 revenue increased strongly to ₹251.7 crore versus ₹177.6 crore in FY25

•Q4FY26 EBITDA increased 67% YoY to ₹26.2 crore with EBITDA margin at 37%

•FY26 EBITDA grew 39% YoY to ₹68.9 crore

•Q4FY26 PAT grew 91% YoY to ₹11 crore

•FY26 PAT increased 74% YoY to ₹30.5 crore

•Gross margins remained healthy at 60% driven by operational efficiencies and oncology scale-up

•Management expects margins to sustain and improve further with rising oncology contribution

Oncology Business Growth

•Oncology business contributed 38% of FY26 revenue versus 21% in FY25

•Q4FY26 oncology revenue stood at ₹31.5 crore

•Company targets doubling oncology revenues over next two years

•Management aims to achieve ₹500 crore revenue milestone within two years driven primarily by oncology

•Long-term oncology-led revenue potential from Bavla facility estimated at ₹800 crore-₹1,000 crore at optimal utilization

•Oncology exports expected to become dominant growth driver over medium term

Exports & International Expansion

•Company positioning itself as a pure-play export-led oncology player

•Exports already underway to UK, Mauritius, Lebanon, Algeria and African markets

•Accord Healthcare UK approved Imatinib manufacturing for European supplies

•More than 60 oncology business contracts signed with 35 ongoing discussions globally

•125 dossiers filed globally out of 250 dossiers shared, with 12 marketing authorizations received

•Company targets 300 dossier approvals and 100 overseas business contracts over next two years

•Management expects oncology exports and domestic oncology sales to become nearly equal during FY27

Partnerships & Technology Transfers

•Technology transfer projects ongoing with Accord, Intas, Torrent, Emcure, Glenmark and Zydus

•Accord-Intas portfolio includes 10 oncology products with revenue opportunity of ₹50 crore-₹100 crore

•Five tech transfer projects for Europe and UK already commercializing from Q1FY27

•Seven additional Accord products under regulatory approval pipeline for Europe

•Management expects strong export commercialisation from Q2FY27 onwards

•Commercial supplies from tech transfer projects expected to significantly accelerate oncology growth

Capacity Utilization & Manufacturing

•EU-GMP approved Bavla oncology facility designed for regulated global markets

•Facility supports oral solids, injectables, oral liquids and oncology APIs

•Current oncology plant utilization remains below 30%, leaving strong operating leverage potential

•Management expects utilization to improve to 50%-55% over next two years

•Long-term expansion achievable without significant incremental capex

•API integration progressing with 21 in-house cytotoxic APIs developed

Regulatory & Product Pipeline

•11 approvals received for key oncology molecules including Imatinib, Abiraterone, Capecitabine and Gemcitabine

•Two CEP approvals already received for Gefitinib and Capecitabine APIs

•Additional API approvals under process for regulated markets

•31 oncology dossiers currently under registration globally

•Company expects significant commercialization of registered products during FY27

•Regulatory approvals and technology transfers validating Sakar’s manufacturing and compliance capabilities

Guidance & Strategy

•Management targeting ~40% revenue growth in FY27

•Oncology expected to remain key growth engine for next several years

•Long-term revenue mix target is 60% oncology and 40% non-oncology

•Within oncology, target mix is 65% exports and 35% domestic

•Focus remains on increasing dossier approvals, expanding international partnerships and scaling regulated market launches

•Company expects EBITDA margins in oncology division to sustain at 25%-30% over medium term

63

May 29

FY 27 guidance: 40%

Disc: This is not a buy/sale recommendation. This is only for Educational purpose only.

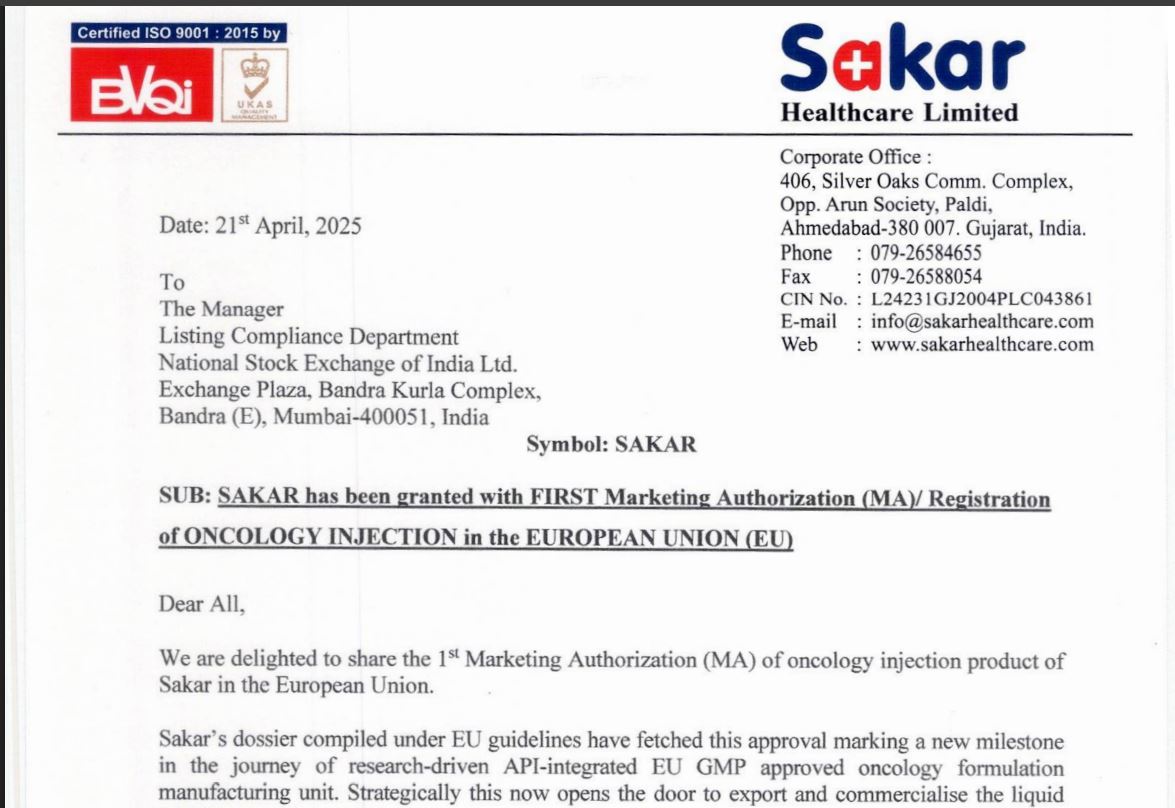

21 Apr 2025

Sakar Share the first MA of oncology injection product of Sakar in EU.This approval signifies a significant milestone in Sakar Healthcare's international expansion, enabling the company to enter the European oncology market.

1

29

Sameer Kumar retweeted

May 29

Oriana Power

H2FY26 results have margin pressure but it may be sustained strategy to get good business and good cash flows. I doubt if these margins are going up in future, more so when BESS etc is coming up

But very strong P&L growth overall in FY26

CFO is also looking good

Transition as bigger player happening

Green Hydrogen and BESS

Good bids there and signing agreements

• Signed a 10-year binding Green Ammonia Purchase Agreement (GAPA) with the Solar Energy Corporation of India (SECI) for a capacity of 60,000 tonnesper annum (TPA). The total contract value is estimated to be approximately ₹3,135 crore.

•Advancing green fuels projects in major industrial states includingMP, AP, Maharashtra and UP, working in line with government policies

• Advancing green ammonia project execution by identification of 1200 acre land in MP

Secured our first utility scale solar BESS hybrid project (100MW/300MWh) connected at CTU Commissioned the first Group Captive Open Access project of Rajasthan, which is also the first Integrated hybrid project (Solar BESS) for Oriana Power.

190 MWh C&I order secured for hybrid projects (Solar BESS), opening new business opportunities

Signed BESPA agreements for 250 MWh of BESS capacity for Navratnas PSU

Signed BESPA agreements for 100 MWh of BESS capacity in Rajasthan

Signed BESPA agreements for 100 MWh of BESS capacity in Tamil Nadu

Signed BESPA agreements for 100 MWh of BESS capacity for Karnataka

Secured VGF worth INR ~150 Crores strengthening revenue visibility while supporting scalable growth

1

1

22

5,349

Sameer Kumar retweeted

May 23

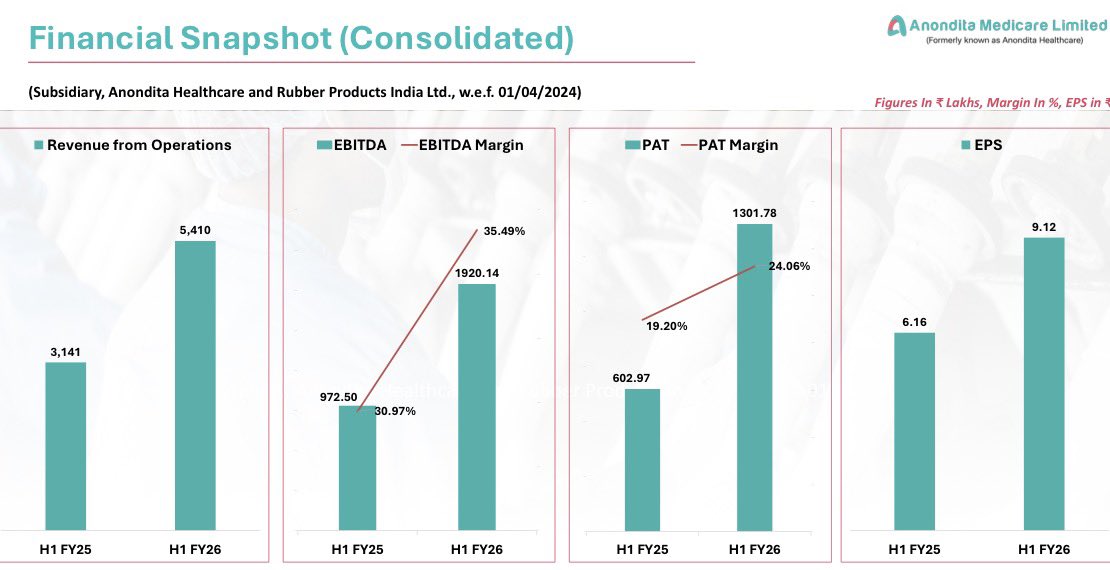

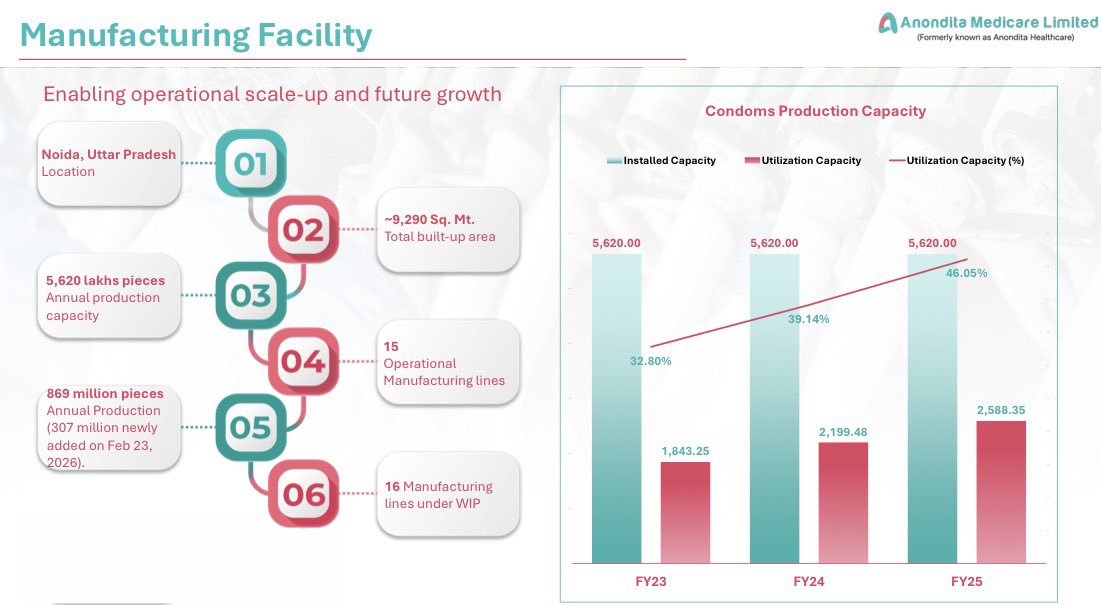

Anondita Medicare Limited (NSE SME: ANONDITA). Business Decode.

India's first MDSAP-certified condom manufacturer. Maker of the "COBRA" brand. Now scaling from a North-India led domestic player to a regulated-market exporter.

H1 FY26 Numbers (Consolidated):

Revenue at Rs. 54.10 crore. Up 72% YoY from Rs. 31.40 crore.

EBITDA at Rs. 19.20 crore. Up 97% YoY from Rs. 9.73 crore.

EBITDA Margin expanded to 35.49%. From 30.97%. 452 bps gain.

PAT at Rs. 13.02 crore. Up 116% YoY from Rs. 6.03 crore.

PAT Margin at 24.06%. From 19.20%. 486 bps gain.

EPS (Diluted) at Rs. 9.12. From Rs. 6.16. Up 48%.

H1 FY26 Standalone tells an even sharper story.

Revenue Rs. 47.65 crore. Up 91% YoY.

EBITDA Rs. 16.79 crore. Up 216% YoY at 35.23% margin.

PAT Rs. 11.47 crore. Up 306% YoY at 24.06% margin.

EPS Rs. 8.14. Up 167% YoY.

For context. FY25 Consolidated did Rs. 76.99 crore revenue, Rs. 25.65 crore EBITDA, Rs. 16.50 crore PAT. H1 FY26 alone is already trending toward beating full-year FY25.

Capacity ramp. Annual production lifted to 869 million pieces. 307 million newly added on Feb 23, 2026. 16 manufacturing lines under WIP.

Capacity utilisation at 46.05% in FY25. Up from 32.80% in FY23 and 39.14% in FY24. Operating leverage kicking in.

Margin expansion of 452 bps at EBITDA and 486 bps at PAT level. Pricing power and scale are both flowing through.

The export-led repositioning:

MDSAP certification received under ISO 13485:2016. Single-audit access to Australia, Brazil, Canada, Japan and USA. Issued by DQS Medizinprodukte GmbH. Anondita is India's first condom manufacturer with this credential.

SABS certification under SANS 4074:2017 for natural rubber latex male condoms. Effective Jan 07, 2026. Unlocks South Africa and Africa-focused tenders.

Shortlisted for South African government supplies. Agreement under finalisation.

Kenya tie-up with overseas partner for COBRA brand. Trial orders received.

UNFPA pre-qualification in advanced stage for female condoms. Targeted export launch end-FY26 or Q1 FY27.

The female condom angle:

Only company in India holding a universal patent for female condom manufacturing.

Female condom unit economics are very different. Roughly USD 2.5 per unit vs USD 0.12 for male condoms. Roughly 20x value per unit.

UNFPA procures approximately 6 million female condoms annually. Globally institutional buyers absorb 1.5 to 2 billion condoms a year.

Additional Noida unit. Incremental capacity 1,360 million pieces per annum.

Project cost ~Rs. 75 crore. Funded via internal accruals and debt.

Existing 869 million pieces plus the new block roughly triples the production base.

Cash and Bank Balance Rs. 36.51 crore.

Long Term Borrowings Rs. 13.07 crore. Short Term Borrowings Rs. 17.73 crore. Total Debt Rs. 30.80 crore.

Net cash positive at H1.

Shareholders Funds Rs. 109.97 crore. Capital Work in Progress Rs. 15.22 crore.

Global condom market Rs. USD 11.9 billion in 2025. Projected USD 17.57 billion by 2032 at 8.10% CAGR.

India market USD 406 million FY24 to USD 773 million FY33 at 7.45% CAGR.

Male condoms hold 95% plus share in India. Non-latex alternatives growing at 10.56% CAGR.

Only 8% of Indian women currently use condoms. The headroom is structural.

HLL Lifecare divestment opens up domestic institutional share to organised private players.

2026 Add female latex manufacturing facilities.

2027 Commence female latex condom production.

2028 Male and female non-latex condoms.

2029 Captive latex plantation for backward integration.

2030 Diversify into medicines and surgical healthcare.

A SME-listed condom manufacturer running at sub-50% utilisation, expanding capacity 3x, exiting H1 FY26 with 35% EBITDA margins, sitting net cash, holding India's first MDSAP credential, the only universal patent on female condoms, and an Africa export pipeline that has just started landing trial orders.

Disclaimer: This post is for educational purposes only and not a recommendation to buy or sell any securities.

9

26

6,939

Sameer Kumar retweeted

May 22

From330cr mcap to 749cr

16 Jun 2025

Self note :

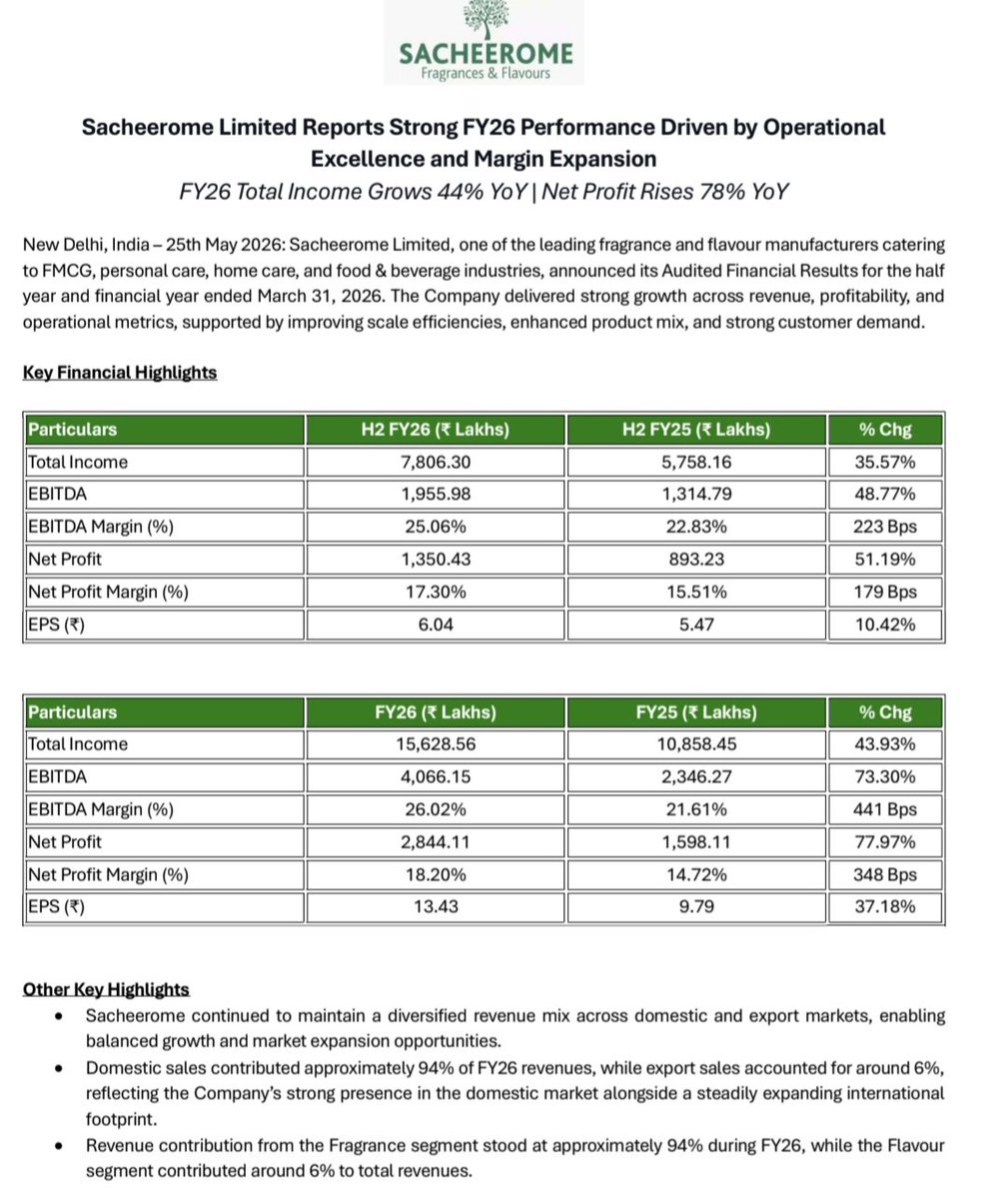

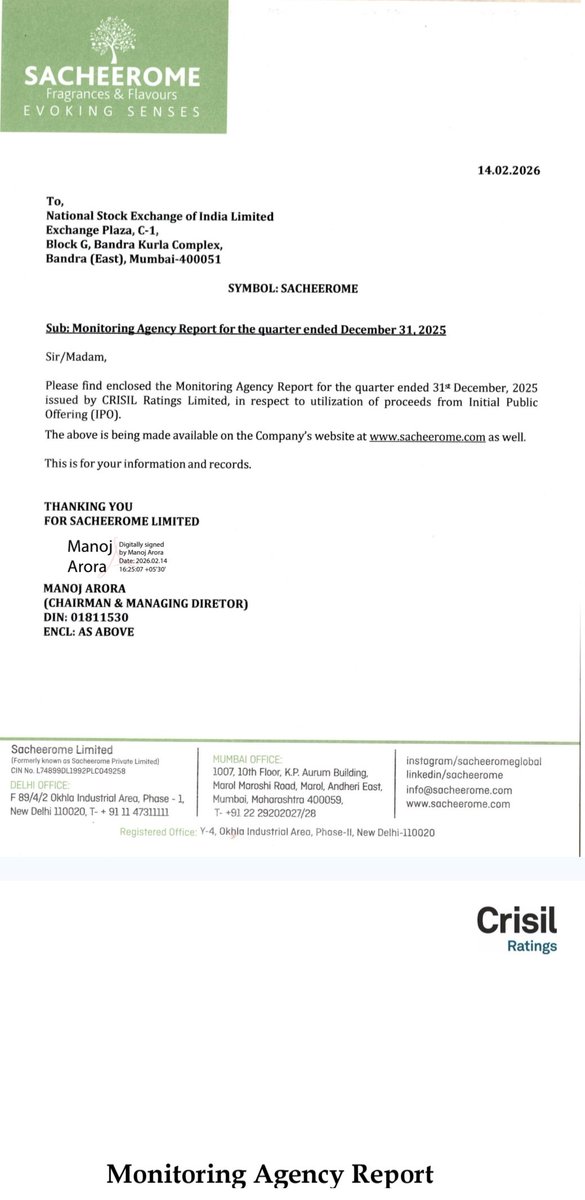

Sacheerome - #Sacheerome

Top notch customers:

ITC,Dabur,Emami,Cavinkare, Himalaya

Listed at an attractive valuations 20x ,Debt free,operationally efficient

3.6x expansion to be operational from Q4 FY26.

Less competition= scarcity premium

2

15

1,753

May 18

India ethanol market is estimated to be valued at US$ 3.28 Bn in 2025, and is expected to reach US$ 9.31 Bn by 2032, exhibiting a compound annual growth rate (CAGR) of 16.1% from 2025 to 2032.

Some of the popular names comes in Ethanol sector as below.

Balrampur Chini Mills

Shree Renuka Sugars

EID Parry

Bajaj Hindusthan Sugar

Trualt Bioenegy

This is for educational purpose only.

Disc: No buy/sell recommendation

#ethanol

1

36

May 16

Excellent update. Concall was great.

Thanks @amurfalcon1 for sharing the details.

May 15

Purple United -Concall

Future looks bright

Management-In next 2 yrs v can easily double our rev 100% on YoY basis

Targeting 200stores in fy27

Fy25-43stores

Fy26-111stores

Employee count has grown by more than 250% in last one yr

Full Concall here youtu.be/6rjQcb-Ilzc?si=vRTO…

24

Sameer Kumar retweeted

May 14

#SME #MSafe #MsafeEquipments

MSafe Equipments H2 FY26 Concall Highlights:

👉FY27 & Future Outlook:

▫️50% CAGR guidance maintained for revenue, driven by new capacity commissioning, formwork expansion, increasing rental penetration, and new product introductions.

▫️Long-term vision (4-5 years): 50-70% CAGR with potential to become one of the top-3 players in aluminium formwork segment.

💠Core scaffolding business: ~20% growth expected in FY27.

💠Steel scaffolding (sale rental combined): multi-fold jump from ~₹5 Cr in FY26 to ₹25-40 Cr in FY27 (5-10x potential).

💠Aluminium formwork: modest first-year target of ₹30-40 Cr in FY27 (production start by June end); multi-fold scaling from FY28 onward.

💠Overall revenue: ~50% growth implied; aluminium scaffolding capacity addition to support further ramp-up to ₹4 Cr/month sale ₹4.5 Cr/month rental post-expansion

▫️Margins:

💠EBITDA % may moderate slightly due to product-mix shift (more steel sales at 5-6% Gross Margins formwork at 10-15% Gross Margins vs high-yield aluminium rental)

💠Absolute EBITDA/PAT expected to grow.

💠Management targeting to maintain overall high profitability levels through operating leverage and rental focus. PAT margins built on rental-led model.

👉Current Utilization / Deployment & Future Pipeline:

▫️Steel scaffolding: Capacity expanded to 62.85 lakh units (doubled ahead of schedule)

💠Currently at peak utilization (factory running 24x7, jam-packed)

💠Revenue run-rate: ~₹1 Cr/month rental ~₹1 Cr/month sale (70% rental deployment, 25-30% sale)

▫️Aluminium scaffolding: Current run-rate ~₹3 Cr/month sale ₹3.5 Cr/month rental

💠Further expansion (10 lakh units) via new factory — partial start Dec 2026, full by May 2027.

💠Current scale: Operating across ~1,000–1,500 construction/infra sites with ~2,500 customers (pan-India from Coimbatore to Guwahati); 18 company-owned warehouses

▫️Formwork pipeline: Machinery orders placed; production commencement expected by June end FY27.

💠Market gap significant (largest player KNEST >₹2,000 Cr; multiple players in ₹500-1,000 Cr band).

💠Company targeting top-3 position in 2-3 years via rental sale hybrid model.

💠Future pipeline drivers: Infra spending, safety compliance push, shift from bamboo/unorganized to organized players; cross-selling to existing customer base; warehouse density increase to 250 km radius coverage across India.

👉Other Notable Points:

▫️Rental business model — core strength:

💠Steel yield 32-38% p.a., aluminium yield 60-66% p.a.

💠Average rental tenor ~4-5 months (aluminium) / ~1 year (steel).

💠Full supply chain control (manufacturing to rental) enables superior yields vs local/regional players

👉Commodity inflation / raw material cost management:

▫️Sales side: Zero impact — very short order book (max 7 days).

💠Full and immediate pass-through of aluminium/steel price increases or decreases to customers

▫️Rental side:

💠Rentals harder to raise, so company absorbs a small portion; however, rental margins have substantial buffer.

💠Management is driving operational efficiencies to protect yields.

👉Long-term structural advantage:

💠Assets depreciated 15% p.a. (fully written off in 5 years in books, negligible book value)

💠Physical/scrap value continues to rise with metal prices. Even after 5-6 years, scrap realization can recover ~50% of original cost (company is “price positive” on aluminium inventory and partially on steel)

👉Gross margins (product-wise):

💠Aluminium sales ~30%, steel sales 5-6%, formwork expected 10-15% (with rental upside).

💠Aluminium inventory revaluation benefit from 40-50% price rise not fully reflected in books.

👉Capex & funding:

💠~₹130 Cr planned in FY27 (including rental asset build machinery)

💠IPO proceeds — 11% already deployed, balance in FY27. Currently near debt-free (net cash ~₹4-5 Cr); debt will rise but expected to be retired within 3 years via strong internal accruals

👉Balance sheet & risk: Bad debts <2% over 6 years (in-house family-led collection team, 1-3 months rental advance security cheques).

💠Strategic moves: Entry into aluminium formwork marks shift to “integrated structural equipment solutions” company

💠Industrial safety products trading division deferred (leverage existing 2,500 customers/sites later).

💠Pan-India organized player advantage vs fragmented local competition.

💠Other: 20 years experience; no channel partners (direct to contractors/developers except planned for industrial ladders)

💠High factory labour attrition but stable admin/sales team

2

2

25

13,998

May 14

Excellent Analysis @ayushmarda07 .

May 13

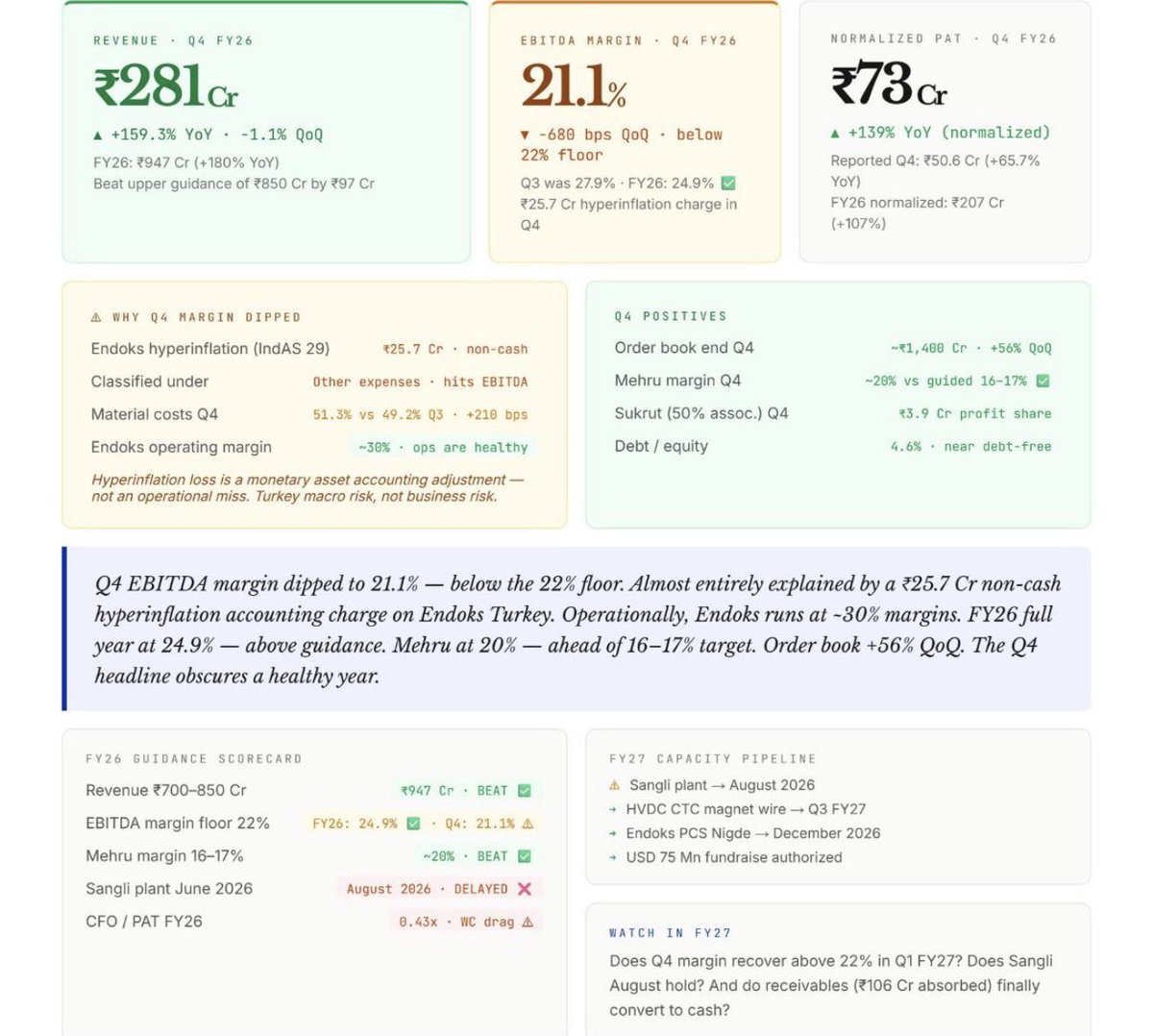

Quality Power Proxy Play to Power , Renewables , AI & Data Center Themes

Solid Q4 FY 26

Management had guided for nearly ₹900 Cr topline and ~22% EBITDA margins, but the company delivered nearly ₹1000 Cr topline with ~24% EBITDA margins.

A lot of people are saying margins have fallen, but they are not understanding the results properly.

The issue is mainly due to the Turkey subsidiary (Endoks), where hyperinflation accounting created a loss impact. Adjusting that, EBITDA and PAT would have been even better.

So overall, margins are completely fine and management has clearly walked the talk.

Now the key thing to watch will be their commentary on data center-related orders in the concall.

At current numbers, TTM PE comes around ~44x if you adjust the Turkey hyperinflation loss (~₹26 Cr).

Another positive thing is that the company turned PAT positive in FY25 despite all these issues.

Most people on Twitter do not know how to properly read results.

No recommendation.

@compoundingaiin

31