Joined August 2015

- Tweets 8,931

- Following 493

- Followers 3,271

- Likes 5,275

934 Photos and videos

Pinned Tweet

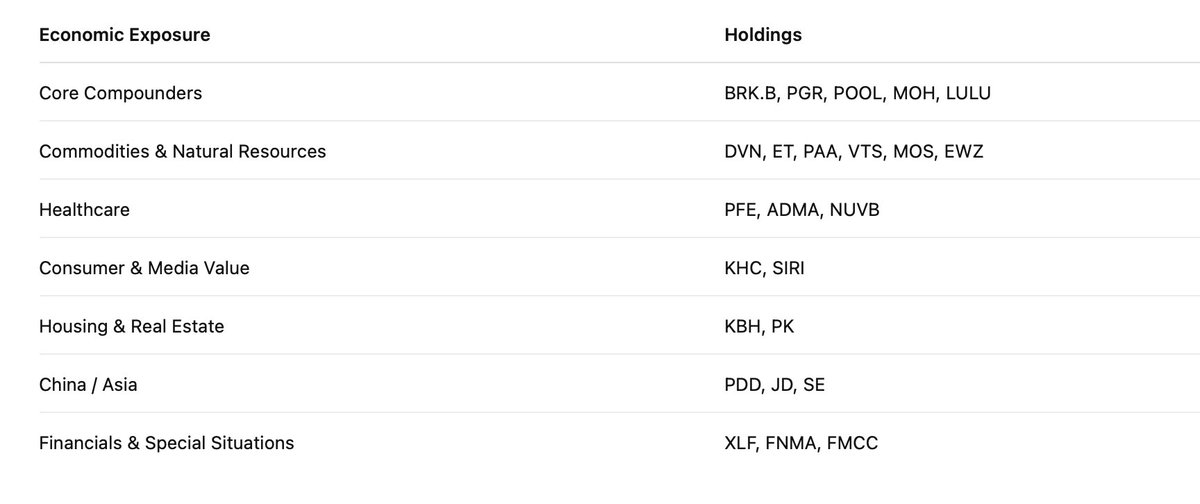

Portfolio Update:

I've been avoiding the high-flying mega-cap starting 2025 December. But that does not mean I stopped buying. Instead, I am opting for cash-generation, asset-heavy businesses, and deeply mispriced cyclical / regulatory plays.

1. Core Compounder: ($BRK.B , $PGR , $POOL , $MOH , $LULU ): Berkshire Hathaway provides defensive diversification, Progressive is a best-in-class underwriter, and Pool Corp dominates its distribution niche. Lululemon adds a high-margin consumer growth element that has faced compressed valuations recently. And $MOH, well, thanks to good ol regulatory news and aftermarket selloff. I was able to accumulate below $120.

2. Commodities & Natural Resources ($DVN , $ET , $PAA, $VTS, $MOS, $EWZ): I do have a macro bet on hard assets, energy infrastructure, and inflation protection. By holding midstream MLPs like Energy Transfer and Plains All American, I plan on locking in high, fee-based distribution yields. Devon gives me direct upstream oil/gas exposure, while Mosaic offers a cyclical play on agricultural nutrients. EWZ (Brazil ETF) adds a heavily commodity-weighted international angle.

3. Healthcare ($PFE, $ADMA, $NUVB): I have a small exposure in healthcare. I call it a mix of deep value and biotech optionality. Pfizer is a classic out-of-favor, high-yield turnaround story. ADMA Biologics represents a rapidly growing specialty plasma company, while Nuvalent is a high-conviction, targeted cancer therapy play.

4. Buffett & Dividends Play ($KHC, $SIRI): Pure, unadulterated value investing. Kraft Heinz is a slow-growth, stable cash-flow giant with strong brand equity. Sirius XM is a heavily shorted, high-free-cash-flow business that has been undergoing major corporate restructuring (via the Liberty Media merger simplification). Thanks to Warren.

5. Housing & Real Estate ($KBH, $PK): Cyclical value. KB Home captures the structural undersupply of U.S. single-family housing. Park Hotels & Resorts is a hospitality REIT levered to group travel and urban lodging recovery. If mortgage rates pull back or stabilize, KBH stands to capture significant pent-up demand, while PK relies on resilient corporate/leisure consumer spending (from worldcup, of course)

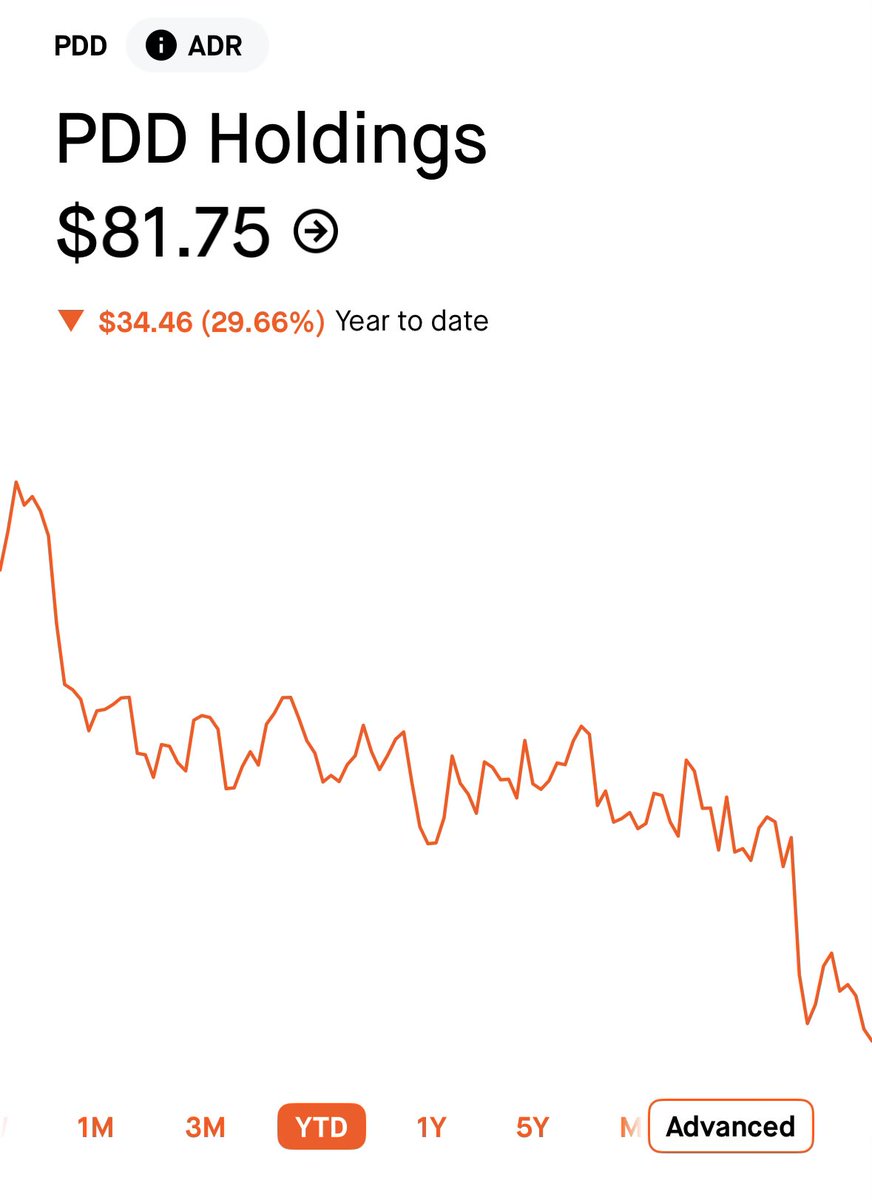

6. China / Asia ($PDD, $JD, $SE): E-commerce dominance at an extreme valuation discount. PDD Holdings (Temu/Pinduoduo) has shown staggering operational efficiency and growth, JD.com represents deep asset-heavy value, and Sea Limited offers a play on Southeast Asian e-commerce stabilization. From a fundamental perspective, the free cash flow generation here is massive relative to market cap. However, this bucket carries elevated geopolitical risk, regulatory overhangs, and macro headwinds. I've been thinking about this a lot.

7. Financials & Special Situations ($XLF, $FNMA, $FMCC): FNMA and FMCC are pure special situations. They generate billions in net income but remain stuck in government conservatorship. If a political or legal catalyst ever releases them to private capital, the upside is exponential; if not, they remain dead money. It's a textbook asymmetric value bet. The XLF gives me broad banking/financial exposure. Too big to fall is one of my favorite movies.

8. Software Steal ($NOW, $ZETA): ServiceNow is the ultimate workflow backbone of the modern enterprise. The market has hit the broader software space with some "AI disruption" anxiety over the past year, dragging $NOW down from its 52-week highs north of $210 to around the $118–$135 range. Luckily, I grabbed some around 83. Zeta, on the other hand, is my high-beta growth engine. I am happy with both, for now.

Before people start calling me out, I know I am fighting the current market momentum. Because I don't have a massive AI/mega-cap tech exposure, this portfolio will likely underperform in a speculative, liquidity-driven bull market, but it is built to heavily outperform if the market cracks or shifts toward a strict focus on tangible cash flows and low multiples. But hey, I researched all of them, and am happy holding them long-term.

And my cash reserve and $SGOV are still there. :)

7

1

20

2,369

Long River Holding retweeted

I guess Knicks fans get to burn down the city tonight. :)

Happy for them!

1

1

1

395

There's also something uniquely appealing about the idea of New York Basketball being relevant again.

I don't even root for New York, but it'd be very cool to see those NY fans finally get one.

2

139

$WU I think it's gonna be another business that's 'going through transition'

After reviewing their 10-K / 10-Q fillings, I think they are trying to push past its reliance on traditional retail remittance networks. There is definitely a slowdown in the core retail business and a great amount of pressure on volume.

They have a few massive digital and inorganic growth projects on going. The acquisition of Intermex is designed to stabilize the crucial US - LatAm corridors and deliver 30M in synergies. They are also expanding into the cryptocurrency space by launching the Digital Asset Network.

They are dealing with a contracting business, sure. But I am also seeing an improving operational leverage. Total expenses were slashed from $3,483.9M to $3,293.4M. Operating income grew 4.34% despite revenue drops, highlighting excellent gross margin protection. Debt principal was successfully paid down by $500M, structurally improving long-term leverage models.

Some might say it's a value trap. But the stock yields roughly 10% to 11%, and the company is aggressively cannibalizing its own shares (shrinking basic shares from 340.0M to 326.6M). The dividend payout remains fully covered by operating cash flow. Branded digital transactions grew by 21%, proving the digital pivot is gaining actual traction. The company maintains immense scale with $8.3 billion in assets, preventing rapid total collapse.

I think near term investment is a no-go for me. From their 2026 Q1 earnings, this is a business where share repurchases ($52.9 million) and dividends ($79.4 million) outpaced quarterly net income ($64.7 million), leading to an expanded accumulated deficit of $76.9 million. The 44.4% drop in diluted EPS to $0.20 emphasizes the near-term earnings pressure.

From a long term perspective, this is a significant cross-border platform managing $3.54 billion in daily settlement assets and obligations. While other digital-heavy competitors focus on other things, they still have a strong compliance infrastructure. The cost to maintain global Money Transmitter Licenses and Anti-Money Laundering frameworks acts as a massive barrier to entry.

It will be a prove-it story to me for the next 2-4 quarters. Until the 'Digital Asset Network' and Intermex synergies scale enough to reverse the EPS dilution, the dividend yield acts as a cushion, not a catalyst.

I am pretty neutral about this: I am waiting for a quarter where Net Income growth consistently clears the total cash payout requirement before considering a long-term position."

Happy Saturday Everyone!

1

1

6

212

Jun 13

Adobe $ADBE just became one of the most interested and debatable trades in tech, and on X, of course.

I checked another thing just to understand the market perception. 13F.

Renaissance Technologies

AQR Capital Management

Harris Associates (Bill Nygren, One of my favorite ones to read and follow)

Paul Tudor Jones,

Joel Greenblatt,

Jeremy Grantham

All these big names added Adobe last quarter. Different strategies, Different time horizons, but Same direction.

This is rare. Because these firms don’t agree on much.

Renaissance is pure systematic signal

AQR is factor valuation discipline

Harris is deep value / compounding quality

Tudor Jones is macro momentum

Greenblatt is earnings yield / magic formula discipline

Grantham is long-cycle mean reversion

And yet they’re all leaning into the same name.

Right now, Adobe is still sitting in a weird narrative gap: AI disruption fear is valid. Executive departure raises concerns.

But underneath that, subscription cash flows remain highly durable. Switching costs are still extreme. AI is more augmentation than replacement (so far) Their margins remain structurally high vs most of software.

I feel good about my position. Thanks to pre-market and after-market panic selling. :)

7

4

61

6,563

Jun 13

$PGR Even though there are some insider selling activities. These executives have retained the vast majority of their equity.

When an executive "dumps" stock (a truly bearish signal), you typically see them selling 50% to 100% of their holdings, or a complete exit. Here, they are maintaining significant "skin in the game."

My heavy-accumulation target is around $168 or lower. :)

Happy Friday everyone.

7

711

Jun 12

And they say it’s gonna grow exponentially.

Jun 12

Meta, $META, to crack down on employee token use, per The Information.

1

1

2

1,076

Long River Holding retweeted

Jun 10

1

6

1,786

Jun 12

$WU do we still have faith in this company? It’s severely undervalued now.

To me, western Union is a classic "melting ice cube." It generates tremendous free cash flow, but the cost to acquire and retain revenue is rising.

Management is attempting to transition to digital and stablecoin rails, but this transitions them from a monopoly-like analog network to a highly commoditized digital battlefield against structurally cheaper operators. The $2.6 billion debt load acts as an anvil if revenues contract faster than 5% annually.

Btw it’s near all time low and down ~60% since its IPO. Lol.

2

4

573

Long River Holding retweeted

Sirius XM Holdings $SIRI will replace Masimo $MASI in the S&P MidCap 400 effective prior to the opening of trading on Thursday, June 11.

Danaher $DHR is acquiring Masimo in a deal expected to be completed soon pending final conditions.

Exciting news for fellow $SIRI holders.

1

5

1,183

Jun 11

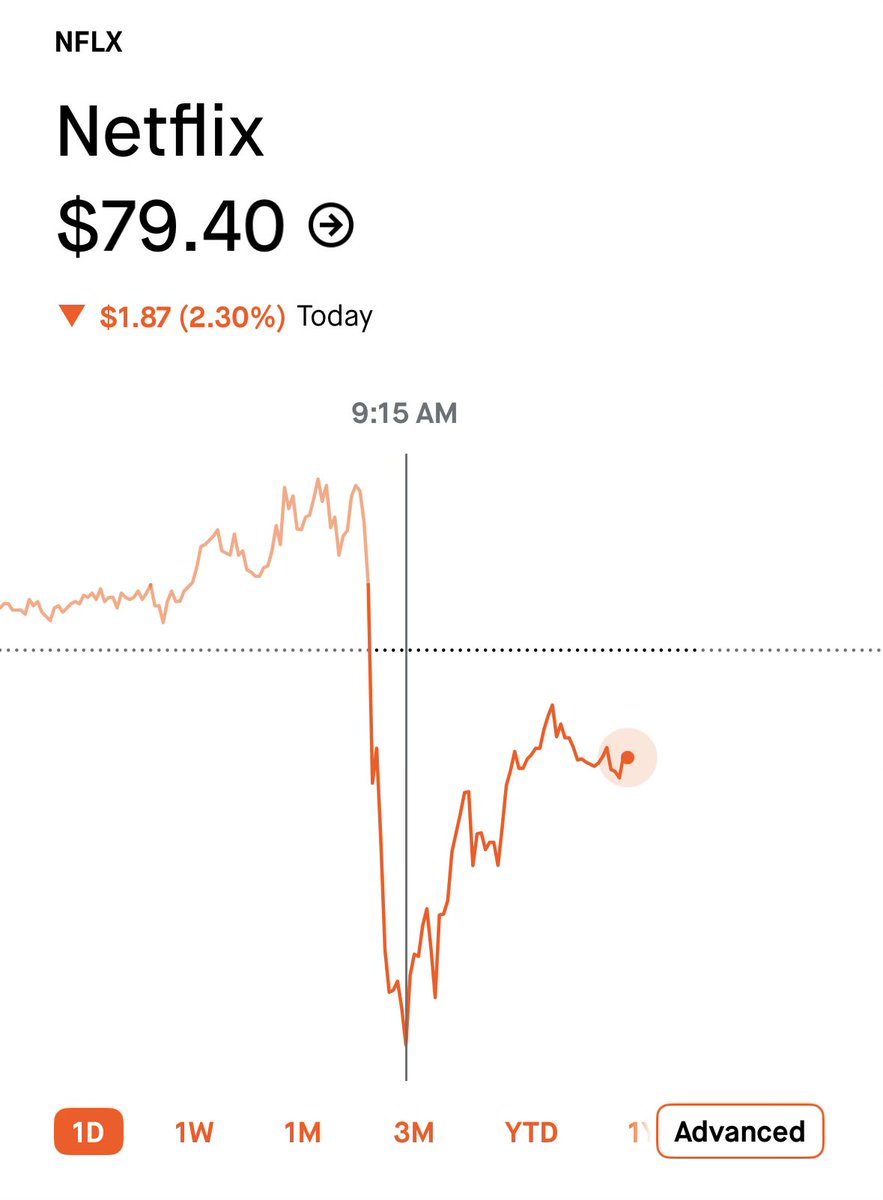

Adding $NFLX on my watchlist as well. I think $75 will be a lovely price for me to start a position. Hope it'll get there. :)

6

14

3,047

Jun 11

I really don't think $ADBE will be the next 'Kodak' or 'Nokia'

Files like .psd, .ai, and .pdf are the universal languages of global commerce. When an agency creates a campaign, it must be handed off to printers, developers, and the market team who all rely on Adobe's file formats. You can't disrupt a standard that the entire global creative industry relies on for interoperability.

As businesses fear AI-related copyright lawsuits, Adobe has built a massive moat by training its Firefly models exclusively on licensed or proprietary data. For a Fortune 500 company, that indemnification is more valuable than a "cool" AI feature from a scrappy, unlicensed startup.

Just something I think its important. :)

16

1

74

7,372

Portfolio Update:

I've been avoiding the high-flying mega-cap starting 2025 December. But that does not mean I stopped buying. Instead, I am opting for cash-generation, asset-heavy businesses, and deeply mispriced cyclical / regulatory plays.

1. Core Compounder: ($BRK.B , $PGR , $POOL , $MOH , $LULU ): Berkshire Hathaway provides defensive diversification, Progressive is a best-in-class underwriter, and Pool Corp dominates its distribution niche. Lululemon adds a high-margin consumer growth element that has faced compressed valuations recently. And $MOH, well, thanks to good ol regulatory news and aftermarket selloff. I was able to accumulate below $120.

2. Commodities & Natural Resources ($DVN , $ET , $PAA, $VTS, $MOS, $EWZ): I do have a macro bet on hard assets, energy infrastructure, and inflation protection. By holding midstream MLPs like Energy Transfer and Plains All American, I plan on locking in high, fee-based distribution yields. Devon gives me direct upstream oil/gas exposure, while Mosaic offers a cyclical play on agricultural nutrients. EWZ (Brazil ETF) adds a heavily commodity-weighted international angle.

3. Healthcare ($PFE, $ADMA, $NUVB): I have a small exposure in healthcare. I call it a mix of deep value and biotech optionality. Pfizer is a classic out-of-favor, high-yield turnaround story. ADMA Biologics represents a rapidly growing specialty plasma company, while Nuvalent is a high-conviction, targeted cancer therapy play.

4. Buffett & Dividends Play ($KHC, $SIRI): Pure, unadulterated value investing. Kraft Heinz is a slow-growth, stable cash-flow giant with strong brand equity. Sirius XM is a heavily shorted, high-free-cash-flow business that has been undergoing major corporate restructuring (via the Liberty Media merger simplification). Thanks to Warren.

5. Housing & Real Estate ($KBH, $PK): Cyclical value. KB Home captures the structural undersupply of U.S. single-family housing. Park Hotels & Resorts is a hospitality REIT levered to group travel and urban lodging recovery. If mortgage rates pull back or stabilize, KBH stands to capture significant pent-up demand, while PK relies on resilient corporate/leisure consumer spending (from worldcup, of course)

6. China / Asia ($PDD, $JD, $SE): E-commerce dominance at an extreme valuation discount. PDD Holdings (Temu/Pinduoduo) has shown staggering operational efficiency and growth, JD.com represents deep asset-heavy value, and Sea Limited offers a play on Southeast Asian e-commerce stabilization. From a fundamental perspective, the free cash flow generation here is massive relative to market cap. However, this bucket carries elevated geopolitical risk, regulatory overhangs, and macro headwinds. I've been thinking about this a lot.

7. Financials & Special Situations ($XLF, $FNMA, $FMCC): FNMA and FMCC are pure special situations. They generate billions in net income but remain stuck in government conservatorship. If a political or legal catalyst ever releases them to private capital, the upside is exponential; if not, they remain dead money. It's a textbook asymmetric value bet. The XLF gives me broad banking/financial exposure. Too big to fall is one of my favorite movies.

8. Software Steal ($NOW, $ZETA): ServiceNow is the ultimate workflow backbone of the modern enterprise. The market has hit the broader software space with some "AI disruption" anxiety over the past year, dragging $NOW down from its 52-week highs north of $210 to around the $118–$135 range. Luckily, I grabbed some around 83. Zeta, on the other hand, is my high-beta growth engine. I am happy with both, for now.

Before people start calling me out, I know I am fighting the current market momentum. Because I don't have a massive AI/mega-cap tech exposure, this portfolio will likely underperform in a speculative, liquidity-driven bull market, but it is built to heavily outperform if the market cracks or shifts toward a strict focus on tangible cash flows and low multiples. But hey, I researched all of them, and am happy holding them long-term.

And my cash reserve and $SGOV are still there. :)

7

1

20

2,369

Jun 11

Opened up a small position of $ADBE, avg price of $208 or below. Thanks to after market sell off.

3

225

Jun 11

$ADBE I am adding it here after market. Below 210 seems like a sweet spot.

Adobe achieved record revenue of $6.62 billion in its second quarter of FY2026, which represents 13% year-over-year growth, or 11% in constant currency.

Diluted earnings per share was $4.25 on a GAAP basis and $5.96 on a non-GAAP basis. GAAP results reflect a $0.17 per share non-cash goodwill impairment charge related to the Publishing & Advertising reporting unit.

Total Adobe Annualized Recurring Revenue (“ARR”) exiting the quarter was $27.10 billion, including approximately $480 million from Semrush.

GAAP operating income in the second quarter was $2.24 billion and non-GAAP operating income was $2.95 billion. GAAP net income was $1.71 billion and non-GAAP net income was $2.40 billion.

Cash flows from operations were $2.17 billion.

Exiting the quarter, Remaining Performance Obligations (“RPO”) were $22.27 billion, and Current Remaining Performance Obligations (“cRPO”) were 67%.

Adobe repurchased approximately 8.5 million shares during the quarter.

2

1

37

2,816

Jun 11

I am officially adding $ADBE on my watchlist. I think the valuation is very attractive, and they will have a way to co-exist with AI.

3

20

1,784

Long River Holding retweeted

May 28

2

2

1,025