4,860 Photos and videos

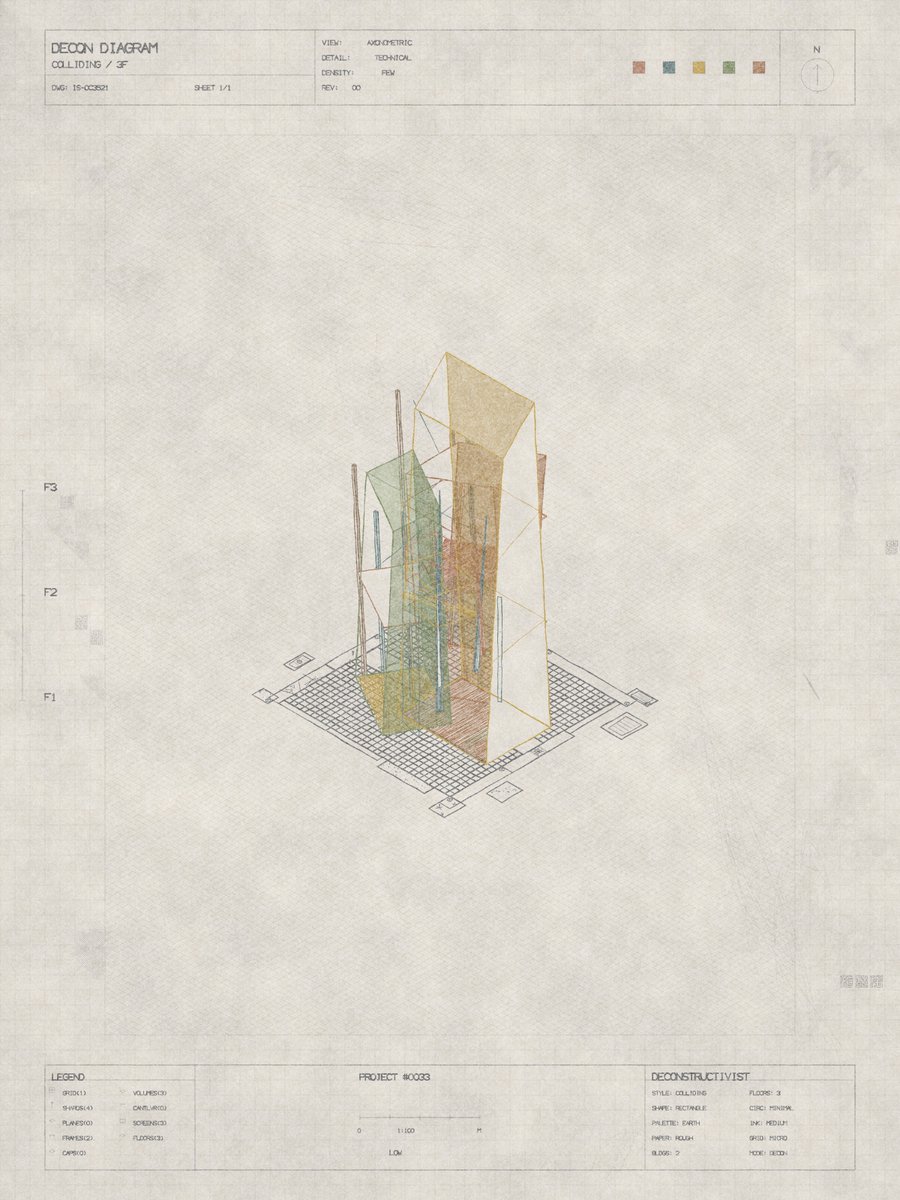

In just 2 hours, Ryokan launches (with @shape and @Highlight_xyz).

At 10:00pm GMT 1 (4:00pm EST, 1:00pm PST), the ten pieces will open for bidding.

A manifesto accompanies the collection, explaining the process, the philosophy, and the intent behind it.

Infos and links ↓

8

13

87

15,279

Mannay 🌹 retweeted

Jun 13

Jun 13

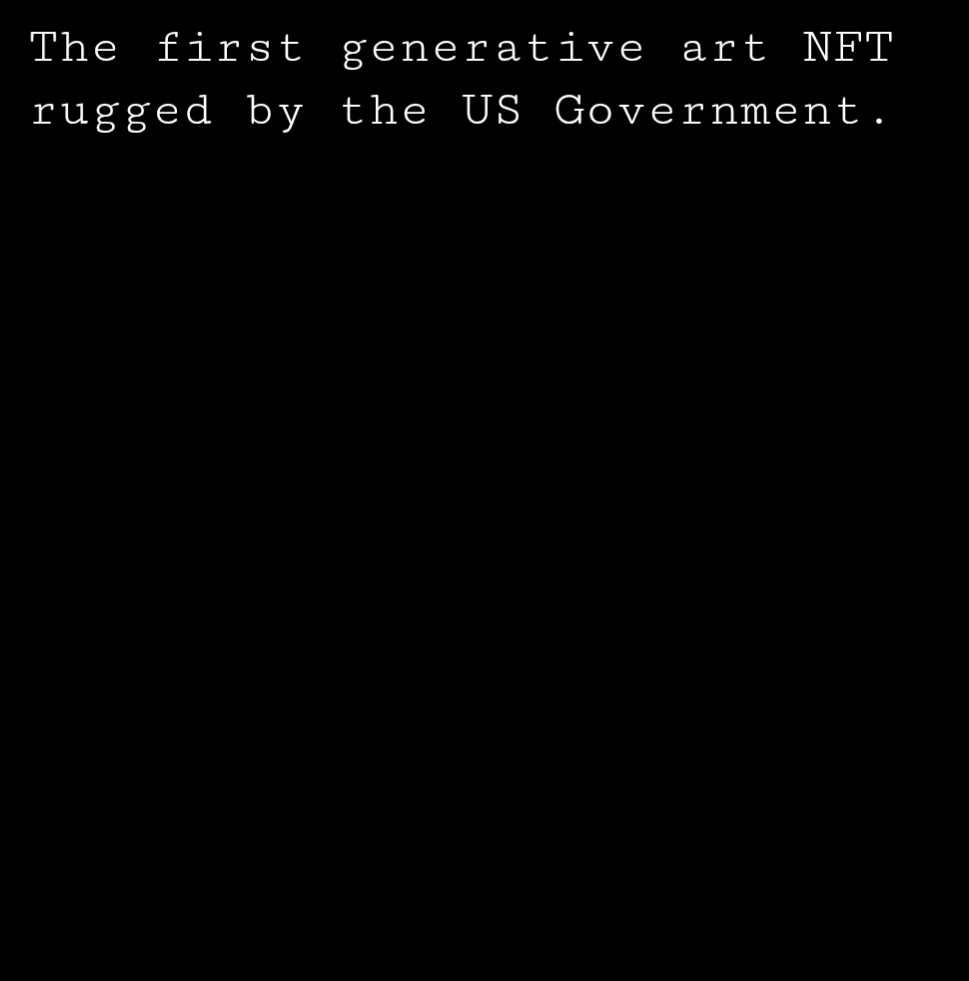

The US government, citing national security authorities, has issued an export control directive to suspend all access to Fable 5 and Mythos 5 by any foreign national, whether inside or outside the United States, including foreign national Anthropic employees.

The net effect of this order is that we must abruptly disable Fable 5 and Mythos 5 for all our customers to ensure compliance.

Access to all other Claude models is not affected.

We apologize for this disruption to our customers. We believe this is a misunderstanding and are working to restore access as soon as possible.

Read our full statement: anthropic.com/news/fable-myt…

3

4

73

4,184

Not an art thread this time. Over the past few days, while readjusting my crypto portfolio—and noticing how everyone’s glued to the US elections or speculating on meme coins—I decided to dig a bit deeper into Michael Saylor and MicroStrategy’s (MS) plans. Saylor has obviously become something of a superstar in the crypto space, but I realized many might not fully understand how MicroStrategy’s strategy works, or the significant risks it involves. Thought it would be worth sharing my perspective on it.

Right now since MS started its aggro strategy in 2020 it owns more than 250,000 Bitcoins in its reserves, accounting for roughly 1.2% of all Bitcoin. To achieve this level of BTC acquisition, MS has taken on nearly $4 billion in debt through convertible bonds and other financial instruments (obviously tying the company to BTC value). While obviously profitable during the bull (and an obvious catalyst for it), i don't see anyone talking about the risks particularly with a crucial $650 million debt due in December 2025.

In December 2025, MS's investors will decide whether to reclaim their cash or convert their bonds to company shares, which depends heavily on BTC's price. If BTC's value remains high, investors might convert to shares, relieving MS's cash burden. But if BTC's price falls, MS could be forced to repay in cash, putting a gigantic pressure on its liquidity. So If faced with a cash shortfall, MS may be forced to sell part of its Bitcoin holdings, which could completely flood the market, driving BTC price down further. I mean everyone's happy with Sailor and all but the strategy doesn't seem sustainable to me, looks like a bubble or am i missing something? It could lead to a pretty dangerous cycle, where the price crash would reduce MS's asset value, triggering more sales and potentially causing one of BTC largest price declines. IE. This scenario would not only impact MS but could also trigger a broader loss of confidence and a sell-off in the entire market, amplifying the price crash.

Obviously, by then, MS might come up with financial instruments—market making or liquidity services for example—to manage its exposure. However, we've seen for the past years that the market have been relying on real-world events that much that it should raise concerns. The crypto world has witnessed catastrophic failures before, from Mt. Gox to FTX, yet, for some reason, there’s minimal skepticism about Saylor’s plans, even though they seem to contradict Bitcoin’s ethos of decentralization. Unlike BlackRock’s ETFs, which offer a straightforward 1:1 Bitcoin exposure, Saylor’s strategy is built on leverage and debt, making it feel more like a bubble. If Bitcoin’s resilience is tied too closely to one corporation’s fortunes, it risks undermining the very principles that made Bitcoin revolutionary in the first place.

Looking ahead, MS's “Plan 2121”—a plan to attempt to raise $42 billion through new shares and debt to double down on Bitcoin over the next 3 years—could either cement Bitcoin’s place in mainstream finance or push it into one of its most precarious positions yet. With intentions to acquire another 1.5% of all Bitcoin, Saylor’s strategy could amplify returns if BTC thrives, but it also adds unprecedented risk if the market turns. While Bitcoin’s technology and decentralized architecture will undoubtedly endure, a crash fueled by over-leveraged corporate exposure could dramatically impact its price, shaking investor confidence and reshaping perceptions about BTC's resilience. Saylor’s approach may be remembered as either visionary or dangerously speculative, and the outcome could serve as a defining moment for BTC's journey toward widespread adoption.

1

2

8

1,093

Mannay 🌹 retweeted

May 25

It’s been a long time coming, and a true labor of love, but I’m proud to introduce The Garden.

An online gallery for digital art. Established 2026.

thegarden.art

107

80

435

31,231

Mannay 🌹 retweeted

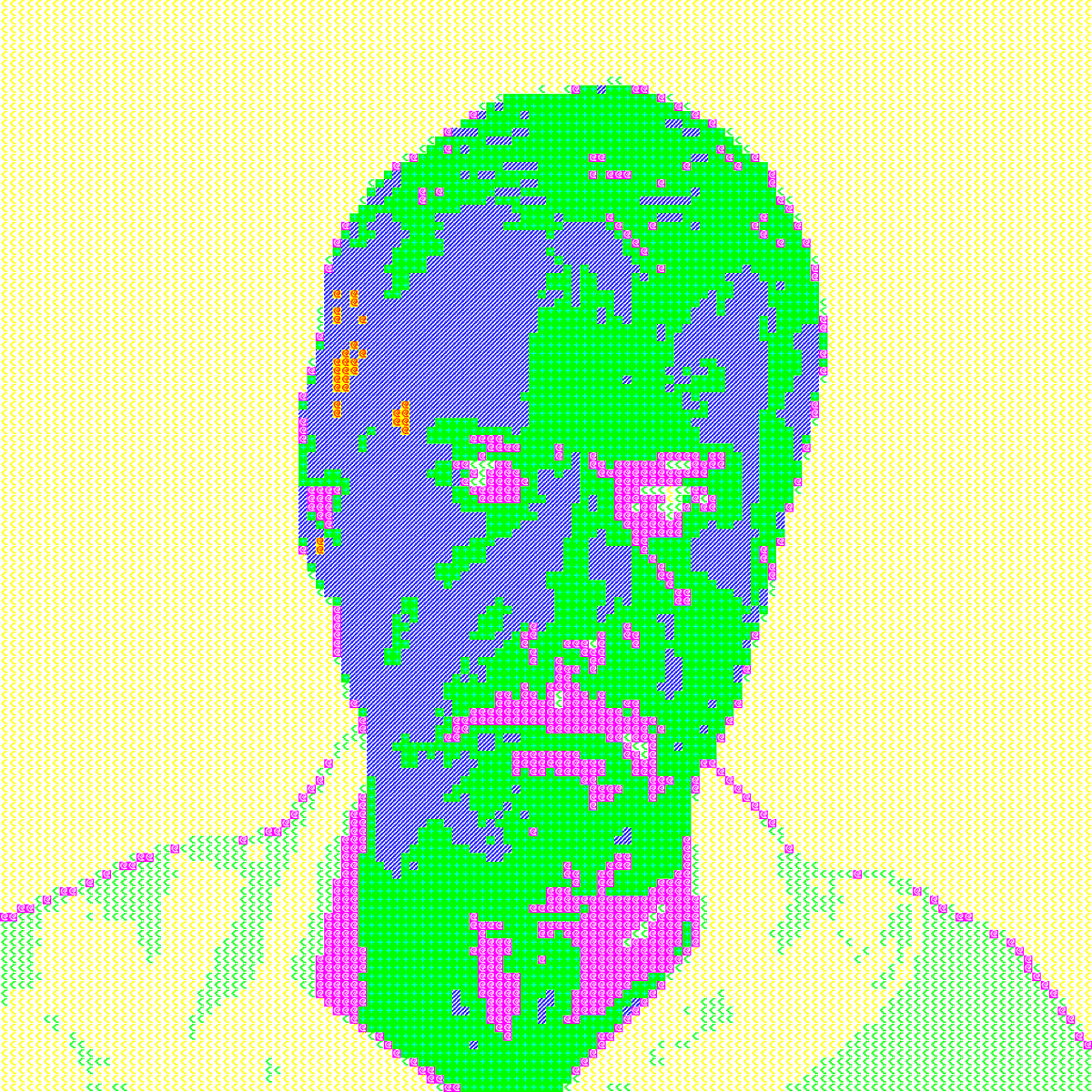

May 27

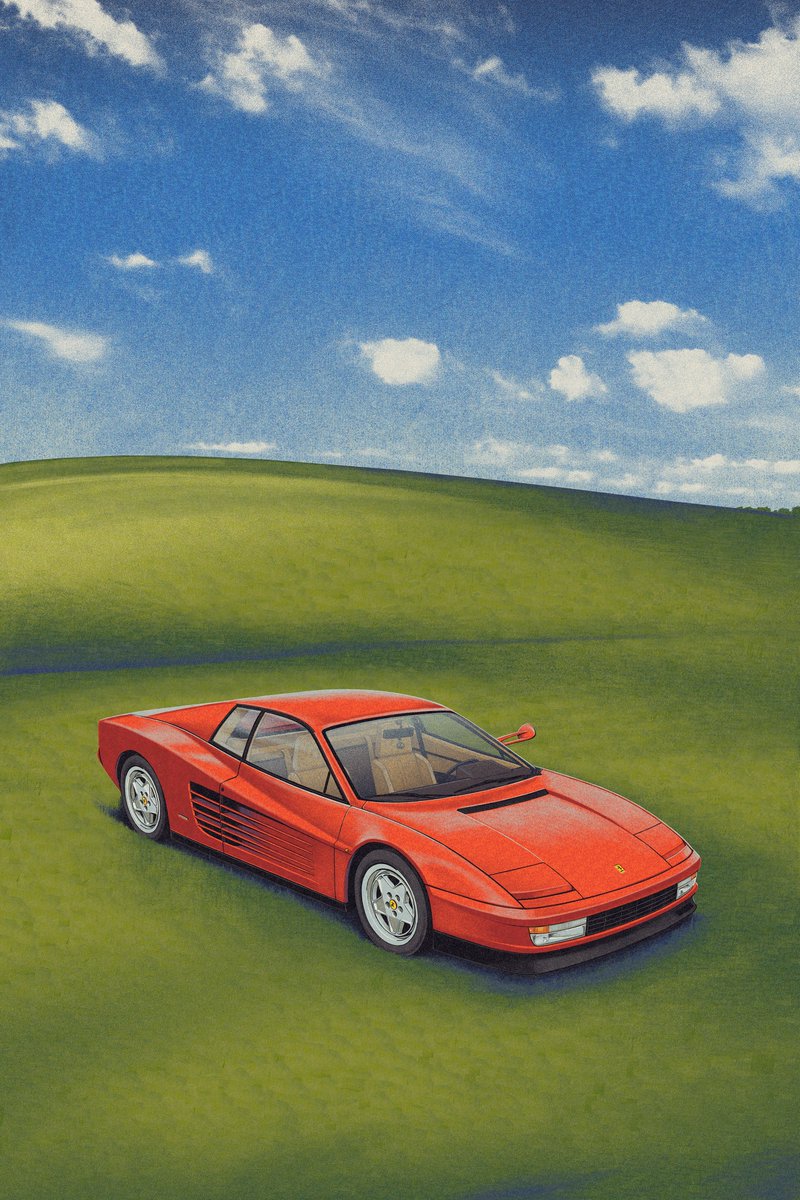

Red on Green

hand drawn digital illustration, 4646ㄨ6969pix

available on Transient with 0.069 reserve

↓↓↓

3

8

26

2,258

Mannay 🌹 retweeted

Apr 8

Hello friends!

Launching today my latest collection called "Cult of Context".

Not much to say except: I've been working hard and been eating my veggies and was kind to strangers! And It's also a very very cool project I've made!

LINK&INFO◢

23

36

181

17,526

Mannay 🌹 retweeted

May 25

zooming in

1

2

16

500

You know i've got a lot of empathy for my peers but my bs shield stays fully activated when you drop the whole "i create only to honor the miracle of the process" essay perfect grid dump after the philosophical "it's so hard" routine for pre-sale edging

it's okay to sell art. you don't need to cosplay reluctance first. sale doesn't need to arrive disguised as a moral accident

8

532

Mannay 🌹 retweeted

May 22

Meltdown’s syntax highlighter function highlighting itself and melting away…

🫠🫠🫠

29

163

1,155

41,903

From "We'd be happy with whatever we receive" to "Pretty disappointed" in a minute. Some of you can't be helped.

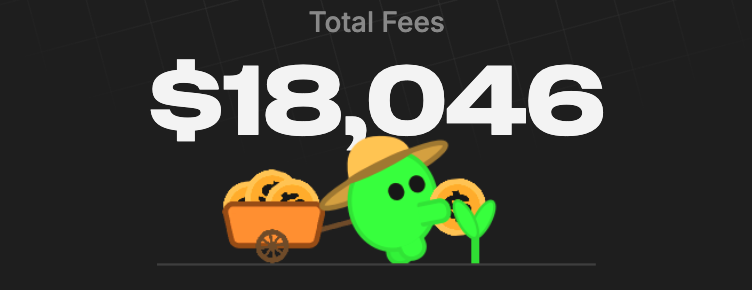

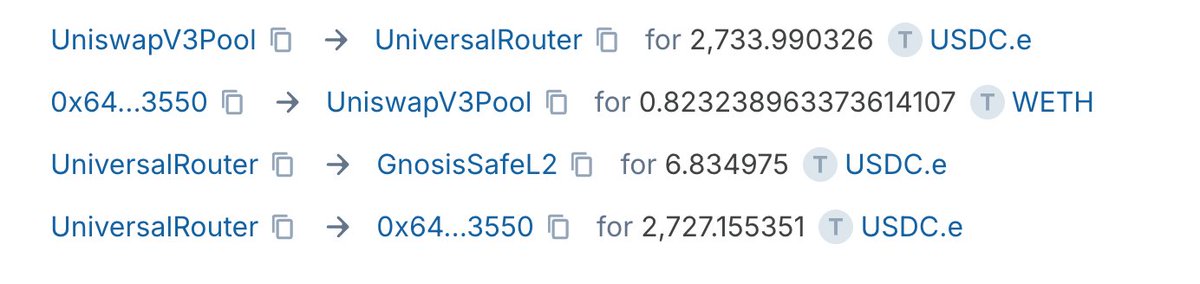

Quick maths.

$31.7M cumulative fees => 86% goes straight to LPs. That's approx. $27.3M already paid out to LPs. Protocol keeps roughly 14% that's $4.4M gross. Minus infra/ops costs/taxes. They give you $1M back on a cashdrop commit $500K in ongoing LP rewards.

They could've just kept it all and printed another worthless token instead, sure buddy.

Either way, grats @Lamboland_ & @BOBBYBIGYIELD. It just confirms further the team alignment w/ the ethos (and thanks for the stimmy) 👏

2

1

6

907

New day, new vulnerabilities.

The modern web stack is a supply-chain casino.

A giant supply-chain machine: Hundreds/thousands of packages. CI pipelines. GH Actions. npm tokens. OIDC. AI agents editing code that's not reviewed.

Now the vibe-coded app hunt begins.

Predictable.

Black hats went after WordPress because everyone used it. Now they’ll go after React/Next/npm for the same reason:

Huge surface area = huge ROI.

The problem isn't really React, it's modern JS dependency sprawl AI assisted low discipline shipping.

For teams, question is no longer "which framework is the safest?" but "How much code can hurt us?"

1

191