Massif Capital is a value-oriented investment boutique focused on real asset investing in materials, energy and industrials.

Joined June 2022

- Tweets 126

- Following 34

- Followers 1,212

- Likes 39

62 Photos and videos

12 Feb 2025

How national security priorities are rewriting global investment rules. From semiconductor wars to energy weaponization, our new paper analyzes the collision of geopolitics and finance. Essential reading for navigating structural shifts.

research.massifcap.com/p/whe…

2

9

3,116

16 Jan 2025

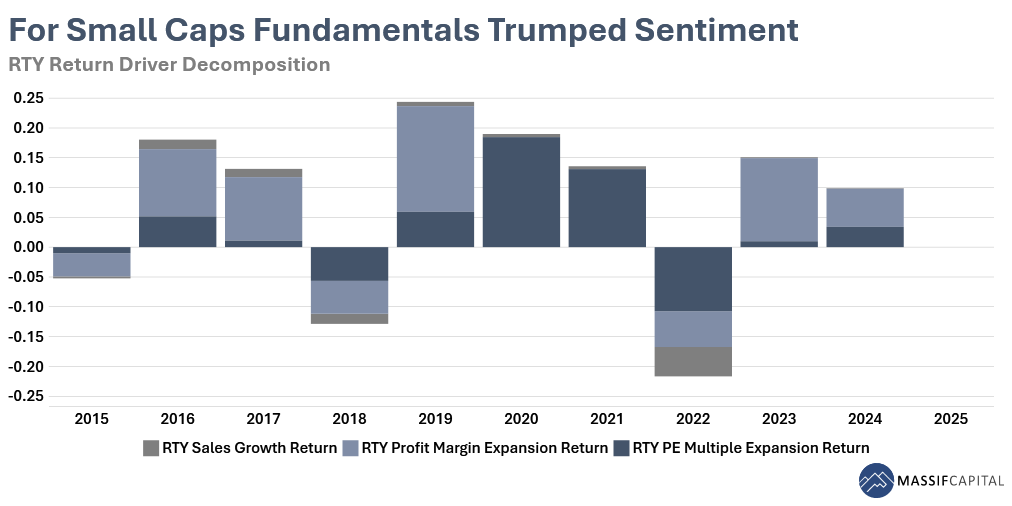

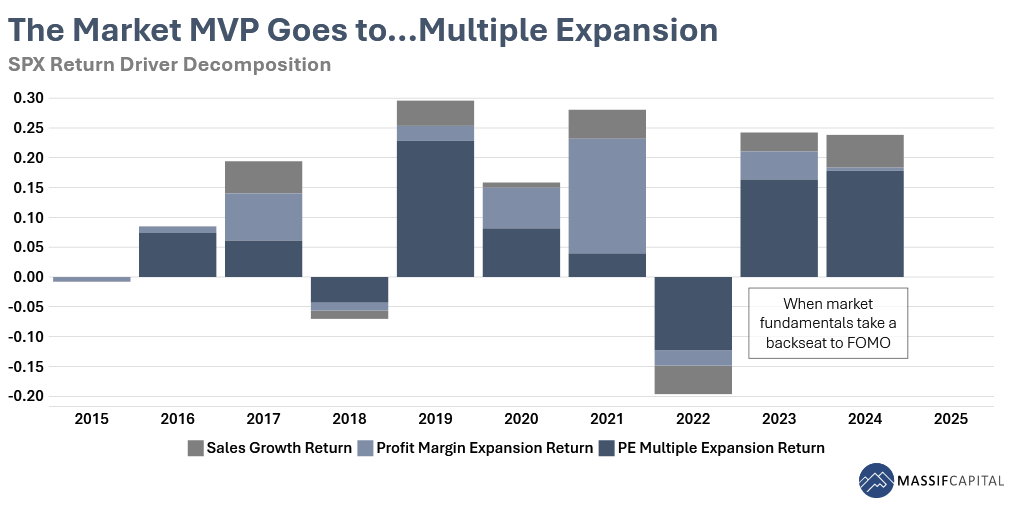

Multiple Expansion has done a lot of heavy lifting in the last two years.

1

4

1,412

massifcap retweeted

16 Jan 2025

From North Sea to global player: Harbour Energy's transformation through M&A creates a unique value proposition in the E&P sector. Dive into our analysis. research.massifcap.com/p/har…

#realassets #EnergyMarkets #Oil

2

8

1,395

massifcap retweeted

15 Jan 2025

🔥 Energy Opportunity: Harbour Energy (HBR) - Unlocking Hidden Value in European E&P. Projected 15-20% FCF yield, strategic global assets, and leadership by Linda Cook. Undervalued with 98% potential return.

research.massifcap.com/p/har…

#EnergyInvesting #realassets #oilandgas

1

5

15

4,220

26 Nov 2024

Copper is king, and Zambia is its throne. Learn why this emerging mining hub could be the next big thing for investors in our latest report. 🛠️🌍 #Copper #Investing research.massifcap.com/p/zam…

4

10

3,190

massifcap retweeted

26 Sep 2024

As soon as @massifcap published our review of the current US elections impact on Real Assets, the Harris team releases an industrial policy platform.

The campaign manager should have called to coordinate our doc release. Lucky we mainly focused on a potential Trump Admin.

research.massifcap.com/p/ano…

1

4

1,036

24 Sep 2024

Another Election, Another Non-Revolution: What Real Asset Investors Should (Not) Be Worried About.

In Massif's latest deep-dive report, we examine the presidential election and consider the potential impact of both a Trump and Harris administration.

research.massifcap.com/p/ano…

1

2

5

1,736

3 Sep 2024

Still putting up positive numbers but not an easy year, grinding it out.

1

2

554

massifcap retweeted

26 Jul 2024

Enjoyed reading @wmthomson22's letter. Thoughtful macro perspective investment theses on Enovix, Siemens Energy, and Lithium Argentina. $LAAC looks like a particularly compelling risk/reward to me.

24 Jul 2024

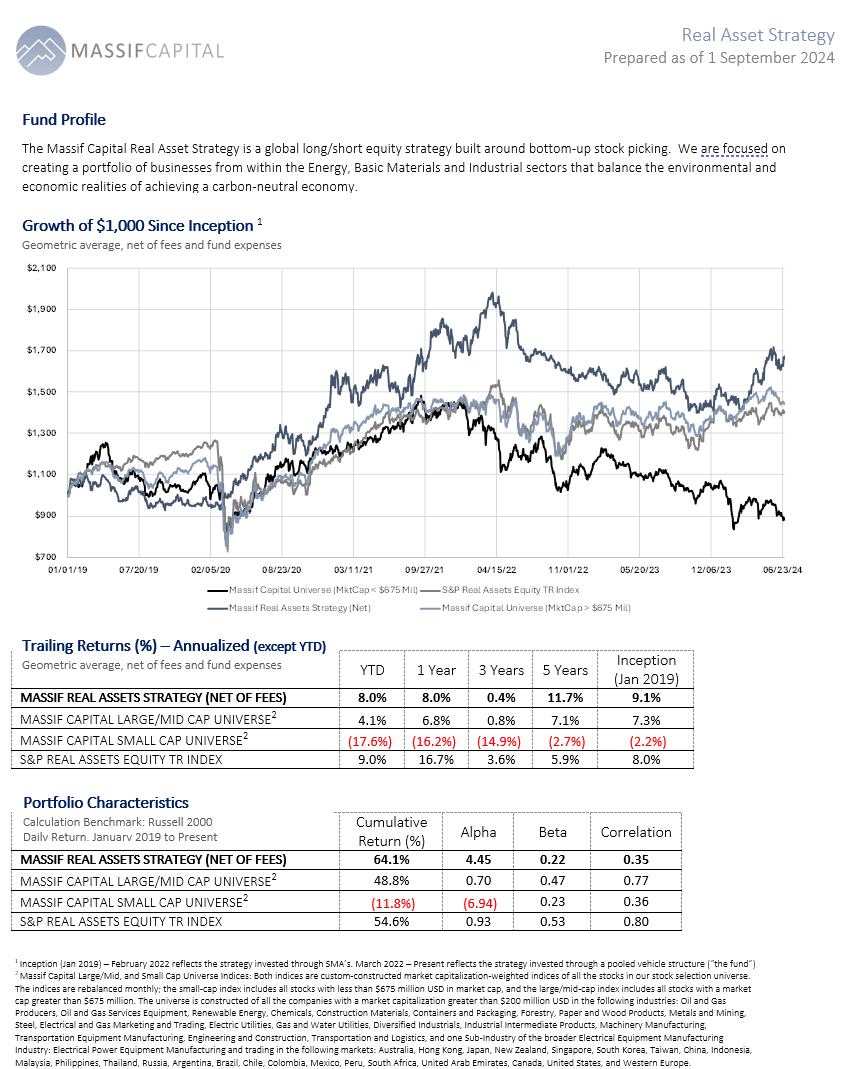

2nd Quarter 2024 Letter to Investors is out today. We discuss our good performance in the first half (up 9.4%), our investments in $ENVX and $ENR, and the importance of investment in the #realasset ecosystem for the broader economy.

research.massifcap.com/p/2nd…

3

25

5,319

massifcap retweeted

24 Jul 2024

The critical #copper question for the next 2-3 years: Which is greater, the fall in demand from the Chinese real estate sector or the growth of new demand sources (electrification, grids, EVs, AI, etc), and if greater is it sufficiently greater to offset the fall in Chinese RE.

2

11

1,180

24 Jul 2024

2nd Quarter 2024 Letter to Investors is out today. We discuss our good performance in the first half (up 9.4%), our investments in $ENVX and $ENR, and the importance of investment in the #realasset ecosystem for the broader economy.

research.massifcap.com/p/2nd…

6

24

9,200

9 Jul 2024

Our research is now available on substack as well as our website: massif.substack.com/p/the-ri…

1

1

3

630

massifcap retweeted

9 Jul 2024

New Post: The Rise of China's Solar Industry

A deep dive into how China's engineering-intensive manufacturing skills are distinct from the West's innovation skill set and crucial for product commercialization. #Manufacturing #RealAssets

research.massifcap.com/p/ris…

2

15

2,983

5 Jul 2024

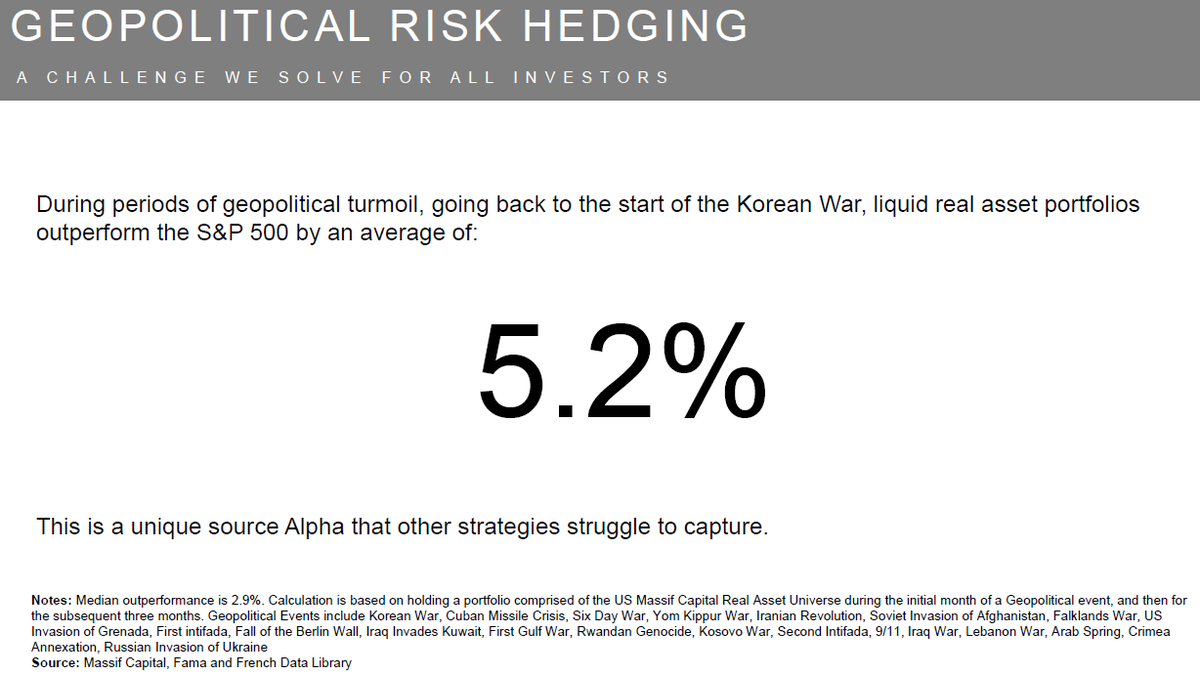

Are you concerned by growing geopolitical risk? You are not alone: ft.com/content/23ce295d-bf65…. Massif Capital focuses on geopolitical risk, which is why our liquid #realasset portfolios outperform during periods of turmoil.

1

2

578

massifcap retweeted

4 Jul 2024

Although I agree with both points, I think they are secondary to the ongoing loss of economic vitality that comes from the slow but steady loss of manufacturing capability (which despite what politicians say is not really about job losses).

At issue is the idea that the knowledge required to manufacture things is either trivial or easily acquired. While that may be true for certain goods, it is not for many energy and industrial goods, products, and processes.

China has become the best place to get an answer to the following question: How can a new product, an invention, be translated into something that can be manufactured or used profitably? That represents a significant loss of value to Western economies, even if it represents a substantial opportunity for specific companies to boost their bottom line through outsourcing (this is management teams thinking economically, but not in terms of political economy).

China is now a manufacturing powerhouse, not because of cheap factors of production; that's only where it started, but because they have mastered a highly innovative and knowledge-intensive proprietary skill set distinct from the capabilities involved in invention and innovation but no less critical.

While most of the profit for some innovations may continue to accrue to Western companies, in some instances, regardless of where the product is manufactured, this skill set has allowed Chinese firms to make inroads with their products of equal and sometimes superior quality to Western products. (See EVs, Solar).

Combined with the large domestic market, that ability to manufacture faster, cheaper, and better acts as a flywheel that enables Chinese firms to level up, enhance productivity, and build sequentially from imitator to peer and finally to leading innovator.

In the 1960s, the Soviet Union's understanding of semiconductors was on par with the US; they fell behind because our companies moved from one-off production of a value-added innovation to mass production. The manufacturing helped create an ecosystem that produced further innovation and demand for innovation…Silicon Valley.

An innovation ecosystem does not need to be co-located, and in the West, they are not, but they do depend on the free exchange of ideas, something that China does not excel at.

Returning to the case of MAN, I have no idea if their turbines represent a security threat, but I do know that China has yet to crack the code for manufacturing high-quality gas turbines. They understand the science, but that is not the same thing as being able to manufacture, for example, a turbine that can start up in 11 minutes, has a blades spinning at 3,600 RPM, in an exhaust stream that is 600c, can but turned on and off a million times and only needs to be serviced every 32,000 operating hours. Knowing the science behind that turbine is different than knowing how to build it, and we are ceding that knowledge to China right and left.

2

4

5

1,730

massifcap retweeted

4 Jul 2024

Given the scale of the Chinese market and their incredible ability to manufacture products faster, better, and cheaper, which at this point is second to none, and should not be underestimated, we will need to see more actions like this (see article below) if the West wants to prevent China from swamping our markets with industrial kit.

Gas turbine engineering is an area of significant company-level proprietary knowledge that China has struggled with. Only last year did they produce their first domestic heavy-duty F and H class turbines, classes developed in the West in the 1990s and early 2010s.

I am a strong supporter of Free Markets, but China's market scale and the CCP willingness to use economics as a tool of the state pose an interesting problem that the West has not yet figured out how to address. Until we do so, we should error on the side of caution.

Unfortunately, the management team at MAN energy solutions is not thinking holistically. Most management teams are not, they think in terms of economics not political-economy. They suggested to the German government that the turbines were not a national security issue. The implication being that we lived in a world were politics and economics could exist in nice neat silos. That is simply not the case, economic power is political power, and represents a very real tool of statecraft for the Chinese.

Germany vetoes sale of sensitive turbine unit to Chinese group on.ft.com/3zBsLxm

1

3

9

4,654

18 Jun 2024

RT @globallithium: Almost 5 years ago, as price was crashing, I said this. I didn't see the extent of the 2022 spike coming nor the rapid r…

5

massifcap retweeted

14 Jun 2024

What was the flows mechanism that prompted the Covid sell off in 2020? Panic flows at the margin? What ever mechanism was at play in 2020, something similar might be at play.

Now admittedly, I don't know what the market response to an invasion of Taiwan would be, but I would certainly want to hedge the downside risk because I have no idea what the response would be. But it will probably be dramatic, befitting such a dramatic action.

I think the more interesting question is why you have such confidence in your flows based understanding to dismiss the possibility that the market could fall 50% in such a unique situation?

Flows still result from the collective informered or uninformed decisions of individuals somewhere, which means more is possible then is conceived and covered in any simplifying model of market action.

When thinking through extreme events “The wildest dreams of Kew (a simplifying model of reality) Are the facts of Khatmandu”

1

5

812

massifcap retweeted

11 Jun 2024

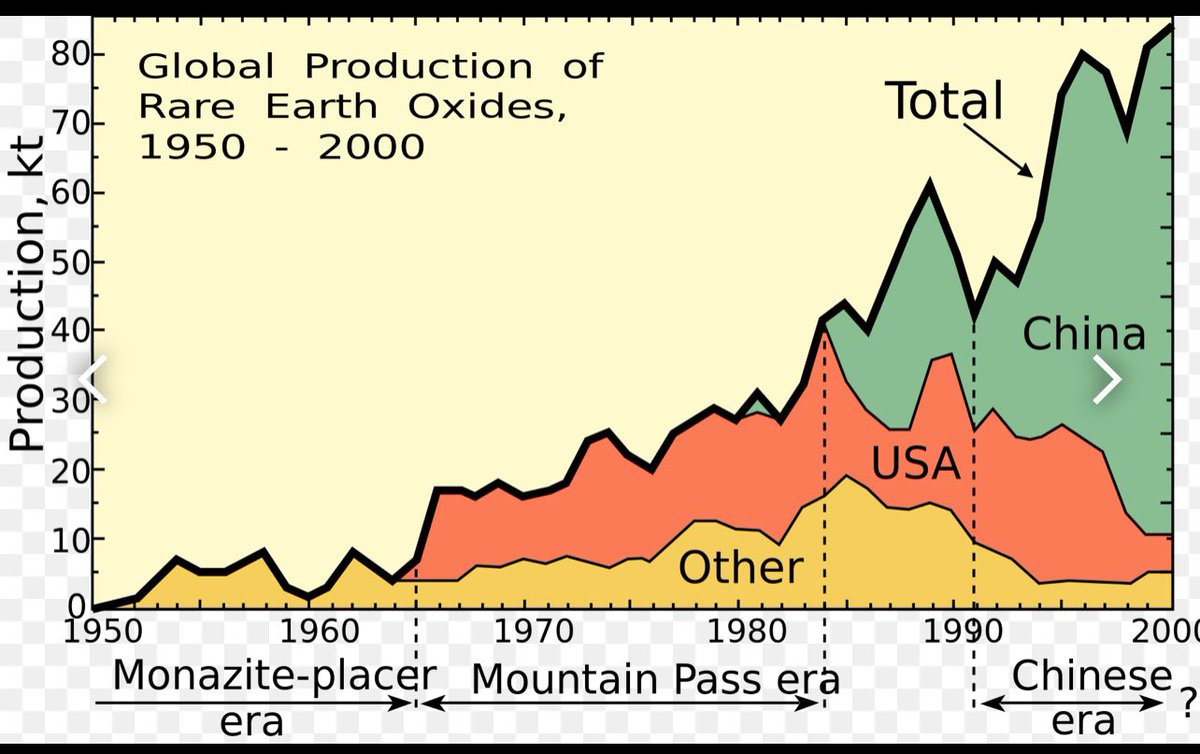

You could not be more wrong, we ceded the rare earth supply chain to China years before EVs or climate change were major drivers of policy. See chart below. Economics is why we don't produce refined REE in the US anymore, it has nothing to do with EVs. You are cherry picking data to push your narrative.

The Government EV push (as poorly conceived as it is, and it is, in that you arec orrect) is the only reason companies are now making an effort to bring REE processing back to the US. Whether that works out or not is a story yet to be written, I will bet on Western innovation to figure out better processing in the long run, but that long run will be awhile.

1

2

3

590