Boost stickiness and revenue - launch your branded neobank in minutes. | Book a demo → masswallets.xyz

Joined April 2026

- Tweets 156

- Following 107

- Followers 60

- Likes 164

8 Photos and videos

Pinned Tweet

Jun 11

🚀 Turn your product into a neobank in minutes.

mass[Wallets] is the one-stop factory for branded, non-custodial wallets powered by your own embedded stablecoin.

No code. No liquidity headaches. No compliance stress.

✅ Custom branding & UX

✅ Up to $150K insurance per holder

✅ Full privacy on public chains

✅ Instant DeFi access

✅ Modular on/off-ramps

Create your app. Your own stablecoin is already there.🪙

Follow Uniswap, 1inch & Hyperliquid. Boost stickiness revenue with your own branded card & stablecoin.

Neobankify with us → masswallets.xyz or DM @masswallets @massfinance

2

4

13

950

massWallets retweeted

Jun 10

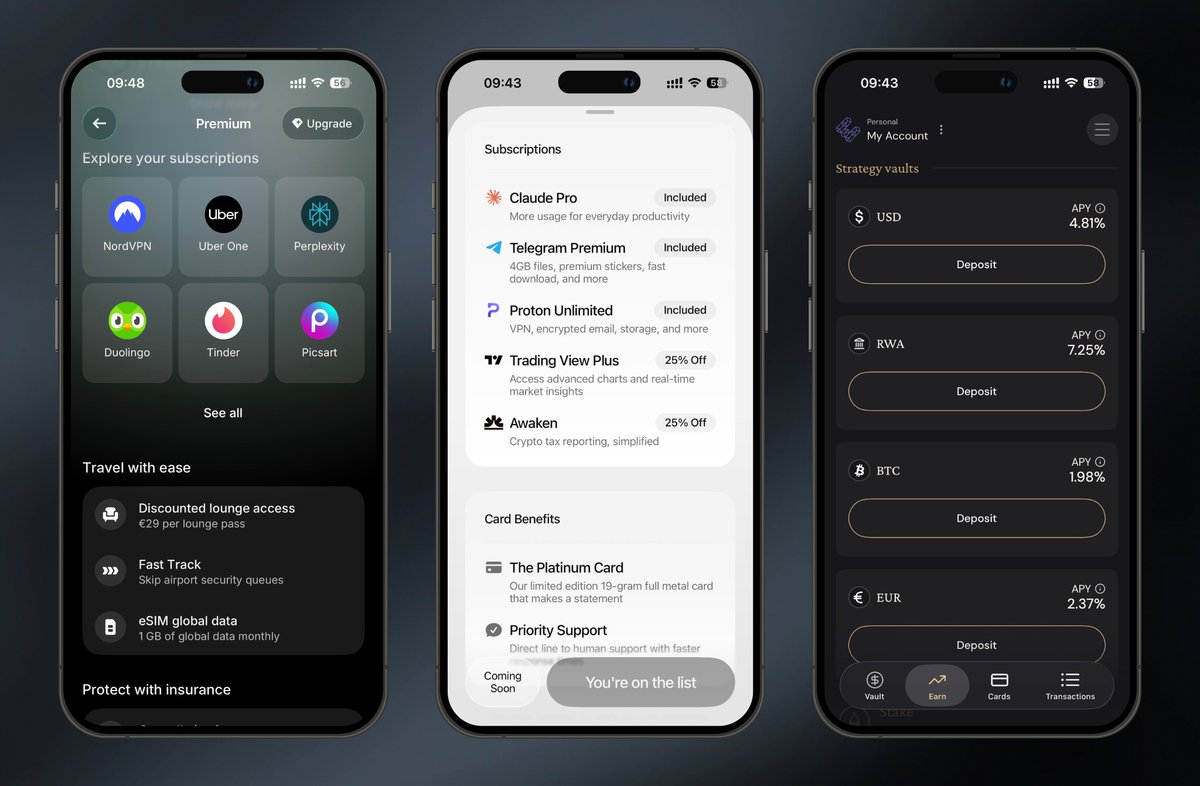

Perks are important.

Anyone who launches with us can:

- Select sustainable perks for end-users

- Program their own loyalty program

- Issue a branded card and stablecoin with a powerful revenue model

...and much more: masswallets.xyz

Nice to see crypto neobanks moving beyond just cashback

Cashback is great, no doubt. But subscription perks, travel benefits, premium support, and even yield on idle balances are what really make these products stand out from traditional banks

The gap between a crypto card and a full financial app keeps getting smaller

What matters most to you in a neobank?

3

9

350

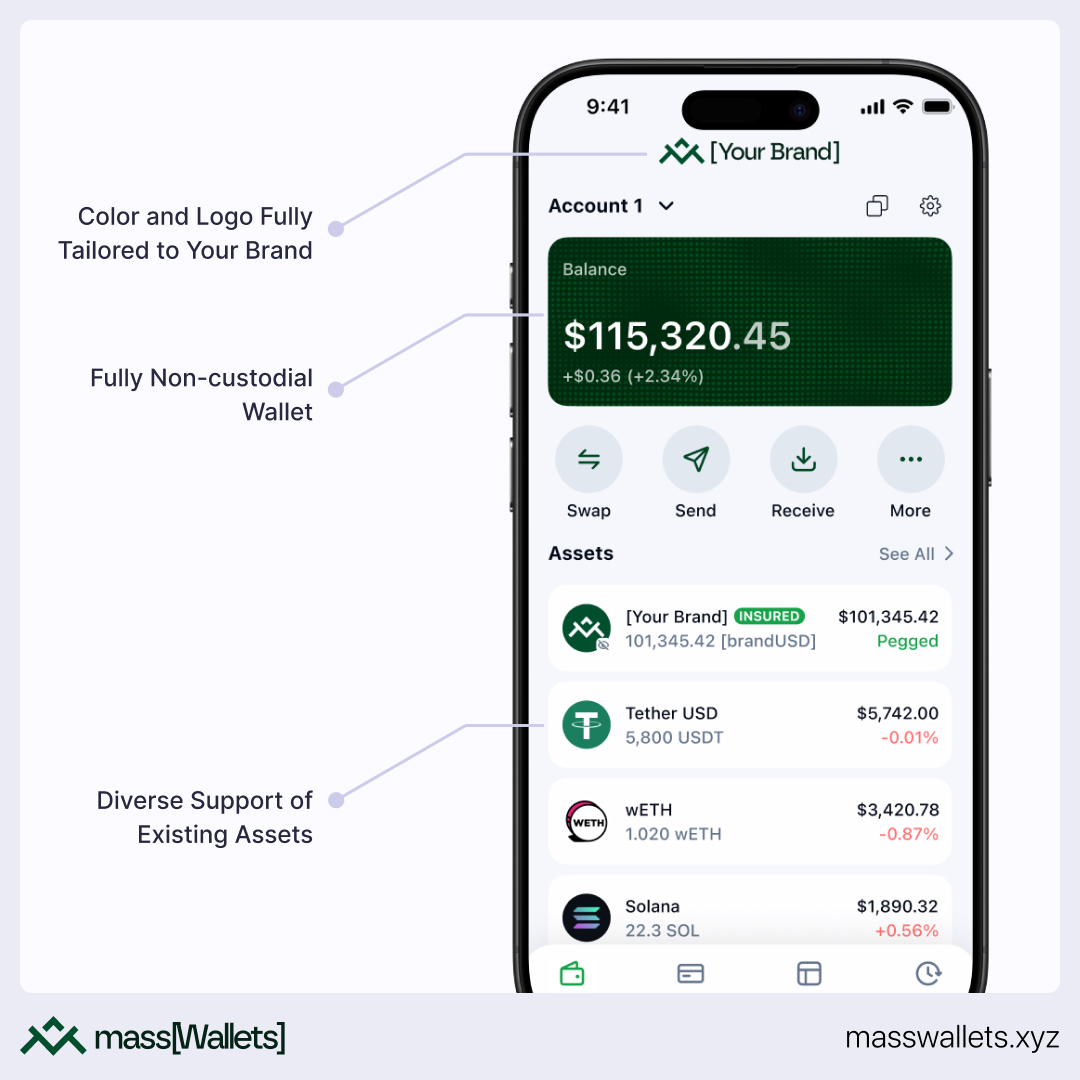

Offer your own branded stablecoin | 5/6

Embed in your neobank, a stablecoin which is:

• Instantly liquid

• Insured up to $150K per holder

• Private on public blockchains

• Generates powerful rewards based on your stablecoin’s market cap

• Instantly interoperable with all DeFi protocols

The same high-margin revenue model as Circle & Tether — without the liquidity, security, or compliance burden.

5

1

14

639

Jun 16

Issue your branded card | 4/6

Launch your neobank with a powerful card:

• Fully customizable logo and colors

• Accepted worldwide

• Your users can spend their stablecoin balances anywhere

• You earn up to 2% on each card transaction

Give your stablecoin real-world spending power.

Branded cards that drive adoption and generate revenue on every swipe.

1

5

104

Jun 16

Seamless Fiat Connectivity | 3/6

Leverage built-in on/off-ramp capabilities:

• Personalized named accounts

• Direct Google & Apple Pay integrations

• Issue your own branded cards

• Enable spending of digital assets, globally, 24/7

Seamless fiat ↔ crypto ramps built in. Users onboard in seconds and spend anywhere, anytime.

3

1

8

135

Jun 16

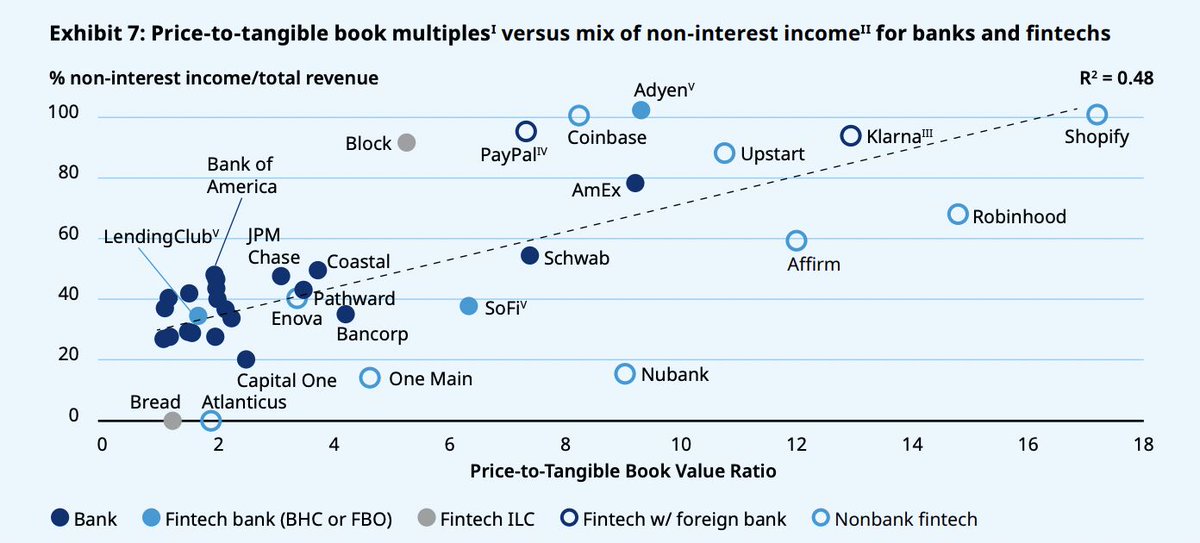

The future innovation will sit somewhere between the traditional, extremely powerful revenue models (deposits and lending) and the fintech business models (captured interchange and fees).

Just a few neobanks in the world leverage both models. We serve them to you on a platter.

Jun 16

The stablecoin opportunity for fintechs is not only cheaper payments. It is revenue architecture.

Banks are usually valued on deposits, lending margins and credit quality. Fintechs get rewarded when revenue looks more like fees, software, payments and platform economics.

Stablecoins sit right in the middle. They can create new fee layers around: payments,FX,conversion,treasury movement,merchant settlement,tokenized assets, embedded finance.

That is why Circle, Stripe, PayPal, Robinhood and Mercury moving closer to bank-like infrastructure is so interesting.

2

109

Jun 15

"Neobankify your product" — we coined it, don't steal it, thx. ®🫡

7

109

Jun 15

The mass[Wallets] Launcher | 2/6

Create branded mobile app in minutes:

• White-label and fully non-custodial

• Full ownership of UX

• Diverse support of assets

No heavy development. No custody headaches. Your brand. Your UX.

Live on iOS & Android in minutes, not months.

3

1

10

2,264

Jun 12

Even debit cards are not easy to displace. Debit cards exist because credit cards have paved the way with merchants. Credit cards exist solely because of credit. To dethrone Visa/MC, one must deeply understand credit.

But what do we know? We’re just a factory for banks 🏦🤗

Jun 11

Bill Gurley says Visa and Mastercard will be "heavily threatened" by stablecoins.

From The Knowledge Project this week:

"Those two companies have two of the highest operating margins in the history of business. They have like 60% operating margins, and they're duopolies, and they were created by the banks. So the whole industry is kind of stuck in this world where they make a lot of money because it is this way. But there's zero reason why it should cost 2 or 3%. Just zero.

In America, if I want to send you 50 bucks digitally, I've got to go through ACH, which is 3-day settlement, which is part of this regulatory capture bullshit... If you have a Coinbase account, you can put your money in a USDC stablecoin and earn 4%, and within seconds immediately transfer money to someone else for pennies...

At this point, I think stablecoins will get there faster than the government will be able to do it."

$V $MA

Agree or disagree?

5

244

Jun 12

🚀Why mass[Wallets]? | 1/6

• Boost your company’s IP — ship iOS & Android apps in minutes

• Fully monetize your user base

• Supercharge your GTM through loyalty & perks

• Drastically reduce churn

Launch a powerful neobank /w embedded stablecoin in minutes & own the full UX

1

10

203

Jun 12

The neobanks of the future will be launched on top of existing communities. Think of them as the modern version of credit unions in the US.

mass[Wallets] is here to accelerate that vision, and we start with DeFi.🫡

1

4

166

Jun 11

We are not just a wrapper on top of a stablecoin; we are the stablecoin.

We are not just a player on top of a settlement chain; we are the settlement layer.

We don’t just tap into liquidity; we are liquidity.

We are not just a wrapper on top of a BaaS; we are the BaaS itself.

1

8

230

Jun 11

Yes, and mass[Wallets] is the factory for neobanks, which spawns stablecoin-backed neobanks with all of these and much more.

Neobankify with us! 🫡

Jun 11

All winning crypto neobanks / cards have:

1. Multichain & asset deposits, esp USDT on Tron

2. Localized distribution in stablecoin rich markets

3. Products beyond payments like earn and swap

4. Ultra simple UX with a shallow learning curve

5. QR payment and money moving rails with banks

6. Tiered memberships with cashback and fee differentiation

Bare minimum

5

211

Jun 10

You can use one, or you can issue your own. Make your pick.

4

195

Jun 10

🚀 Hundreds of OTC desks, DeFi protocols, and crypto projects have tried building their own mobile app… and most gave up.

The reason? 6–12 months of development, high costs, and ongoing maintenance.

Today, that changes.

With mass[Wallets], you can launch a fully branded, non-custodial mobile app — complete with your own branded stablecoin and credit card — in minutes, not months.

No engineering team required.

Unlock new revenue streams (up to 2% on card transactions 3–9% on stablecoin float), increase user loyalty, and keep users inside your ecosystem.

Built with:

- @privy_io – secure key management (75M wallets)

- Leading card partners (@InterlaceMoney & @reapglobal )

- @masscurrencies for the stablecoin infrastructure

Read the full article here. 👇

2

4

10

977

Jun 4

A single solution focused on the core of money can unlock an entirely new universe of possibilities. Welcome to the next quantum leap in finance.

This is mass[Finance].

6

111

Apr 29

A few days in Paris, filled with valuable conversations.

One theme kept coming up: brands increasingly want to own their wallet experience.

We see a strong interest in mass[Wallets]—helping businesses launch fast, native wallet experiences tied to real business value.

1

5

81