Midnight Explorer is a Block Explorer and Analytics Platform for Midnight Network | Powered by @texlabsorg.

Joined November 2023

- Tweets 610

- Following 82

- Followers 1,926

- Likes 4,151

113 Photos and videos

Midnight Explorer retweeted

May 25

May’s State of the Network shows programmable privacy moving fast from concept to real-world infrastructure.

From discussions at Consensus Miami on compliant privacy and AI, to new live deployments, developer tools, and ecosystem apps, everything points to the same goal: making privacy usable, scalable, and ready for builders and institutions.

🔗 Explore what shipped this month and what’s next: midnight.network/blog/state-…

16

51

289

7,595

Midnight Explorer retweeted

JUST IN: Midnight surpasses 100,000 transactions on mainnet according to Midnight Explorer.

ALT JUST IN: Midnight surpasses 100,000 transactions on mainnet according to Midnight Explorer.

4

10

81

1,444

Midnight Explorer retweeted

May 12

Midnight is building the universal privacy layer.

43

98

675

31,269

🚨BREAKING NEWS:

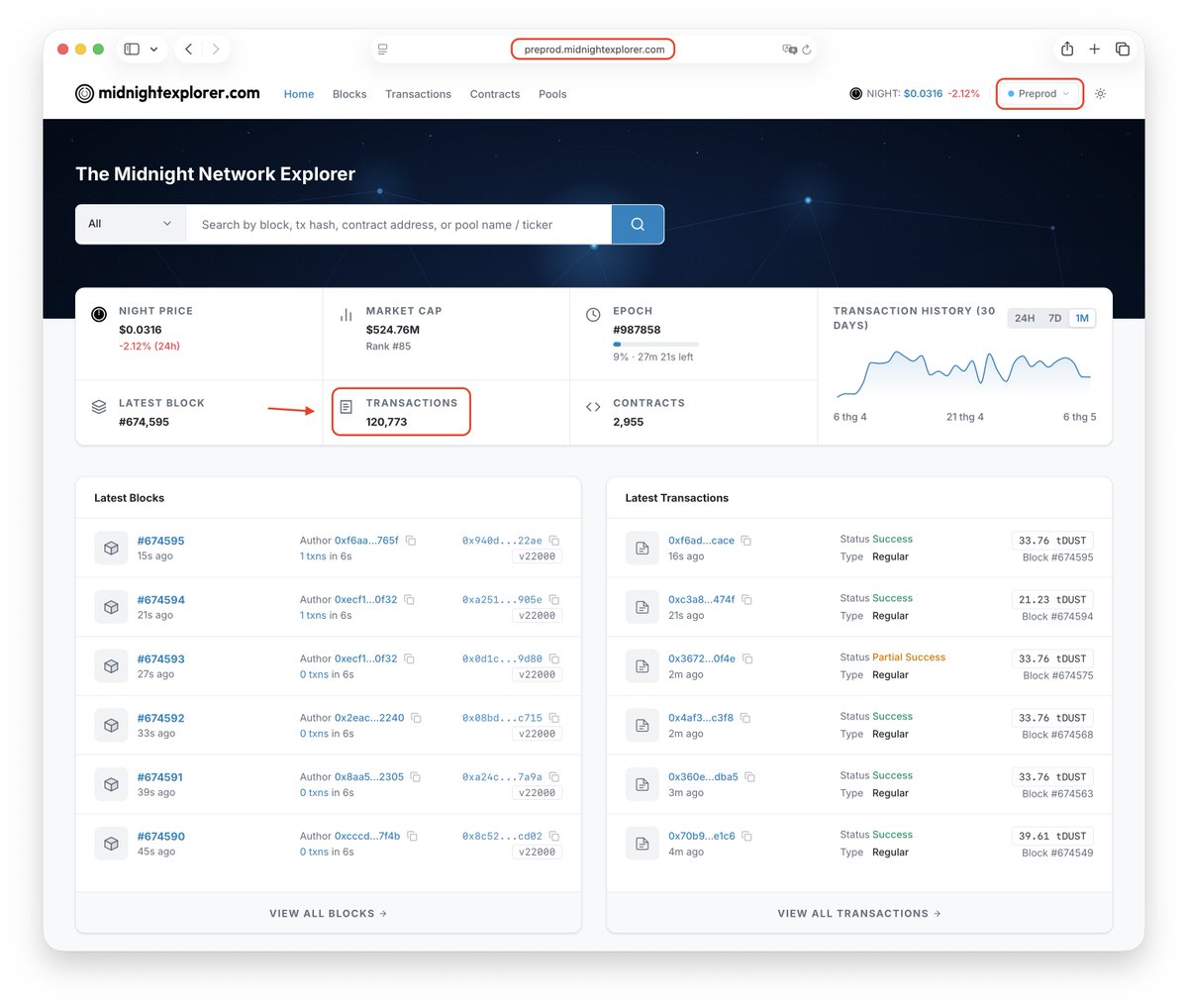

According to statistics from @midnightexplr , the number of transactions created on the Preprod Network has reached over 120,000.

This is a significant number considering that Midnight's Preprod Network has only been operational for a few months.

16

20

120

2,145

Midnight Explorer retweeted

Why AI agents and blockchains need privacy.

Full @IOHK_Charles keynote.

Come build on Midnight!

16

87

510

21,867

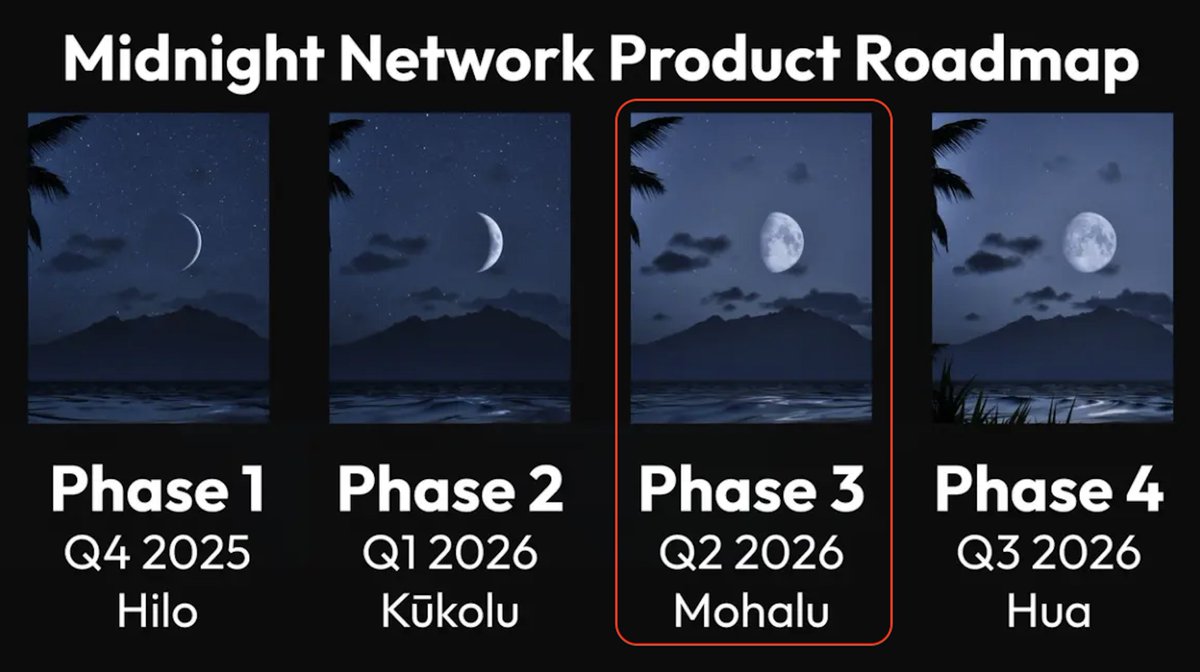

🚨BREAKING: Midnight is in phase 3 - Mōhalu: Broadening network participation.

As Midnight moves beyond initial mainnet stability, the network enters Mōhalu — the phase of expansion, openness, and real participation at scale.

This is where things get serious.

Mōhalu is not just about growth — it’s about stress-testing the network in real-world conditions. The federated mainnet begins to scale, onboarding more participants, more infrastructure, and more activity. Block production is no longer limited — it starts to involve a broader set of operators contributing directly to the network’s security and performance.

At this stage, Midnight evolves from a controlled launch environment into a living, growing system.

Key highlights of Mōhalu 👇

🌐 Expanded participation: More node operators and contributors join the network

🧱 Block producer activity: Moving toward a more distributed validation layer

🧪 Testing at scale: Real usage, real load, real feedback

🎯 Scaled Incentivized Testnet: Contributors are recognized and rewarded

⚡ DUST capacity exchange: Unlocking the economic layer for network usage

But beyond the tech, Mōhalu represents something bigger:

👉 It’s the moment the network opens up to the world

👉 The moment future SPOs step in and prove their capabilities

👉 The moment Midnight starts shaping its long-term resilience

If Kūkolu was about launching safely,

then Mōhalu is about growing confidently.

And this is where the foundation for true decentralization begins. 🔥

14

71

321

6,413

Midnight Explorer retweeted

May 1

Apr 30

This GPT Image 2 prompt is going insanely viral right now.

“Redraw the attached image in the most clumsy, scribbly, and utterly pathetic way possible. Use a white background, and make it look like it was drawn in MS Paint with a mouse. It should be vaguely similar but also not really, kind of matching but also off in a confusing, awkward way, with that low-quality pixel-by-pixel feel that really emphasizes how ridiculously bad it is. Actually, you know what, whatever, just draw it however you want.”

18

33

283

14,032

Apr 22

🚨 MIDNIGHT EXPLORER v2.0.0 IS NOW LIVE 🚀

The upgrade is complete, with near-zero downtime.🔥

Midnight Explorer v2.0.0 has been successfully deployed - marking a major leap forward for the Midnight Network ecosystem.

This isn’t just a redesign. It’s a transformation.

✨ A completely new UI/UX — cleaner, faster, more intuitive

⚡ Smoother performance — built for real-time, real-world usage

🧭 Better navigation — making on-chain data easier to explore than ever

But the real shift is deeper 👇

Midnight Explorer is no longer just an explorer, it’s becoming a modular infrastructure layer and ready to be integrated into wallets, dashboards, and dApps across the ecosystem

@MidnightNtwrk @midnightfdn @IOHK_Charles @IOGroup

18

85

389

25,876

Apr 20

🚨COMING SOON: MIDNIGHT EXPLORER v2.0.0 🚀

A major upgrade is on the way.

Midnight Explorer v2.0.0 is being rebuilt with:

✨ A completely new UI/UX

⚡ Smoother, faster performance

🧭 Improved navigation & data experience

But more importantly 👇

🔌 Designed to be easily integrated into other projects - making it not just an explorer, but a modular infrastructure layer for the Midnight Network

⏰ Launch time: 16:00 UTC, April 22, 2026

This is a big step toward turning Midnight Explorer into a tool developers can build on, not just use.

Stay tuned. The next version is coming. 🔥

midnightexplorer.com

27

44

247

5,701

Apr 13

Visit Midnight.fun to see what's fun at Midnight! 🔥

Apr 12

Want to experience Midnight in action?

Check out midnight.fun, a live gallery of games designed to demonstrate programmable privacy 🎮

Featuring:

👉 Kachina Kolosseum

👉 Block Kart Legends

👉 Safe Solver

New drops coming soon: midnight.network/blog/introd…

6

24

100

3,045

Midnight Explorer retweeted

Apr 9

Bitget now supports NIGHT.

As a leading derivatives and spot exchange, @bitget gives users a new channel to access NIGHT and participate in the Midnight ecosystem.

Bitget’s support further accelerates mainstream exposure to privacy-first blockchain infrastructure.

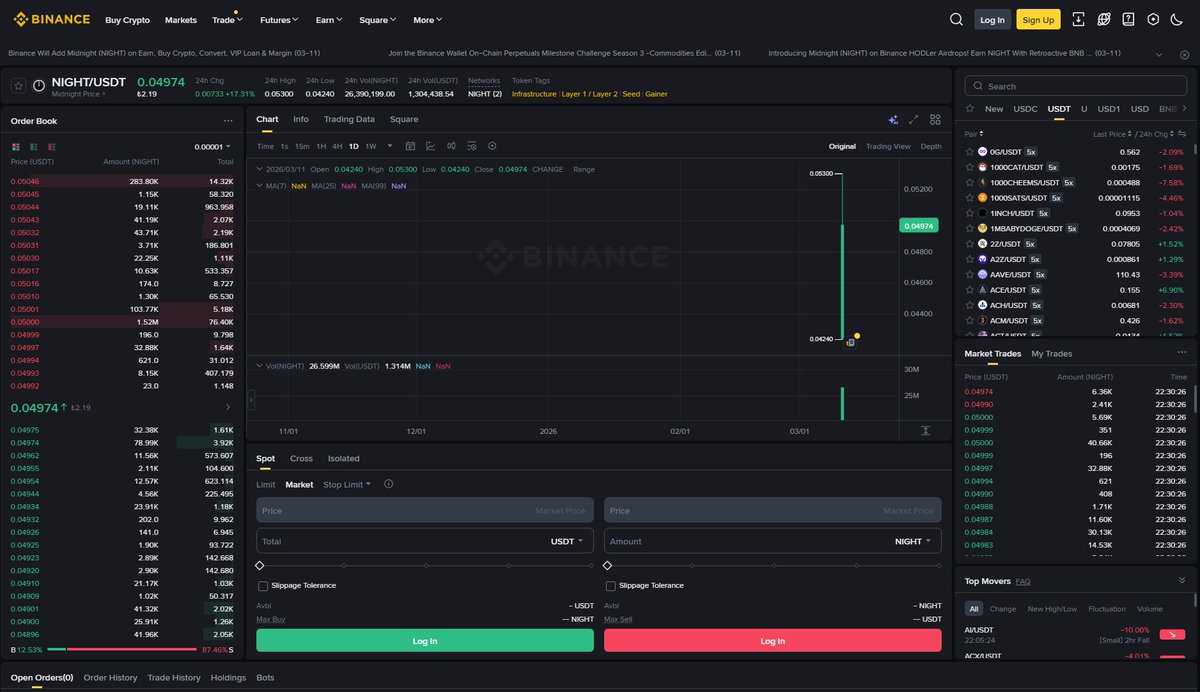

New Listing - $NIGHT @MidnightNtwrk

🔹Pair: NIGHT/USDT

🔹Deposit available: now

🔹Trading available: April 9, 2026, 11:00 (UTC)

🔥 Watch out for Launchpool, Candybomb, PoolX, and more.

Details: bitget.com/support/articles/…

32

163

756

32,662

Midnight Explorer retweeted

Some top Midnight projects to keep an eye on that’ll help power our DEX 👇

💳 Wallet: @OneAmXYZ

📰 Explorer: @midnightexplr

🆔 Identity: @MidnamesTeam

Privacy DeFi is loading…

Are you ready? 👀

5

8

50

1,371

Mar 31

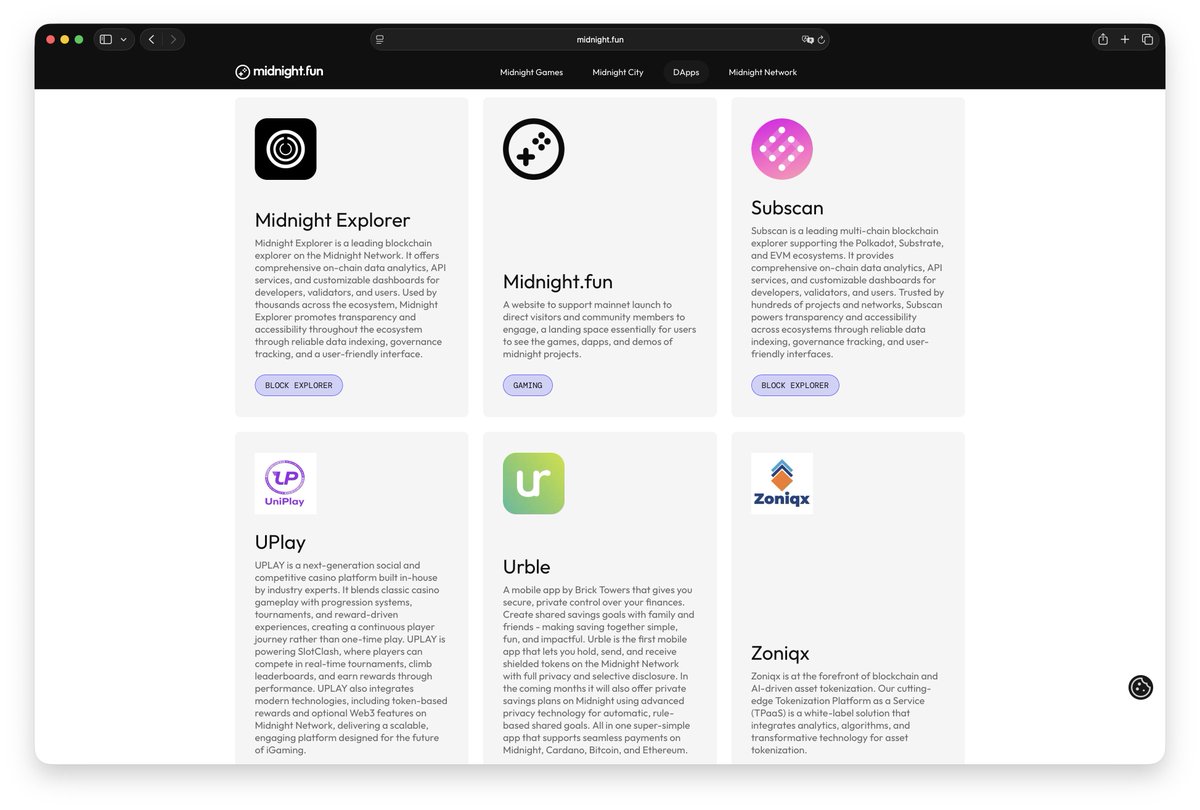

🚨JUST IN: Let's explore the products available in Midnight.fun's Dapp catalog.

Here we have the following categories:

👉Wallet: @Ctrl_Wallet @lace_io @urbleapp @dynamic_xyz

👉Defi: @BodegaCardano @zoniqxinc @balance_canada @webisoft_

👉Gaming: midnight.fun @UniPlayToken

👉Block Explorer: @midnightexplr @subscan_io

👉Dapp: @OneAmXYZ

👉Tokenized RWAS: @zoniqxinc

👉AI: @OneAmXYZ

These are all projects that are making significant contributions to the community.🔥

10

31

129

3,615

Mar 30

🚀 Midnight Explorer Mainnet Lite is officially live!

Alongside the launch of the Midnight mainnet, we’re excited to announce:

🔥 Midnight Explorer has released the Mainnet Lite version

The Lite version is designed to:

⚡️ Provide faster and smoother access on mainnet

🔍 Enable simple transaction and block lookups

🧭 Optimize the experience for both new and advanced users

This is just the first step in our journey to deliver a fully featured explorer, bringing transparency and efficiency to the Midnight ecosystem. More detailed features will be rolled out as soon as possible.

👉 Try it now and start exploring the Midnight mainnet:

mainnet-lite.midnightexplore…

4

50

235

6,238

Midnight Explorer retweeted

Mar 30

The moment is here. Midnight is live.

Welcome to the era of privacy by default, and disclosure by choice.

Read the full announcement article 👇

199

486

1,774

169,482

Mar 26

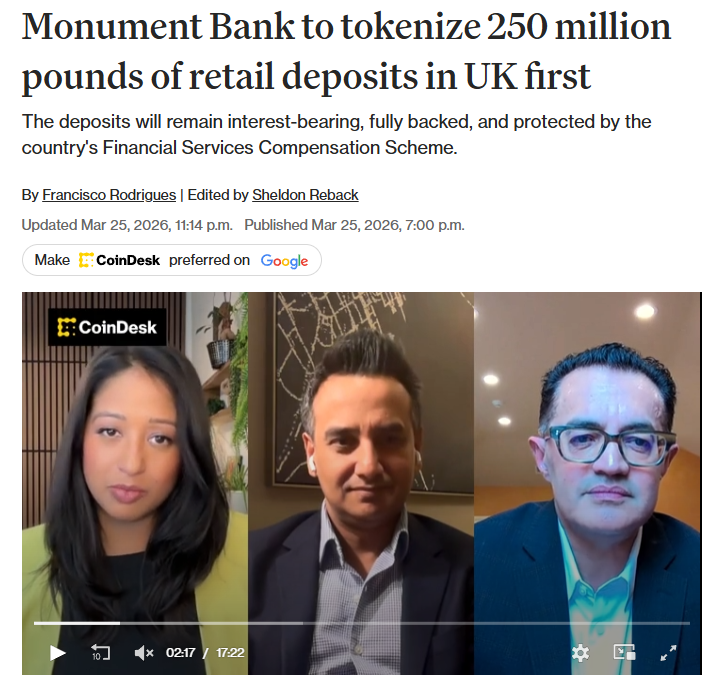

From a numerical perspective, Monument Bank Limited launching £250M in tokenized deposits in its first phase reflects a highly institutional approach: large enough to validate real-world performance, yet controlled in scope to manage risk. This is not a small pilot, but a live deployment in a regulated environment. Importantly, these deposits remain fully backed 1:1, redeemable in GBP, and protected under FSCS, meaning users do not have to trade off safety when adopting new blockchain-based infrastructure.

From a benefits standpoint, integrating Midnight Network enables a new financial model: tokenization with built-in compliance and privacy. Users can access advanced financial products (RWA, private equity, lending) directly within a banking app without needing to understand or manage blockchain, while institutions maintain data confidentiality through zero-knowledge technology. If successfully scaled, this model could unlock a $4T–$16T tokenization market by 2030, positioning blockchain as a core financial infrastructure layer rather than an experimental technology.

Mar 25

Midnight 🤝 Monument Bank

Monument is set to become the first UK-regulated bank to tokenize retail customer deposits on a public blockchain — representing interest-bearing savings as digital tokens while remaining fully backed, redeemable in GBP, and protected under existing regulatory frameworks.

Built on Midnight’s privacy-enhancing blockchain infrastructure, this approach ensures that transaction data remains shielded and accessible only to authorized participants — enabling the use of blockchain technology while maintaining the confidentiality and compliance required in regulated financial services.

The initiative begins with a target of £250 million in tokenized deposits and represents the first phase in a broader rollout to expand access to tokenized financial products. Over time, this includes enabling exposure to asset classes such as private equity and structured products, and introducing more flexible lending models — capabilities historically reserved for institutional and private banking clients.

Together, this partnership demonstrates how regulated financial institutions can bring traditional financial products on-chain — unlocking a more flexible, accessible, and programmable financial system without compromising privacy or regulatory standards.

4

15

76

1,611

Mar 25

🚨 FIRST BANK GOES ON-CHAIN WITH MIDNIGHT — AND IT CHANGES EVERYTHING 🚨

A UK-regulated bank is bringing real customer deposits onto blockchain.

🤝 Monument Bank Limited × Midnight Foundation

This isn’t a pilot. This is a live financial shift:

💷 Up to £250M in retail deposits being tokenised

🔒 Fully backed, redeemable in GBP, and protected under UK regulation

🧾 1:1 representation of real bank deposits on-chain

But here’s what makes it groundbreaking 👇

👉 Built on Midnight Network

→ Zero-knowledge privacy

→ Regulatory compliance

→ No exposure of sensitive financial data

This unlocks something bigger:

📈 Tokenised assets for everyday users (not just institutions)

🏦 On-chain savings, investments, and lending

🌍 A new financial system where privacy compliance coexist

And this is just Phase 1.

Next:

→ Tokenised investment products (private equity, commodities…)

→ Lending against on-chain assets (like private banking, but for more people)

From $4T–$16T tokenisation market… to real retail banking use cases.

This is how blockchain enters traditional finance. 🚀

12

86

532

7,501

Mar 25

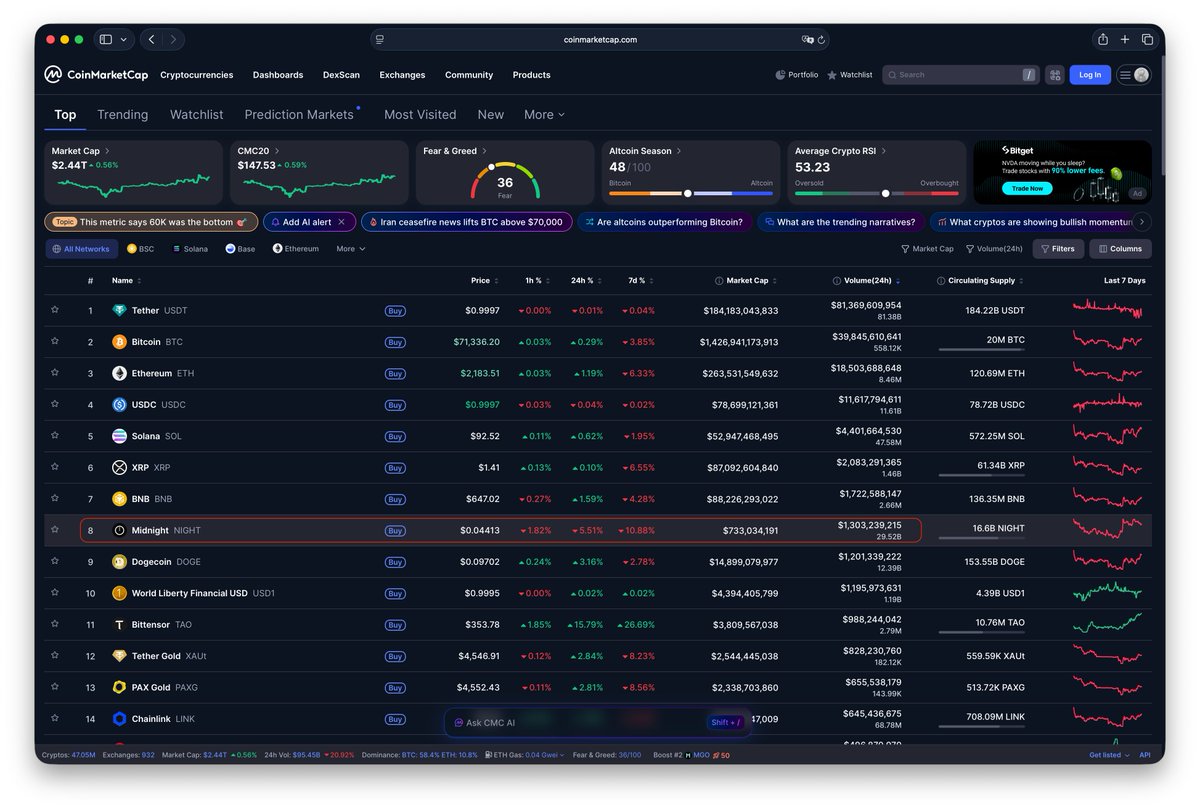

🚨BREAKING: $NIGHT IS AMONG THE TOP 10 CRYPTOCURRENCIES WITH THE HIGHEST TRADING VOLUME IN 24 HOURS.

According to data from @CoinMarketCap, $NIGHT ranks 8th with a trading volume of $1.3 billion, trailing only major global cryptocurrencies like $BTC, $ETH, $BNB, $XRP, and $SOL in terms of trading volume.🔥

And the mainnet is coming closer to us.🚀

12

40

259

4,587

Mar 19

🚨BREAKING: Midnight Explorer is Mainnet Ready 🚀

As the Midnight Network moves closer to mainnet launch, Midnight Explorer is fully prepared to support the network from block one.

For builders, users, and institutions, the transition from test environments to mainnet requires reliable infrastructure. Midnight Explorer eliminates that gap by already supporting the network across multiple stages of development.

Today, Midnight Explorer provides block exploration across:

👉Preview: preview.midnightexplorer.com

👉Preprod: preprod.midnightexplorer.com

This ensures a seamless transition to mainnet monitoring, analytics, and transparency the moment the network goes live.

🔎 From early testing to production infrastructure - Midnight Explorer is ready to track the next generation of privacy-enhancing blockchain activity.

Mainnet is coming. We’re ready.🔥

👉midnightexplorer.com

28

86

421

8,858