building and funding tech ventures | @HorusGroup_ 𓂀 | @Orbitmoney_

Joined October 2023

- Tweets 1,820

- Following 712

- Followers 545

- Likes 3,783

31 Photos and videos

last months in fundraising:

- success-fee broker blasting 32 projects in one go

- founders ghosting VCs I intro'd them to

- a team we almost invested in scamming other investors for $10M

- a GP publicly humiliating a founder we know

and this is just what i can talk about.

9

4

30

3,831

someone asked me this week what the sentiment in web3 is and the honest answer took two words.

everyone's broke.

founders calling it "heads down" because the alternative is admitting the raise died. agencies folding.

funds we know from the LP side stretching deployment out so the vintage looks alive longer.

none of it makes the timeline, the timeline is all partnership announcements.

and the projects actually making money are nearly impossible to get a meeting with, because they don't need anyone.

3

75

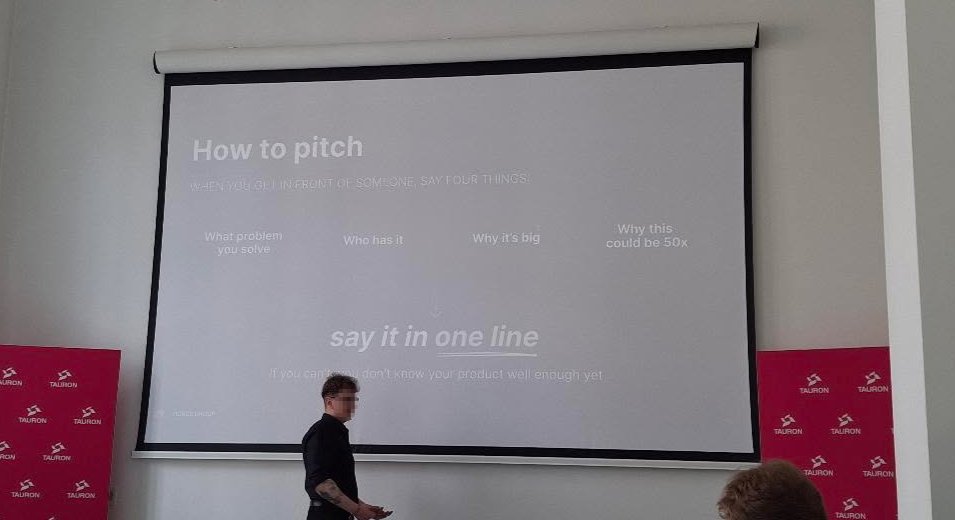

nobody reads a flyer twice. you glance at it and either know you need the thing or you bin it.

your pitch works the same way.

founders keep handing VCs five slides of product architecture before getting to the part where anyone makes money. the partner isn't evaluating features. he's deciding in about a minute whether this is a machine that turns his fund's money into more money.

say what it does in one line. spend the rest on why it prints.

the product deep-dive lives in the second meeting, which you only get if the flyer worked.

2

83

pre-seed founders all run at the same 50 VC funds and ignore the corporates sitting in their own network.

a corporate venture arm

- doesn't care about your valuation the way a fund does. they're not optimizing a portfolio model.

- they need what you're building to exist because it plugs a hole in their own roadmap, and that shows up in the terms.

two real caveats:

1) they move slower than funds,

2) and some VCs get twitchy seeing a corporate on an early cap table.

but if you're pre-seed with industry contacts and no warm path to funds, you're probably pitching the wrong room.

2

76

Miles 𓂀 retweeted

Jun 11

Where is the VC money going in crypto this year.

"The verticals", most to least (Q1 2026, % of total disclosed capital)

Payments

$2.39B across 17 deals, 35.0% — anchored by the BVNK $1.8B M&A transaction and Rain's $250M Series C CRYPTO fundraising

Prediction Markets

$1.72B across 11 deals, 25.2% — entirely driven by Kalshi ($1.0B) and Polymarket ($600M), both closing in the final 12 days of March CRYPTO fundraising

Finance/Banking

$835M across 25 deals, 12.2% — the most active sector by deal count CRYPTO fundraising

Real-World Assets

$284M across 7 deals, 4.2% CRYPTO fundraising

Marketplace

$255M across 2 deals, 3.7% CRYPTO fundraising

Infrastructure

$184M across 12 deals, 2.7% CRYPTO fundraising

Tax & Accounting

$175M across 2 deals, 2.6% CRYPTO fundraising

API

$150M across 1 deal, 2.2% (that's Alpaca's Series D alone) CRYPTO fundraising

Social Network

$100M, 1 deal, 1.5% CRYPTO fundraising

DeFi

$88.7M across 5 deals, 1.3% CRYPTO fundraising

11

1

31

2,406

Miles 𓂀 retweeted

Jun 11

Currently looking for 5-10 solo saas founders or small digital business owners to act as early pilots/build partners with us at Orbit Money.

We are building automations for solo SaaS founders and small digital businesses to take the most painful parts of money financial admin off the plate.

We’ll work closely together to unblock bottlenecks and automate workflows.

Primarily around reconciliation, invoicing, cash flow visibility. Things that you are currently doing manually in the background but shouldn’t be.

Will be then be solidified in the early product.

Comment below or send me a Dm if you’re interested or to chat.

3

3

3

136

i sold a company once that, being honest, had stopped working as a startup.

the product stack still had value, the distribution still had value, someone wanted both, and the buyer ran it as a feature instead of a business.

most founders in that spot just let the thing die. you spent two years building a product, integrations, a user base, relationships. that's an asset someone adjacent to your market will pay for even when the standalone bet didn't land.

and if you get to the end and there's genuinely nothing in there anyone would buy, that tells you something about what you were building the whole time.

48

a pattern i keep hitting on intro calls:

the product sits next to what its users do all day instead of inside it.

the user already has a flow that works well enough, and this thing asks them to step out of it for a marginal improvement.

then the founder reads the silence as a marketing problem and starts hiring for growth.

the actual problem is the user has to leave what they're doing to come use the thing, and almost nobody leaves a working flow for a marginal one.

2

37

underrated advantage crypto founders have over web2 founders: almost all of them have seen the inside of a startup.

nobody in crypto is coming from 15 years at a corporation. so by the time someone starts a project they already know raising is a thing, know roughly what a deck looks like, know there's a rhythm to going out for a round.

web2 tech founders often come from one industry silo and have genuinely never watched a company get built from zero. the crypto founder might have a worse idea but they know the moves, and that matters more than people think in the first 12 months.

2

4

228

Miles 𓂀 retweeted

Jun 7

my first vc story is a crazy one. my 2 cofounders and i met the gp and his investment committee at his office. they were extremely rowdy, couldnt tell if they were taking us serious or not. spoiler: they weren't. right as were about to start the pitch some assistant walks in with three hats and the gp tells us to put them on. a rainbow propellor hat, a magicians hat, and a dunce cap. i wore the dunce cap. couldnt believe it was happening but whatever. gp is now laser focused on our pitch while the peanut gallery throws charcuterie at us and interjects by calling us names. halfway through the gp yelled and asked us what our moat was. a wrong answer was given, he made one of us do pushups until he said stop. a little later he asked the other cofounder to recite the greek alphabet, backwards. his punishment was wall sits. a series of wrong answers and punishments. he made us pitch again a couple nights later. thats another story

41

14

503

349,497

"in conversations with a tier 1 VC" decoder:

partner replied to your DM: in conversations

associate took a 20 min call: deep in conversations

they said "interesting, send more": advanced talks

they ghosted after the call and you dont know it yet: finalizing terms

you follow the partner and he hasn't followed back: strategic alignment

1

5

142

a clear no from a VC is worth more than a soft maybe, and most partners get this backwards.

founders remember the investor who passed in one clean sentence with an actual reason.

they also remember the one who said "let's circle back next quarter" and then went silent.

the industry is way smaller than VCs act like it is. the reputation you build passing on deals follows you into every round those founders raise later, and founders talk to each other more than partners assume.

2

12

773

when raising, fast investor replies signal something deeper than hustle.

they tell you how quickly a founder makes decisions, and decision speed is the thing that actually compounds across a whole company.

slow replies usually have less to do with being busy and more with a founder who hasn't decided yet, and that hesitation tends to show up everywhere else in the business too.

5

10

1,384

"pick one vertical and go all in" is good advice with a missing prerequisite.

niching down only works if you actually have an edge in that niche first. picking a vertical because it's hot, with no real expertise underneath, just makes you loud, and loud gets exposed the second the cycle moves and the easy attention dries up.

the focus only becomes a moat if the expertise was already there underneath it.

May 31

Not many people talks about the fog of war phase of building a startup.

You have a good vision of where you're going, but the exact path to it isn't always clear.

Every step you take is a bet and you're trying to extract as much signal from the market as possible, but it's not always clear.

You see so many success stories after the fact where the path they took looked obvious, but you didn't see the 2-3 years where they were pivoting wedges and stuck in the fog of war themselves, you just read about the one path that worked.

3

6

291

the first term sheet matters way more than the terms on it.

one term sheet, almost any term sheet, flips a round from "interesting" to "other people are already in." VCs back what other VCs are backing and a signed term sheet is the cleanest proof someone else committed.

the move most founders miss is asking for a modest believable number, getting the fast yes, then letting the round get bid up off the scarcity that creates. asking for the moon upfront is how you end up with 4 months of "we'll keep an eye on it"

1

11

832

when you're bootstrapped, everything ends up 3x more expensive and 3x slower than you planned.

even when you think you're being conservative, you're still off. i'd put money on it. early on, first 6-12 months, every decision runs on theses that only exist in your head, and you're a founder so you're bullish on all of them.

people say second-time founders cut losses faster, and they do, but it's less about discipline and more that they already know nothing's as easy as the version in their head.

you'll learn the same thing the first time around, just more expensively. the thing i was most grateful for starting @HorusGroup_ was knowing the hard part was still ahead. when it came the team and i were ready and made it through. most of the peers i was watching at the very beginning aren't around anymore.

2

6

392

Miles 𓂀 retweeted

May 29

Altseason is dead and I couldn't be more bullish about it.

I know I tend to get ahead of myself when it comes to calling altseason. Half the time I do it on purpose just to bait the midcurved permabears lol.

But let me be clear: the 2020-2021 era where you could blindly throw a dart at CoinGecko and always hit a winner is over. It's never coming back and that's a good thing.

What's replacing it is something much more powerful: consolidation.

The last few years filtered out the bullshit and the tourists. What's left are assets like $HYPE, $ZEC, $VVV, $CARDS and others that have been putting in impressive performances over the last few weeks and months while most people were still crying about a dead market.

I'm strongly convinced we have left the bear market bottom behind us. We already see appetite is coming back. But investors won't bid blindly anymore, they got burnt and learnt from their mistakes.

All of this will be accelerated by the CLARITY Act eventually going through, opening up the altcoin market for the institutional bid. But also institutions won't touch your memecoins or experimental utility tokens. They will bid real businesses onchain with actual revenue and product market fit.

The incredible run of winners will be our next altseason. If you found one, just hold on to it, because this altseason will be bigger and longer (because sustainable) than anything we've ever seen.

And we are in the first inning of it as we speak.

37

11

170

14,511

an underrated fundraise prep move is looking at what the VCs you're targeting have been seeing in their pipeline lately.

the move is understanding what's making every deck in their inbox look the same so you can package against it.

example: in prediction markets right now, every web3 VC is seeing PM aggregators come through their pipeline. the category is mature enough that partners already know aggregation alone isn't a product and they're looking for what's built on top

your first sentence has to surface that differentiation in the easiest possible way before the partner mentally puts you in the same bucket as the 6 other PM aggregators they saw last week. skipping this step is how good projects lose rounds in the subject line of the first DM.

2

4

706

half the reasons founders don't get a call booked or get ghosted entirely come down to the same thing.

unable to answer basic questions before the call. or pushing for a meeting with nothing but "hi, here's the deck and my calendly."

or running a 45 minute monologue and saying "happy to answer questions at the end."

the whole exchange before and during a VC call should feel like a real conversation. it's the same as selling any product.

you wouldn't drop a link to a deck on a customer and ask them to look at it and let you know if they maybe want to buy. that's lazy. VCs are operators too and most of them have zero patience for outreach that puts all the work on their side.

2

91

"we don't just want investors, we want partners"

every founder says this on a fundraise pitch. almost none of them actually mean it.

real partners come with opinions and push back on decisions you've already made when they think you're wrong.

most founders using the phrase actually want a checkbook that doesn't ask too many questions and shows up for the demo day photo. and that's fine, it's a valid thing to want.

just be clear about which one you're actually optimising for when you decide who to take money from.

6

14

590