香港天風國際證券分析師,分享科技產業趨勢觀察|TF International Securities (HK) analyst sharing tech trend insights

Joined March 2011

- Tweets 1,332

- Following 376

- Followers 238,864

- Likes 1,845

114 Photos and videos

Jun 11

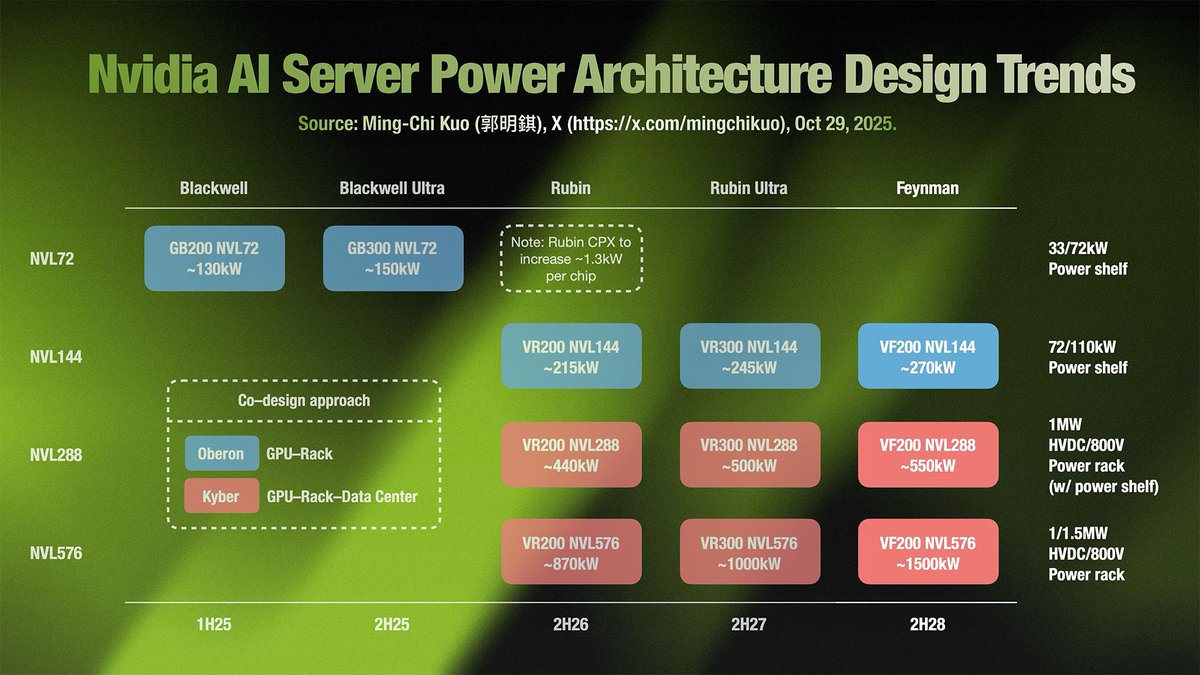

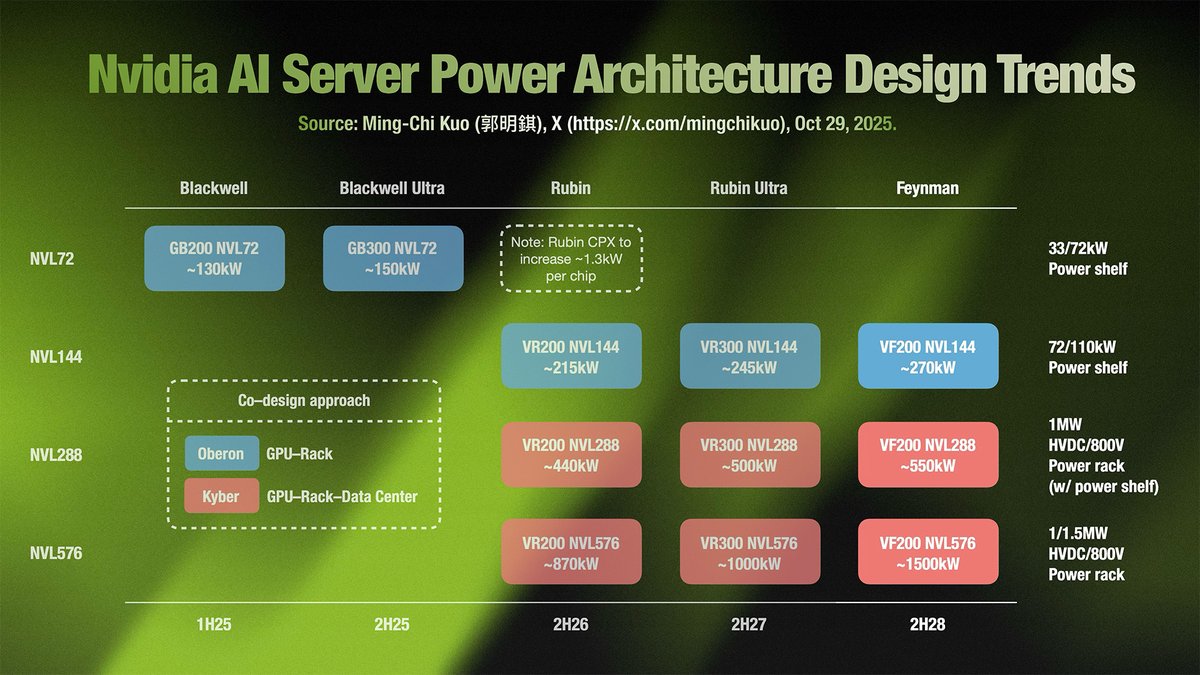

Key takeaways on TSMC's next-generation advanced packaging, CoPoS (publicly available technical details omitted):

1. CoPoS is currently expected to enter mass production in 2H28. It is designed to improve the economics of ultra-large packages above the 9.5x reticle-size class, with NVIDIA’s Feynman AI chip a potential first adopter.

2. According to industry checks, glass is used in two distinct places (dimensions in mm):

→ 310 x 310 temporary glass carriers

→ 250 x 250 (pilot) / 510 x 515 (mass production) glass panels, processed and later cut into individual glass core substrates

3. The glass core substrate is essentially a three-layer structure: a glass core sandwiched between ABF (ABF-GCP) build-up layers on both sides. The widely discussed glass processing challenges, such as TGV formation and copper filling / metallization, are tied to this part of the stack.

4. Common misconceptions about CoPoS:

→ ❌ Misconception 1: CoPoS uses a glass interposer. ⭕️ Correction: The glass is not an interposer. The interconnect role is instead handled by the chip-side RDL, plus the TGV/Cu interconnects and ABF build-up layers in the glass-core substrate stack.

→ ❌ Misconception 2: Glass replaces ABF. ⭕️ Correction: As the substrate architecture above shows, glass and ABF coexist.

→ ❌ Misconception 3: Chips sit directly on glass. ⭕️ Correction: Chips are attached to the ABF build-up surface of the glass core substrate.

5. CoPoS should extend and reinforce TSMC’s leadership in advanced packaging, potentially giving that advantage visibility through around 2032.

35

126

770

555,092

Jun 11

關於台積電的次世代先進封裝 CoPoS 的幾個關鍵(省略可查詢到的技術細節):

1. 預計 2H28 量產,目標提升 9.5 倍光罩尺寸以上的封裝之量產經濟性,Nvidia 的 AI 晶片 Feynman 可能將首度採用。

2. 根據產業調查,兩個不同的地方會用到玻璃(尺寸 mm):

→ 310 x 310 的臨時玻璃載具(glass carrier)

→ 250 x 250(測試)/ 510 x 515(量產)的玻璃面板,加工後切割為玻璃核心載板(glass core substrate)

3. 玻璃核心載板的架構主要分成三層:玻璃作為核心層,上下以 ABF(ABF-GCP)增層包覆。玻璃加工的挑戰,像是TGV(through glass via)、填銅 / 金屬化(metallization)等,指的都是這個階段。

4. CoPoS 常見的錯誤論述:

→ ❌ 錯誤 1:採用玻璃中介層(interposer)。⭕️ 應修正為:玻璃非中介層,其互連角色由晶片側 RDL 與玻璃核心載板側 TGV / ABF 增層分別承接。

→ ❌ 錯誤 2:玻璃取代 ABF。⭕️ 應修正為:如前述的玻璃核心載板架構,玻璃與 ABF 並存。

→ ❌ 錯誤 3:晶片放在玻璃上。⭕️ 應修正為:晶片貼附於玻璃核心載板的 ABF 增層表面。

5. CoPoS 將延續並強化台積電先進封裝的優勢,預期讓該優勢能見度可達約2032年。

38

75

698

180,021

Jun 8

WWDC26 won't change Apple's positive 2H26 share-price trend, but it will test the staying power of the bull narrative

‒‒

1. Apple's core bull narrative right now is an almost intuitive market consensus that few people push back on: "Even if Apple is temporarily behind on AI, it will ultimately catch up and come out ahead."

2. Based on my latest supply-chain checks, I believe Apple's business momentum will remain strong through year-end, which should further reinforce the narrative into something like: "If Apple is doing this well without AI, just imagine once it has AI."

3. So regardless of what Apple says at WWDC26, as long as this core bull narrative stays intact, Apple's positive 2H26 share-price trend is unlikely to change.

4. That core bull narrative has its weak spots, but I think it has a good chance of holding at least through end-2026. How much longer it can last is what makes WWDC26 genuinely worth watching.

5. The key takeaway from WWDC26 will not be the short-term share-price reaction after the event. It will be whether Apple, using the same Gemini, can deliver better AI applications, agentic workflows, and on-device & cloud hybrid experiences than Google.

6. If the answer is yes, it would help extend Apple's core bull narrative. If the answer is no, it would suggest that Gemini sets the ceiling for Apple's AI experience. The stock may not necessarily turn bearish, but the "Apple will ultimately come out ahead" narrative would start to face growing scrutiny.

23

33

319

60,556

Jun 8

WWDC26 不影響 Apple 2H26 股價正向趨勢,但將揭露多頭敘事的續航力

‒‒

1. Apple 目前的多頭核心敘事,是一個近乎直覺、沒什麼人反駁的市場共識:「即使 Apple 在 AI 進度上暫時落後,最終仍能後來居上」。

2. 根據最新的供應鏈調查,我認為 Apple 的業績將會好到今年底,而這會進一步強化多頭核心敘事成為:「Apple 沒有 AI 都這麼好,有了 AI 還得了!」

3. 因此,無論 Apple 在 WWDC26 上講什麼,只要這個多頭核心敘事沒有被破壞,Apple 2H26 的股價正向趨勢就不易改變。

4. 上述多頭核心敘事並非沒有破綻,但我認為至少有機會維持到 2026 年底。至於能維持多久,就是這次 WWDC26 真正值得觀察的地方。

5. 這次 WWDC26 的重點,不在於發表會結束後的短線股價反應,而是:同樣使用 Gemini,Apple 能否做出比 Google 更好的 AI 應用、agentic workflow、裝置端與雲端混合體驗。

6. 如果答案是肯定的,將有利於延長 Apple 的多頭核心敘事;如果答案是否定的,意味著「Gemini 決定了 Apple AI 體驗的上限」,則股價雖未必會轉空,但「Apple 終究會後來居上」的多頭核心敘事,將開始被更多人重新檢視。

10

34

433

75,535

Jun 3

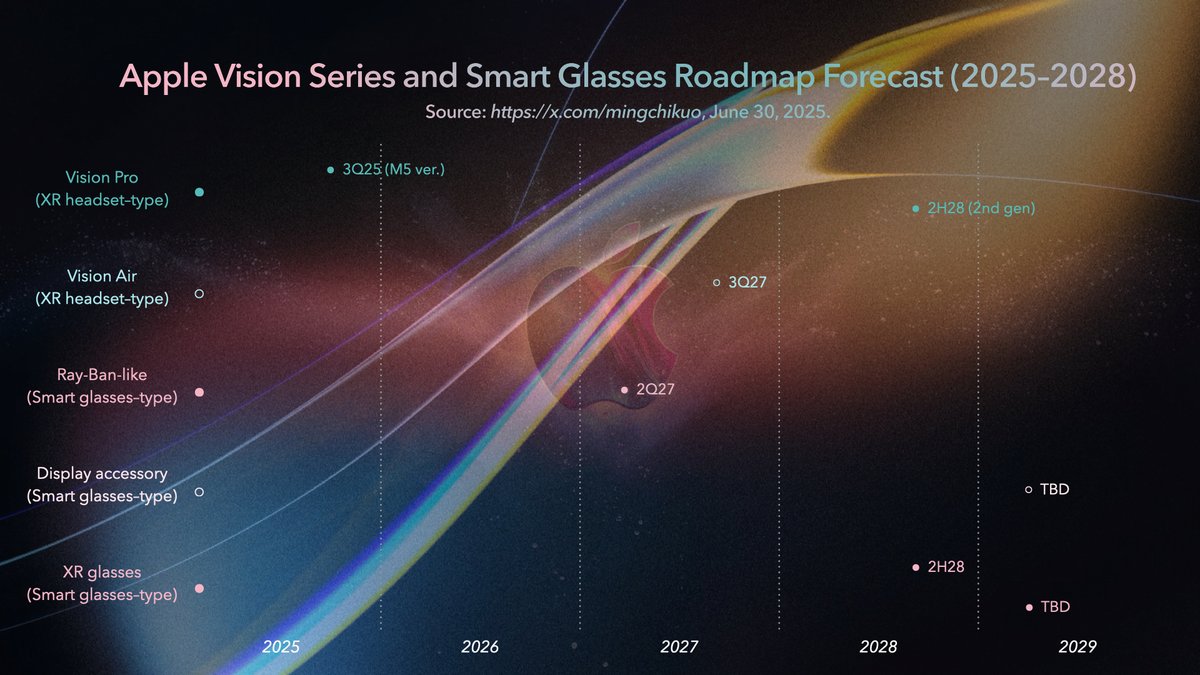

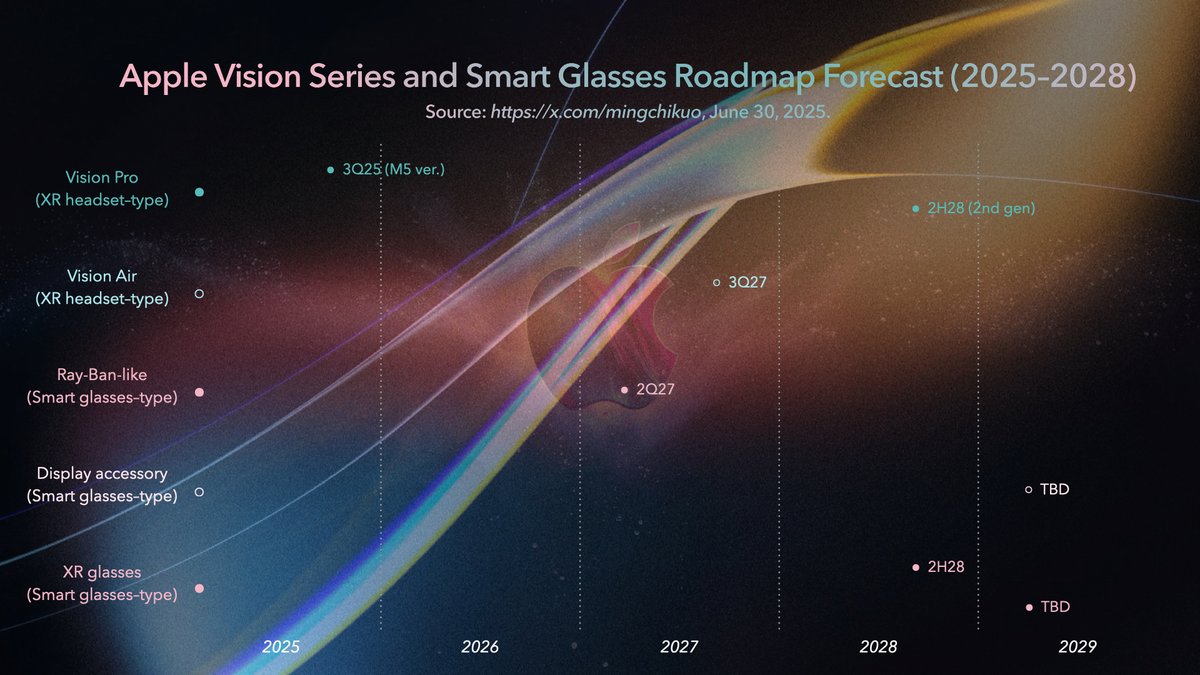

1. The Apple XR headset and smart glasses roadmap I put together about a year ago is no longer a useful reference. For now, only two smart glasses products remain visible in the roadmap.

2. The major overhaul was signed off by Apple's next CEO, John Ternus. This shift actually happened a while back. I'm just late updating the chart. I think removing the Vision Pro line was the right call, as Apple shifts resources toward smart glasses with greater mass-market potential.

3. My latest supply chain checks suggest Apple’s display-equipped AR/XR smart glasses device, powered by optical waveguides, has slipped to 2029. The display-less AI glasses, similar to Ray-Ban Meta, are still expected to ship in 2027.

29 Jun 2025

Apple Vision Series and Smart Glasses Roadmap (2025–2028): Smart Glasses Set to Drive the Next Wave in Consumer Electronics

Full story: mingchikuo.craft.me/b4ueOLIj…

17

41

385

430,579

Jun 3

1. 我大約一年前做的這張 Apple 的 XR 頭戴裝置與智慧眼鏡之規劃路線(roadmap)沒什麼參考價值了,目前只剩兩個智慧眼鏡裝置有能見度。

2. 規劃路線大改是由 Apple 的下一任 CEO John Ternus 拍板定案(其實已經改變一段時間,只是我沒即時更新),我認為移除 Vision Pro 系列、並將資源轉向具有更廣大消費潛力的智慧眼鏡類產品是正確決定。

3. 最新的供應鏈調查指出,Apple 具有顯示功能的 AR / XR 智慧眼鏡(採用光波導)將延後到 2029 年。沒有顯示功能的 AI 眼鏡(類似 Ray-Ban Meta)預計還是在 2027 年推出。

29 Jun 2025

Apple Vision系列與智慧眼鏡產品規劃預測 (2025-2028):智慧眼鏡可望帶動下一個消費電子趨勢

全文連結:mingchikuo.craft.me/FgF89wv0…

7

16

237

57,774

Jun 2

A few thoughts on NVIDIA RTX Spark, setting aside the specs for now: the on-device AI agent narrative, a reality check on delivery, and Apple’s WWDC.

1. At the heart of it are two things: Jensen Huang’s “reinvent the PC” slogan and a concept demo of an on-device AI agent workflow. (I call it a concept demo because there was no live demo.)

The slogan and concept demo should help speed up market consensus around on-device AI agents in the near term.

2. The key elements of the on-device AI agent concept:

OS cloud/local LLM switching agent harness cross-app workflow sandbox

The concept isn't new, but thanks to GTC's reach, it will likely shape how people talk about on-device AI agent use cases for the foreseeable future.

3. Jensen laid out the vision and narrative for on-device AI agents earlier than most. But over the next two years, RTX Spark devices will still be a niche slice of the laptop market, so it's too early to call who wins commercially.

4. Before GTC, most discussion and predictions around RTX Spark / N1X focused on its codename, specs, and supply chain. The operating system rarely came up. In his keynote, Jensen placed the OS alongside the chip platform at the heart of “reinventing the PC.” That echoes my earlier point: the operating system is the key to on-device AI driving the next upgrade cycle.

5. Software is what makes or breaks the user experience. For users to actually experience the agentic workflow Jensen showed, a lot still has to happen. At a minimum, NVIDIA’s CUDA Toolkit needs to officially support Windows Arm64, while Microsoft needs to move Windows’ on-device AI agent stack from preview to general availability (GA), including MCP on Windows, ODR, and agent connectors (all still in public preview), plus Agent Workspace (still in private preview).

If these developer and OS tools still aren't in place when the hardware ships, RTX Spark devices will struggle to deliver on the keynote’s core promise: enabling users to actually create and experience AI agent workflows, the product’s core selling point.

6. After Huang's "reinvent the PC" pitch, how Apple responds to on-device AI agent workflows at WWDC (expected June 8) becomes another thing to watch, alongside how much Siri improves.

For NVIDIA and Microsoft, even if RTX Spark's development or shipping timeline slips, it won't dent their strong growth in AI infrastructure. Apple is in a different position: consumer electronics is its entire hardware business, and on-device AI is where consumer electronics innovation is heading. So beyond a compelling narrative, Apple also needs to show a concrete plan to deliver, including clearer developer tools and an agent-ready OS update timeline.

May 31

許多人期待、Nvidia 可能將要發布的 N1X / Windows PC 處理器,供應鏈調查與重點分析:

▌供應鏈調查顯示,配備 N1X 的裝置未來兩年出貨量約10M

➡ 仍屬利基市場,瞄準對裝置端 AI 算力有需求的重度使用者。

➡ 未來出貨能否上修,除售價因素,還是取決於 Windows 能否提供真正調度裝置端 AI 算力的應用與工作流。

▌目前 PC(Windows 與 Mac)的主流 AI 應用為「用瀏覽器上 LLM 網站」與「透過 API 消耗雲端 LLM 的算力 / token」:

➡ 核心都是使用雲端 AI 算力,非裝置端。

▌2026 年 目前為止 PC 產業的兩個熱門事件,都與裝置端 AI 算力幾乎無關:

➡ MacBook Neo 的熱賣。我的產業調查顯示,2026 年該機種出貨量顯著調升約 100% (5M → 10M)。消費者買的是「低價 設計 生態」,不是買裝置端 AI 算力。

➡ 便宜的小 PC 主機雖仍屬利基市場,但因能長時間掛機跑 AI agent(如OpenClaw)而受到高度關注(如 Mac mini)。這類 agent 的推論算力幾乎也來自雲端。

➡ 小結:無論銷量(裡子)或話題(面子),都與裝置端 AI 算力幾乎無關。

▌裝置端 AI 推動升級換機潮的關鍵為作業系統:

➡ 裝置端 AI 與雲端最大差異,在於兼顧隱私下,能高度整合跨應用程式的用戶資料與工作流,然這需作業系統支援。

➡ 目前 PC 作業系統 AI 化主要仍處於「為本家應用程式增加 AI 功能」與「輕度整合跨應用程式的工作流」。

➡ 已有善用裝置端 AI 算力的應用,如語音轉錄文字,但不足以推動顯著升級換機需求。

▌N1X 裝置可望提供 AI 重度使用者另一個好選擇:

➡ 受益於 N1X,裝置設計能在 AI 算力、記憶體、外觀與攜帶性之間,取得一個更好的新平衡點。

➡ 對在本地端跑 LLM 的重度使用者而言,在不錯的裝置端 AI 算力與大容量記憶體裝置的選擇上,N1X 裝置是除了 Mac 以外的另一個好選擇。

➡ 若欲帶動顯著升級換機潮,除售價外,作業系統(Windows)支援仍是關鍵。

17

31

252

72,943

Jun 2

我對 NVIDIA RTX Spark 的幾個想法(先不討論規格細節):裝置端 AI agent 敘事、實現檢視與 Apple WWDC

1. 核心是 NVIDIA CEO 黃仁勳提出的「重新發明 PC」口號,以及裝置端 AI agent workflow 的概念展示(會說概念展示,是因為沒有實機演示)。上述口號與概念展示,有助於短期內加速形成市場對裝置端 AI agent 的共識。

2. 裝置端 AI agent 展示概念元素:

OS cloud/local LLM switching agent harness cross-app workflow sandbox

此概念並非原創,但藉由 GTC 的高曝光度與敘事張力,在可見未來將會主導裝置端 AI agent 使用者情境的敘事。

3. 雖然黃仁勳領先提出了裝置端 AI agent 的願景與敘事,但畢竟未來 2 年內,RTX Spark 裝置仍是筆記型電腦的利基市場,因此現在判斷商業競爭誰輸誰贏還太早。

4. 在 GTC 前,絕大部分關於 RTX Spark(N1X)的討論與預測都聚焦在晶片代號、規格與供應鏈;相較之下,作業系統的重要性鮮少被提及。而黃仁勳此次演說,將作業系統與晶片平台一同放在「重新發明 PC」的核心位置,這也呼應了我先前提出的核心觀點:裝置端 AI 推動升級換機潮的關鍵在作業系統。

5. 軟體是使用者體驗的關鍵。若要確保使用者能體驗到黃仁勳展示的 agentic workflow,仍有很多工作待完成。至少要看到 NVIDIA 的 CUDA Toolkit 公開支援 Windows Arm64,以及 Microsoft 讓 Windows 本機 AI agent 架構從預覽版走向正式商用(GA),包括目前仍在 public preview 的 MCP on Windows、ODR、agent 連接器,以及仍在 private preview 的 Agent Workspace。

如果硬體發售時,上述開發與 OS 工具仍不到位,RTX Spark 裝置就很難兌現發表會的核心訴求,也就是讓使用者真正創造並體驗 AI agent workflow 這個關鍵賣點。

6. 在黃仁勳提出「重新發明 PC」的口號後,Apple 預計在 6 月 8 日舉辦的 WWDC,會如何回應裝置端 AI agent workflow,就變成除了 Siri 改善程度以外的另一個觀察重點。

對 NVIDIA 與 Microsoft 而言,即使 RTX Spark 後續開發與出貨時程有任何變動,也無損這兩家公司在 AI 基礎建設的強勁成長動能。相較之下,消費電子就是 Apple 硬體事業的全部,而裝置端 AI 就是消費電子創新趨勢的主軸,因此 Apple 除了要提出吸引人的敘事外,也需要給出明確的實現規劃,例如更明確的開發工具、agent-ready OS 的更新時程等。

May 31

許多人期待、Nvidia 可能將要發布的 N1X / Windows PC 處理器,供應鏈調查與重點分析:

▌供應鏈調查顯示,配備 N1X 的裝置未來兩年出貨量約10M

➡ 仍屬利基市場,瞄準對裝置端 AI 算力有需求的重度使用者。

➡ 未來出貨能否上修,除售價因素,還是取決於 Windows 能否提供真正調度裝置端 AI 算力的應用與工作流。

▌目前 PC(Windows 與 Mac)的主流 AI 應用為「用瀏覽器上 LLM 網站」與「透過 API 消耗雲端 LLM 的算力 / token」:

➡ 核心都是使用雲端 AI 算力,非裝置端。

▌2026 年 目前為止 PC 產業的兩個熱門事件,都與裝置端 AI 算力幾乎無關:

➡ MacBook Neo 的熱賣。我的產業調查顯示,2026 年該機種出貨量顯著調升約 100% (5M → 10M)。消費者買的是「低價 設計 生態」,不是買裝置端 AI 算力。

➡ 便宜的小 PC 主機雖仍屬利基市場,但因能長時間掛機跑 AI agent(如OpenClaw)而受到高度關注(如 Mac mini)。這類 agent 的推論算力幾乎也來自雲端。

➡ 小結:無論銷量(裡子)或話題(面子),都與裝置端 AI 算力幾乎無關。

▌裝置端 AI 推動升級換機潮的關鍵為作業系統:

➡ 裝置端 AI 與雲端最大差異,在於兼顧隱私下,能高度整合跨應用程式的用戶資料與工作流,然這需作業系統支援。

➡ 目前 PC 作業系統 AI 化主要仍處於「為本家應用程式增加 AI 功能」與「輕度整合跨應用程式的工作流」。

➡ 已有善用裝置端 AI 算力的應用,如語音轉錄文字,但不足以推動顯著升級換機需求。

▌N1X 裝置可望提供 AI 重度使用者另一個好選擇:

➡ 受益於 N1X,裝置設計能在 AI 算力、記憶體、外觀與攜帶性之間,取得一個更好的新平衡點。

➡ 對在本地端跑 LLM 的重度使用者而言,在不錯的裝置端 AI 算力與大容量記憶體裝置的選擇上,N1X 裝置是除了 Mac 以外的另一個好選擇。

➡ 若欲帶動顯著升級換機潮,除售價外,作業系統(Windows)支援仍是關鍵。

22

64

455

94,525

May 31

Nvidia's Much-Anticipated, Reportedly Upcoming N1X / Windows PC Processor: Supply Chain Checks and Key Takeaways

▌Supply chain checks point to around 10M shipments of N1X-based devices over the next two years.

➡ Still a niche market, aimed at power users who need on-device AI compute.

➡ Whether shipments get revised up will come down to price, but mainly to whether Windows can deliver apps and workflows that truly orchestrate on-device AI compute.

▌Today, the main ways people use AI on a PC (both Windows and Mac) are accessing cloud LLM services through a browser and calling LLMs via API to consume a cloud provider's compute / tokens:

➡ In both cases, the core AI compute happens in the cloud, not on the device.

▌So far in 2026, the two hottest stories in the PC market have had almost nothing to do with on-device AI compute:

➡ Strong MacBook Neo sales. My industry checks suggest 2026 shipments of Neo models were revised up by roughly 100% (5M → 10M). Buyers are paying for price, design, and ecosystem, not for on-device AI compute.

➡ Cheap mini PCs, still niche, are drawing a lot of attention because they can run AI agents (like OpenClaw) around the clock (e.g., Mac mini). These agents also run inference in the cloud.

➡ Bottom line: neither the sales nor the buzz has much to do with on-device AI compute.

▌The key to on-device AI driving an upgrade cycle is the operating system (OS):

➡ What really sets on-device AI apart from the cloud is its ability to deeply integrate a user's data and workflows across apps while keeping things private. But that needs OS support.

➡ AI in today's PC OS is still mostly about adding AI features to first-party apps and loosely connecting workflows across apps.

➡ Some apps already make good use of on-device AI compute, like speech-to-text, but not enough to drive meaningful upgrade demand.

▌The N1X devices could give AI power users another solid option:

➡ Thanks to the N1X, device makers can strike a better new balance across AI compute, memory, design, and portability.

➡ For power users running LLMs on-device, an N1X device is a solid alternative to the Mac when it comes to capable on-device AI compute and large memory.

➡ But if the goal is a real upgrade cycle, then beyond price, OS support (Windows) is still what matters.

34

80

525

315,256

May 31

許多人期待、Nvidia 可能將要發布的 N1X / Windows PC 處理器,供應鏈調查與重點分析:

▌供應鏈調查顯示,配備 N1X 的裝置未來兩年出貨量約10M

➡ 仍屬利基市場,瞄準對裝置端 AI 算力有需求的重度使用者。

➡ 未來出貨能否上修,除售價因素,還是取決於 Windows 能否提供真正調度裝置端 AI 算力的應用與工作流。

▌目前 PC(Windows 與 Mac)的主流 AI 應用為「用瀏覽器上 LLM 網站」與「透過 API 消耗雲端 LLM 的算力 / token」:

➡ 核心都是使用雲端 AI 算力,非裝置端。

▌2026 年 目前為止 PC 產業的兩個熱門事件,都與裝置端 AI 算力幾乎無關:

➡ MacBook Neo 的熱賣。我的產業調查顯示,2026 年該機種出貨量顯著調升約 100% (5M → 10M)。消費者買的是「低價 設計 生態」,不是買裝置端 AI 算力。

➡ 便宜的小 PC 主機雖仍屬利基市場,但因能長時間掛機跑 AI agent(如OpenClaw)而受到高度關注(如 Mac mini)。這類 agent 的推論算力幾乎也來自雲端。

➡ 小結:無論銷量(裡子)或話題(面子),都與裝置端 AI 算力幾乎無關。

▌裝置端 AI 推動升級換機潮的關鍵為作業系統:

➡ 裝置端 AI 與雲端最大差異,在於兼顧隱私下,能高度整合跨應用程式的用戶資料與工作流,然這需作業系統支援。

➡ 目前 PC 作業系統 AI 化主要仍處於「為本家應用程式增加 AI 功能」與「輕度整合跨應用程式的工作流」。

➡ 已有善用裝置端 AI 算力的應用,如語音轉錄文字,但不足以推動顯著升級換機需求。

▌N1X 裝置可望提供 AI 重度使用者另一個好選擇:

➡ 受益於 N1X,裝置設計能在 AI 算力、記憶體、外觀與攜帶性之間,取得一個更好的新平衡點。

➡ 對在本地端跑 LLM 的重度使用者而言,在不錯的裝置端 AI 算力與大容量記憶體裝置的選擇上,N1X 裝置是除了 Mac 以外的另一個好選擇。

➡ 若欲帶動顯著升級換機潮,除售價外,作業系統(Windows)支援仍是關鍵。

75

73

599

281,864

May 29

▌The latest supply chain checks indicate that Sunny Optical is seeing several new positive trends:

1. Leveraging its existing optical technology strengths, the company is preparing to enter AI server CPO / silicon photonics coupling components.

2. Securing orders for optical components in OpenAI's devices.

3. Two positive Apple order trends: 1) becoming a new Apple CCM supplier, with iPhone CCM orders expected in 2028; 2) winning the high-ASP variable aperture lens for the 2H26 new iPhones, with a order share approaching 50%.

▌Preparing to enter AI server CPO / silicon photonics coupling components:

1. Has already planned and is preparing to ship samples of CPO / silicon photonics coupling components, including collimating lenses, microlens arrays, and optical path redirection elements (micro-prisms, metalenses, etc.).

2. The company has decided to actively pursue its AI server business through strategic investments and M&A.

▌OpenAI device optical components order:

Sunny has secured NPI projects for optical components used in OpenAI’s smartphone and another pocket / mobile device.

▌Positive Apple order trends:

1. Sunny has become a new Apple CCM supplier, producing the MacBook Neo CCM. MacBook Neo shipments have come in better than expected, with the 2026 shipment forecast raised from 5 million to 10 million units.

2. The 2028 iPhone's ultra-wide CCM is expected to drop flip-chip in favor of an improved COB version, and Sunny Optical is well positioned to become a supplier.

3. For the 2H26 new iPhone 18 Pro/Pro Max, the variable aperture lens carries a 50% higher ASP (vs. the high-end 7P lens), with Sunny's supply share reaching 40–50%.

44

41

352

220,909

May 29

▌最新的供應鏈調查顯示,舜宇光學迎來數個新正向趨勢:

1. 利用既有光學技術優勢,準備進入 AI 伺服器 CPO / 矽光(硅光)耦合元件

2. OpenAI 裝置光學零組件訂單

3. 兩個 Apple 訂單正向趨勢:1) 成為 Apple 新 CCM 供應商,並預計在 2028 年取得 iPhone CCM訂單、2) 取得用於 2H26 新款 iPhone 的高單價可變光圈鏡頭,比重近50%

▌準備進入 AI 伺服器 CPO / 矽光(硅光)耦合元件:

1. 已規劃並準備送樣 CPO/矽光(硅光)耦合元件,包括準直透鏡、微透鏡陣列、光路轉向元件(micro-prism 微稜鏡、metalens 等)。

2. 公司已決定將積極透過轉投資與併購推進 AI 伺服器事業。

▌OpenAI 裝置光學零組件訂單:

取得 OpenAI 手機與另一口袋 / 移動裝置的光學零組件 NPI

▌Apple 訂單正向趨勢:

1. 成為 Apple 新 CCM 供應商,生產 MacBook Neo CCM。MacBook Neo 出貨優於預期,2026 年出貨量從 500 萬提升至 1,000 萬。

2. 2028 年 iPhone 的超廣角 CCM 預計捨棄 Flipchip 改用 COB 改良版,舜宇光學可望成為供應商。

3. 2H26 新款 iPhone 18 Pro/Pro Max 可變光圈鏡頭單價提升 50% (vs. 高階 7P 鏡頭),舜宇供應比重達 40-50%。

59

32

262

47,749

May 5

【Industry Check Update】OpenAI appears to be fast-tracking its first AI agent phone, with mass production targeted as early as 1H27. Potential drivers include supporting a year-end IPO narrative and intensifying competition in AI agent phones. MediaTek currently appears better positioned to become the sole processor supplier, with the device set to use a customized version of the Dimensity 9600, built on TSMC’s N2P node in 2H26. The ISP is the headline spec, with an enhanced HDR pipeline improving real-world visual sensing. Other key specs include a dual-NPU architecture for heterogeneous AI compute, LPDDR6 UFS 5.0 to ease memory bottlenecks, and pKVM inline hashing for security. If development stays on track, combined 2027–2028 shipments could reach around 30 million units.

42

75

431

465,296

May 5

【產業調查更新】OpenAI 可能正加速首款 AI agent 手機開發,目標最快於 1H27 量產,考量原因或包括有利年底 IPO 敘事、AI agent 手機競爭加速等。目前聯發科更有可能獨家取得處理器訂單,該機預計採用基於天璣 9600 的客製版本,並於 2H26 由台積電 N2P 生產。ISP 強化高動態範圍輸出,有利真實世界視覺感知,故為規格焦點;其他關鍵規格包括雙NPU架構(AI 算力分層)、LPDDR6 UFS 5.0(緩解記憶體瓶頸)、pKVM inline hashing(安全性)等。若開發順利,預計 2027 與 2028 年共出貨約 3,000 萬支。

28

40

339

145,709