350 Photos and videos

Pinned Tweet

Jun 12

$INFQ Here’s the honest place I think we are after this week.

A couple weeks ago, quantum was playing offense. Right now, we’re playing defense.

That has very little to do with whether the underlying INFQ thesis has improved or weakened. It has almost everything to do with the macro environment suddenly becoming much more hostile toward pre-profit, high beta, long-duration stocks.

The May jobs report was a genuine blowout. Payrolls increased by 172,000 versus expectations near 85,000, prior months were revised higher, and unemployment held at 4.3%.

That is excellent news for the economy.

But the bond market heard something very different:

The economy may be too strong for rate cuts.

Inflation may remain sticky.

The Fed may have to hold rates higher for longer, and the possibility of another hike cannot be completely dismissed.

The 10-year Treasury immediately jumped to roughly 4.54%.

That is the real gravity currently sitting on stocks like INFQ.

When investors can earn close to 4.5% in a Treasury, the market becomes much less generous when valuing companies whose largest earnings may still be years away. That does not mean the company is bad. It means the discount rate being applied to its future has gone up.

Then Iran reignited and oil/inflation risk returned, which added another reason to reduce speculative exposure.

The peace optimism this week removed some of that immediate geopolitical fear and brought money back into the broader market, but it did not completely reverse the damage done by the jobs report and bond market.

That is why the Dow can rally hundreds of points while quantum, small-cap mining, and other high-beta names barely participate.

Not every market rally is a high-beta rally.

Sometimes investors are simply buying profitable, liquid, large-cap companies again while leaving speculative exposure behind.

I also don’t believe the SpaceX IPO is the main explanation.

It probably absorbed an enormous amount of attention, speculative capital, and institutional risk budget for a few days. But quantum had already been aggressively de-risked before SpaceX began trading.

SpaceX may have temporarily taken oxygen out of the room.

The jobs report and bond market were what changed the room.

So are we stuck waiting for a recession before Treasury yields come down?

Not necessarily.

The 10-year can fall without the economy collapsing.

A durable Iran agreement could reduce oil and inflation pressure. Cooler CPI/PPI readings could restore confidence in disinflation. The Fed could adopt less hawkish guidance, slow balance-sheet runoff, or communicate that hikes are unlikely. Better Treasury-auction demand, reduced long-term issuance pressure, or credible progress on deficits could also lower the term premium.

2

4

28

2,406

Mason retweeted

The biolab story have always been a great tell for who is actually against the deep state and who isn't

Notice the exact same people who were behind the Wuhan lab coverup are attacking anyone who discusses the biolabs

Great litmus test

122

931

4,982

64,564

Mason retweeted

Thank you, @DNIGabbard, for exposing U.S. funded biolabs around the world. The American people deserve the truth.

Jun 12

Today, I’m releasing never before seen intelligence revealing new evidence of past US government funding for more than 120 biolabs in over 30 countries, including Ukraine.

In support of President Trump‘s Executive Order to end federal funding of dangerous gain of function research around the world, and increase transparency and accountability, ODNI will continue working with partners across the Administration to identify where these labs are, what pathogens they contain, and what “research” is being conducted.

odni.gov/index.php/newsroom/…

1,797

11,236

51,478

750,830

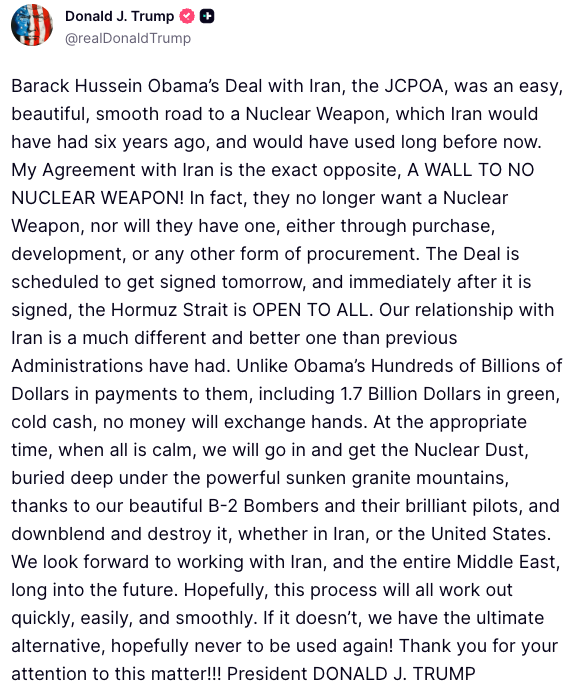

BREAKING: Trump says a deal with Iran is scheduled to be signed tomorrow.

“Immediately after it is signed, the Hormuz Strait is OPEN TO ALL.”

The president says the agreement will permanently prevent Iran from obtaining a nuclear weapon and described it as the exact opposite of the Obama-era nuclear deal.

Trump also said no money will exchange hands under the agreement and warned that if the process falls apart, the U.S. has “the ultimate alternative.”

3,068

3,312

14,271

883,368

Jun 12

Final trades!

Here's what @timseymour @michael_khouw @karenfinerman and @grassosteve are trading.

$XLE $ALB $NVDA $INFQ

cnbc.com/video/2026/06/12/fi…

10

1,253

Mason retweeted

Jun 12

This is why they came for Tulsi so hard

72

257

5,111

50,166

Mason retweeted

Jun 12

So in other words, the Biden administration, the MSM, entities within our government, and powerful NGOs, were all lying, and I was right.

191

699

7,055

100,081

Mason retweeted

Jun 12

Today, I’m releasing never before seen intelligence revealing new evidence of past US government funding for more than 120 biolabs in over 30 countries, including Ukraine.

In support of President Trump‘s Executive Order to end federal funding of dangerous gain of function research around the world, and increase transparency and accountability, ODNI will continue working with partners across the Administration to identify where these labs are, what pathogens they contain, and what “research” is being conducted.

odni.gov/index.php/newsroom/…

13,006

69,168

231,995

17,213,480

Mason retweeted

538

2,568

14,958

2,164,671

🚀🚀🚀🚀🚀🚀🚀🚀🚀🚀🚀🚀🚀

Jun 12

J.P. Morgan SpaceX= Largest IPO

Congratulations to the @spaceX team on this milestone, we were proud to serve as a lead bookrunner on the transaction.

5,984

14,715

152,058

14,577,124

Mason retweeted

Jun 12

J.P. Morgan SpaceX= Largest IPO

Congratulations to the @spaceX team on this milestone, we were proud to serve as a lead bookrunner on the transaction.

627

1,673

14,503

14,940,278

Mason retweeted

Jun 12

That’s too categorical. $INFQ ’s Sqywire/Quantum Spectrum platform is specifically built to detect, locate and classify RF signals in contested environments, and it has already been tested with Army EW systems.

Tiqker also explicitly lists hypersonic missile tracking, “radar beamforming”/tracking and fire control as applications.

That doesn’t mean INFQ itself is firing interceptors or currently calculating the intercept point. But its sensing and timing products absolutely can sit inside the detection, tracking and fire control chain that enables missile defense.

1

2

9

626

Jun 12

$INFQ Here’s the honest place I think we are after this week.

A couple weeks ago, quantum was playing offense. Right now, we’re playing defense.

That has very little to do with whether the underlying INFQ thesis has improved or weakened. It has almost everything to do with the macro environment suddenly becoming much more hostile toward pre-profit, high beta, long-duration stocks.

The May jobs report was a genuine blowout. Payrolls increased by 172,000 versus expectations near 85,000, prior months were revised higher, and unemployment held at 4.3%.

That is excellent news for the economy.

But the bond market heard something very different:

The economy may be too strong for rate cuts.

Inflation may remain sticky.

The Fed may have to hold rates higher for longer, and the possibility of another hike cannot be completely dismissed.

The 10-year Treasury immediately jumped to roughly 4.54%.

That is the real gravity currently sitting on stocks like INFQ.

When investors can earn close to 4.5% in a Treasury, the market becomes much less generous when valuing companies whose largest earnings may still be years away. That does not mean the company is bad. It means the discount rate being applied to its future has gone up.

Then Iran reignited and oil/inflation risk returned, which added another reason to reduce speculative exposure.

The peace optimism this week removed some of that immediate geopolitical fear and brought money back into the broader market, but it did not completely reverse the damage done by the jobs report and bond market.

That is why the Dow can rally hundreds of points while quantum, small-cap mining, and other high-beta names barely participate.

Not every market rally is a high-beta rally.

Sometimes investors are simply buying profitable, liquid, large-cap companies again while leaving speculative exposure behind.

I also don’t believe the SpaceX IPO is the main explanation.

It probably absorbed an enormous amount of attention, speculative capital, and institutional risk budget for a few days. But quantum had already been aggressively de-risked before SpaceX began trading.

SpaceX may have temporarily taken oxygen out of the room.

The jobs report and bond market were what changed the room.

So are we stuck waiting for a recession before Treasury yields come down?

Not necessarily.

The 10-year can fall without the economy collapsing.

A durable Iran agreement could reduce oil and inflation pressure. Cooler CPI/PPI readings could restore confidence in disinflation. The Fed could adopt less hawkish guidance, slow balance-sheet runoff, or communicate that hikes are unlikely. Better Treasury-auction demand, reduced long-term issuance pressure, or credible progress on deficits could also lower the term premium.

2

4

28

2,406

Jun 12

We don’t necessarily need bad economic news.

We need the market to believe inflation can fall without another tightening cycle.

Until that happens, however, high-beta stocks will probably remain extremely sensitive to every inflation number, employment report, oil move, and Fed statement.

There are a few catalysts capable of creating an exception specifically for quantum.

The biggest is the National Quantum Initiative reauthorization.

Both the Senate Commerce Committee and House Science Committee have advanced versions of the legislation. The proposals go far beyond simply funding more quantum-computing research. They emphasize real-world applications, quantum sensing, testbeds, domestic manufacturing, NASA programs, supply chains, workforce development, and commercialization.

That breadth fits Infleqtion unusually well.

INFQ is not solely waiting for a fault-tolerant computer.

It has neutral-atom compute, optical clocks, inertial sensing, RF sensing, software, defense programs, NASA work, and government relationships across several parts of the quantum infrastructure stack.

A full reauthorization could tell the market that federal quantum support is not a temporary science experiment. It is becoming a sustained national industrial and national-security policy.

That could absolutely reignite the entire quantum basket and temporarily override some of the macro pressure.

But there is an important distinction:

Authorization creates the programs.

Appropriations provide the money.

Named contracts and task orders determine which companies actually benefit.

The bill passing would be bullish for the sector narrative.

Actual funding and named awards would be much more powerful and durable for INFQ.

1

1

552

Jun 12

Then we have the $19–$20 area.

After two separate trips toward that zone followed by full round trips back into the low teens, I think we have to be realistic: $19–$20 is probably serious resistance now.

It isn’t some mystical technical number.

It represents overhead supply.

People who bought near the highs are waiting to get back to even. Traders who watched gains disappear twice may sell the next return. Investors who no longer trust the stock to hold a breakout may take profits earlier.

A press release could push INFQ back toward $19.

Holding above $20 will require enough new demand to absorb all of that selling.

What could realistically do it?

The reauthorization bill passing, especially if followed by appropriations or a directly relevant program.

The proposed $100M CHIPS funding moving from a conditional LOI toward a definitive agreement with clear milestones.

A meaningful prime contract or task order where INFQ is not simply eligible to compete, but is actually selected and funded to deliver.

A strong quarter with revenue acceleration, raised guidance, and evidence that cash burn is improving relative to growth.

A commercial deployment or production order for Tiqker, Quantum Spectrum, sensing, or software that demonstrates movement beyond prototypes and research programs.

A major hyperscaler, defense-prime, telecom, or infrastructure relationship with identifiable economics.

Broader analyst coverage and institutional sponsorship that begins replacing short-term momentum traders with investors willing to hold through volatility.

Progress updates on RF sensing, neutral atoms, and software are all important to the thesis.

But we should be honest: another technically impressive announcement without a customer, deployment, meaningful contract value, or revenue attached may not be enough by itself to permanently clear $20 in this environment.

That doesn’t make the work irrelevant.

It means the market’s burden of proof has risen.

I have not changed my long-term INFQ thesis.

I have changed my short-term expectations for how easily the market will reward it.

Quantum is not playing offense with unlimited liquidity right now. Macro gravity is real, yields near 4.5% are real, and the stock has to repair technical damage created by two failed moves near $20.

The reauthorization bill could put the sector back on offense.

A major direct award could create its own gravity.

Falling yields could reopen the speculative-growth trade.

The strongest outcome would be some combination of all three.

Until then, $19–$20 should probably be treated as resistance, not automatically assumed to be the beginning of the next breakout.

INFQ has already proven it can rally there.

Now it has to prove it can stay there.

2

12

1,448